Market Overview: Surface Durability Is Becoming A Design and Cost-Control Lever Across Mobility, Devices, and Built Environments

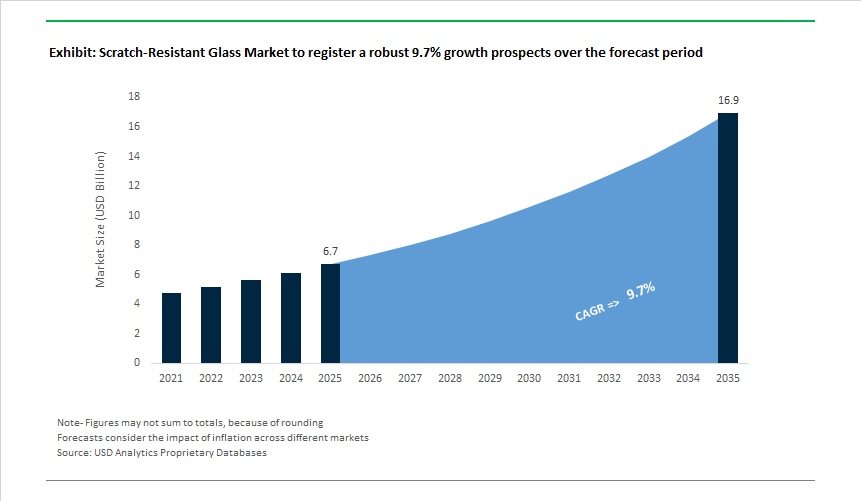

The Scratch-Resistant Glass Market is valued at USD 6.7 billion in 2025 and is projected to reach USD 16.9 billion by 2035, expanding at a 9.7% CAGR as glass surfaces evolve from passive protection layers into critical user-interface and lifetime-performance components. Growth is not simply volume-driven; it is anchored in how durability, optical clarity, and long-term appearance directly influence brand perception, warranty exposure, and replacement cycles for OEMs and infrastructure owners.

In e-mobility, the proliferation of large-format cockpit displays, head-up displays, and panoramic glass roofs has fundamentally changed the economics of glazing. Scratches, haze, or surface wear on interior and exterior glass now translate into high replacement costs and customer dissatisfaction, particularly in premium EV platforms where glass surfaces dominate the cabin experience. As a result, automotive OEMs increasingly specify chemically strengthened and coated glass systems that maintain surface hardness and optical performance under repeated touch, cleaning, UV exposure, and thermal cycling. Here, scratch resistance is not a cosmetic upgrade-it is a total cost of ownership (TCO) control mechanism across multi-year vehicle lifecycles.

Consumer electronics remain a second structural demand pillar, but the value capture logic is shifting. Smartphones, tablets, wearables, and laptops compete on perceived durability as much as on processing power or display resolution. Incremental gains in scratch resistance materially reduce screen replacement rates and after-sales service costs while supporting thinner and lighter device designs. For premium handset makers, advanced glass formulations and surface treatments function as brand differentiators, locking suppliers into long qualification cycles once a durability-performance threshold is met.

Beyond mobility and devices, industrial, architectural, and outdoor digital infrastructure applications are expanding the addressable market. Public-facing displays, smart building façades, kiosks, and control panels operate in abrasive, high-contact environments where surface degradation directly affects readability and asset lifespan. In these use cases, scratch-resistant glass supports longer maintenance intervals and lower lifecycle costs, making performance under real-world wear more important than initial material price.

From a competitive standpoint, advantage is increasingly defined by process integration and speed-to-specification. Scalable chemical strengthening, thin-glass handling, and advanced surface engineering-such as nanostructured coatings and plasma-enhanced deposition techniques-allow suppliers to tailor hardness, anti-glare behavior, and optical purity for specific OEM requirements. Vertical integration across float glass production, strengthening, coating, and lamination shortens development cycles and improves yield control, which is critical as automotive and electronics customers push for rapid platform refreshes.

Recent Industry Shifts - Product Launches, Capacity and Manufacturing Advances

The market shifted decisively during 2025 as manufacturers moved from incremental material improvements to strategic capacity and technology plays. In December 2025, the U.S. Department of Energy funded a research consortium to develop ultra-thin, high-strength flexible glass for foldables and wearables, underscoring the R&D priority of combining scratch resistance with bending endurance. In October 2025 SCHOTT AG strengthened its technology stack by acquiring QSIL GmbH Quarzschmelze Ilmenau, expanding specialty quartz and semiconductor-grade glass capabilities that feed into high-precision scratch-resistant and packaging glass. Also in October 2025, a major smartphone OEM shipped a flagship device using an updated aluminosilicate cover that claims 2× improvement in scratch resistance over the previous generation - resetting durability expectations across the mobile segment.

Capacity and vertical integration moves reinforced supply reliability and automotive focus: Asahi India Glass (AIS) commissioned its third float plant in August 2025 to secure automotive-grade flat glass feedstock, and Corning reported a 12% YoY core sales increase in Q2 2025 driven by demand for high-performance display glass in mobile and automotive platforms. Sustainability and cross-market tech transfer were evident in May 2025 when Saint-Gobain integrated its low-carbon ORAÉ glass into façade products-creating a requirement to pair those substrates with durable scratch-resistant coatings. Earlier in March 2025, Corning commercialised a Solar Market-Access Platform whose advanced handling and precision techniques are being repurposed for specialty display glass, while January 2025 advances in PECVD-applied super-hard carbon thin films signalled a near-term route to sapphire-level scratch resistance for premium wearables and rugged devices.

Scratch-Resistant Glass Market Trends and Opportunities

Trend 1: Ultra-Thin, Chemically Strengthened Glass for Multi-Fold Consumer Devices

Foldable and emerging tri-fold device architectures are pushing scratch-resistant glass into an unprecedented mechanical regime, where thicknesses below 100 microns must coexist with high surface hardness and fatigue resistance. Unlike early foldables that relied heavily on polymer overlays, 2025-generation devices are returning to glass-dominant stacks to restore premium tactile feel and long-term scratch resistance.

In December 2025, Samsung unveiled its first tri-fold smartphone with a 10-inch class display measuring 3.9 mm at its thinnest point, underscoring how aggressively OEMs are reducing glass thickness while increasing fold count. These devices employ ultra-thin glass (UTG) integrated with reinforced overcoats, engineered to survive both inward and outward folding without surface micro-fracture propagation—a failure mode that plagued early UTG generations.

The durability trade-off between scratch resistance and drop survival is also being recalibrated. Corning’s latest chemically strengthened aluminosilicate platforms have demonstrated the ability to survive 1-meter drops onto concrete-simulated rough surfaces, while maintaining a scratch resistance threshold roughly 4× higher than conventional competitors. This balance is critical for “glass sandwich” designs where both front and rear surfaces are exposed to abrasion.

Material innovation is extending beyond ion exchange. Glass-ceramic hybrids introduced in 2025 leverage high-density nanocrystal dispersion to inhibit crack initiation and lateral propagation. These substrates allow slimmer device profiles while significantly reducing the formation of micro-scratches caused by dust-borne silica—now recognized as one of the dominant real-world wear mechanisms in consumer devices.

Trend 2: Anti-Glare and Anti-Fingerprint Automotive Interior Glass

Vehicle interiors are rapidly transforming into high-brightness digital environments, with display surface area per vehicle increasing 40–50% in EV platforms compared to ICE predecessors. This shift is elevating scratch-resistant glass from a cosmetic element to a safety-critical optical component, particularly as screens extend from center stack to full dashboard width.

At IAA Mobility 2025, AGC Automotive showcased large-format, curved interior glass using p-polarized thin-glass structures designed for pillar-to-pillar displays. These solutions combine chemical strengthening with dry-coated anti-glare (AG) and anti-fingerprint (AF) layers, enabling consistent haptics and visibility across complex geometries.

Brightness targets are escalating. Modern automotive HMIs are now specified above 1,500 nits to maintain readability in direct sunlight. To prevent glare without introducing image “sparkle,” etched AG glass with tightly controlled surface roughness is being deployed. However, yield remains a constraint—complex curved AG automotive glass still averages ~65% usable yield, making process control and defect reduction a central competitive differentiator.

Durability requirements are also expanding. Automotive interior glass must now tolerate –40°C to 105°C thermal cycling, repeated chemical cleaning, and constant touch interaction. Advanced nano-coatings applied in 2025 provide scratch resistance alongside oleophobic and self-cleaning functionality, preventing long-term haze and clouding that degrade display legibility over a vehicle’s service life.

Opportunity 1: Scratch-Resistant Cover Glass with Anti-Soiling Functionality for Solar Panels

The rapid expansion of solar capacity in high-dust, high-irradiance regions is creating a distinct opportunity for scratch-resistant glass engineered for permanent surface cleanliness. Mechanical cleaning remains one of the leading causes of optical degradation in solar installations, making abrasion-resistant, anti-soiling cover glass strategically important.

In May 2025, India imposed a five-year anti-dumping duty on imported solar glass, triggering a localization push. Domestic manufacturers such as Borosil Renewables reactivated expansion programs, targeting 1,850 TPD capacity (~12 GW equivalent) by 2026. This policy environment favors value-added glass with integrated scratch-resistant and anti-soiling coatings rather than commodity float glass.

Regulatory specifications increasingly mandate ≥90.5% light transmission alongside textured, toughened surfaces. Permanently bonded hydrophobic and photocatalytic coatings are gaining traction because they reduce abrasive cleaning frequency, preserving both transmission efficiency and surface integrity over decades of operation.

Technology spillover from space applications is also emerging. In late 2025, SCHOTT introduced radiation-resistant solar glass for satellite constellations, highlighting coating strategies that maintain optical stability under extreme UV exposure—capabilities increasingly relevant for high-altitude and desert-based terrestrial solar projects.

Opportunity 2: High-Hardness Glass Windows for Industrial and Medical HMIs

The acceleration of Industry 4.0 is driving demand for scratch-resistant glass in industrial touchscreens that must operate reliably in abrasive, corrosive, and high-cleanliness environments. Unlike consumer devices, industrial HMIs face continuous exposure to dust, chemicals, and repetitive mechanical contact.

Industrial systems introduced in 2025 increasingly specify deeply chemically strengthened glass or sapphire-grade substrates to prevent deep gouges that can compromise structural integrity. Enhanced ion-exchange processes are producing thicker compressive stress layers, significantly improving resistance to the kind of localized scratches that act as crack initiation sites under vibration or pressure.

Zero-defect manufacturing is becoming non-negotiable. To support pharmaceutical, food processing, and hazardous-area installations, manufacturers such as SCHOTT have deployed real-time quality systems capable of analyzing over 100,000 data points per minute during production. This level of control ensures that microscopic flaws—often invisible at installation but catastrophic over time—are eliminated.

As industrial automation expands into harsher environments, scratch-resistant glass is evolving from a protective layer into a reliability-defining component, directly influencing uptime, safety compliance, and total cost of ownership.

Market Share Analysis: Scratch-Resistant Glass Market

Market Share by Product Type: Chemically Strengthened Lithium-Aluminosilicate Glass Sets the Durability Benchmark

Chemically strengthened glass holds around 65% share of the Scratch-Resistant Glass Market because it delivers the most commercially scalable balance between scratch hardness, drop survivability, optical performance, and manufacturability—a combination sapphire and tempered glass still fail to match at volume. The dominance of lithium-aluminosilicate (LAS) and emerging glass-ceramic hybrids is rooted in the ion-exchange strengthening process, which creates deep compressive stress layers without increasing thickness or brittleness. In 2025, leading platforms such as Corning’s Gorilla® Armor 2 and Victus® 2 have reset industry expectations by demonstrating 4× higher scratch resistance versus standard aluminosilicate glass, with Knoop scratch thresholds of 8–10 Newtons, compared to 2–4 Newtons for legacy solutions. This performance leap is not cosmetic; it directly reduces warranty claims and refurbishment losses for OEMs operating at smartphone shipment scales exceeding hundreds of millions of units annually. Equally critical is survivability under real-world abuse—lithium-based strengthened glass now shows up to 10× higher survival rates in concrete drop tests while maintaining Vickers hardness above 660 kgf/mm², proving that scratch resistance is no longer achieved at the expense of impact toughness. The segment’s share is further reinforced by optical innovation: anti-reflective surface engineering delivering up to 75% reflection reduction has turned glass from a passive cover into an active display-performance enabler, making chemically strengthened glass the default specification for premium and upper-midrange devices in 2025.

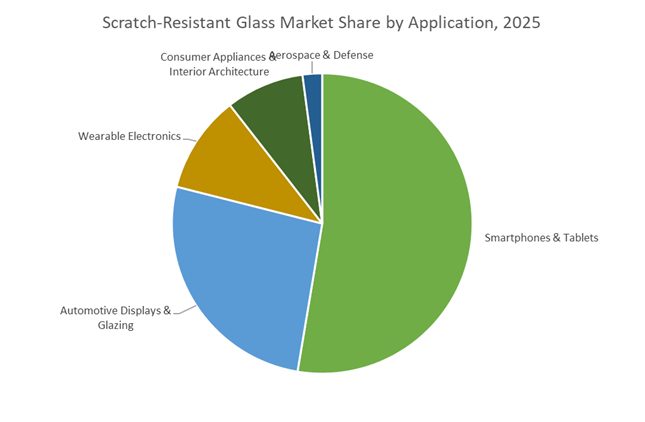

Market Share by Application: Smartphones and Tablets Drive High-Volume Adoption of Premium Glass Technologies

Smartphones and tablets account for approximately 50% of total scratch-resistant glass demand, acting as both the volume engine and the innovation testbed for next-generation glass technologies. This dominance is structurally linked to shifting consumer behavior: device replacement cycles have extended to 3–5 years, forcing OEMs to prioritize long-term cosmetic durability alongside drop protection. As a result, flagship smartphones have established new mechanical benchmarks—2025 launches now specify 2.2-meter drop survival onto concrete-like surfaces, more than doubling the effective requirement seen two product cycles earlier. Consumer research reinforces this pull; large-scale surveys consistently rank scratch resistance as the #1 durability concern, on par with impact resistance, making smartphones uniquely demanding compared to wearables, automotive displays, or architectural glazing. At the same time, aggressive industrial design trends—foldables, curved edges, and ultra-thin form factors—have intensified reliance on chemically strengthened glass sheets in the 0.4 mm to 1.2 mm thickness range, a performance window that competing materials cannot reliably support at scale. Sustainability considerations are also reshaping procurement: lead-, arsenic-, and antimony-free manufacturing has become a baseline requirement for Tier-1 OEMs aligning with ESG targets, favoring established glass suppliers with mature, compliant supply chains. Together, high shipment volumes, escalating durability expectations, and rapid design evolution ensure that smartphones and tablets remain the single largest and most influential application shaping market share dynamics in the scratch-resistant glass market.

Competitive Snapshot - Strategy, Capability and Product Positioning Of Leading Suppliers

Market leadership clusters around companies that combine chemically strengthened glass know-how, coating technologies, large-scale float integration and sustainability credentials. These firms are expanding vertically and investing in advanced coatings and low-carbon processes to win automotive, mobile and architectural specifications.

Corning Incorporated - The Benchmark in Chemically Strengthened Display Glass

Corning remains the global standard for chemically strengthened aluminosilicate cover glass (Gorilla Glass), with placement in billions of devices and growing traction in automotive display surfaces and interior glazing. Its Q2 2025 results (12% core sales growth) reflect successful expansion into automotive and high-performance displays. Corning is commercialising advanced handling and wafer-level techniques (Solar Market-Access Platform, Mar 2025) that accelerate transferability of precision processing to specialty display glass. Strategy focuses on higher “Corning content” per device - thin, strong glass plus coating systems - to capture more downstream value in mobile, wearables and EV cockpit surfaces.

AGC Inc. (Asahi Glass) - Scaled Float Capacity and Automotive Glazing Leadership

AGC (Dragontrail™) couples global float manufacturing scale with chemical strengthening expertise to serve both consumer electronics and large automotive glazing applications. The commissioning of a third float plant in Soniyana (Aug 2025) strengthens vertical integration and supply security for automotive OEMs. AGC emphasises laminated door glass, illuminated sunroofs and high-clarity panels, leveraging chemical strengthening and coating compatibility to meet demanding scratch-resistant and optical specs across mobility and industrial displays.

SCHOTT AG - Specialty Optical Glass, Precision Wafers and Sustainable Melting Innovation

SCHOTT’s acquisition of QSIL (Oct 2025) and its €450 million capex posture underpin leadership in specialty quartz and precision glass for optics and semiconductor packaging with clear synergies for high-precision display substrates. SCHOTT demonstrated large-scale hydrogen melting in 2024-an industry-leading low-carbon production method-while continuing to advance low TTV and ultra-high clarity glass used in LiDAR, radar covers and premium displays that require durable, scratch-resistant coatings.

Nippon Sheet Glass (NSG) / Pilkington - Thin-Film Coatings and Multi-Function Automotive Glazing

NSG/Pilkington offers a broad portfolio of chemically strengthened, laminated and coated glass solutions focused on impact resistance and thermal stability for automotive and architectural markets. Its thin-film coating technologies (solar control, thermal coatings) combine with scratch resistance to produce multifunctional glazing solutions for windshields, cockpit windows and façades where visual clarity and scratch durability are critical for safety and performance.

Saint-Gobain - Low-Carbon Architectural Glazing With A Durability Specification Requirement

Saint-Gobain’s ORAÉ low-carbon glass (integrated May 2025) positions the company at the interSection of sustainability and high-performance façades. Its COOL-LITE® XTREME solar control and fire-resistant (safety) ranges demand robust exterior scratch-resistant coatings to preserve lifetime performance. Saint-Gobain also invests in digital tools (Calumen live) to help specifiers model durability and scratch performance, making product data a commercial differentiator for long-life architectural and façade projects.

The United States has reasserted leadership in scratch-resistant cover glass manufacturing by anchoring high-volume, high-spec production onshore. The pivotal inflection point arrived in August 2025, when Apple and Corning Incorporated announced a $2.5 billion expansion at Harrodsburg, Kentucky, enabling 100% U.S.-manufactured cover glass for all iPhone and Apple Watch models sold globally. This move elevates the U.S. from partial supplier to sole-source hub for premium aluminosilicate and lithium-aluminosilicate glass, materially de-risking global supply chains amid rising display sovereignty policies.

Operationally, the Kentucky site now hosts the world’s most advanced smartphone glass lines, optimized for Ceramic Shield and the Gorilla® Glass Ceramic portfolio—delivering higher drop performance without sacrificing scratch resistance. Importantly, the reshoring strategy also creates semiconductor adjacency: under CHIPS and Science Act frameworks, Corning is extending its glass know-how into silicon-on-glass wafers for advanced packaging customers, tightening the linkage between protective glass, interposers, and next-gen chip manufacturing.

China: Dual-Release Compliance and Ultra-Thin Glass (UTG) Industrialization

China’s 2025 posture marks a transition from volume processing to high-end material governance, particularly for ultra-thin glass (UTG) used in foldables and advanced touch interfaces. In December 2025, the Ministry of Industry and Information Technology (MIIT) updated its Industrial Policy Catalogue, explicitly prioritizing UTG for touch panels and advanced packaging equipment—unlocking targeted incentives for thickness control, ion-exchange strengthening, and yield optimization.

Quality governance intensified with NMPA reforms: the 2025 GMP issued in November 2025 mandates stricter data traceability for Class III high-risk materials, extending compliance expectations to medical-grade touch and diagnostic glass. Sustainability also advanced; December 2025 saw China’s first ISO 14021 PCR Glass Certification for a Zhanjiang facility, formalizing post-consumer recycled (PCR) content as a viable input for technical glass—an important cost and ESG lever as UTG volumes scale.

South Korea: AI-Era Glass-Ceramics and Foundry-Level Integration

South Korea is converging scratch-resistant glass, AI hardware, and automotive displays into a single value proposition. Early 2025 product launches—most notably Gorilla® Armor 2 and Gorilla® Glass Ceramic 2 on flagship smartphones—introduced anti-reflective glass-ceramics that cut glare by ~75% while maintaining top-tier scratch resistance, accelerating adoption in bright-ambient and cockpit environments.

At the ecosystem level, the Ministry of Trade, Industry and Energy committed ₩4.5 trillion ($3.06 billion) in December 2025 to a public-private foundry program that includes glass-based interposers for HBM and AI chip cooling. Manufacturing execution has improved materially: AI-assisted binning deployed across 2025 cut defect rates in chemically strengthened glass by ~66%, reinforcing Korea’s case for foundry-grade glass substrates.

Japan: GX 2040 Decarbonization and Green High-Strength Glass

Japan’s GX 2040 Vision, approved January 18, 2025, positions the country as the global benchmark for low-carbon, high-strength glass. Subsidies favor hydrogen-assisted kilns and energy-efficient melting for specialty products such as Dragontrail™, aligning durability gains with lifecycle emissions reduction.

Execution leadership comes from AGC Inc., which continues to scale Dragontrail™ via a float process that eliminates arsenic and antimony, pre-empting EU ESPR requirements. Under Japan’s 7th Strategic Energy Plan (Feb 2025), incentives also target lightweight automotive glazing to extend EV range while enabling large AR-HUDs, expanding the addressable market for scratch-resistant glass beyond handheld devices.

Germany: Space-Grade Cover Glass and Semiconductor Packaging Precision

Germany remains Europe’s nucleus for specialty scratch-resistant glass in space and semiconductors. In November 2025, SCHOTT AG launched exos, a cerium-doped cover glass for next-gen satellite solar cells, developed with European Space Agency funding. The material delivers exceptional radiation tolerance and thermal stability (CTE ≈ 6.9×10⁻⁶ K⁻¹), extending mission lifetimes.

Strategically, SCHOTT’s early-2025 acquisition of QSIL GmbH deepens high-purity quartz capabilities for semiconductor packaging. The company’s Semicon Taiwan 2025 showcase of glass carrier wafers for 3D IC and wafer thinning underscores Germany’s role in enabling the angstrom-era precision demanded by advanced nodes.

India: SEMICON India Momentum and PLI-Driven Display Localization

India is accelerating display and cover glass localization through unprecedented incentive deployment. At SEMICON India 2025 (September), the government confirmed that ~₹65,000 crore ($7.8 billion) of the ₹76,000 crore PLI outlay for semiconductors and displays has been committed, catalyzing downstream demand for scratch-resistant cover glass.

New display fab clusters in Gujarat and Uttar Pradesh are pulling in LED chip packaging and light-management ecosystems, reducing import dependence for mobile and automotive glass. The inauguration of 3-nm chip design facilities (May 2025) further tightens the linkage between domestic electronics design and high-end optical/protective glass, setting up sustained pull-through into 2026–2028.

2025 Strategic Matrix: Scratch-Resistant Glass Development

Scratch-Resistant Glass Development Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Material Focus

|

|

United States

|

Supply chain reshoring

|

$2.5B Apple–Corning Kentucky expansion

|

Ceramic Shield; Gorilla® Glass

|

|

China

|

Ultra-thin substrates & compliance

|

MIIT Industrial Policy Catalogue update

|

UTG; PCR technical glass

|

|

South Korea

|

AI & foundry synergy

|

₩4.5T public-private foundry program

|

Glass interposers; Armor 2

|

|

Japan

|

Decarbonization (GX 2040)

|

GX 2040 Cabinet approval

|

Dragontrail™; eco-glazing

|

|

Germany

|

Space & semiconductor packaging

|

Launch of SCHOTT exos (ESA-funded)

|

Cerium-doped glass; quartz

|

|

India

|

Display fabs (PLI)

|

₹65k Cr PLI commitments realized

|

Cover glass; LED substrates

|

Scratch-Resistant Glass Market Report Scope

Scratch-Resistant Glass Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.7 Billion

|

|

Market Size (2035)

|

$16.9 Billion

|

|

Market Growth Rate

|

9.7%

|

|

Segments

|

By Product Type (Chemically Strengthened Glass, Glass-Ceramic Composites, Sapphire Glass, Scratch-Resistant Coated Glass), By Strengthening Process (Ion-Exchange Method, Thermal Tempering, Thin-Film Deposition), By Application (Smartphones & Tablets, Automotive Displays & Glazing, Wearable Electronics, Consumer Appliances, Interior Architecture, Aerospace & Defense)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Corning Incorporated, AGC Inc., SCHOTT AG, Nippon Electric Glass Co. Ltd., Saint-Gobain S.A., Nippon Sheet Glass Co. Ltd., Guardian Industries, Kyocera Corporation, JNTC Co. Ltd., Xinyi Glass Holdings Limited, Crystalwise Technology Inc., Swiss Jewel Company, Rubicon Technology Inc., Monocrystal, Heraeus Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Scratch-Resistant Glass Market Segmentation

By Product Type

- Chemically Strengthened Glass

- Glass-Ceramic Composites

- Sapphire Glass

- Scratch-Resistant Coated Glass

By Strengthening Process

- Ion-Exchange Method

- Thermal Tempering

- Thin-Film Deposition

By Application

- Smartphones & Tablets

- Automotive Displays & Glazing

- Wearable Electronics

- Consumer Appliances

- Interior Architecture

- Aerospace & Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Scratch-Resistant Glass Market

- Corning Incorporated

- AGC Inc

- SCHOTT AG

- Nippon Electric Glass Co., Ltd.

- Saint-Gobain S.A.

- Nippon Sheet Glass Co., Ltd.

- Guardian Industries

- Kyocera Corporation

- JNTC Co., Ltd.

- Xinyi Glass Holdings Limited

- Crystalwise Technology Inc.

- Swiss Jewel Company

- Rubicon Technology, Inc.

- Monocrystal

- Heraeus Group

*- List not Exhaustive