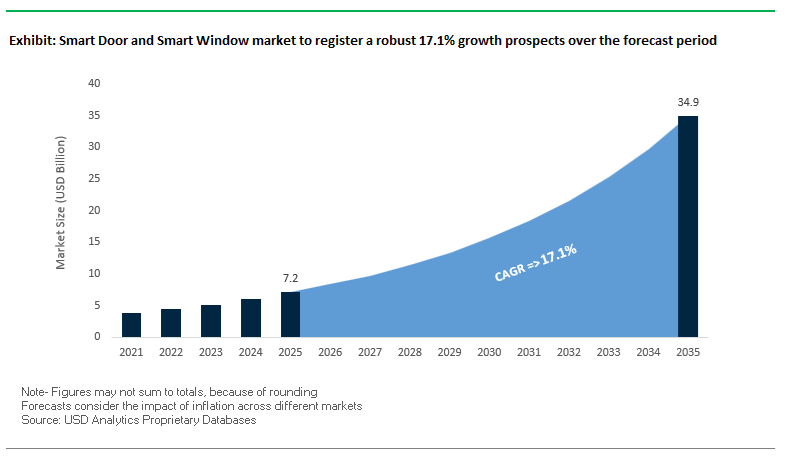

The Smart Door and Smart Window market is set to grow from USD 7.2 billion in 2025 to USD 34.9 billion by 2035, registering an impressive CAGR of 17.1% (2025–2035). The growth is anchored in dynamic glazing technologies—electrochromic (EC), Suspended Particle Device (SPD), and emerging thermochromic systems—that enable real-time control of solar heat gain, visible light, glare, and privacy in both building façades and smart vehicle cabins. In particular, smart doors and smart windows are evolving into core elements of high-performance building envelopes and intelligent mobility platforms, rather than niche architectural upgrades.

- Deep SHGC modulation for NZEB design: Electrochromic smart windows can reduce Solar Heat Gain Coefficient (SHGC) from about 0.47 (clear) to as low as 0.09 (fully tinted), enabling up to 80% reduction in unwanted solar heat gain—critical for Net Zero Energy Building (NZEB) strategies and HVAC downsizing.

- Wide VLT range for visual comfort and privacy: Dynamic glazing in smart doors and smart windows can shift from 55–70% visible light transmittance (VLT) in a clear state to 1–2% VLT in a dark state, offering tight glare control, occupant comfort, and on-demand privacy in offices, luxury homes, and smart vehicle cabins.

- Ultra-low power consumption during tinting: EC glass for smart façades typically requires only 2.5 W/m² during transition and almost no power to maintain tint, meaning a 200 m² façade draws power comparable to a single 60 W bulb while switching—demonstrating that operating costs are negligible relative to HVAC savings.

- Real-time SPD switching for transportation glazing: SPD smart glass achieves 1–2 second switching regardless of glass size, making it uniquely suited for EV panoramic roofs, aircraft windows, and premium automotive smart doors, where instant glare and heat management is a safety and comfort advantage.

- System-level energy savings via IoT/BMS integration: When smart windows are integrated with BMS and IoT predictive control algorithms, dynamic glazing systems can deliver up to 28% better energy performance versus conventional smart glass baselines, proving their value as active components in smart building and smart mobility ecosystems.

The Smart Door and Smart Window market is entering a scale-up phase, driven by both manufacturing capacity expansions and new high-value applications in EVs, premium real estate, and aircraft. In November 2025, industry data on tier-one producers including Kinestral (Halio) and Guardian indicated that global smart glass manufacturing capacity is expected to rise to around 12.5 million m² by 2028, up from just 2.8 million m² in 2024. The more than fourfold capacity increase underscores strong confidence in dynamic glazing penetration in commercial buildings, smart homes, and transportation cabins, especially as energy codes tighten and developers target LEED, WELL, and NZEB certification. Further, industry forecasts from December 2024 point to polymer and organic electrochromic materials becoming the second-largest segment in EC glass by 2035, enabling faster switching and lower fabrication cost, which is essential for mid-market smart window adoption.

On the automotive and mobility side, SPD smart glass is rapidly becoming a flagship technology for smart roofs and glazing in EVs and luxury vehicles, directly influencing the smart door and smart window ecosystem. In July 2025, Gauzy and Research Frontiers announced the first customer deliveries of General Motors’ Cadillac CELESTIQ, featuring the industry’s largest multi-zone SPD dimmable roof, designed to manage light and heat on a zonal basis for each occupant. The same month, performance data for the SPD roof indicated the ability to block up to 95% of infrared (IR) radiation, helping to reduce HVAC energy consumption in the EV by up to 40%—a compelling metric for OEMs focused on range extension and cabin comfort. Earlier, in May 2025, Research Frontiers reported Q1 2025 royalty revenues of USD 560,000, a 79% year-over-year increase, with growth driven mainly by new SPD-SmartGlass automotive models. The evidence confirms that transportation applications are a core volume driver for dynamic glazing, with direct spillovers into smart doors and integrated side glazing systems.

At the building scale, the market is being reshaped by retrofit solutions and new material classes that expand the addressable installed base. In October 2025, Research Frontiers and AIT Group launched a retrofit SPD-SmartGlass system at GlassBuild, explicitly targeting existing façades—a crucial strategic step because most global building stock is already built and cannot be easily replaced. In parallel, academic and industrial research on thermochromic hydrogel smart windows has accelerated; as of September 2025, hydrogel-based smart window materials already accounted for approximately 24.9% of the thermochromic material market, with published results showing VLT up to 87% and switching times as low as five seconds. The drives the future where multi-technology smart window portfolios—combining EC, SPD, PDLC, and hydrogel thermochromics—will be tailored by application, from low-power passive thermochromics in residential smart windows to fast-switching SPD systems in mobility and aviation.

Trend 1: Electrochromic Glazing Becomes a Mandatory Component of Net-Zero Energy Building (NZEB) Architecture

Electrochromic (EC) smart glass is rapidly transitioning from an optional performance upgrade to a baseline requirement in Net-Zero Energy Building (NZEB) designs, where dynamic solar heat management is essential for meeting aggressive energy reduction targets. Building simulations across North American climates consistently show that EC glazing significantly reduces peak cooling demand-with performance gains quantified at 0.46–0.65 W/ft² versus static low-e options. Full-scale testbeds further validate a 25%–58% reduction in peak cooling loads compared to spectrally selective low-e glazing, establishing EC windows as a high-impact tool for energy optimization.

The extreme reduction in solar heat gain-up to 88.9%-also enables substantial HVAC downsizing, a major capital cost advantage for architects and developers pursuing NZEB certification. Notably, annual energy savings of 6–30 kWh/ft² have been reported in cooling-dominated climate zones, equating to as much as 40% lower total cooling and lighting energy consumption across commercial buildings.

Government incentives are further accelerating adoption. The U.S. Department of Energy (DOE) highlights that EC glazing now qualifies under IRA-driven Section 48 and Section 179D tax credits, making electrochromic windows a financially justified choice for large-scale commercial developments targeting net-zero performance metrics.

Trend 2: PDLC Smart Windows Become Mission-Critical for On-Demand Privacy and Infection Control in Healthcare & Offices

Polymer-Dispersed Liquid Crystal (PDLC) technology is gaining widespread adoption across hospitals, commercial offices, and collaborative workspaces requiring instant, hygienic privacy solutions. Unlike mechanical blinds or fabric curtains, PDLC smart windows switch between transparent and opaque states within milliseconds, enabling real-time privacy for operating rooms, MRI suites, or emergency examination zones.

The hygienic advantage is enormous: by eliminating fabric, PDLC windows significantly reduce contamination risk and simplify infection-control compliance-an increasingly critical requirement in healthcare facility upgrades. The laminated structure also delivers superior acoustic dampening, improving patient comfort and enhancing confidentiality for clinical consultations or corporate meetings.

Long-term durability is a central value driver. PDLC systems often exceed 100,000 operating hours, delivering multi-decade performance with minimal maintenance-an attractive specification for hospitals and high-occupancy commercial buildings where lifecycle cost optimization is a priority.

Opportunity 1: Solar-Powered, Self-Tinting Smart Glass for Automotive Sunroofs and EV Thermal Management

The automotive industry-especially the EV sector-is a major emerging market for next-generation smart windows. Solar-control smart glazing technologies (including SPD, PDLC, and photochromic layers) can block up to 86% of infrared (IR) radiation, dramatically reducing cabin heat and lowering air-conditioning load. This is particularly valuable for EVs, where HVAC energy consumption directly reduces driving range.

Key application drivers include:

- Up to 99% UV protection, extending interior material lifespan and enhancing passenger comfort

- Elimination of mechanical sunshades, freeing headroom and reducing system weight

- Minimal operating power, especially advantageous for EV energy efficiency

- Development of self-powered glass, where integrated photovoltaic (PV) films generate the switching energy required for dynamic tinting

This opportunity aligns with broader automotive goals to reduce component mass, eliminate mechanical complexity, and enhance energy efficiency across all vehicle classes.

Opportunity 2: Transparent Conductive Heater Films for Advanced De-icing, De-fogging, and ADAS Clarity

Integrating transparent conductive heaters into smart windows is a high-value opportunity for the automotive, aerospace, and transportation sectors, where visibility and safety are mission-critical.

Breakthroughs in heater film technology include:

- Ice melting performance: Advanced multilayer transparent heaters demonstrate the ability to melt 30 mm of ice in ~110 seconds, while maintaining 88% visible transmittance and a figure of merit up to 759

- Wire-free transparency using CNT or Ag-nanowire heaters, ensuring zero optical distortion-critical for ADAS cameras and LIDAR sensors

- Up to 40% lower energy consumption compared to conventional wire-based heaters, aligning with EV efficiency requirements

- Automotive-grade reliability, including compliance with the demanding 85°C/85% RH for 2,000 hours qualification test

This positions transparent heater films as a multi-functional upgrade that enhances defogging, de-icing, safety, and sensor clarity while integrating seamlessly into next-generation smart glazing architectures.

Smart Door and Smart Window Market Share Analysis

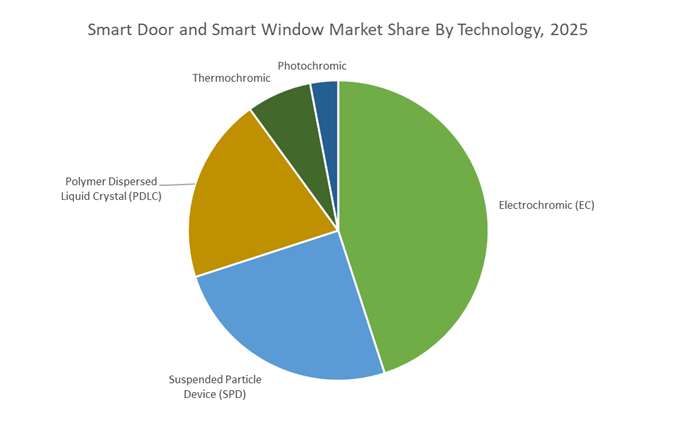

Market Share by Technology: Electrochromic Solutions Lead Through Superior Solar Heat Management, Energy Efficiency, and View-Preserving Transparency

Electrochromic (EC) technology commands the dominant 45% share of the Smart Door and Smart Window Market, driven by its unmatched capability to dynamically control both light transmission and solar heat gain while maintaining optical transparency—an essential combination for energy-efficient building design. Unlike alternative smart glazing technologies such as PDLC, which merely switch between clear and opaque states, EC glass transitions smoothly between clear and tinted modes, enabling continuous modulation of glare, daylight levels, and thermal load without obstructing views. This performance advantage is particularly important for commercial buildings where preserving visual connection to the outdoors supports occupant comfort and wellness. EC glass delivers exceptional solar heat gain coefficient (SHGC) control, with fully tinted states capable of reducing incoming solar heat by over 90%, dramatically lowering cooling demand in high-solar-exposure environments. This ability to reduce HVAC loads contributes to whole-building energy savings of 20% to 30%, as validated by smart building case studies that integrate EC glazing into automated lighting and climate systems. Its scalability across façades, skylights, and high-performance envelopes, combined with its compatibility with modern IoT-based building management platforms, ensures that electrochromic glazing remains the most technologically advanced and commercially favored smart window solution, securing its leading market share position.

Market Share by End-Use Industry: Construction and Architectural Applications Dominate Through Code Compliance, HVAC Optimization, and Green Building Adoption

The Construction and Architectural sector holds a commanding 65% share of the Smart Door and Smart Window Market, driven by the global shift toward high-performance building envelopes, stringent energy-efficiency regulations, and widespread adoption of green building certifications. Smart glazing—particularly electrochromic windows—is now integral to achieving compliance with modern building standards such as LEED, BREEAM, and national energy codes, all of which prioritize reduced energy consumption, daylight optimization, and minimized peak HVAC demand. EC glass plays a strategic role in enabling architects to design highly glazed façades that meet strict thermal performance criteria without compromising aesthetics or natural light access. By significantly reducing solar heat gain, EC systems allow mechanical engineers to downsize HVAC capacity, often reducing equipment tonnage and delivering meaningful CapEx savings that offset the cost premium of dynamic glazing technologies. This value proposition aligns directly with the financial and environmental priorities of developers, especially in large commercial projects, airports, hospitals, educational facilities, and premium residential towers.

Moreover, regulatory momentum—such as Europe’s Energy Performance of Buildings Directive (EPBD) and increasingly aggressive building codes across North America and Asia—is accelerating the adoption of smart window systems as a practical pathway to meeting low-SHGC and net-zero-energy design targets. As urbanization and climate-resilient infrastructure initiatives expand globally, the Construction/Architectural segment’s demand for smart glazing materials continues to grow, solidifying its position as the dominant market driver within the smart door and smart window ecosystem.

Country Analysis: Global Smart Glass Development Hubs

United States – Commercial Real Estate Electrification and Regulatory Momentum Accelerating Electrochromic Smart Window Adoption

The United States remains the leading global hub for Smart Door and Smart Window technology, supported by its advanced commercial real estate sector, robust venture capital ecosystems, and strong regulatory frameworks promoting energy efficiency. A major catalyst for the market is the country’s aggressive shift toward dynamic glazing solutions, driven by LEED-oriented building designs and state-level mandates that require quantifiable reductions in building energy consumption. SageGlass, one of the largest electrochromic glass manufacturers globally, continues to spearhead deployment across high-value commercial and institutional buildings. In 2024, its retrofit installation at a major U.S. university delivered a documented 10% reduction in energy consumption, illustrating the ROI potential that is accelerating adoption across the corporate and public-sector real estate portfolios.

U.S. innovation leadership is further reinforced by the 2025 launch of SageGlass RealTone™, a next-generation electrochromic product engineered to deliver the most neutral tint currently available in the market. This responds directly to architectural demand for natural aesthetics while still delivering advanced solar control performance. Parallel to commercial real estate, the U.S. Department of Energy (DoE) continues to play an instrumental role through grant funding, technical partnerships, and long-term innovation roadmaps aimed at scaling durable, fast-switching electrochromic technologies. Meanwhile, the automotive industry is emerging as a high-growth segment, exemplified by Rivian’s 2024 adoption of electrochromic sunroofs that improve EV cabin thermal management by 10%. This cross-industry integration cements the U.S. as a critical hub for both infrastructure-scale and transportation-scale smart glazing advancement.

Europe (Germany/France) – Zero-Energy Building Compliance and Automotive OEM Integration Driving Large-Scale Smart Window Penetration

Europe’s Smart Door and Smart Window Market is propelled by some of the world’s most stringent sustainability mandates, particularly those arising from the Energy Performance of Buildings Directive (EPBD). As European countries progress toward near Zero Energy Buildings (nZEB), smart glazing becomes an essential component in achieving regulated Solar Heat Gain Coefficient (SHGC) thresholds and HVAC efficiency improvements. This regulatory pressure is directly translating into rising demand for electrochromic glazing and Suspended Particle Devices (SPD), especially in commercial buildings, premium office spaces, and public infrastructure.

European Tier-1 automotive suppliers, including AGC Automotive and Saint-Gobain, have significantly advanced the commercialization of smart automotive glazing, supplying SPD and electrochromic panels for panoramic roofs, side windows, and shading systems in luxury EV platforms. Europe’s smart glazing footprint also extends into aviation, where Airbus continues to specify dynamic glazing for passenger comfort and glare management—maintaining a thriving, high-value aerospace segment. Architectural adoption remains strong, with SageGlass installations exceeding 1,500 globally, including landmark European projects such as Belgium’s Office Greisch. Europe’s integrated automotive, aerospace, and commercial building value chains position the region as one of the most mature markets for high-performance dynamic glazing.

India – Self-Powered Smart Glass Innovation and World-Leading Commercial Deployments Transforming Market Adoption

India is rapidly emerging as a major growth engine in the global Smart Door and Smart Window Market, propelled by unprecedented commercial construction activity and breakthrough indigenous R&D aimed at reducing system costs and improving long-term operational efficiency. A notable scientific advancement was achieved by the Centre for Nano and Soft Matter Sciences (CeNS) with DST support: the development of a Redox Potential-Based Self-Powered Electrochromic (RP-SPEC) device, which eliminates the need for external electrical power. This innovation significantly enhances energy independence and reduces lifecycle operating costs—two critical barriers in large-scale smart window adoption.

CeNS has also achieved cost reductions by eliminating expensive ITO-based counter electrodes and adopting an Al³⁺-based electrolyte instead of lithium, paving the way for scalable, domestically manufactured smart glazing technologies. India is not only progressing technologically but also demonstrating the world’s largest commercial smart glass deployment. SageGlass was selected for the Rio Business Park in Bangalore, with more than 200,000 sq ft of electrochromic glass installed—now recognized as the largest single smart glass installation globally. This establishes India as both an innovation hub and a global-scale deployment market, particularly for commercial buildings, IT parks, and green-certified infrastructure.

Israel – Global Center for SPD/PDLC Film Manufacturing and Automotive-Ready Smart Glass Integration

Israel plays a foundational role in the global Smart Door and Smart Window Market due to its leadership in Suspended Particle Device (SPD) and Polymer Dispersed Liquid Crystal (PDLC) film manufacturing. The country’s flagship player, Gauzy Ltd., is the world’s only company producing both PDLC and SPD films, positioning Israel as a critical Tier-1 supplier to automotive OEMs, building façade suppliers, and architectural glazing fabricators worldwide. This vertically integrated capability ensures faster customization, shorter lead times, and the ability to support both lamination and retrofit smart glass applications.

In July 2025, Gauzy launched the world’s first prefabricated automotive smart glass stack, designed to meet OEM-level industrialization requirements and reduce complexity for vehicle manufacturers adopting switchable glass technologies. This innovation accelerates the integration of smart glazing into EV and premium vehicle platforms. Additionally, Gauzy’s $12 million capital expansion initiative—announced in late 2025—aims to scale PDLC/SPD film production and expand market penetration across Europe, North America, and Asia. Israel’s contributions are thus pivotal not only from a materials manufacturing perspective but also from the standpoint of automotive-grade reliability, industrial scalability, and global technology diffusion.

Competitive Landscape: Leading Smart Glass Players Shaping Smart Door and Smart Window Systems

The Smart Door and Smart Window market is dominated by a mix of IP licensors, dynamic glazing manufacturers, and integrated building solution providers. Competitive differentiation is increasingly based on switching speed, energy performance, control software, and integration with BMS/vehicle ECUs, rather than simply glass production capacity. Below is an overview of how the major players position themselves within the smart door and smart window ecosystem.

Research Frontiers is the inventor and global licensor of Suspended Particle Device (SPD) SmartGlass technology, monetizing the smart door and smart window opportunity primarily through royalty income on SPD films and finished glazing products. The company’s technology is engineered to block up to 99.5% of visible light and around 95% of IR radiation, making it highly attractive for vehicle roofs, aircraft windows, and premium smart doors where instant privacy and thermal comfort are key buying criteria. In Q1 2025, the company recorded a 79% year-on-year increase in royalty revenue to USD 560,000, driven largely by the adoption of SPD-SmartGlass in new automotive models. Strategically, Research Frontiers is focusing on high-end transportation platforms and premium architecture, where its 1–2 second switching speed is a clear differentiator versus slower electrochromic solutions, and where OEMs are willing to pay for performance-led dynamic glazing.

View, Inc. is widely recognized as a pioneer of electrochromic (EC) smart glass for architectural applications, positioning its products as central components of smart, connected building platforms. Its dynamic glazing units are integrated with AI- and machine learning-based control systems that can predict sunlight patterns, optimize SHGC in real time, and reduce glare automatically, thereby improving both energy performance and occupant comfort. Large-scale deployments of View Smart Glass have been engineered to deliver up to 26% reduction in cooling energy use compared with conventional high-performance glazing, a compelling metric for property developers and corporate real estate owners. The firm’s strategic vision is to position smart windows not just as building components, but as sensor-rich endpoints in IoT ecosystems, enabling data-driven services around comfort, productivity, and wellness in offices, healthcare, and education buildings.

Through its SageGlass brand, Saint-Gobain leverages decades of experience in low-E coatings and façade engineering to offer electrochromic smart glass solutions targeted at large commercial buildings, airports, and institutional projects. Recent product lines launched for the European market emphasize aesthetic flexibility (tint shades, zoning options) and compatibility with sustainable construction requirements, supporting developers seeking LEED and other green building certifications. SageGlass systems are designed to integrate seamlessly with major Building Management Systems (BMS) including Honeywell and Johnson Controls, enabling automated tint control based on solar position, occupancy, and HVAC strategy. The company’s competitive strength lies in its ability to bundle smart glazing with other Saint-Gobain building envelope products, presenting architects and contractors with a single, technically coherent façade package.

Gauzy is a leading manufacturer and processor of SPD and PDLC smart films, and serves as a key licensee and industrialization partner for Research Frontiers’ SPD technology. It plays a central role in transforming SPD film into ready-to-integrate smart door and smart window units for both automotive and architectural markets. A landmark achievement came in July 2025, when Gauzy and General Motors delivered the Cadillac CELESTIQ, featuring the industry’s largest multi-zone SPD dimmable roof, capable of significantly reducing cabin heat load and enabling up to 40% HVAC energy savings in the EV. Beyond luxury vehicles, Gauzy is scaling SPD film coating capacity to support high-volume OEM platforms, while also promoting PDLC-based privacy glass for conference rooms, hospital partitions, and premium residential doors. The dual-technology portfolio allows Gauzy to address both real-time tinting and instant privacy use cases across smart doors and smart windows.

Kinestral Technologies, through its Halio product line, focuses on electrochromic smart glass with a neutral gray tint, designed to preserve natural color rendering and exterior aesthetics for high-end buildings. The company emphasizes uniform tinting and natural-looking transitions across large glass panels, positioning its technology as a premium alternative to traditional blue-tinted tungsten-oxide EC systems. Industry capacity projections in November 2025 indicate that Halio, alongside other tier-one producers, is contributing to the ramp-up toward 12.5 million m² of smart glass manufacturing capacity by 2028, underscoring its commitment to scaling dynamic glazing for mainstream architectural adoption. Strategically, Kinestral targets luxury residential towers, premium commercial real estate, and signature projects, where architects demand unobstructed views, elegant façade design, and integrated shading performance without compromising on energy efficiency or occupant comfort.

Smart Door and Smart Window market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.2 Billion

|

|

Market Size (2035)

|

$34.9 Billion

|

|

Market Growth Rate

|

17.1%

|

|

Segments

|

By Technology (Electrochromic, Suspended Particle Device, Polymer Dispersed Liquid Crystal, Thermochromic, Photochromic), By Mechanism/Function (Dynamic Shading & Light Control, Privacy Control, Energy Harvesting, Glare Reduction, UV/IR Blocking), By Component/Form (Laminated Smart Glass, Adhesive Smart Film, Insulated Glass Units, Polymer Interlayers), By End-Use Industry (Construction & Architectural, Transportation, Consumer Electronics), By Control System (Building Automation Integration, Mobile-Based Control, Voice-Based Control, Autonomous/AI Control)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Saint-Gobain S.A. (SageGlass), AGC Inc., Gentex Corporation, Gauzy Ltd., Research Frontiers Inc., View Inc., Nippon Sheet Glass Co. Ltd., Polytronix Inc., Guardian Glass, Vitro Architectural Glass, Chromogenics AB, Smartglass International

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Smart Door and Smart Window Market Segmentation

By Technology

- Electrochromic (EC)

- Suspended Particle Device (SPD)

- Polymer Dispersed Liquid Crystal (PDLC)

- Thermochromic

- Photochromic

By Mechanism/Function

- Dynamic Shading/Light Control

- Privacy Control

- Energy Harvesting

- Glare Reduction

- UV/IR Blocking

By Component/Form

- Laminated Smart Glass

- Adhesive Smart Film/Retrofit Film

- Insulated Glass Units (IGUs)

- Polymer Interlayers (TPU/PVB)

By End-Use Industry

- Construction/Architectural

- Transportation

- Consumer Electronics

By Control System

- Building Automation Systems (BAS) Integration

- Mobile-Based App Control

- Voice-Based Control

- Autonomous/AI Control

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Smart Door and Smart Window Manufacturers

- Saint-Gobain S.A. / SageGlass

- AGC Inc.

- Gentex Corporation

- Gauzy Ltd.

- Research Frontiers Inc. / SPD Control Systems

- View, Inc.

- Nippon Sheet Glass Co. Ltd. (NSG Group)

- Polytronix, Inc.

- Guardian Glass (Koch Industries)

- Vitro Architectural Glass

- Chromogenics AB

- Smartglass International

*- List not Exhaustive