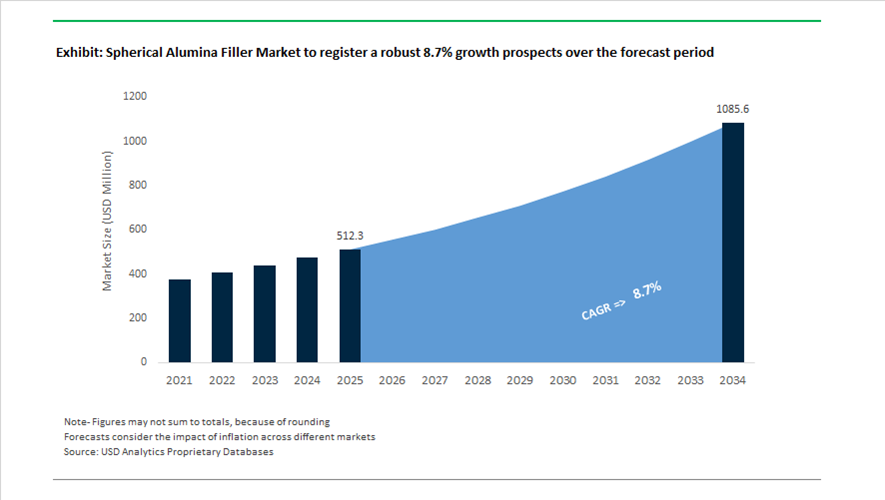

Spherical Alumina Filler Market Valuation 2025–2034: $512.3 Million to $1,085.4 Million at 8.7% CAGR Accelerated by AI Servers, EV Thermal Management, and 5G Materials Innovation

The global spherical alumina filler market is valued at $512.3 million in 2025 and is projected to reach $1,085.4 million by 2034, expanding at a robust CAGR of 8.7%. Growth is being driven by escalating demand for high-purity spherical alumina fillers in thermal interface materials (TIMs), semiconductor encapsulation compounds, epoxy molding compounds (EMCs), silicone potting systems, EV battery modules, and advanced communication devices. As AI data centers, HBM memory architectures, electric vehicles, and 5G and 6G infrastructure scale globally, manufacturers are prioritizing ultra-low impurity alumina, narrow particle size distribution, high thermal conductivity, and low dielectric constant materials. The market is transitioning toward AI-assisted quality control, low-alpha radiation grades, and regionally integrated electronics supply chains to meet stringent reliability standards.

Strategic capacity expansion intensified across Asia in 2024 and 2025. In July 2024, Shin-Etsu implemented a global price revision of 10% or more across silicone and alumina-filled specialty products, citing higher raw material and energy costs. In November 2024, PQ completed a major expansion of its specialty silica and alumina facility in Indonesia, positioning the site as a Southeast Asian hub for spherical alumina beads used in high-performance TIMs and electronic encapsulants. In late 2024, PPG finalized the divestiture of its silica and alumina filler business to Qemetica, reflecting ongoing portfolio realignment among coatings-focused manufacturers. In February 2025, Denka confirmed that expanded production lines for high-value inorganic fillers, including spherical alumina, will begin operations at its Omuta Plant in fiscal 2025 under its Mission 2030 strategy focused on advanced ICT materials. In May 2025, Wacker commissioned a new production site in Zhangjiagang, China, dedicated to specialty silicones and high-purity spherical alumina thermal fillers serving medical electronics and semiconductor packaging.

Product innovation and digital manufacturing upgrades are reshaping competitive dynamics. In February 2025, Denka launched SNECTON low-dielectric insulating materials engineered to function alongside spherical alumina fillers in high-frequency communication modules. Throughout 2025, Admatechs intensified R&D on Low-Alpha Ray Spherical Alumina grades critical for HBM3 and HBM4 memory chips used in AI servers, addressing soft-error risks in advanced semiconductor nodes. In late 2025, Dowa Electronics Materials reported rising demand for complex oxide powders based on alumina systems for next-generation solid-state battery electrolyte development. In December 2025, Resonac deployed a deep-learning AI inspection model at its Toyama Plant, improving spherical alumina particle inspection accuracy by 40% and reducing false detection rates to 3.2%, enhancing consistency in particle morphology and size distribution.

Strategic partnerships and regional expansion continue into 2026. Shin-Etsu’s Zhejiang specialty hub, announced in May 2024 and scheduled for completion in February 2026, will produce silicone-alumina emulsions and advanced fillers tailored for China’s EV and electronics manufacturing base. In early 2026, Solenis entered a multi-year agreement with Marathon Petroleum incorporating advanced specialty fillers for high-temperature refractory and insulation systems in refinery environments, signaling cross-industry expansion of spherical alumina applications beyond electronics. These capacity additions, AI-driven quality control advancements, semiconductor-grade material innovations, and energy transition applications are positioning the spherical alumina filler market for accelerated growth through 2034.

Technology-Led Trends and High-Value Opportunities in the Spherical Alumina Filler Market

Strategic Adoption as a Thermal Interface Material Filler for High-Density AI Server Racks

The Spherical Alumina Filler Market is undergoing a rapid upshift as artificial intelligence infrastructure moves toward extreme power density architectures. Next-generation AI platforms, including NVIDIA Blackwell systems, are driving rack-level power densities into the 120 kW to 140 kW range. At these thresholds, conventional Thermal Interface Materials fail to deliver the thermal conductivity, mechanical stability, and dispensing consistency required for continuous high-load operation. This has elevated spherical alumina fillers from a formulation option to a specification-grade requirement in advanced TIM systems.

By late 2025, thermal conductivity benchmarks moved decisively upward. In December 2025, Henkel introduced Bergquist TGF 10000, a liquid gap filler achieving 10 W/m·K. This performance level relies heavily on optimized spherical alumina particle packing, which enables high filler loading while preserving rheological stability during automated dispensing. As GPU power draw scales from 700 W toward 1,200 W per module, TIM formulations must resist pump-out caused by repeated thermal cycling. Spherical alumina morphology reduces internal friction and particle interlocking, allowing weight loadings above 75% without the exponential viscosity increase associated with angular calcined alumina. For hyperscale data centers, this translates directly into longer service intervals, lower failure rates, and predictable thermal performance across thousands of nodes.

Low-Alpha Qualification for 3D IC and Advanced Semiconductor Packaging

Advanced semiconductor packaging has become a second structural growth pillar for the spherical alumina filler market. As the industry transitions toward Fan-Out Wafer-Level Packaging and three-dimensional integrated circuits, fillers are no longer evaluated solely on thermal or mechanical performance. They are now assessed as reliability-critical materials with direct impact on silicon integrity. For High Bandwidth Memory and logic stacking, spherical alumina fillers must meet Ultra-Low Alpha emission thresholds to prevent soft errors and long-term data corruption.

In July 2024, Resonac Corporation launched the US-JOINT consortium in Silicon Valley to accelerate back-end semiconductor process innovation. Within this framework, spherical alumina fillers are being qualified for epoxy molding compounds that manage coefficient of thermal expansion mismatch in dense chiplet architectures. Leading foundries are now mandating alpha-particle emission rates below 0.002 counts per square centimeter per hour, effectively excluding conventional mineral fillers from advanced nodes. To meet these requirements, producers such as Admatechs are scaling high-purity spherical alumina and silica production. This shift positions spherical alumina not merely as a filler, but as a yield-protection material embedded directly into semiconductor qualification roadmaps.

High-Loading Thermally Conductive Adhesives for 800V EV Power Electronics

The global transition to 800-volt electric vehicle architectures and Silicon Carbide power electronics has created a high-margin opportunity for spherical alumina fillers in thermally conductive adhesives. Inverters and power modules now operate under aggressive thermal cycling conditions approaching 200 degrees Celsius, requiring materials that combine strong adhesion with stable heat dissipation. Spherical alumina enables these formulations by delivering high thermal conductivity at viscosities compatible with automated assembly lines.

Strategic capacity investments underscore this opportunity. Denka expanded its spherical alumina production capacity in Singapore by 30% to support environment and energy applications, with EV thermal management identified as a priority segment. By 2025, company disclosures confirmed that specialty alumina fillers had become a core growth driver for battery and power electronics systems. Product-level data from automotive-grade formulations such as DOWSIL TC-8225 demonstrate how spherical alumina enables thermal conductivities of 2.7 W/m·K while maintaining processable viscosities near 490 Pa·s. This balance allows Tier 1 suppliers to deploy high-speed meter-mix dispensing, reducing cycle times and improving yield consistency in large-scale EV manufacturing.

Ceramic Matrix Composites for Aerospace and High-Voltage Energy Systems

Beyond electronics and mobility, spherical alumina fillers are gaining traction in ceramic matrix composites for aerospace and high-voltage energy applications. These environments demand electrical insulation and thermal stability far beyond the limits of polymer-based systems. Alumina-filled composites are being specified for applications exceeding 500 degrees Celsius, where dielectric integrity and mechanical stability are mission-critical.

Research published in August 2025 on lightweight aerospace insulation systems highlights the integration of alumina-based nanostructures into ceramic fiber felts and tiles used in jet engines and satellite platforms. These composites deliver stable dielectric constants around 10.5 with minimal dielectric loss under extreme thermal stress. Parallel studies from early 2025 confirm that high-purity spherical alumina, typically above 99.6%, maintains electrical insulation resistance up to 28 teraohms. This makes it a preferred filler for high-voltage bushings, advanced grid components, and next-generation fusion and energy storage systems where insulation failure carries catastrophic risk. As aerospace and energy systems push further into high-temperature, high-voltage regimes, spherical alumina fillers are positioned as a foundational material enabling reliability, safety, and long-term system integrity.

Spherical Alumina Filler Market Share and Segmentation Insights

Medium Particle Size Spherical Alumina Leads the Market Through Optimal Thermal Conductivity and Processing Performance

Medium particle size spherical alumina accounted for 42.80% of the spherical alumina filler market in 2025, reflecting its strong adoption in high-performance thermal management materials. Typically ranging from 10 to 50 microns, this particle size range provides an optimal balance of thermal conductivity, packing density, and manageable viscosity in filled materials. It is widely used in thermal interface materials and electronic encapsulation compounds, where high filler loading is required without compromising processing efficiency. A key 2025 technology development is the growing use of bimodal particle size distributions, where medium particles create the primary thermal conduction network while ultrafine particles fill voids between larger particles, increasing packing density and improving overall heat transfer performance.

Thermal Interface Materials Drive Global Demand for Spherical Alumina Fillers

Thermal interface materials accounted for 38.60% of the spherical alumina filler market in 2025, making them the largest application segment across electronics thermal management systems. These materials include thermal greases, gap fillers, pads, and gels that transfer heat away from electronic components such as processors, power modules, and LED systems. Spherical alumina fillers provide high thermal conductivity while maintaining electrical insulation, which is critical for reliable device operation. A major 2025 demand driver is the rapid growth of high-power electronics used in electric vehicles, 5G infrastructure, and data centers, where increased power density requires improved thermal management solutions capable of achieving thermal conductivity levels exceeding 5 W/m·K.

Spherical Alumina Filler Market Competitive Landscape

The spherical alumina filler market in 2026 is defined by ultra-high purity, low sodium content, and engineered particle size distributions enabling >80% filler loading. Demand is accelerating in semiconductor packaging, EV thermal management, and high-performance TIMs, with innovation centered on sphericity, low-alpha materials, and multimodal filler systems.

Denka Leads High-Purity Spherical Alumina with Ultra-Fine Grades for AI Chips and EV Thermal Management

Denka continues to set the global benchmark in spherical alumina fillers through advanced melting technology and precision particle engineering. Its DAM and DAW series deliver near-perfect sphericity and ultra-low conductivity, with DAW-90 widely adopted in high-reliability power modules. The ASFP ultra-fine series (d50 down to 0.3 μm) is enabling next-generation HBM packaging and AI accelerator chip integration. Denka’s fillers are critical for EV battery thermal interface materials, improving heat dissipation and mechanical durability. Under its Mission 2030 Phase 2 strategy, the company is prioritizing ICT and healthcare-driven specialty materials. Integration with conductive additives like acetylene black is advancing hybrid filler systems for high-voltage EV applications.

Resonac Strengthens Semiconductor Packaging Ecosystem with High-Loading Spherical Alumina Fillers

Resonac is advancing its position in spherical alumina fillers by integrating materials development with semiconductor back-end processing capabilities. Its ALUNABEADS™ series delivers high purity and superior flowability, enabling high filler loading in epoxy molding compounds and potting resins. Through its Packaging Solution Center, Resonac validates alumina-filled materials using real semiconductor manufacturing conditions, accelerating commercialization cycles. The company’s end-to-end offering across packaging materials strengthens its competitive advantage in thermal management systems. It is expanding applications into silicon carbide (SiC) power modules for EVs, addressing high-voltage thermal challenges. The shift toward mobility and advanced electronics is reinforcing demand for its functional ceramic fillers.

Admatechs Dominates Low-Alpha Spherical Alumina for High-Density Memory and EV Thermal Applications

Admatechs is the global leader in low-alpha spherical alumina fillers, critical for preventing soft errors in advanced semiconductor devices. Its Admafine series, produced via VMC technology, ensures ultra-low radioactivity and high purity required for HBM3e and HBM4 memory. The company expanded sub-micron spherical alumina capacity in 2026 to meet rising demand from EV battery thermal management systems. Its narrow particle size distribution and high sphericity reduce equipment wear, improving efficiency for compounders. As a Toyota-linked joint venture, Admatechs benefits from deep integration with automotive electronics requirements. Its materials are increasingly used in ADAS systems and onboard chargers where thermal reliability is critical.

Sumitomo Chemical Expands High-Purity Alumina Portfolio for Semiconductor and Sustainable Materials Innovation

Sumitomo Chemical is strengthening its specialty alumina filler portfolio through strategic restructuring and innovation in ICT and mobility applications. The integration of its polyolefin business allows greater capital allocation toward high-purity alumina and semiconductor materials. Its recognition as a Clarivate Top 100 Global Innovator highlights advancements in alumina-based functional materials for displays and battery separators. The acquisition of a Taiwanese semiconductor chemicals company enhances its regional supply chain for IC packaging materials. Under the Sumika Sustainable Solutions program, the company is developing recycled-content alumina fillers to support carbon neutrality goals. Its focus on advanced materials positions it strongly in next-generation electronics and EV ecosystems.

Bestry Scales High-Volume Spherical Alumina Production for 5G Electronics and Automotive Thermal Adhesives

Bestry is emerging as a dominant supplier of spherical alumina fillers within China’s rapidly expanding electronics manufacturing ecosystem. With China accounting for approximately 72% of global production, Bestry plays a critical role in supplying thermally conductive materials. Its products are optimized for high filler loading in epoxy, silicone, and polyurethane systems, supporting 5G infrastructure and automotive electronics. The company’s fillers enhance thermal conductivity, reduce CTE, and improve mechanical strength in thermal conductive adhesives used in ECUs. In response to raw material cost inflation, Bestry is investing in vertical integration and advanced classification technologies. Its focus on low-sodium, high-uniformity grades is enabling expansion into global high-performance markets.

Japan: AI-Led Process Control and Semiconductor Back-End Specialization

Japan remains a global technology anchor for spherical alumina fillers, with market momentum driven by advanced semiconductor packaging, power electronics, and AI hardware demand. In late 2025, Resonac Corporation expanded its proprietary AI-based image analysis across spherical alumina production lines, compressing sphericity defect inspection from minutes to roughly 20 seconds. This capability materially improves lot-to-lot consistency for high-performance filler grades required in generative AI semiconductor packaging, where thermal conductivity and particle morphology directly influence yield and reliability.

Collaborative R&D further reinforces Japan’s leadership. Resonac’s US-JOINT program, launched in mid-2024 as an extension of its JOINT2 open consortium, brings together ten global partners to optimize spherical alumina for advanced back-end processes in Silicon Valley. Application pull is also strengthening. Denka Company Limited reported that spherical alumina is increasingly replacing spherical fused silica in high-voltage applications due to superior thermal conductivity, with particular relevance to thermal management of AI processing units. After a 2024 cyclical low, Japanese producers recorded a V-shaped recovery in H1 FY2025, supported by power infrastructure investments and AI-related hardware expansion.

United States: Trade Protection, Domestic Consolidation, and EV-Focused Formulations

The United States spherical alumina filler market is being reshaped by assertive trade policy, supply chain consolidation, and application-specific innovation for electrified mobility. On May 30, 2025, the U.S. administration announced plans to raise Section 232 tariffs on derivative aluminum articles, including alumina powders under HTS 2818.20, to 50% ad valorem. This measure intensifies incentives for domestic production scale-up and localization of specialty alumina supply.

Regulatory action continued with antidumping and countervailing duty investigations initiated by the U.S. Department of Commerce on January 7, 2025, targeting sol-gel and ceramic alumina-based grains from China. On the innovation front, Momentive Technologies commercialized its Boratherm™ SA powder line in 2025, leveraging narrow size distribution spherical alumina to deliver low-viscosity thermally conductive plastics for North American EV OEMs. Momentive’s acquisition of Sibelco’s spherical alumina assets across late 2024 and 2025 further consolidated U.S. supply for high-performance thermal interface materials.

China: Capacity Scale-Up, Battery Pull, and Export Friction

China’s spherical alumina filler market combines state-backed capacity expansion with strong domestic demand from batteries and electronics, while facing export volatility. Aluminum Corporation of China reported a fully integrated value chain expansion in 2025, prioritizing high-purity chemical alumina for semiconductors and structural ceramics. Between 2023 and early 2025, suppliers commissioned additional ultrafine powder throughput lines, adding an estimated 8,000 tons to global sub-micron spherical alumina capacity.

Demand composition is evolving rapidly. Battery leaders such as CATL specified sub-micron spherical alumina fillers in 2025 cathode modules and thermal interface layers to improve temperature uniformity in high-nickel chemistries. However, export channels tightened in 2025 due to prior informed consent requirements and new EU and U.S. tariff structures, contributing to a domestic spot market surplus by Q4 2025 despite high production levels.

Singapore: Capacity Uplift and Regional Export Orchestration

Singapore plays a pivotal role as a high-purity manufacturing and logistics hub for spherical alumina. Denka Advantech Pte. Ltd. operationalized a new production line at its Tuas facility during 2024–2025, lifting the company’s global spherical alumina capacity by approximately 30%. The city-state’s logistics efficiency and regulatory stability have reinforced its position as Denka’s primary export node for environment and energy sector materials, supplying semiconductor clusters in Taiwan and South Korea with consistent quality and lead times.

South Korea: Battery Module Integration and Supply Realignment

South Korea’s spherical alumina filler demand is tightly coupled with its battery manufacturing ecosystem and power electronics specialization. LG Energy Solution integrated advanced spherical alumina-filled potting compounds into 2025 high-voltage battery modules to mitigate moisture-induced degradation and enhance thermal pathways. On the supply side, Momentive Technologies’ 2025 acquisition of domestic spherical alumina businesses reshaped the local market toward specialized grades for xEV power electronics, emphasizing performance over commodity volumes.

India: Early-Stage Semiconductor Supply and Incentivized Purity Upgrades

India is emerging as a nascent but accelerating participant in the spherical alumina filler market, driven by semiconductor packaging ambitions and policy incentives. In 2024, CMP supplied 90 tons of spherical alumina to the domestic semiconductor packaging sector, marking a notable entry into high-tech filler supply chains. Policy tailwinds are building. Under 2025 green manufacturing updates, Indian alumina producers are evaluating plasma-melting routes to achieve ultra-high purity spherical grades exceeding 99.9%, targeting export qualification and integration into global electronics and EV supply networks.

Comparative Snapshot: Country-Level Strategic Drivers in the Spherical Alumina Filler Market

Spherical Alumina Filler Market County Level Snapshot

|

Country

|

Primary Driver

|

Core Application Pull

|

Structural Direction

|

|

Japan

|

AI-enabled quality control and consortium R&D

|

Advanced packaging, AI hardware

|

Precision grades and back-end specialization

|

|

United States

|

Tariffs and domestic consolidation

|

EV polymers, TIMs

|

Localization and trade-protected scale

|

|

China

|

Capacity expansion and battery demand

|

Batteries, semiconductors

|

Domestic absorption amid export friction

|

|

Singapore

|

Capacity uplift and logistics

|

Semiconductor materials

|

Regional export orchestration

|

|

South Korea

|

Battery integration

|

High-voltage modules

|

Application-specific specialization

|

|

India

|

Policy incentives and early semiconductor supply

|

Packaging materials

|

Purity upgrades and export orientation

|

Spherical Alumina Filler Market Report Scope

Spherical Alumina Filler Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$512.3 Million

|

|

Market Size (2034)

|

$1085.4 Million

|

|

Market Growth Rate

|

8.7%

|

|

Segments

|

By Particle Size (Ultrafine, Medium, Coarse, Specialty), By Application (Thermal Interface Materials, Encapsulation Materials, Thermally Conductive Plastics, Alumina Ceramic Filters, Thermal Spray and Abrasives), By End-User Industry (Automotive, Electronics, Aerospace and Defense, Industrial and Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Denka Company Limited, Resonac Corporation, Admatechs, Momentive Technologies, Sumitomo Chemical Co., Ltd., Nippon Steel Chemical & Materials, Bestry Performance Materials, Anhui Estone Materials Technology, Jiangsu Novoray New Material, Sibelco, CMP, Zibo Zhengze Aluminum, Dongkuk R&S, Bengbu Silicon-Based Materials, Showa Denko

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Spherical Alumina Filler Market Segmentation

By Particle Size

- Ultrafine

- Medium

- Coarse

- Specialty

By Application

- Thermal Interface Materials

- Encapsulation Materials

- Thermally Conductive Plastics

- Alumina Ceramic Filters

- Thermal Spray and Abrasives

By End-User Industry

- Automotive

- Electronics

- Aerospace and Defense

- Industrial and Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Spherical Alumina Filler Market

- Denka Company Limited

- Resonac Corporation

- Admatechs

- Momentive Technologies

- Sumitomo Chemical Co., Ltd.

- Nippon Steel Chemical & Materials

- Bestry Performance Materials

- Anhui Estone Materials Technology

- Jiangsu Novoray New Material

- Sibelco

- CMP

- Zibo Zhengze Aluminum

- Dongkuk R&S

- Bengbu Silicon-Based Materials

- Showa Denko

*- List not Exhaustive