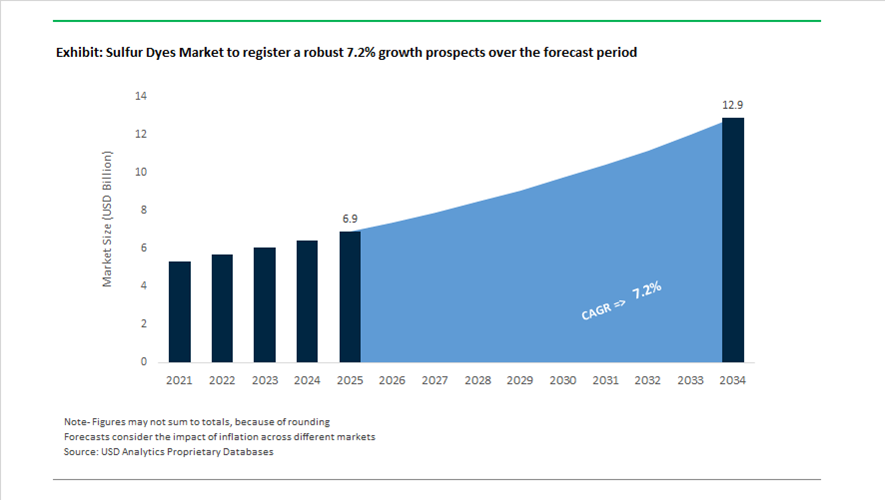

Sulfur Dyes Market Valuation 2025–2034: $6.9 Billion to $12.9 Billion at 7.2% CAGR Accelerated by Sustainable Denim Processing and Supply Chain Integration

The global sulfur dyes market is valued at $6.9 billion in 2025 and is projected to reach $12.9 billion by 2034, expanding at a CAGR of 7.2%. Growth is being propelled by rising demand for sulfur black dyes, pre-reduced liquid sulfur dyes, non-sulfide sulfur colorants, and bio-based dye intermediates used primarily in denim, workwear, and cotton textiles. Increasing environmental scrutiny on sulfide discharge, water consumption, and hazardous oxidizing agents is driving innovation toward low-sulfide dyeing processes, recyclable wastewater systems, and carbon-conscious raw materials. Manufacturers are modernizing sulfur dye chemistry to reduce effluent load, improve fixation efficiency, and enable high-contrast finishing techniques compatible with laser and ozone-based denim processing.

Capacity upgrades and feedstock integration gained momentum in 2024. In early 2024, Archroma scaled its EarthColors® EVOLUTION BLACK sulfur-based dye synthesized from non-edible agricultural waste such as nut shells and leaves, supporting carbon-conscious denim collections adopted by global apparel brands. During 2024, Shree Pushkar Chemicals & Fertilisers expanded its sulfur derivative capacity at Ratnagiri, India to strengthen supply of high-purity sulfur dye intermediates. In late 2024, Kensing LLC acquired Advanced Organic Materials, increasing access to plant-based feedstocks increasingly explored for sustainable dye synthesis. Through 2024 and 2025, Archroma expanded its DIRESUL® RDT pre-reduced liquid sulfur dye portfolio, enabling up to 50% water savings and significantly lower sulfide content compared to conventional powder sulfur dyeing systems.

Operational consolidation and sustainable processing breakthroughs defined 2025. In February 2025, DyStar consolidated its North American operations into its Reidsville, North Carolina facility to optimize production efficiency for specialty dyes and textile chemicals. In June 2025, DyStar transitioned to full ownership under Zhejiang Longsheng Group, strengthening integration with upstream sulfur intermediate supply chains. In September 2025, MKS Devo Chemicals launched non-sulfide, recyclable sulfur dye solutions in Bangladesh in partnership with Dysin Group, allowing textile mills to filter and reuse wastewater across multiple cycles. In October 2025, Archroma received the ITMF Sustainability & Innovation Award for its DENIM HALO process, a sulfur dyeing and pretreatment technology enabling high-contrast laser etching on black denim while eliminating potassium permanganate and manual scraping.

Strategic restructuring and material science alignment continue into 2026. In February 2025, Asahi Kasei announced the merger of its epoxy subsidiaries effective April 2026, streamlining resin technologies frequently paired with dye fixation systems in technical textiles. In early 2025, Nippon Kayaku advanced its KAYAKU Vision 2025 strategy, emphasizing high-margin fine chemicals and specialized colorants. In February 2026, Huntsman confirmed its corporate restructuring program remains on track for completion by the end of 2026, targeting cost efficiencies across textile effects and chemical intermediates. These sustainability-driven dye innovations, sulfur intermediate capacity expansions, vertical supply integration efforts, and operational consolidations are reshaping the sulfur dyes market trajectory through 2034.

Structural Trends and Monetizable Opportunities in the Sulfur Dyes Market

Regulatory Mandates Driving Clean Sulfur Dye Chemistry in Global Exports

The sulfur dyes market is undergoing a structural reset as regulatory compliance becomes a prerequisite for participation in global apparel supply chains. Export-oriented textile hubs across India, Bangladesh, and Southeast Asia are rapidly transitioning toward ECO-Passport and bluesign approved sulfur dye systems to meet Zero Discharge of Hazardous Chemicals conformance requirements. Global fashion retailers such as H&M and Inditex now mandate ZDHC Conformance Level 3 across dyeing auxiliaries, effectively eliminating legacy sulfur dyes containing restricted aromatic amines, aniline residues, and heavy metal impurities.

By mid-2025, specialty chemical suppliers had accelerated portfolio upgrades to maintain market access. Archroma confirmed that its DIRESUL RDT range achieved Cradle to Cradle Certified Material Health Gold status under Version 4.0, signaling a shift from commodity sulfur dyes toward high-purity, formulation-controlled systems. This regulatory alignment has tangible commercial impact. Heightened inspection regimes enforced by the European Chemicals Agency in 2025 increased scrutiny of imported textiles for trace chromium and copper contamination. Mills that migrated to pre-reduced liquid sulfur dyes reported materially lower consignment rejections at European ports, protecting long-term supply contracts and reducing shipment volatility for private-label apparel exporters.

Continuous Sheet Dyeing Adoption Redefining Denim Production Economics

The global denim sector is rapidly modernizing dyeing infrastructure as brands demand reproducible dark shades with lower environmental intensity. Continuous Sheet Dyeing systems are replacing conventional rope-dyeing lines, particularly for black, sulfur-indigo hybrids, and earth-tone denim. These systems rely on stabilized liquid sulfur dyes that allow uniform penetration and controlled oxidation across wide fabric widths.

Environmental and cost benchmarks are reshaping investment decisions. Archroma’s 2025 sustainability disclosures show that DIRESUL Evolution Black reduces overall environmental impact by 57% versus conventional Sulfur Black 1. When deployed in continuous dyeing ranges, water consumption can fall by up to 50% compared with indigo rope dyeing, directly supporting water stewardship targets set by brands such as Levi Strauss & Co., which aims to recycle or reuse 40% of manufacturing water by 2025. Public policy is reinforcing this transition. Early-2025 incentives under the Gujarat Textile Policy offered capital subsidies of up to 30% for mills upgrading to resource-efficient dyeing machinery, accelerating regional adoption of smart denim platforms that prioritize liquid sulfur chemistry, shade consistency, and lower reprocessing losses.

Specialty Sulfur Dyes for High-Visibility and Protective Workwear

A fast-expanding opportunity is emerging in high-visibility and protective apparel, where sulfur dyes are being repositioned as performance-critical colorants rather than cost-driven commodities. Infrastructure, utilities, and transportation sectors increasingly require EN ISO 20471 compliant garments that maintain chromatic contrast after repeated industrial laundering and prolonged UV exposure. While sulfur dyes already deliver strong wash fastness, innovation is now focused on developing UV-stable contrast shades such as deep navy and engineered blacks that achieve lightfastness ratings of 6 or higher.

In parallel, technical textile developers are exploring synergistic formulations that combine sulfur dyes with phosphorus-based flame retardant finishes. Pilot-scale data released in 2025 indicate that sulfur-dyed cotton blends retain superior tensile and tear strength after FR treatment compared with vat-dyed fabrics. This mechanical resilience translates into lighter garments with equivalent protection levels, creating a compelling value proposition for industrial coveralls, rail safety uniforms, and oil and gas protective apparel.

Decarbonizing Effluent Through Low-Sulfide and Bio-Derived Reduction Systems

Effluent toxicity associated with sodium sulfide reduction remains the most critical environmental bottleneck for sulfur dyes. With wastewater discharge limits tightening globally, the shift toward low-sulfide and sulfide-free application systems represents the sector’s most transformative opportunity. Stabilized pre-reduced liquid sulfur dyes and organic reducing agents are rapidly displacing inorganic sodium sulfide, reducing chemical oxygen demand and eliminating sulfide salt accumulation in effluent streams.

Industry leaders such as DyStar have commercialized integrated systems like Cadira Denim, replacing traditional reducers with biodegradable alternatives. Mills adopting these platforms have reported wastewater treatment cost reductions of up to 20% alongside near-zero sulfide toxicity. Beyond process optimization, circular feedstock innovation is creating differentiation. Archroma’s EarthColors technology synthesizes sulfur dyes from non-edible agricultural waste, including nut shells and forestry by-products. Having moved beyond pilot collaborations with niche brands, these bio-based sulfur dyes are now scaling into mainstream denim and casualwear production, offering petroleum-free, REACH-aligned color solutions for sustainability-driven apparel portfolios.

Sulfur Dyes Market Share and Segmentation Insights

Liquid Sulfur Dyes Dominate the Sulfur Dyes Market with Automation-Ready Textile Dyeing Formulations

Liquid sulfur dyes accounted for 52.80% of the sulfur dyes market in 2025, establishing them as the preferred dye form across large-scale textile dyeing operations. Liquid formulations enable direct dosing into dye baths, eliminating the dissolution step required for powder dyes and reducing dust exposure in manufacturing environments. This convenience supports efficient use in high-volume textile dyeing processes, particularly for denim and dark-colored fabrics. The 2025 industry shift is the increasing adoption of automated textile dyeing systems, where liquid sulfur dyes provide stable, pumpable formulations compatible with automated dosing equipment, ensuring consistent shade reproduction and improved operational efficiency in modern textile mills.

Denim and Casual Wear Drive Global Sulfur Dye Consumption

Denim and casual wear accounted for 58.60% of sulfur dyes market demand in 2025, reflecting the extensive use of sulfur dyes in producing dark shades for denim fabrics and casual apparel. Sulfur dyes such as Sulfur Black are widely used in denim overdyeing processes, enabling manufacturers to achieve deep black, navy, and other dark color tones required for fashion garments. The scale of global denim production supports sustained demand for sulfur dyes in textile finishing operations. The 2025 development trend centers on sustainable denim dyeing technologies, including low-liquor ratio dyeing systems, electrochemical dyeing methods, and improved washing processes, which reduce water consumption and chemical discharge while maintaining the deep color intensity required in modern denim manufacturing.

Sulfur Dyes Market Competitive Landscape

The sulfur dyes market in 2026 is shaped by circularity-driven coloration, low-COD dye chemistries, and laser-compatible denim systems. Competition is concentrated in sulfur black innovation, wastewater reduction, and bio-based feedstocks, with manufacturers integrating sustainability certifications, digital dyeing processes, and advanced effluent management solutions.

Archroma Advances Low-Impact Sulfur Black with Bio-Based Feedstocks and Laser-Compatible Denim Systems

Archroma leads the sustainable sulfur dyes market through its Super Systems+ platform and advanced R&D at Castellbisbal. Its DIRESUL® EVOLUTION BLACK, launched in 2026, delivers a 57% environmental impact reduction versus conventional Sulfur Black 1, addressing COD and effluent toxicity challenges. The company achieved Cradle to Cradle Certified® Material Health Gold for multiple dye portfolios, reinforcing clean-label positioning. Its collaboration with Artistic Milliners introduces laser-friendly sulfur dyes optimized for denim finishing and reduced CO2 emissions. The EarthColors® range utilizes agricultural waste feedstocks, enabling traceable, bio-based dye production. Archroma’s focus on wastewater treatability and circular chemistry strengthens its leadership in premium denim and workwear segments.

Atul Integrates Digital Manufacturing and Renewable Energy into High-Volume Sulfur Dye Production

Atul is strengthening its sulfur dyes market position through Industry 4.0-enabled manufacturing and sustainability-led operations. Its digitalization initiatives, recognized in 2026 excellence awards, enhance dye yield consistency and process efficiency. The company received industry recognition for water conservation and indigenous sulfur dye technology, particularly in high-performance blue shades. Atul’s investment in a hybrid renewable energy venture supports its transition to wind and solar-powered dye production by 2027. With exports spanning over 90 countries, Atul maintains strong supply chain resilience amid global volatility. Its vertically integrated Colors business ensures scalability across denim, textiles, and industrial dyeing applications.

Asahi Focuses on Water-Soluble Sulfur Dyes and Clean Reducing Chemistry for Continuous Dyeing

Asahi Songwon and Asahi Dyestuff are advancing eco-efficient sulfur dyeing through high-solubility Asathiosol dyes and cleaner reducing systems. Its water-soluble sulfur dyes enable continuous two-phase dyeing processes, improving leveling and reproducibility across cotton and nylon substrates. The introduction of Asahi Thiogen replaces sodium sulfide, significantly reducing hydrogen sulfide emissions and simplifying wastewater treatment. Despite pricing pressures, the company reported ₹120.75 crore revenue in FY2026 (Q3), emphasizing operational efficiency in its blue dye segment. Expansion across China and South Korea supports capacity scaling and regional diversification. Its strategy integrates specialty colorants and imaging materials to reduce dependence on conventional textile dyes.

Jay Chemical Expands Effluent Treatment Integration and Hybrid Dyeing Systems for Global Denim Markets

Jay Chemical is enhancing its global sulfur dyes footprint by integrating water treatment chemicals with dye supply, offering textile mills a full-cycle effluent management solution. Its powdered sulfur dyes are widely adopted in Latin America due to cost efficiency and storage stability. The company is developing hybrid reactive-sulfur dyeing systems to achieve deeper blacks and navy tones with improved fastness properties. Expansion into sub-Saharan Africa strengthens its presence in emerging denim export hubs. Its strategy focuses on digital-ready auxiliaries and high-affinity sulfur blacks tailored for modern textile processing. The combined chemical and treatment approach reduces environmental compliance costs for large-scale dyeing operations.

Nippon Kayaku Leverages Functional Chemistry and Catalyst Optimization for High-Durability Sulfur Dyes

Nippon Kayaku positions sulfur dyes within its broader functional chemicals ecosystem, emphasizing durability, lightfastness, and sustainability. Under KAYAKU Vision 2025, the company is optimizing catalyst systems to increase synthesis efficiency and reduce CO2 emissions across dye production. Its R&D capabilities extend to dichroic dyes and polarizers, enabling cross-application innovation in automotive displays and HUD systems. The company is expanding inkjet ink and colorant production in Asia to capitalize on specialty materials demand. Its customized catalyst services allow manufacturers to improve sulfur dye purity and reduce environmental impact during synthesis. Nippon Kayaku’s integration of advanced materials science supports high-performance textile and industrial applications.

China Sulfur Dyes Market Under Cost Pressure and Regulatory Reconfiguration

China’s sulfur dyes industry entered a structurally constrained phase in 2025–2026 as upstream sulfur economics and downstream regulatory mandates converged. Domestic prices for 99.5% sulfur CIF in East China surged to around 3,860 yuan per ton by late 2025, representing a 166% year-on-year escalation, with early 2026 projections exceeding 5,000 yuan per ton. This sharp increase has materially raised the production cost of bulk sulfur black, particularly for commodity-grade denim applications where pricing elasticity is limited. The pressure is further amplified by competition from China’s fast-growing solid-state battery sector, which has absorbed increasing volumes of high-purity sulfur since Q1 2026, tightening availability for dye intermediates.

At the regulatory level, the mandatory rollout of GB 30981-2025 coating standards by June 2026 has become a de facto inflection point for sulfur dye manufacturers. The requirement to sharply reduce aromatic amines and heavy metals is accelerating the exit of smaller non-compliant players while favoring vertically integrated and technology-forward producers. Companies such as Jiangsu Dipu Technology have responded by backward integrating into sodium sulfide production, achieving reported raw material cost savings of 15 to 20% and improving supply security. Parallel investments in digital-sulfur hybrid dyeing systems within Zhejiang textile clusters have demonstrated 60 to 70% reductions in water consumption, signaling that process innovation is emerging as a core competitive lever alongside compliance credentials. Recognition of facilities such as the Archroma Panyu site for clean production reinforces the shift toward export-grade, regulation-aligned sulfur dyes as China pivots from volume to value.

India Sulfur Dyes Market Driven by Denim Exports and Sustainable Chemistry

India’s sulfur dyes market in 2025 has been shaped by resilient textile exports and accelerating adoption of energy- and resource-efficient dyeing technologies. With textile exports growing by an estimated 12 to 15% year over year, domestic demand for liquid sulfur black has expanded rapidly, particularly within the denim and casual wear segments concentrated in Gujarat and Maharashtra. This growth has supported a structural transition away from powder-based sulfur dyes toward stabilized liquid formulations that offer improved shade consistency and lower handling risks.

Innovation capacity has become a defining differentiator. In late 2025, Archroma expanded its Global Innovation Center of Excellence in Mumbai, consolidating R&D for pre-reduced sulfur dyes and low-impact auxiliaries. Indian mills have also accelerated adoption of Denim Halo pretreatment technologies using DIRSOL chemistry, enabling distressed aesthetics while cutting energy consumption by up to 36%. On the policy front, increasing uptake of ISCC PLUS certification reflects alignment with European fashion brands’ Green Tier sourcing requirements, while the Production Linked Incentive framework has begun channeling capital toward startups developing biosynthetic and waste-derived dye chemistries. Collectively, these trends position India as a growth-oriented, compliance-ready sulfur dyes hub with rising relevance in global denim supply chains.

Vietnam Sulfur Dyes Market Anchored in Trade Compliance and Automation

Vietnam has emerged as a strategically important sulfur dyes consumption market, supported by its expanding textile and apparel export base. Infrastructure upgrades in 2025 marked a turning point, with the textile chemicals segment, a major end user of sulfur dyes, projected to approach USD 115 million in value by 2029. Preferential access under EVFTA and CPTPP has imposed stricter compliance thresholds, making ZDHC Level 3 conformity a prerequisite for sulfur dyes used in export-oriented denim destined for European markets.

Operationally, Vietnamese dye houses have moved quickly toward digital transformation. By late 2025, Industry 4.0 automated dispensing systems for liquid sulfur dyes were increasingly deployed, narrowing color consistency deviations to within plus or minus five%. Sustainability has become equally central, as export-focused manufacturers pursue OEKO-TEX and GOTS certifications to satisfy 2026 brand mandates. These developments collectively shift Vietnam’s sulfur dyes demand toward high-purity, low-impurity liquid grades rather than cost-driven bulk powders.

United States Sulfur Dyes Market Focused on Specialty and Application Innovation

The U.S. sulfur dyes market remains comparatively small in volume but increasingly influential in specialty applications and downstream process innovation. In its December 2025 outlook, Huntsman Corporation highlighted expectations for a stronger 2026, supported by stabilizing interest rates and easing tariff uncertainty across U.S.–China trade flows. This macro stabilization has encouraged renewed investment in differentiated sulfur dye formulations rather than commodity capacity.

Regulatory alignment has played a decisive role. Responding to EPA-driven trends, U.S. producers introduced stabilized liquid sulfur dyes in 2025 that eliminate hazardous reducing agents during application, aligning with Safer Choice-style procurement preferences. In parallel, collaborations between dye manufacturers and laser-finishing technology providers have yielded DIRESUL sulfur blacks optimized for high-contrast laser etching. These dyes enable precise denim finishing without manual scraping, reducing labor intensity and water usage. As a result, the U.S. market is increasingly characterized by application-specific sulfur dyes engineered for automation, safety, and high-value apparel finishing rather than bulk coloration.

Comparative Snapshot: Sulfur Dyes Industry by Country

Sulfur Dyes Market County Level Snapshot

|

Country

|

Primary Market Driver

|

Strategic Shift

|

Competitive Differentiator

|

|

China

|

Sulfur feedstock inflation and regulation

|

Vertical integration and digital dyeing

|

Cost buffering and clean-production compliance

|

|

India

|

Denim export growth

|

Liquid and pre-reduced sulfur dyes

|

Energy-efficient processes and certification readiness

|

|

Vietnam

|

Trade agreement compliance

|

Automation and digital dispensing

|

ZDHC, OEKO-TEX, and GOTS alignment

|

|

United States

|

Specialty apparel finishing

|

Safer formulations and laser compatibility

|

Application-driven innovation

|

Sulfur Dyes Market Report Scope

Sulfur Dyes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.9 Billion

|

|

Market Size (2034)

|

$12.9 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Product Form (Liquid Sulfur Dyes, Powder and Granular Sulfur Dyes, Specialty Sulfur Dye Blends), By Chemical Type (Sulfur Black, Colored Sulfur Dyes, Leuco Sulfur Dyes), By Application (Denim and Casual Wear, Industrial and Workwear, Leather and Hides, Paper and Pulp, Home Textiles)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archroma, Huntsman Corporation, Nippon Kayaku Co., Ltd., Jiangsu Dipu Technology Co., Ltd., DyStar Group, Shanxi Linfen Dyeing Chemicals Group Co., Ltd., Ningxia Langli New Material, Linyi Kemele Chemical, Asahi Songwon Colors Ltd., Dongyang Xinghong, Swiss Orgochem, Kiri Industries Limited, Atul Ltd., Inner Mongolia Yayanhua Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sulfur Dyes Market Segmentation

By Product Form

- Liquid Sulfur Dyes

- Powder and Granular Sulfur Dyes

- Specialty Sulfur Dye Blends

By Chemical Type

- Sulfur Black

- Colored Sulfur Dyes

- Leuco Sulfur Dyes

By Application

- Denim and Casual Wear

- Industrial and Workwear

- Leather and Hides

- Paper and Pulp

- Home Textiles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Sulfur Dyes Industry

- Archroma

- Huntsman Corporation

- Nippon Kayaku Co., Ltd.

- Jiangsu Dipu Technology Co., Ltd.

- DyStar Group

- Shanxi Linfen Dyeing Chemicals Group Co., Ltd.

- Ningxia Langli New Material

- Linyi Kemele Chemical

- Asahi Songwon Colors Ltd.

- Dongyang Xinghong

- Swiss Orgochem

- Kiri Industries Limited

- Atul Ltd.

- Inner Mongolia Yayanhua Group

*- List not Exhaustive