Textile Chemicals Market 2025–2034: $29.6 Billion to $44.4 Billion at 4.6% CAGR Driven by ZDHC Compliance, Bio-Based Finishes, and Regional Manufacturing Shifts

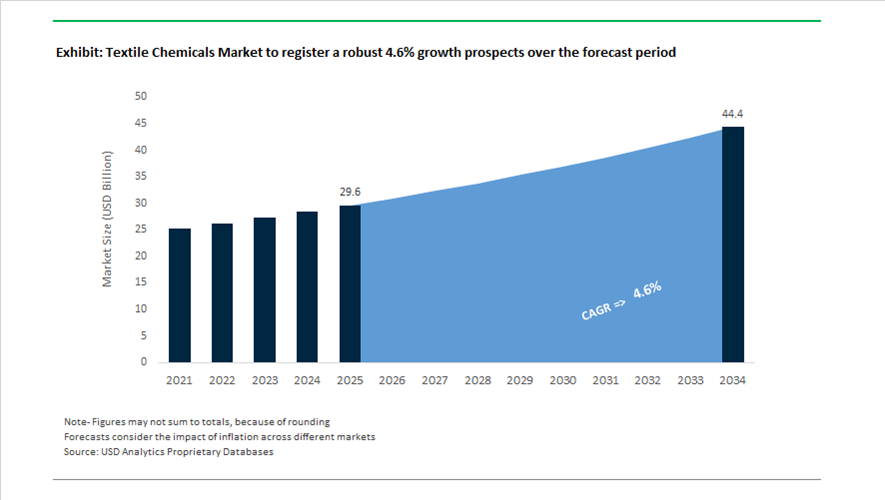

The global textile chemicals market is valued at $29.6 billion in 2025 and is projected to reach $44.4 billion by 2034, expanding at a CAGR of 4.6%. Growth is anchored in functional finishes, sustainable dyeing auxiliaries, antimicrobial treatments, and performance-enhancing coatings tailored to sportswear, technical textiles, automotive fabrics, and home furnishings. The market is undergoing structural transformation as brands and regulators push for zero-discharge chemistry, PFC-free water repellents, and traceable bio-based formulations. Compliance with ZDHC MRSL Level 3 standards and global “forever chemical” restrictions has become a primary competitive differentiator, influencing procurement strategies across global apparel supply chains.

Sustainability partnerships and portfolio consolidation accelerated in 2025–2026. On February 1, 2026, RUDOLF GmbH assumed exclusive global distribution of Sanitized® textile technologies, centralizing odor-control and hygiene chemistries under a unified supply platform. In January 2026, Archroma entered a co-marketing agreement with HeiQ to expand bio-based anti-odor and antimicrobial solutions targeting activewear and home textiles. Archroma strengthened its R&D presence in late 2025 by expanding its Innovation Center of Excellence in Mumbai, reinforcing India’s role as a global textile chemical innovation hub. In December 2025, Archroma earned Champion status at the adiFormulator Awards for the second consecutive year, demonstrating progress toward 80% ZDHC MRSL Level 3 compliance across its portfolio. Meanwhile, in January 2026, Pulcra Chemicals introduced STABIFIX® NBF, a next-generation fixing agent engineered to improve polyamide color fastness while meeting stricter environmental criteria.

Regional investment momentum is strongest in India and the Middle East. In April 2025, Shivtek Spechemi Industries announced a ₹650 crore investment in green textile auxiliary plants in Gujarat and Rajasthan. Gujarat’s 30% capital subsidy under its updated textile policy triggered significant upgrades in effluent treatment and eco-chemistry systems during 2024–2025. In February 2026, Rossari Biotech partnered with Sadara Chemical Company to localize textile chemical supply in Saudi Arabia, reflecting the geographic diversification of production beyond traditional Asian hubs. Machinery and process innovation also advanced sustainability goals: in February 2025, Tonello acquired Flainox to integrate dyeing and finishing systems that reduce water and chemical consumption. Earlier, in January 2024, RUDOLF introduced bio-based HYDROCOOL® technologies with up to 87% renewable content, while in November 2025 Pulcra and Devan launched DEVAN REPEL ONE, a fully PFC- and isocyanate-free durable water repellent for polyester.

Structural Inflection Points and Value-Creation Opportunities in the Textile Chemicals Market

PFAS Exit Reshapes the Performance Finishing Chemicals Landscape

The global textile chemicals market is undergoing a non-negotiable reformulation cycle as regulatory bans on PFAS-based durable water repellents move from policy intent to commercial enforcement. From January 1, 2025, large U.S. consumer markets including California and New York have prohibited the sale of apparel containing intentionally added PFAS, including C6 fluorinated finishes. This has converted what was previously a sustainability-led transition into a compliance-driven market reset, directly impacting finishing chemistries used in outdoor, sportswear, and technical textiles.

Major OEMs such as Patagonia and The North Face have fully migrated their waterproof portfolios to fluorine-free DWR systems, signaling to upstream chemical suppliers that fluorinated technologies are no longer commercially defensible. At the membrane level, Gore-Tex scaled its expanded polyethylene membrane into premium product tiers during the Winter 2024–2025 season, enabling compliance with emerging 100 ppm total organic fluorine thresholds without sacrificing breathability or abrasion resistance.

Simultaneously, certification regimes have tightened. The OEKO-TEX® Association lowered allowable PFHxA limits to 25 µg/kg effective April 2025, while Bluesign has implemented a full long-chain PFAS exclusion. These shifts have forced chemical producers such as Archroma and Rudolf Group to redesign entire weather-protection portfolios around bio-based, silicone, and dendrimer architectures. The commercial implication is a structural premium on fluorine-free DWR systems that can meet hydrostatic head and wash durability benchmarks previously monopolized by C6 chemistry.

Digital Printing and Waterless Dyeing Drive High-Purity Auxiliary Demand

Parallel to regulatory pressure, the accelerating adoption of digital textile printing is reshaping the auxiliaries segment from a volume-driven business into a performance-led specialty market. Digital systems are now strategically favored by brands due to their ability to compress design-to-shelf timelines while delivering material sustainability gains. Industry data consolidated in 2025 confirms that digital printing reduces water consumption by up to 90% and energy use by approximately 30% compared to rotary screen processes.

This shift is creating a structurally attractive niche for digital pre-treatment agents, reactive binders, and fixation auxiliaries engineered for high-frequency inkjet environments. Unlike conventional dyeing chemicals, these formulations must exhibit ultra-low impurity profiles and stable rheology to avoid nozzle clogging while ensuring consistent ink-to-fiber bonding on cotton, viscose, and blended substrates.

Technology providers are now scaling integrated platforms that blur the line between machinery and chemistry. In October 2025, Alchemie Technology expanded commercial partnerships for its Endeavour digital dyeing system, which combines automated chemical dosing with precision application to achieve up to a 95% reduction in water waste. This has shifted purchasing behavior toward solution-based chemical contracts, favoring suppliers capable of delivering digitally compatible auxiliaries validated at industrial print speeds.

Enzyme-Driven Denim Finishing Replaces Oxidative Chemistry

One of the most commercially material opportunities in textile chemicals lies in enzyme-based finishing systems for denim. Brands are rapidly eliminating potassium permanganate and hypochlorite bleaching due to worker safety risks, wastewater toxicity, and brand-level ESG scrutiny. Enzymatic abrasion and bleaching have moved from pilot trials to industrial baselines for mills supplying Europe and North America.

Water stewardship commitments are accelerating adoption. Levi Strauss & Co. has embedded enzyme-mediated finishing across its Water From a compliance perspective, enzyme portfolios are increasingly expected to meet ZDHC Level 3 standards. As the EU’s Ecodesign for Sustainable Products Regulation tightens chemical disclosure and safety requirements, bio-desizing, bio-polishing, and enzyme abrasion agents have become mandatory rather than optional for export-oriented denim mills. This positions specialty enzyme suppliers for sustained margin expansion relative to commodity oxidizing agents.

Specialty Additives Unlock Higher rPET Content in Performance Textiles

The final high-growth opportunity is emerging at the intersection of recycled polyester adoption and chemical performance restoration. As fashion and sportswear brands commit to 50% or higher recycled content targets, limitations inherent to rPET such as yellowing, viscosity loss, and uneven dye uptake are becoming bottlenecks at scale.

Advanced compatibilizers and stabilizing additives are now being deployed to restore intrinsic viscosity during melt processing and to suppress thermal degradation. Chemical systems such as Holland Colours’ ViscoBoost and CircStab are enabling higher rPET loadings without compromising fiber tensile strength or color consistency, directly supporting premium apparel applications.

Policy momentum is reinforcing demand. The EU Packaging and Packaging Waste Regulation and Extended Producer Responsibility frameworks approved in September 2025 are forcing brands to account for garment end-of-life outcomes. This has elevated fiber-to-fiber recycling chemistry into a strategic procurement category, particularly additives that enable rPET to be blended with cotton or elastane while maintaining colorfastness and processability. For chemical suppliers, this represents a defensible specialty niche aligned with long-term circular textile economics rather than short-cycle fashion trends.

Textile Chemicals Market Share and Segmentation Insights

Product Type Market Share: Coating and Sizing Agents Lead with Functional Textile Innovation

Coating and sizing agents hold the largest share in the textile chemicals market at 28.40% in 2025, driven by their critical role in yarn protection, weaving efficiency, and performance enhancement. These chemicals enable key functionalities such as water repellency, flame retardancy, antimicrobial properties, and durability, making them indispensable across high-volume textile production. Other segments including colorants and auxiliaries, finishing agents, surfactants, and desizing and pre-treatment agents maintain steady demand across processing stages. A key growth catalyst is the rise of functional textiles, where advanced solutions such as nano-based coatings, smart finishes, and high-performance treatments are increasingly adopted in apparel, sportswear, and technical textiles.

Application Market Share: Apparel and Garments Segment Dominates Amid Sustainable Textile Shift

Apparel and garments account for 52.80% of the textile chemicals market in 2025, supported by the large-scale consumption of chemicals across pre-treatment, dyeing, finishing, and performance enhancement processes. The segment benefits from continuous production cycles driven by fast fashion, seasonal collections, and evolving consumer preferences. Home textiles, technical textiles, and industrial textiles contribute smaller shares but are expanding with specialized applications. A major industry shift is the growing demand for sustainable textile chemicals, including bio-based finishes, heavy metal-free dyes, biodegradable auxiliaries, and water-efficient processing solutions, enabling apparel manufacturers to align with environmental regulations while maintaining fabric quality and performance standards.

Textile Chemicals Market Competitive Landscape

The textile chemicals market in 2026 is defined by green decoupling strategies, with manufacturers shifting production to Asia and North America while advancing Right-First-Time (RFT) processing. Demand is accelerating for PFAS-free finishes, bio-based auxiliaries, and low-energy textile processing technologies that reduce water and energy consumption by up to 60%.

Archroma Leads RFT Textile Processing with SUPER SYSTEMS+ and Global Innovation Centers

Archroma remains the global benchmark in sustainable textile chemicals, focusing on integrated system solutions under its "Beyond Compliance" framework. The launch of Global Centers of Innovation in Mumbai, Prat, and Charlotte strengthens its regional innovation capabilities. Its SUPER SYSTEMS+ platform enables fiber-specific RFT processing, reducing water usage by up to 80% in pretreatment. Collaboration with HeiQ enhances antimicrobial and odor-control finishes for high-performance textiles. Achieving EcoVadis Gold rating and targeting 80% ZDHC MRSL Level 3 compliance underscores sustainability leadership. Archroma continues to dominate eco-efficient textile auxiliaries and functional finishing technologies.

Huntsman Repositions Portfolio Toward High-Performance Intermediates After Textile Effects Divestiture

Huntsman Corporation is focusing on operational discipline and cost optimization following the divestment of its Textile Effects division. The company achieved $100 million in cost savings in 2025 and is targeting an additional $45 million in 2026. Strategic emphasis is on MDI-based polyurethanes, epoxies, and specialty intermediates used in textile coatings and laminates. Facility rationalization and workforce optimization have improved margin stability. Recovery in China and North America is expected to support demand for performance materials. Huntsman maintains relevance in textile chemicals through upstream intermediates and advanced material solutions.

DyStar Strengthens Global Textile Chemical Supply with Longsheng Integration and Cadira Sustainability Modules

DyStar Group has entered a new phase of stability following full integration into Zhejiang Longsheng Group in 2026. This consolidation enhances upstream raw material security and global supply chain efficiency. The Cadira® modules remain a core offering, enabling mills to reduce carbon footprint and optimize resource consumption. Manufacturing consolidation in the Americas supports growth in high-value specialty segments. ISO 14001 certification at its Indonesia facility reinforces environmental compliance. DyStar continues to lead in sustainable dyeing solutions and digitalized textile chemical management systems.

RUDOLF Drives PFAS-Free Textile Finishing with BIONIC-FINISH® ECO and Carbon Transparency Programs

RUDOLF Group is leading the transition to PFAS-free textile chemicals through its BIONIC-FINISH® ECO platform, the industry benchmark for fluorine-free water repellency. Expansion of Sanitized® technologies enhances odor control and hygiene finishes for technical textiles. Its PCF program, aligned with PACT and TfS, delivers transparent carbon footprint data to customers. Innovations like OX20 provide non-biocidal odor neutralization using physical adsorption mechanisms. Compliance with EN 17681-1:2025 standards ensures regulatory readiness. RUDOLF’s focus on sustainable finishing technologies positions it strongly in performance apparel and industrial textiles.

Pulcra Accelerates Low-Impact Textile Processing with Sustineri Technology and Bio-Based Finishes

Pulcra Chemicals is advancing bio-based textile chemistry through its integrated beamhouse-to-finishing solutions. The acquisition of Devan Chemicals expands its portfolio into antimicrobial, probiotic, and thermoregulation technologies. Sustineri Coloring, developed with Inditex, enables one-bath processing that reduces water by 80% and energy by 60%. Its PULCRA TEC® and Naturalis® platforms meet stringent bluesign® and GOTS standards. With operations in 16 countries, Pulcra emphasizes local-for-local technical deployment. The company is scaling PFAS-free repellents and antistatic finishes for automotive and medical textile applications.

Croda Expands High-Purity Bio-Based Textile Chemicals with Smart Science and Consumer-Centric Innovation

Croda International Plc is focusing on high-purity, bio-based textile chemicals through its Smart Science approach. The company reported £1.70 billion in 2025 sales and is targeting over 20% operating margins by 2028. Growth is driven by New & Protected Products (NPP) and customer co-creation pipelines, which increased by 12% in 2025. Croda is leveraging Life Sciences expertise to develop biodegradable, skin-friendly textile finishes. Despite softness in Industrial Specialties, innovation in consumer care-driven coatings is expanding application scope. Its portfolio supports sustainable, high-performance textile formulations aligned with evolving ESG requirements.

India Textile Chemicals Market Driven by Policy-Led Modernization and ZLD-Centric Adoption

India’s textile chemicals market in 2025–2026 is being structurally reshaped by fiscal support, infrastructure upgrades, and a decisive pivot toward sustainable processing. The Union Budget 2025–26 increased allocations to the Ministry of Textiles by 19% to ₹5,272 crore, directly strengthening the Production Linked Incentive framework for man-made fibers and technical textiles. This funding wave is translating into higher demand for polymer-based sizing agents, high-performance scouring auxiliaries, and next-generation dye-fixing chemicals, particularly as a new five-year Cotton Mission with ₹600 crore in initial funding targets productivity gains in Extra-Long Staple cotton. Higher ELS cotton output typically requires low-foaming wetting agents and controlled-alkali scouring systems to preserve fiber integrity during high-speed processing.

Technology adoption is accelerating in parallel. Full customs duty exemption on shuttle-less looms from 2025 has catalyzed the shift toward rapier and air-jet weaving, structurally increasing consumption of low-viscosity, high-shear-stable sizing formulations. Innovation from domestic leaders such as Zydex Group, which launched the bio-eliminable siZaltex LVn as a PVA alternative, highlights the market’s movement toward effluent-load reduction. Integration of centralized Zero Liquid Discharge facilities across PM MITRA parks further incentivizes eco-compatible auxiliaries. Simultaneously, reactive dye capacity expansions by firms like Kiri Industries and Bodal Chemicals reflect India’s growing role as a global sourcing alternative to China, intensifying domestic demand for leveling agents, dispersants, and dye bath optimization chemicals.

China Textile Chemicals Market Anchored in Integration, Recycling, and Self-Sufficiency

China remains the most vertically integrated textile chemicals market globally, with 2025 marking a decisive shift toward circularity and energy efficiency. In early 2025, BASF SE inaugurated its first commercial loopamid® facility at Caojing, Shanghai, enabling nylon-6 textile waste to be chemically recycled at scale. This development is structurally increasing demand for specialty depolymerization catalysts, solvent systems, and purification chemicals embedded within recycling-driven textile value chains.

Upstream integration continues to reinforce cost leadership. Sinopec’s Yizheng Chemical Fiber site reached full operational status in 2025, deploying short-process manufacturing routes for polyester intermediates that reduce energy intensity by approximately 15%. Regulatory pressure under MIIT’s 2025 Green Manufacturing Roadmap mandates low-temperature oxidation and wastewater heat recovery for all new textile chemical units, pushing suppliers toward process chemicals compatible with heat-integrated systems. Under the 14th Five-Year Plan, China has also achieved meaningful self-sufficiency in high-performance coating agents for automotive and medical textiles, compressing import dependence on European specialty suppliers while expanding domestic demand for resin binders, crosslinkers, and durability enhancers.

Germany Textile Chemicals Market Defined by PFAS Exit and Green Chemistry Leadership

Germany’s textile chemicals market is transitioning from performance-at-all-costs to compliance-first innovation, with sustainability and regulatory anticipation as primary demand drivers. Under the “Winning Ways” strategy launched in 2025, BASF SE has prioritized green transformation chemistry, supported by nearly €2 billion in R&D spending in 2024. Investments in X3D® catalyst shaping and methane pyrolysis pilots at Ludwigshafen are laying the groundwork for low-carbon hydrogen and ammonia inputs into textile auxiliaries, particularly amines and finishing agents.

Market differentiation is increasingly compliance-led. The award of the German Sustainability Award 2025 to CHT Group for its solvent-free PIGMENTURA pigment printing system signals industry validation for energy-efficient coloration routes. Concurrently, German suppliers including Rudolf Group and Pulcra Chemicals completed the transition to fully PFAS-free water-repellent portfolios by end-2025, well ahead of broader EU restrictions. This shift is redefining global benchmarks for repellency agents, binders, and crosslinking systems, with German formulations increasingly specified by international brands seeking regulatory certainty.

Bangladesh Textile Chemicals Market Scaling with Green Factory Investments and RMG Demand

Bangladesh’s textile chemicals market is expanding in tandem with its evolution into a sustainability-led Ready-Made Garment hub. In 2025, multinational chemical suppliers invested over Tk 2,000 crore to support the country’s growing base of certified green factories, directly lifting demand for low-temperature enzymes, heat-recovery-compatible auxiliaries, and formaldehyde-free finishing agents. Leading apparel manufacturers such as DBL Group reported CO₂ reductions exceeding 3,000 tons in 2025 through the adoption of sustainable finishing chemistries and waste-heat utilization, reinforcing the commercial case for advanced process chemicals.

Domestic capability is also strengthening. Local players like Matex Bangladesh and Ecochem introduced EU-aligned eco-finishing ranges tailored for export-oriented RMG units, while a sharp increase in spinning capacity to 1.9 million tons for FY2025–26 has driven incremental demand for spinning lubricants, antistatic agents, and fiber-protection additives. As compliance requirements tighten across European buyers, Bangladesh’s textile chemicals consumption is increasingly skewed toward performance-balanced, regulation-ready formulations rather than cost-driven basics.

United States Textile Chemicals Market Shaped by PFAS Bans and Specialty Amine Reshoring

The U.S. textile chemicals market is undergoing a structural reformulation cycle driven by federal and state-level regulation. The Environmental Protection Agency’s finalized rules prohibiting articles containing PIP (3:1) from October 31, 2026, are forcing a comprehensive redesign of flame retardants, adhesives, and coating systems used across technical textiles. State-level bans in California and New York on intentionally added PFAS, effective January 2025, are further redefining sourcing requirements, with global suppliers compelled to certify fluorine-free compliance for U.S.-bound products.

Trade and industrial policy are reinforcing domestic production. Following recent realignments, the U.S. recorded a 12% increase in domestic output of specialty amines used as catalysts in polyurethane textile coatings. This on-shoring trend is elevating demand for high-purity intermediates, process stabilizers, and performance additives compatible with next-generation, PFAS-free coating architectures, positioning the U.S. as a critical test market for compliant textile chemical innovation.

Comparative Snapshot: Textile Chemicals Market by Country

Textile Chemicals Market County Level Snapshot

|

Country

|

Primary Driver

|

Structural Shift

|

Implication for Suppliers

|

|

India

|

PLI funding and ZLD parks

|

High-speed weaving and eco-sizing

|

Strong growth for bio-compatible auxiliaries

|

|

China

|

Integration and recycling

|

Circular nylon and energy-efficient polyester

|

Scale-driven demand for specialty process chemicals

|

|

Germany

|

PFAS exit and green R&D

|

Compliance-led reformulation

|

Premium positioning for sustainable chemistries

|

|

Bangladesh

|

Green RMG expansion

|

Export-oriented eco-finishing

|

Rising demand for EU-compliant formulations

|

|

United States

|

Regulatory bans and reshoring

|

PFAS-free redesign

|

Innovation-led demand for compliant additives

|

Textile Chemicals Market Report Scope

Textile Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$29.6 Billion

|

|

Market Size (2034)

|

$44.4 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product Type (Coating and Sizing Agents, Colorants and Auxiliaries, Finishing Agents, Surfactants, Desizing and Pre-Treatment Agents), By Fiber Type (Natural Fibers, Synthetic Fibers, Cellulosic Fibers), By Application (Apparel and Garments, Home Textiles, Technical Textiles, Industrial Textiles)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archroma, BASF SE, Huntsman Corporation, Tanatex Chemicals, CHT Group, Rudolf GmbH, DyStar Group, Kiri Industries Ltd., Evonik Industries AG, Dow Chemical Company, Wacker Chemie AG, Solvay S.A., LANXESS AG, Bozzetto Group, NICCA Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Textile Chemicals Market Segmentation

By Product Type

- Coating and Sizing Agents

- Colorants and Auxiliaries

- Finishing Agents

- Surfactants

- Desizing and Pre-Treatment Agents

By Fiber Type

- Natural Fibers

- Synthetic Fibers

- Cellulosic Fibers

By Application

- Apparel and Garments

- Home Textiles

- Technical Textiles

- Industrial Textiles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Textile Chemicals Industry

- Archroma

- BASF SE

- Huntsman Corporation

- Tanatex Chemicals

- CHT Group

- Rudolf GmbH

- DyStar Group

- Kiri Industries Ltd.

- Evonik Industries AG

- Dow Chemical Company

- Wacker Chemie AG

- Solvay S.A.

- LANXESS AG

- Bozzetto Group

- NICCA Chemical Co., Ltd.

*- List not Exhaustive