Market Overview: High-Current-Density HTS and Grid-Scale Use-Cases Drive the Superconducting Wire Market

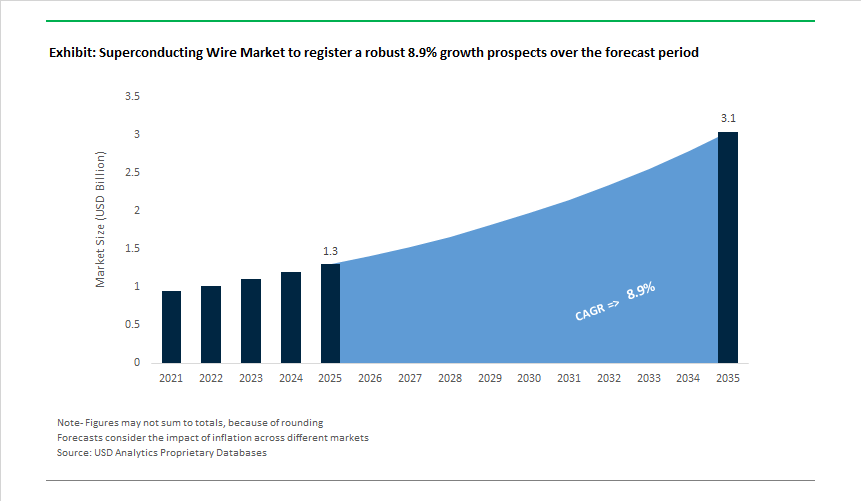

The Global Superconducting Wire Market is valued at USD 1.3 billion in 2025 and is projected to reach USD 3.0 billion by 2035, expanding at a CAGR of 8.9% as superconducting conductors move from research-centric procurement into infrastructure-grade deployment. Today, market growth is being shaped by power system constraints rather than pure technology push-specifically, the need to transmit more electricity through limited corridors, stabilize grids under renewable intermittency, and enable ultra-high-field magnet systems that conventional conductors cannot support.

Power utilities in dense urban regions are increasingly constrained by right-of-way limitations, thermal losses, and fault-current limits. High-temperature superconducting (HTS) wires, particularly 2G REBCO conductors, are being specified for fault current limiters (FCLs), medium-voltage DC (MVDC) links, and superconducting power cables because they enable Zero or near-zero transmission losses, Compact, high-current-density transmission in existing corridors, Fast-response fault protection without bulky mechanical systems, and others. As grids absorb higher shares of renewables and electrified loads, superconducting wire is shifting from pilot projects to strategic grid assets in select geographies.

The next decade of growth is strongly influenced by fusion reactor development and advanced magnet systems. Large-scale public programs (such as ITER) and emerging commercial fusion ventures are converging on HTS-based magnet architectures to achieve higher magnetic fields in smaller footprints. These systems require kilometer-scale lengths of superconducting wire, creating step-change demand profiles that are project-driven but long-duration. For wire manufacturers, fusion represents a volume anchor with high qualification barriers, supporting predictable multi-year offtake once programs advance beyond prototype stages. While mature, MRI and research magnets continue to provide a stable baseline for superconducting wire demand. Incremental upgrades in field strength, system efficiency, and operating cost are sustaining replacement and retrofit demand, particularly as healthcare systems invest in higher-resolution diagnostic capability.

The market is undergoing a clear technology shift from low-temperature superconductors (LTS) to high-temperature superconductors (HTS). HTS wires operate at higher temperatures, enabling simpler cooling architectures and better system economics for power and magnet applications. This transition is expanding the addressable market but also raising the bar on manufacturing consistency, yield, and scale, favoring suppliers with deep process control and long-length production capability.

The superconducting wire market through 2035 reflects a measured but structurally sound growth trajectory. While adoption will remain selective due to system cost and qualification timelines, demand is anchored in non-deferrable infrastructure needs-grid stability, energy security, and next-generation energy systems. As electrification deepens and high-field applications scale, superconducting wire is evolving from a specialty material into a strategic enabler of modern power and energy infrastructure, supporting sustained, fusion energy, and advanced medical systems.

Market Analysis: HTS Commercialization, MVDC Demonstrations and Fusion Partnerships Accelerate Industry Momentum

Commercial demonstrations and strategic R&D partnerships have substantially de-risked HTS deployment and strengthened the commercial pipeline. In June 2025, Nexans showcased an MVDC HTS cable demonstration capable of enabling multi-gigawatt (3.2 GW at 320 kV DC) zero-loss transmission-an important proof point for large-scale renewable integration and long-distance urban corridors. That same spring, Tokamak Energy and Furukawa Electric advanced their partnership (June 2025) toward commercial fusion, signaling that wire manufacturers are aligning R&D and supply-chain capabilities to support future fusion magnet winding volumes and qualification timelines.

Manufacturers also continue to invest in product and margin improvement. AMSC reported meaningful revenue growth and improved gross margins in Q1-Q2 FY2025, driven by grid business demand for superconducting fault current limiters and HTS-based systems (reported in November 2025 results). Industry R&D activity increased in October 2025, when Furukawa Electric launched a full-scale R&D initiative under a national NEDO project to develop high-temperature assembled superconductors for industrial magnets, underscoring national and corporate-level commitments to next-generation conductor technologies. Academic discoveries (January 2024) of novel superconducting material classes (e.g., certain TMDs) continue to expand the long-term materials frontier, but near-term commercialization will be dominated by proven ReBCO (2G HTS), Nb3Sn, and NbTi conductor technologies.

Collectively, these events indicate a two-track market: near-term commercial rollouts for HTS grid systems, data center and defense applications, and continued LTS dominance in medical imaging; and long-term, large-scale programs (fusion, high-field science) that will consume vast lengths of specialized wire, reinforcing demand predictability for established wire manufacturers that can meet qualification requirements.

Superconducting Wire Market Trends and Opportunities

Trend 1: HTS Wire as an Enabler for Compact Fusion Energy

The global superconducting wire market is undergoing a structural inflection as high-temperature superconducting (HTS) wire becomes a foundational input for compact fusion reactor architectures. Private fusion developers are moving away from the scale-heavy, capital-intensive ITER model and instead pursuing smaller Tokamak and Stellarator designs that rely on ultra-high magnetic fields exceeding 20 Tesla. This shift directly elevates the strategic importance of second-generation (2G) REBCO HTS tapes, which can sustain extreme current densities under high magnetic stress. In mid-2025, Commonwealth Fusion Systems validated this paradigm by deploying more than 260 kilometers of REBCO wire in a single high-field magnet test, confirming operational performance near 120 A/mm² at 20 Tesla. This level of performance enables dramatic reductions in reactor size, steel mass, and construction complexity, materially improving fusion’s economic viability. Momentum accelerated further in November 2025 when Tokamak Energy’s Demo4 magnet cluster achieved 18.3 Tesla, underscoring that HTS wire performance is no longer a laboratory constraint but a supply chain scaling challenge. Equally critical is the thermal advantage: HTS magnets operate efficiently at 20–40 K using liquid hydrogen or neon cooling, cutting cryogenic energy penalties by more than 60% compared to liquid-helium-cooled LTS systems. This efficiency gain directly improves the fusion Q-factor and shifts HTS wire from an enabling material to a cost-defining variable in commercial fusion roadmaps.

Trend 2: Strategic Industrialization of HTS Manufacturing Capacity

As HTS wire moves from experimental deployments into national energy and defense priorities, governments and manufacturers are aggressively industrializing production to reduce cost and improve yield. Today, HTS wire economics remain constrained by complex deposition processes and material losses that can account for nearly 30% of total manufacturing cost. In response, the U.S. Department of Energy allocated $34 million during 2024–2025 to its “HTS for Fusion” initiative, explicitly targeting kilometer-scale uniformity of the REBCO layer and higher production throughput. Parallel corporate investments reinforce this push. By late 2025, leading suppliers announced capacity expansions focused on continuous CVD and PVD process optimization, with internal targets to reduce price-per-meter by 15–20% by 2026 while improving engineering current density. Europe is pursuing a parallel path driven by strategic autonomy concerns. Under EU industrial and materials security frameworks, domestic superconducting thin-film production is being prioritized to reduce dependence on imported substrates and precursors. Collectively, these initiatives signal a shift in HTS wire from a specialty research material toward a semi-commoditized strategic input, with cost-reduction trajectories increasingly benchmarked against a $50/kA-m threshold viewed as critical for widespread grid, fusion, and defense adoption.

Opportunity 1: HTS-Based Fault Current Limiters for Grid Resilience

One of the most immediate commercial opportunities for superconducting wire lies in HTS-based fault current limiters (FCLs), as power grids struggle to absorb renewable generation, electrification loads, and energy-intensive AI data centers. Modern urban grids are experiencing rising short-circuit currents that exceed the design limits of existing transformers and breakers, creating a need for fast-acting protection without costly infrastructure replacement. HTS FCLs address this challenge by operating with zero impedance under normal conditions and transitioning to a resistive state within milliseconds during a fault. In 2025, deployment programs under the Resilient Electric Grid initiatives in major cities entered second-phase implementation, demonstrating that HTS FCLs can be integrated into live networks with minimal operational disruption. From a cost perspective, utilities view FCLs as a non-wire alternative capable of avoiding up to $2 million per substation in breaker and transformer upgrades. Long-duration field data strengthens the case: European installations using BSCCO and REBCO conductors have logged more than 10,000 operating hours without maintenance events, validating reliability at grid scale. As grid reinforcement spending accelerates globally, HTS FCLs represent a near-term, high-visibility growth channel for superconducting wire suppliers beyond fusion-led demand.

Opportunity 2: Long-Horizon Demand from Particle Accelerator Infrastructure

While HTS captures headlines, low-temperature superconducting (LTS) wire remains indispensable for large-scale physics infrastructure, providing the superconducting wire market with long-duration demand stability. The most significant driver is the planned Future Circular Collider, where feasibility studies released in 2025 indicate a requirement of roughly 9,000 tonnes of Nb₃Sn wire—an order of magnitude greater than total global production during the entire construction of the Large Hadron Collider. This scale fundamentally reshapes procurement dynamics for niobium-based wires, favoring manufacturers capable of sustained ultra-high-purity output. In parallel, next-generation accelerators such as LCLS-II-HE are tightening material specifications, demanding niobium with Residual Resistivity Ratios above 300 to minimize thermal losses in superconducting radiofrequency cavities. These purity thresholds push metallurgical capabilities and create pricing power for specialized wire producers. Importantly, multinational funding commitments in 2025 for projects such as the Electron-Ion Collider and the International Linear Collider provide a decade-long visibility window for LTS wire demand. This insulates suppliers from the cyclical volatility of medical imaging markets and anchors superconducting wire production in publicly funded, long-life infrastructure programs where reliability and performance outweigh short-term cost sensitivity.

Market Share Analysis: Superconducting Wire Market

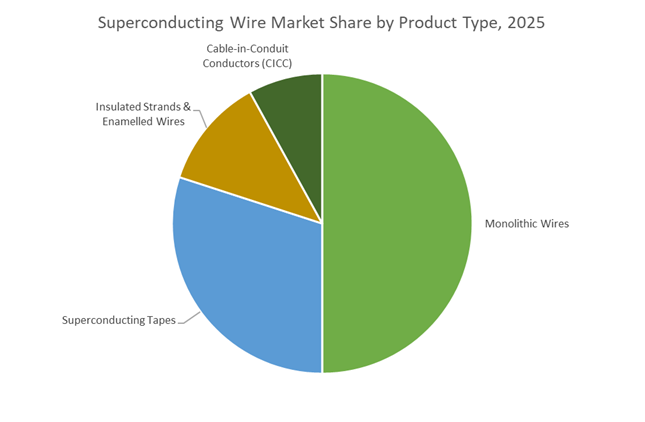

Market Share by Product Segment: Monolithic LTS Wires as the Commercial Backbone of High-Field Systems

Monolithic superconducting wires, commanding ~50% of global market value in 2025, remain the dominant product format because they align reliability, manufacturability, and cost efficiency at industrial scale—especially for low-temperature superconductor (LTS) applications. Despite growing interest in HTS, production data from Bruker EST and Luvata confirms that LTS still accounts for ~82% of total superconducting volume, with monolithic NbTi wires preferred for their mechanical robustness and predictable field homogeneity. Entering 2025 at $1.49 billion, the superconducting wire market assigns roughly $745 million to monolithic formats, expanding at a ~10.7% CAGR as clinical diagnostics scale across emerging economies. The cost curve advantage is structural: Luvata alone has supplied >525 million kilometers of filament, enabling economies of scale that newer architectures cannot yet match. Precision has also tightened—Sumitomo Electric and Fujikura report <1% cross-sectional deviation in 2025 production, a “zero-tolerance” requirement for ultra-stable magnetic fields. Together, scale economics, quality assurance, and field-proven reliability lock monolithic LTS wires into their majority share despite accelerating R&D elsewhere.

Market Share by End-User Industry: Medical Imaging Anchors Demand Through High-Field MRI Upgrades

The medical sector, led by MRI, accounts for ~55% of superconducting wire demand in 2025, making it the market’s commercial anchor and most predictable revenue stream. Superconducting MRI magnets alone represent a $2.45 billion opportunity and consume over half of global wire output, a dominance reinforced by the industry’s shift toward high-field systems. Installation data from Siemens Healthineers and GE HealthCare shows 3T scanners now comprise ~45% of new installs, materially increasing wire content per system versus 1.5T platforms and effectively doubling wire-to-system revenue intensity. The segment’s innovation halo is evident in ultra-high-field milestones: Luvata delivered 158 km of specialized cable for the 11.75T MRI, signaling diagnostic capabilities capable of detecting neurodegenerative disease at earlier stages—an institutional procurement catalyst. Simultaneously, the transition to helium-free (“dry”) magnets by Bruker and ASG Superconductors reduces operating costs by $20k–$30k per year per suite, sharpening hospital ROI and accelerating replacement cycles. These dynamics—higher field strength, greater material intensity, and lower lifecycle costs—structurally entrench medical imaging as the leading end-use for superconducting wire.

Competitive Landscape: Integrated System Suppliers, Legacy LTS Specialists and Rising HTS Manufacturers

The competitive field balances integrated system providers who both manufacture wire and deploy superconducting systems, long-standing LTS specialists servicing medical and high-field research markets, and global cable integrators focused on utility-scale HTS cable projects. Competitive differentiation rests on critical current density (Jc), conductor architecture (tape vs. round multi-filament), mechanical robustness for winding, cryogenic insulation systems, and vertically integrated system delivery.

American Superconductor Corporation (AMSC) - Integrated HTS Wire Producer and Grid Systems Integrator

AMSC combines production of 2G HTS wire (Amperium®) with turnkey grid solutions such as d-VARR® systems and superconducting Fault Current Limiters. The company leverages its vertical integration to capture value across supply and systems deployment, which is reflected in grid business contributing the majority of revenue (83% of recent quarterly revenue). AMSC’s strategy centers on using its own HTS conductors inside megawatt-scale systems-accelerating adoption by offering performance guarantees and reducing integration risk for utilities and defense customers.

Sumitomo Electric Industries - Established HTS Wire Manufacturer With Advanced Processing For Mechanical Strength

Sumitomo produces both BSCCO (1G) and ReBCO (2G) HTS wires, utilizing proprietary pressurized sintering and advanced processing to enhance critical current and mechanical properties. With a strong track record in early HTS power transmission projects, Sumitomo emphasizes supply-chain stability by focusing on non-rare-earth superconductors and robust conductor architectures suitable for utility verification campaigns. Their long history in cable and wire manufacturing supports scale and quality for grid and industrial magnet programs.

Furukawa Electric Co., Ltd. - Diversified Electrical Manufacturer Focusing On Fusion and High-Field Magnet R&D

Furukawa offers a broad portfolio spanning electrical and optical products and has recently intensified R&D on high-temperature assembled superconductors under national programs. The company’s partnership with Tokamak Energy and acquisition integration moves strengthen its position in the fusion magnet supply chain. Furukawa’s deep capabilities in conventional cable manufacturing and its expansion into superconducting R&D position it as a key supplier for future industrial-scale magnet projects and MVDC HTS infrastructure.

Nexans S.A. - HTS Cable Integrator Targeting MVDC and Urban Power Corridors

Nexans focuses on engineering, manufacturing and installing HTS cable systems, including the recent demonstration of 320 kV DC 3.2 GW HTS transmission-highlighting its ability to address large renewable integration use cases. Nexans’ system focus extends to data center power solutions where HTS low-voltage DC cables can dramatically reduce footprint. The company differentiates by coupling conductor technology with high-voltage insulation and turnkey installation capabilities for urban grid modernization projects.

Bruker Corporation - LTS Specialist Supplying Nbti/Nb3Sn For MRI, NMR and High-Field Research

Bruker is a leading provider of low-temperature superconducting (LTS) wire, including NbTi and Nb3Sn, serving clinical MRI and high-field NMR spectrometer markets. Its offering includes Bi-2212 round multifilament wire, a unique HTS product with isotropic, round-wire performance suitable for very high-field solenoids. Bruker’s focus on reliability, specialty conductor forms and tailored conductor profiles keeps it central to medical imaging manufacturers and to projects requiring proven, qualified LTS conductors for scientific and fusion research applications.

The United Kingdom has emerged as one of the most structurally important demand centers for the superconducting wire market in 2025, driven primarily by its sovereign commitment to commercial fusion energy and ultra-high-field research infrastructure. The government’s £410 million fusion investment under the “Plan for Change” has transformed superconducting wire from a research input into a strategic national material, particularly for 2G HTS REBCO-based tapes required in next-generation tokamak magnets. The STEP (Spherical Tokamak for Energy Production) program alone is expected to consume unprecedented volumes of high-current-density HTS wire for magnetic confinement systems operating beyond 20 tesla.

Procurement activity led by UK Industrial Fusion Solutions (UKIFS) entered a decisive execution phase in late 2025, with multi-hundred-million-pound contracts awarded for HTS-based magnet systems. Beyond fusion, the installation of 1.2 GHz NMR spectrometers at leading UK universities highlights parallel demand from life sciences and materials characterization, where only ultra-high-quality superconducting wire can sustain such extreme magnetic fields. Collectively, these developments position the UK as a volume anchor market for HTS wire, rather than merely an R&D hub.

South Korea – World-First Superconducting Power Grids for AI Data Centers

South Korea has become the global testbed for grid-scale superconducting wire deployment, uniquely linking HTS wire adoption to the explosive electricity demands of AI data centers. In July 2025, Korea Electric Power Corporation (KEPCO) signed a landmark MOU with LS Cable & System and LS Electric to launch the world’s first superconducting power grid dedicated to data center clusters. These systems leverage HTS cables to transmit massive power loads at low voltage, eliminating the need for land-intensive substations in dense urban zones.

Material innovation is equally strategic. The June 2025 partnership between Taihan Cable & Solution and SuperNode focuses on replacing traditional stainless-steel cryogenic sheaths with polymer-based designs, extending cooling station spacing by up to five times. This directly improves the economic viability of long-distance HTS cable systems. As LS Cable & System ramps commercial production of 2G HTS wire, South Korea is positioning itself as the first nation to monetize superconducting grids at scale, rather than through pilots alone.

United States – Naval Resiliency, Grid Hardening, and HTS Commercialization

The United States continues to be the innovation and revenue backbone of the global superconducting wire market, with demand anchored in naval defense, grid resiliency, and advanced power systems. In December 2025, American Superconductor (AMSC) completed its acquisition of Comtrafo, extending its reach into utility markets while reinforcing its dominance in superconducting-enabled power solutions. AMSC’s 53% year-over-year revenue growth to USD 222.8 million underscores the commercial maturity of superconducting wire-based systems, particularly fault current limiters and naval applications.

On the defense side, AMSC’s Ship Protection Systems (SPS)—built around superconducting degaussing coils—are being deployed across a wider share of the U.S. Navy fleet to enhance stealth and survivability. Parallel to this, the U.S. Department of Energy (DOE) continues to allocate over USD 100 million annually toward superconducting R&D, with a strong focus on reducing cryogenic energy penalties. This sustained funding ensures that HTS wire adoption in U.S. grids transitions from demonstration to utility-grade resilience infrastructure.

Japan – Frontier HTS Architectures and Hydrogen-Cooled Systems

Japan’s superconducting wire strategy in 2025 is defined by frontier applications, targeting aviation decarbonization, hydrogen energy systems, and fusion leadership. Under the New Energy and Industrial Technology Development Organization (NEDO) Frontier Development Project, Furukawa Electric and academic partners are advancing SCSC-IFB superconducting cables, designed for liquid-hydrogen-cooled generators in electric aircraft. This represents a significant departure from conventional liquid-nitrogen-cooled HTS systems.

Japan’s ambition extends into fusion through the FAST (Fusion by Advanced Superconducting Tokamak) project, unveiled between late 2024 and 2025. Supported by Fujikura, the program relies on high-uniformity REBCO tapes capable of sustaining extreme magnetic fields over long operational lifetimes. Fujikura’s improvements in batch repeatability and wire homogeneity are positioning Japan as a preferred supplier to international fusion startups, reinforcing its status as a technology frontier leader rather than a volume-driven market.

China – Strategic Mineral Integration and Urban HTS Deployment

China’s superconducting wire market is tightly integrated with its strategic mineral policy and non-ferrous metals industrial planning. The 2025–2026 growth plan targeting a 5% annual increase in non-ferrous metals value explicitly supports niobium and rare-earth supply chains essential for both LTS and HTS wire production. This vertical integration reduces exposure to imported feedstocks and enables cost-controlled scaling of superconducting materials.

At the research frontier, the Hefei Institute of Physical Science has reported breakthroughs in transition metal dichalcogenide superconductors, signaling long-term diversification beyond YBCO-based systems. Simultaneously, state-owned grid operators are expanding urban HTS cable pilots in cities such as Shanghai, using real-world load conditions to validate long-distance superconducting transmission. China’s approach emphasizes system-level deployment backed by mineral sovereignty, creating a structurally resilient domestic market.

Germany – Medical Imaging Manufacturing and European Research Backbone

Germany functions as the manufacturing and export nucleus for Europe’s superconducting medical and research infrastructure. In December 2025, Bruker Energy & Supercon Technologies announced USD 25 million in new orders from leading European research institutions, including the Max Planck Institute. These systems rely on both LTS and HTS wires to achieve ultra-high magnetic fields for battery research, solid-state chemistry, and life sciences.

Bruker’s continued expansion of its German and U.S. production sites reflects four-fold demand growth over the past decade, validating superconducting wire as a stable industrial market rather than a cyclical research niche. German institutes are also leading the deployment of 800 MHz to 1 GHz HTS-based NMR systems, reinforcing Germany’s role as the European anchor for high-field superconducting wire consumption.

2025 Strategic Comparison: Superconducting Wire National Matrix

Superconducting Wire National Matrix

|

Country

|

Primary Strategic Driver

|

2025 Key Milestone

|

Primary Material Focus

|

|

United Kingdom

|

Fusion energy scale-up

|

£410M fusion funding for STEP

|

2G HTS REBCO tapes

|

|

South Korea

|

AI data center power density

|

World’s first superconducting data center grid

|

HTS cables with polymer sheaths

|

|

United States

|

Naval resilience & grid hardening

|

AMSC–Comtrafo acquisition

|

HTS degaussing & FCL wires

|

|

Japan

|

Aviation decarbonization

|

NEDO hydrogen-cooled HTS launch

|

SCSC-IFB / REBCO

|

|

China

|

Material sovereignty

|

Non-ferrous metals growth plan

|

Rare-earth & niobium-based HTS

|

|

Germany

|

Medical & battery research

|

USD 25M Bruker MRI/NMR orders

|

Ultra-high-field LTS & HTS

|

Superconducting Wire Market Report Scope

Superconducting Wire Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2035)

|

$3 Billion

|

|

Market Growth Rate

|

8.9%

|

|

Segments

|

By Material Type (LTS, MTS, HTS, Iron-Based Superconductors), By Product Type (Monolithic Wires, Superconducting Tapes, Cable-in-Conduit Conductors, Insulated Strands & Enamelled Wires), By Application (Medical, Energy & Utilities, Research & Science, Transportation, High-Tech)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

American Superconductor Corporation, Bruker Energy & Supercon Technologies, Sumitomo Electric Industries Ltd., Fujikura Ltd., Luvata (Mitsubishi Materials), Furukawa Electric Co. Ltd., Nexans S.A., SuperOx, Theva Dünnschichttechnik GmbH, MetOx Technologies Inc., Western Superconducting Technologies Co. Ltd., Oxford Instruments plc, LS Cable & System Ltd., ASG Superconductors S.p.A., Japan Superconductor Technology Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Superconducting Wire Market Segmentation

By Material Type

- Low-Temperature Superconductors (LTS)

- Medium-Temperature Superconductors (MTS)

- High-Temperature Superconductors (HTS)

- Iron-Based Superconductors (IBS)

By Product Type

- Monolithic Wires

- Superconducting Tapes

- Cable-in-Conduit Conductors

- Insulated Strands & Enamelled Wires

By Application

- Medical

- Energy & Utilities

- Research & Science

- Transportation

- High-Tech

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Superconducting Wire Market

- American Superconductor Corporation

- Bruker Energy & Supercon Technologies

- Sumitomo Electric Industries, Ltd.

- Fujikura Ltd.

- Luvata (Mitsubishi Materials)

- Furukawa Electric Co., Ltd.

- Nexans S.A.

- SuperOx (Russia/Japan)

- Theva Dünnschichttechnik GmbH

- MetOx Technologies, Inc.

- Western Superconducting Technologies Co., Ltd.

- Oxford Instruments plc

- LS Cable & System Ltd.

- ASG Superconductors S.p.A.

- Japan Superconductor Technology Inc

*- List not Exhaustive