Market Overview: HTS Wire Scalability and Fusion Magnet Demand Propel the Superconducting Materials Market Outlook

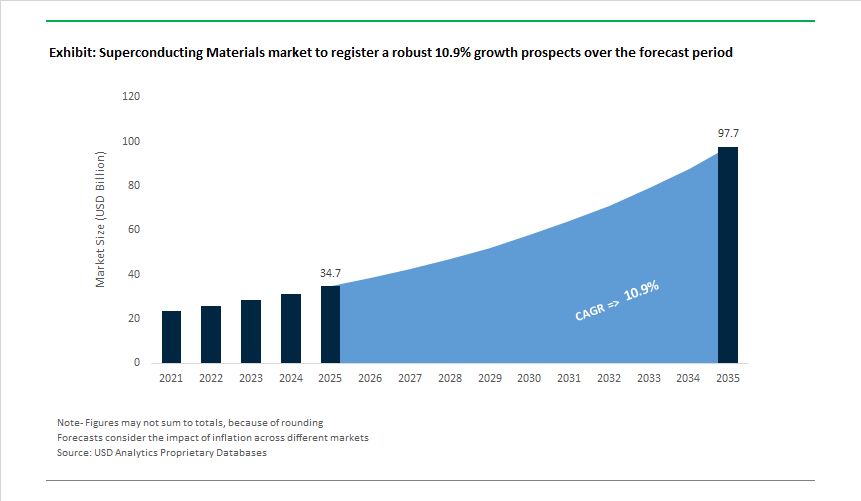

The Global Superconducting Materials Market is valued at USD 34.7 billion in 2025 and is projected to reach USD 97.6 billion by 2035, growing at a 10.9% CAGR as superconductivity moves decisively from laboratory-scale science into infrastructure-grade industrial deployment. The market’s momentum is being driven by a convergence of three forces: the scaling of high-temperature superconductors (HTS), the capital influx into fusion energy and high-field magnet systems, and the need for grid-level resilience solutions in increasingly electrified economies.

At the core of this shift is a technology-economic inflection point. High-temperature superconductors, particularly REBCO-based coated conductors, are changing the cost and feasibility equation for superconducting systems by operating at higher temperatures and enabling simpler, more energy-efficient cooling. This improvement is translating into lower system complexity, higher reliability, and improved lifetime economics, which in turn is expanding the addressable market well beyond traditional low-temperature superconducting (LTS) applications such as MRI systems.

The most visible demand accelerator is fusion energy development. Commercial fusion programs are no longer theoretical; they are material-intensive engineering projects. Compact, high-field magnet designs-now favored across next-generation fusion reactor architectures-require orders of magnitude more superconducting material than historical applications. As a result, superconducting wire demand is shifting from incremental growth to step-change scale requirements, placing HTS wire production capacity, yield, and long-length manufacturability at the center of supplier competitiveness.

In addition, power grid modernization is providing a second, structurally stable demand pillar. Utilities are increasingly evaluating superconducting technologies such as fault current limiters, superconducting magnetic energy storage (SMES), and high-capacity power cables to manage grid congestion, improve fault tolerance, and support renewable integration. These applications are not driven by efficiency alone, but by system reliability and response speed, particularly in dense urban networks and mission-critical infrastructure.

Market Analysis: Fusion Collaboration, HTS Wire Innovation, and Government Funding Drive Industry Acceleration

Market developments reflect a transformative phase for the Superconducting Materials Industry, driven by national energy security priorities, breakthroughs in HTS wire production, and significant public-private collaboration in fusion R&D. In November 2025, Furukawa Electric initiated full-scale R&D under a NEDO project to develop next-generation industrial superconductors capable of supporting ultra-high-field magnet performance. Concurrently in the United States, AMSC reported an 80% YoY revenue increase (Q1 2025), validating its strategic shift toward grid systems and defense applications that incorporate HTS Wire technologies. Also in October 2025, the U.S. Office of Electricity committed up to USD 15 million in funding for advanced energy storage initiatives-including HTS-based SMES-reinforcing the government’s role in shaping Electric Grid Resilience through superconducting technologies.

Fusion remains the most significant technological catalyst. In June 2025, Tokamak Energy and Furukawa Electric deepened their partnership to scale manufacturing for HTS Wire magnet systems, with direct implications for commercial fusion reactor development. Earlier in April 2025, the University of Tokyo initiated a multi-corporate research program to accelerate fusion materials science, engaging several leading Superconducting Materials producers. Defense applications continue to expand, supported by AMSC’s USD 75 million contract in February 2025 for superconducting magnet-based naval Ship Protection Systems (SPS).

Government-backed R&D momentum extended into Q4 2024, with the U.S. DOE significantly increasing funding for fusion magnets, HTS cable systems, and long-length conductor programs. In Europe, a major utility completed a successful pilot of an HTS Fault Current Limiter (FCL) in Q4 2024, validating the commercial readiness of HTS solutions for high-voltage substations.

Superconducting Materials Market Trends and Opportunities

Trend 1: Commercial-Scale Production of REBCO HTS Tapes for Fusion Energy

The transition from laboratory-scale fusion research to pilot and pre-commercial fusion reactors is fundamentally reshaping demand patterns in the superconducting materials market, with REBCO-based high-temperature superconducting (HTS) tapes emerging as the core enabling technology. Unlike legacy low-temperature superconductors, REBCO tapes can sustain extremely high current densities under intense magnetic fields, making them indispensable for compact, high-field fusion magnet systems. This shift has forced rapid industrialization of what was previously a niche, R&D-driven supply chain. In April 2025, the establishment of a dedicated HTS Tape Supply Framework for the UK’s STEP fusion program marked a structural inflection point, moving procurement away from ad-hoc research orders toward multi-supplier, industrial-scale contracting. Initial framework lots, valued at roughly £1.5 million each, were designed not only to secure material volumes but also to de-risk qualification across multiple vendors ahead of reactor construction timelines. Technical validation has reinforced this momentum. By late 2025, next-generation tokamak magnet systems demonstrated sustained magnetic fields approaching 12 Tesla at cryogenic temperatures near −243°C, using precision-wound REBCO conductors capable of handling millions of ampere-turns. These results confirmed current densities roughly 200 times higher than copper-based systems, validating REBCO as the only practical pathway for economically viable fusion-scale magnets. Capital flows have followed performance proof points: major private fusion developers raised substantial late-stage funding in 2025 specifically earmarked for HTS magnet scale-up, signaling confidence that superconducting materials are no longer a scientific bottleneck but a manufacturable, industrial input. As fusion timelines compress, REBCO tape production is shifting from specialty output to strategic infrastructure, with long-term implications for pricing discipline, supplier concentration, and cross-sector competition for capacity.

Trend 2: Material Optimization for Quantum Processor Qubit Coherence

In quantum computing, the industry narrative has pivoted decisively from headline qubit counts to the harder, more material-intensive challenge of qubit quality. Superconducting quantum processors are now constrained less by lithographic capability and more by energy loss mechanisms rooted in materials purity, thin-film interfaces, and substrate defects. As of 2025, commercial and near-commercial quantum processing units are targeting coherence times that enable deeper algorithm execution and practical error correction, placing unprecedented demands on superconducting materials engineering. Recent processor announcements demonstrate that qubit fidelities approaching 99.99% are achievable when atom-level control is applied to dopant placement and crystal lattice uniformity, dramatically reducing dielectric loss and environmental noise. Parallel progress is visible across industrial platforms, where standardized coherence times near 100 microseconds have become a baseline expectation rather than a research milestone. These gains are tightly coupled to advances in superconducting thin films—particularly aluminum and niobium layers—where interface roughness, oxide contamination, and grain boundary defects have historically limited performance. By late 2025, focused interface engineering programs showed measurable reductions in decoherence rates by minimizing interfacial oxides between superconducting films and silicon substrates. This materials-driven improvement is critical as the sector moves toward 100-qubit and beyond superconducting architectures, where aggregate system fidelity depends exponentially on individual qubit stability. As a result, superconducting materials suppliers are increasingly embedded upstream in quantum hardware roadmaps, with material qualification cycles now directly influencing processor commercialization timelines rather than being treated as interchangeable inputs.

Opportunity 1: Superconducting Cables for Resilient Urban Grid Links

Urban power infrastructure constraints are opening a high-impact deployment pathway for superconducting materials, particularly HTS cables designed to deliver transmission-scale power within existing rights-of-way. Conventional copper and aluminum conductors are reaching physical and thermal limits in dense cities, where expanding corridors is politically, economically, and socially infeasible. HTS cable systems address this constraint by delivering order-of-magnitude increases in power density without proportional increases in footprint. By 2025, technical benchmarks showed that a single HTS cable with a diameter under 20 centimeters can transmit more than 3 gigawatts of power—equivalent to multiple large power stations—while generating negligible heat and electromagnetic fields. This capability aligns directly with grid modernization priorities focused on resilience, redundancy, and climate adaptation. Public funding has become a decisive catalyst. U.S. federal grid programs launched in 2025 explicitly prioritize superconducting technologies for high-impact urban corridors, recognizing their ability to harden networks against extreme weather events and cascading failures. Operational case studies reinforce feasibility: superconducting grid projects demonstrated that transmission-level power can be delivered at distribution voltages, simplifying substation architecture and improving fault tolerance. As electrification accelerates across transport, data centers, and building systems, HTS cables represent a rare infrastructure solution where performance gains, permitting advantages, and long-term operating efficiency converge, creating a durable growth opportunity for superconducting materials beyond laboratory and scientific applications.

Opportunity 2: Ultra-Pure Niobium and High-RRR Aluminum for Particle Accelerators

Large-scale physics infrastructure is re-emerging as a multi-decade demand anchor for ultra-pure superconducting materials, particularly niobium-based alloys and high-residual-resistivity-ratio (RRR) aluminum. Next-generation particle accelerators and light sources require superconducting radiofrequency cavities and high-field magnets that operate with extreme efficiency under continuous duty cycles, leaving little tolerance for impurities or microstructural inconsistencies. The 2025 feasibility confirmation of future collider projects outlined unprecedented material requirements, including long lengths of high-field magnet conductors and thousands of superconducting cavities fabricated from ultra-high-purity niobium. These applications demand RRR values that ensure minimal resistive losses and stable cryogenic performance over decades of operation. In parallel, existing accelerator upgrades reached operational maturity in 2025, validating large-scale deployment of superconducting cavities and triggering follow-on material orders tied to user program expansion. Sustainability considerations are now influencing material design as well. Accelerator research roadmaps increasingly emphasize thin-film superconducting coatings on copper substrates, a strategy that preserves electromagnetic performance while significantly reducing cryogenic energy consumption. This approach not only lowers lifecycle operating costs but also broadens the supplier base capable of participating in accelerator material supply chains. Collectively, these developments position ultra-pure superconducting materials as long-cycle, high-specification products with stable demand profiles, offering suppliers insulation from short-term market volatility while anchoring long-term investment in advanced metallurgical and purification capabilities.

Market Share Analysis: Superconducting Materials Market

Market Share by Application: Medical Imaging Systems Anchor Nearly Half of Global Demand

The medical application segment, accounting for approximately 48% of the global superconducting materials market, remains the structural anchor of demand in 2025, driven almost entirely by the economics and upgrade cycle of Magnetic Resonance Imaging (MRI) infrastructure. Annual installation data from leading OEM supply chains confirms that more than 3,200 new MRI systems were deployed globally in the latest cycle, each system embedding several kilometers of high-purity superconducting wire and creating a predictable, recurring revenue stream for material suppliers. What sustains medical dominance is not unit growth alone, but field-strength escalation: hospitals are steadily migrating from legacy 1.5T scanners toward 3T, 7T, and ultra-high-field platforms, culminating in landmark installations such as 11.75 Tesla research-grade MRI systems, which require up to three times more superconducting material per unit. This intensity-per-system effect structurally favors the medical segment over emerging applications. At the same time, a 14-month global shortage of trained cryogenic engineers has reshaped procurement behavior—medical OEMs increasingly source pre-wound superconducting magnet modules instead of raw wire, shifting value capture upstream and raising average selling prices for integrated suppliers. Adjacent growth in proton beam therapy, where compact accelerator magnets rely heavily on NbTi superconductors, further reinforces healthcare as a high-margin, regulation-protected end market. Collectively, long equipment lifecycles, mandatory uptime requirements, and continuous performance upgrades ensure that medical imaging remains the most resilient and monetizable application segment within the superconducting materials ecosystem.

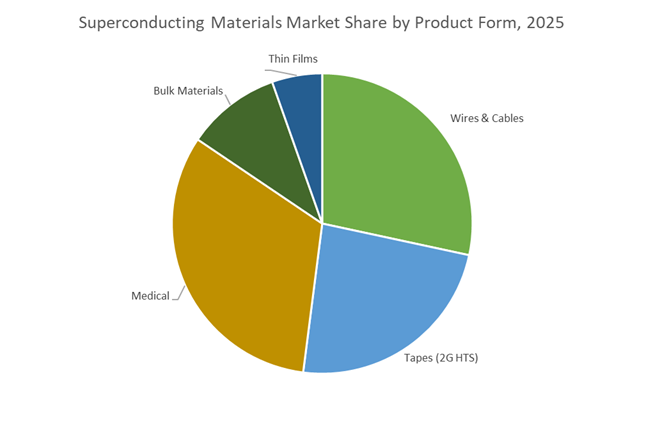

Superconducting Materials Market Share by Product Form

Competitive Landscape: Global HTS Leaders Expand Wire Technologies, Fusion Readiness, and Utility-Scale Deployments

The competitive landscape is characterized by vertically integrated superconducting wire manufacturers, grid-systems innovators, and companies advancing fusion-ready magnet technologies. Their strategic differentiation revolves around long-length conductor production, material purity, tensile strength optimization, cryogenic performance, and large-scale deployment for utilities, fusion, and defense programs.

Sumitomo Electric Industries - Pioneer in Long-Length HTS Wire With Demonstrated Grid-Level Integration

Sumitomo Electric remains one of the world’s foremost producers of oxide HTS wire and Bi-2223-based superconductors, with its DI-BSCCO™ Type HT-NX achieving tensile strengths up to 400 MPa at 77 K, essential for ultra-high-field magnet structures. The company holds the distinction of deploying the world’s first superconducting cable into a utility grid (2003), a testament to its early leadership in Electric Grid Resilience technologies. Sumitomo’s materials science expertise, built over centuries of copper refining excellence, underpins its capability to produce HTS conductors in continuous lengths up to 500 meters, enabling commercial scalability for large fusion magnets, power cables, and industrial magnet systems.

American Superconductor Corporation (AMSC) - HTS Wire Innovation Strengthens Grid, Wind, and Defense Portfolios

AMSC is leveraging its Amperium® 2G HTS Wire to expand in both grid modernization and defense applications. The company enhanced its market momentum after securing a USD 75 million SPS defense contract in early 2025, demonstrating the strategic value of superconducting magnet technology for naval mine countermeasures. Its HTS wire is available in copper, brass, and stainless steel laminations, the latter specifically optimized for Fault Current Limiter (FCL) applications where normal-state resistance is essential. AMSC’s pivot toward Gridtec® and Windtec® system integration has diversified revenue, while its historical success in deploying the world’s first commercial HTS cable (Columbus, Ohio) validates its long-standing role in advancing superconducting infrastructure.

Furukawa Electric - Expanding HTS Coated Conductor Capabilities To Accelerate Fusion Magnet Commercialization

Furukawa Electric’s strategic direction is strongly aligned with global fusion initiatives, supported by a £10 million investment in Tokamak Energy in 2024 and extensive experience supplying LTS Wire for major scientific programs including ITER. Its subsidiary SuperPower Inc. is a leading producer of REBCO Coated Conductors for high-density energy, medical imaging, and transportation applications. The company’s HTS portfolio is deeply integrated with Japan’s Fusion Energy Innovation Strategy, focusing on manufacturing scale-up, tensile strength improvement, and cryogenic efficiency enhancements to meet the performance thresholds required for commercial fusion reactor deployment.

Superconductor Technologies Inc. (STI) - Proprietary HTS Wire Processes Advance Cost-Effective 2G Conductor Manufacturing

STI leverages a robust intellectual property base of 100+ patents in HTS materials, RF filters, and cryogenic technologies. Its RCE-CDR manufacturing platform enables precise control of 2G HTS Wire properties, targeting high-yield, low-cost production suitable for motors, generators, and next-generation power electronics. STI has introduced innovations such as the patented enhancement technique improving Conductus® HTS wire performance in high magnetic fields through intrinsic pinning. Although historically focused on telecommunications-with 1,700+ SuperFilter® RF systems deployed globally-the company has increasingly pivoted toward power and industrial applications where HTS materials offer compelling performance advantages.

The United States is setting the global pace in high-temperature superconducting (HTS) materials commercialization, driven primarily by private fusion energy capital and defense-backed procurement frameworks. The most decisive catalyst in 2025 has been the acceleration of REBCO (2G-HTS) tape production, as ultra-high-field magnet demand moves from experimental labs into pre-commercial fusion reactors. The $863 million Series B2 funding round closed by Commonwealth Fusion Systems in August 2025 underscores how superconducting materials have become the rate-limiting input for fusion scale-up. These funds are directly tied to the SPARC tokamak, which relies on REBCO magnets exceeding 20 tesla, a threshold unattainable with legacy low-temperature superconductors.

Parallel to private capital, the U.S. Department of Energy (DOE) has reinforced materials innovation through FIRE and INFUSE awards, channeling public funding into radiation-tolerant HTS tapes suitable for fusion neutron environments. On the defense side, American Superconductor (AMSC) has translated HTS know-how into near-term revenues, with naval ship protection systems and grid stabilization applications driving a >20% year-over-year revenue increase in 2025. Collectively, the U.S. market is defined by vertical integration between materials science, magnet manufacturing, and end-use systems, reducing time-to-deployment for next-generation superconducting infrastructure.

China – Industrial Self-Sufficiency and Scale Economics in HTS

China’s superconducting materials strategy in 2025 reflects the culmination of Made in China 2025, with HTS now treated as a foundational industrial input rather than a research material. The Shanghai High-Quality Materials Plan (2025–2027) formally elevated high-temperature superconductors into one of five priority industrial clusters, signaling state-backed commitment to mass manufacturing of REBCO and MgB₂ conductors. Unlike Western markets driven by fusion startups, China’s demand profile is anchored in smart grids, MRI systems, and large-scale power applications, where volume and cost control are decisive.

A structural advantage lies in China’s dominance over rare earth purification, allowing domestic producers to supply 99.99%+ purity rare-earth oxides for REBCO tapes at 40–50% lower cost than Western competitors. At the same time, national policy targets raising domestic content of core “new materials,” including superconductors, to 70% by end-2025, accelerating substitution away from imported HTS components. As a result, China is positioning itself as the lowest-cost global supplier of HTS conductors, with scale economics likely to shape international pricing once export controls stabilize.

Japan – Precision Manufacturing and Infrastructure-Led Demand

Japan continues to differentiate itself through manufacturing precision and materials reliability, particularly in Bi-2223 (1G-HTS) wire, where it retains unmatched process maturity. Sumitomo Electric Industries reaffirmed its commitment to bismuth-based HTS in 2025, emphasizing its pressurized sintering technology that enables high-volume production without reliance on costly rare earths. This approach provides Japan with a strategic hedge against rare-earth supply volatility while serving applications where mechanical flexibility and long-length uniformity are critical.

Infrastructure remains a defining demand driver. The L0 Series Maglev program, operated by Central Japan Railway Company, continues to validate superconducting magnets at commercial scale, with 2025 efforts focused on cooling efficiency and lifecycle cost reduction. Complementing this, research initiatives led by National Institute for Materials Science (NIMS) are applying AI-driven discovery tools to reduce dependence on heavy rare earths in HTS formulations. Japan’s market is thus characterized by incremental, reliability-focused scaling, rather than disruptive capacity expansion.

South Korea – Grid-Scale Validation and Fusion Performance Leadership

South Korea has emerged as the global benchmark for real-world superconducting deployment, particularly in HTS power transmission. The validation of a 154 kV-class superconducting cable by the Korea Electrotechnical Research Institute (KERI) represents a decisive transition from pilot demonstrations to utility-grade infrastructure. Operating with near-zero transmission loss over a one-kilometer span, this system now serves as the technical blueprint for South Korea’s planned nationwide Super Grid upgrade.

In parallel, fusion research has reinforced domestic demand for advanced superconducting magnets. The Korea Institute of Fusion Energy (KFE) reported sustained 100 million °C plasma operation in the KSTAR reactor during 2025, a performance milestone made possible by continuous optimization of its superconducting magnet systems. Recognizing this strategic convergence, the South Korean government formally designated superconducting materials as a National Strategic Technology, unlocking preferential tax credits and accelerated R&D funding. This policy alignment positions South Korea as the leading validation market for HTS systems at grid and reactor scale.

United Kingdom – Commercial Fusion Magnets and IP Monetization

The United Kingdom has consolidated its role as a global fusion commercialization hub, with superconducting materials innovation concentrated around Oxfordshire. Tokamak Energy closed 2025 with record-breaking performance from its ST40 device, including the highest fusion triple product achieved by a privately operated tokamak. These results have directly elevated demand for compact, high-current HTS magnet systems, prompting a strategic pause for the $52 million LEAPS upgrade co-funded with U.S. and UK partners.

A defining market development has been the licensing of Tokamak Energy’s proprietary HTS cable technology to Type One Energy, signaling a shift toward intellectual property monetization rather than sole in-house deployment. Following re-entry into Horizon Europe, UK research groups also secured new funding streams in late 2025 to lead consortia targeting superconducting solutions for climate, mobility, and quantum systems. The UK market is therefore distinguished by IP-led growth, bridging fusion R&D and exportable superconducting technologies.

Germany – Cryogenic Systems and European HTS Manufacturing Backbone

Germany functions as the engineering backbone of Europe’s superconducting ecosystem, specializing in cryogenics, precision manufacturing, and system integration. In 2025, companies such as Theva and Bruker Corporation expanded 2G-HTS tape production, responding to rising demand from quantum computing startups, MRI manufacturers, and accelerator facilities across the EU. This expansion reflects Germany’s role as a reliable supplier of industrial-grade HTS conductors, rather than experimental prototypes.

Public-sector support has reinforced deployment pathways. The Federal Ministry for Economic Affairs and Climate Action (BMWK) concluded the latest phase of the SuperLink project in 2025, demonstrating superconducting cable integration in urban grids with energy loss reductions approaching 5%. At the frontier of high-energy physics, collaboration with CERN has validated German-developed HTS links for the High-Luminosity LHC upgrade, proving durability under extreme radiation loads. Germany’s market strength lies in system reliability, cryogenic excellence, and pan-European industrial deployment.

2025 Strategic Comparison: Superconducting Materials by Country

Superconducting Materials by Country

|

Country

|

Primary Material Focus

|

2025 Strategic Milestone

|

Key Application

|

|

United States

|

REBCO (2G-HTS)

|

$863M CFS Series B2; DOE FIRE awards

|

Commercial fusion, naval defense

|

|

China

|

REBCO / MgB₂

|

Shanghai 2025–27 HTS industrial plan

|

Smart grids, MRI systems

|

|

Japan

|

Bi-2223 (1G-HTS)

|

Sumitomo pressurized sintering scale-up

|

Maglev, energy efficiency

|

|

South Korea

|

HTS power cables

|

154 kV zero-loss grid validation

|

Urban transmission, fusion

|

|

United Kingdom

|

HTS magnet systems

|

Tokamak Energy magnet licensing

|

Fusion energy, quantum tech

|

|

Germany

|

2G-HTS & cryogenics

|

SuperLink urban grid integration

|

Accelerators, quantum computing

|

Superconducting Materials Market Report Scope

Superconducting Materials market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$34.7 Billion

|

|

Market Size (2035)

|

$97.6 Billion

|

|

Market Growth Rate

|

10.9%

|

|

Segments

|

By Material Type (Low-Temperature Superconductors [LTS], High-Temperature Superconductors [HTS]), By Product Form (Wires & Cables, 2G HTS Tapes, Bulk Materials, Thin Films), By Application (Medical, Energy & Power, Research & Fusion, Transportation, Electronics), By Sales Channel (Direct Sales [OEMs], Indirect / Distributor Sales)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

American Superconductor Corporation, Bruker Energy & Supercon Technologies, Sumitomo Electric Industries Ltd., Furukawa Electric Co. Ltd., Fujikura Ltd., Nexans SA, Western Superconducting Technologies Co. Ltd., Tokamak Energy / TE Magnetics, Luvata (Mitsubishi Materials), ASG Superconductors SpA, Metamaterial Inc., Oxford Quantum Circuits, Commonwealth Fusion Systems, Hyper Tech Research Inc., Can Superconductors

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Superconducting Materials Market Segmentation

By Material Type

- Low-Temperature Superconductors (LTS)

- High-Temperature Superconductors (HTS)

By Product Form

- Wires & Cables

- Tapes (2G HTS)

- Bulk Materials

- Thin Films

By Application

- Medical

- Energy & Power

- Research & Fusion

- Transportation

- Electronics

By Sales Channel

- Direct Sales (OEMs)

- Indirect / Distributor Sales

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Superconducting Materials Market

- American Superconductor Corporation

- Bruker Energy & Supercon Technologies

- Sumitomo Electric Industries, Ltd.

- Furukawa Electric Co., Ltd.

- Fujikura Ltd.

- Nexans SA

- Western Superconducting Technologies Co., Ltd.

- Tokamak Energy / TE Magnetics

- Luvata (Mitsubishi Materials)

- ASG Superconductors SpA

- Metamaterial Inc.

- Oxford Quantum Circuits

- Commonwealth Fusion Systems

- Hyper Tech Research Inc.

- Can Superconductors

*- List not Exhaustive