Market Overview: High-Field Magnet Performance Metrics Accelerating Adoption in MRI, Fusion Energy & Cryogen-Free Systems

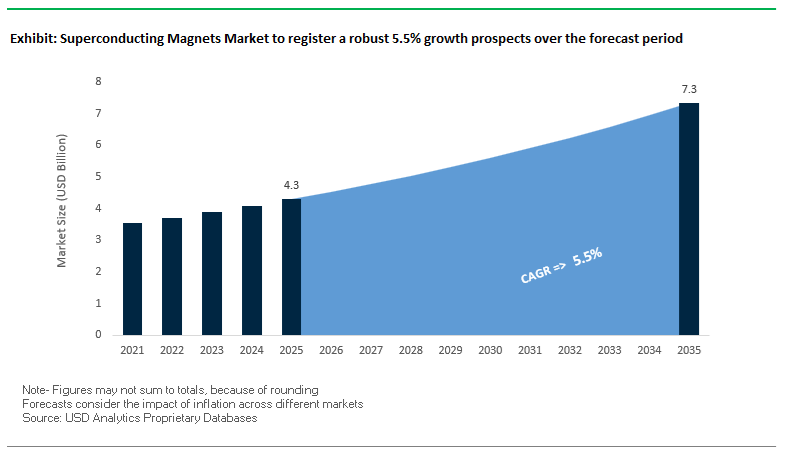

The Superconducting Magnets Market is projected to grow from USD 4.3 billion in 2025 to USD 7.3 billion by 2035, advancing at a CAGR of 5.5%. Growth is driven by increasing penetration of high-field magnets in medical imaging, fusion research, particle accelerators, mass spectrometry, and quantum research, combined with the rapid commercialization of cryogen-free superconducting magnet systems that reduce operational and infrastructure costs. Manufacturers and vendors are focusing on LTS (Low-Temperature Superconductors) such as NbTi and Nb₃Sn, while next-generation HTS materials (YBCO, BSCCO) expand the market’s performance limits.

The market is technically defined by breakthrough field target thresholds: commercial NbTi LTS magnets typically produce <15 T at 4.2 K, whereas Nb₃Sn-based systems exceed 20 T, enabling their deployment in fusion projects and high-energy physics applications. MRI systems, the largest application segment, continue to standardize around 1.5 T and 3.0 T, ensuring optimal signal-to-noise ratio and clinical diagnostic quality. Meanwhile, the ITER Central Solenoid—the world’s most powerful pulsed superconducting magnet—demonstrates the extreme material intensity of the sector, integrating 40 metric tons of Nb₃Sn conductor.

Cryogen-free magnets are rapidly adopted due to the helium supply constraints, with advanced systems operating at 20 K using closed-loop cryocoolers, eliminating periodic liquid helium refills and reducing total cost of ownership.

Key Insights for Manufacturers & Vendors

- NbTi vs. Nb₃Sn Field Strength: NbTi magnets <15 T; Nb₃Sn magnets exceed 20 T, becoming the standard for fusion and accelerator systems.

- MRI Market Anchor: Clinical MRI operates at 1.5–3 T, representing the highest commercial magnet volume globally.

- Fusion Demand Surge: ITER Central Solenoid reaches 13 T, using 40 metric tons of Nb₃Sn, signaling massive material requirements.

- Cryogen-Free Momentum: HTS-based and dry-cooled magnets achieve stability at 20 K, eliminating liquid helium dependency.

- Grid Modernization: SMES systems increasingly piloted by power utilities to strengthen instant-response grid stability.

Market Analysis: High-Field Magnet Deployments, Helium-Reduction Breakthroughs & HTS Conductor Advances Shape Global Growth

The global superconducting magnets ecosystem continues to evolve through significant R&D progress, strategic investments, and downstream deployments across energy, medical imaging, and scientific research. In August 2025, General Atomics completed the final ITER Central Solenoid modules—establishing the world’s largest pulsed superconducting magnet, a landmark achievement driving global recognition of Nb₃Sn technology in fusion energy science. This milestone reinforces the massive scaling potential of superconducting magnets for high-energy systems requiring precise plasma confinement.

Advancements in MRI continue to shape the commercial landscape. In February 2025, GE HealthCare launched a 3.0T MRI system with a 67% reduction in helium usage, significantly lowering siting requirements and offering more sustainable magnet lifecycle economics. Siemens Healthineers further advanced the market in February 2024 with Magnetom Flow, a 1.5T MRI system operating on a closed helium circuit of just 0.7 liters with no quench pipe required, leveraging DryCool technology to minimize installation constraints in urban hospitals.

The HTS domain is witnessing rapid breakthroughs as well. In December 2025, researchers successfully engineered BSCCO-based HTS superconductors incorporating GaP quantum dots as flux pinning centers, delivering major gains in critical current density (Jc) for ultra-high-field magnet applications. Earlier, in September 2024, Oxford Superconducting Technology reported non-copper Jc ≈ 2,900 A/mm² at 12 T for next-gen Nb₃Sn wires—pushing the limits of LTS magnet performance for high-energy physics.

Government funding remains a powerful accelerator. In Q3 2025, the U.S. allocated USD 240 million to the ITER program, reaffirming long-term investment in fusion energy technologies dependent on high-performance superconducting magnets. Across Europe, January 2025 marked expanding pilot deployments of SMES systems as power grid operators explore instantaneous energy storage to support renewables and reduce grid instability risks.

Downstream adoption is also rising. In November 2025, Bruker Corporation confirmed the deployment of its 21 T FT-ICR mass spectrometry system at a national laboratory—highlighting the growing demand for ultra-high-field magnets in structural biology and chemical analysis research.

Next-Generation Advancements in HTS Fusion Magnets, Quantum Computing Stability, Cryogen-Free MRI Systems, and High-Power Electric Aviation

Market Trend 1: Acceleration of High-Temperature Superconductor (HTS) Magnet Deployment for Compact Nuclear Fusion Systems

A dominant trend transforming the Superconducting Magnets Market is the global pivot toward REBCO-based HTS magnets, which enable unprecedented magnetic field strengths for next-generation fusion reactors. The core performance differentiator lies in their ability to generate on-axis magnetic fields exceeding 10 Tesla and withstand peak conductor fields above 20 Tesla, creating compact reactor geometries that significantly reduce system mass and capital requirements. Unlike conventional NbTi or Nb₃Sn low-temperature superconductors, HTS conductors operate efficiently at 20–30 K, avoiding the extreme cryogenic burden of 4.2 K liquid helium systems. This temperature flexibility unlocks major reductions in refrigeration power consumption and system complexity.

Equally impactful is the ultra-high critical current density (Jc) of REBCO tapes, now exceeding 1,000 A/mm² at 20 K and 20 T, enabling the densely packed coil architectures essential for high-field fusion tokamaks and stellarators. These performance benchmarks underpin multi-billion-dollar fusion initiatives globally—where HTS magnets directly enable higher confinement efficiency, reduced reactor size, and accelerated commercialization timelines. As fusion startups and national programs transition from conceptual design to prototype builds, HTS magnetization is emerging as the pivotal supply-chain and technology driver shaping the industry’s next decade.

Market Trend 2: Advancement of Ultra-Stable, Low-Noise Superconducting Magnets for Commercial Quantum Computing Platforms

Quantum computing imposes some of the strictest magnetic field uniformity and stability requirements of any industry, and this is driving rapid innovation in low-noise superconducting magnet architectures. For qubit arrays—particularly transmons—field uniformity must achieve <1 ppm homogeneity across the operational volume to ensure identical qubit frequency response and minimize systematic error. Equally critical is temporal magnetic stability, with commercial systems requiring <0.1 ppm drift per hour to preserve qubit coherence times (T₂) and prevent decoherence-induced operational failures.

Noise suppression is another defining metric. Quantum processors demand magnets engineered to achieve magnetic noise floors below 1 μT, necessitating vibration isolation, EMI shielding, and advanced current stabilization electronics. The operational environment compounds the challenge: superconducting qubits run at 10–50 mK, placing stringent requirements on cryostat–magnet integration to avoid thermal gradients and vibration transfer. These technical constraints are fueling adoption of specialized low-noise HTS and hybrid magnet systems designed specifically for quantum computing laboratories and commercial cloud-based quantum services.

Market Opportunity 1: Expansion of Cryogen-Free, Conduction-Cooled Superconducting Magnets for MRI and Semiconductor Processing

The shift toward cryogen-free systems represents one of the most commercially scalable opportunities in the Superconducting Magnets Market. Traditional MRI and analytical magnets rely heavily on liquid helium, a resource that is increasingly expensive and supply-constrained. Conduction-cooled magnets—powered by GM or Pulse Tube cryocoolers—achieve the required low-temperature environment without helium baths. These cryocoolers deliver ≈40 K at the first stage for thermal shields and 3–4 K at the second stage for LTS coils, making them ideal for industrialization.

The engineering benefit lies in thermal load reduction: conduction-cooled magnets typically operate with <1 W heat load at 4 K, enabling long-term, maintenance-free operation. Commercial cryogen-free magnets already achieve 3–10 Tesla field strengths, suitable for MRI, wafer metrology, ion implantation, and analytical spectroscopy. As semiconductor manufacturing pushes toward nanometer-scale precision, the demand for stable, cryogen-free superconducting magnet systems for beam steering, lithography alignment, and high-resolution inspection tools is accelerating—creating a robust multi-industry adoption runway.

Market Opportunity 2: Integration of Superconducting Magnets into High-Efficiency Electric Motors for Aviation and Megawatt-Class Propulsion

Superconducting magnets are emerging as a breakthrough pathway to achieving the power density and efficiency targets required for electric aviation. High-field superconducting motor topologies can achieve 10–20 kW/kg power density, far surpassing the 3–5 kW/kg range typical of permanent magnet machines used in today’s electric vehicles. This performance leap directly translates into lighter propulsion units, greater payload, and extended flight range—key metrics for next-generation regional aircraft, hybrid-electric jets, and eVTOL platforms.

HTS-based propulsion motors also achieve ≈99% electrical efficiency, drastically reducing thermal losses and simplifying cooling architecture for megawatt-scale electric propulsion systems. Their high current-carrying capacity—100–300 A per HTS conductor at operating conditions—enables compact stator and rotor designs suited to aviation-grade power density requirements. As aerospace OEMs push toward commercializing hybrid-electric and fully-electric aircraft, superconducting magnet-integrated propulsion systems represent one of the most disruptive technological opportunities in the sector.

Superconducting Magnets Market Share Analysis

Market Share by Conductor Material: Low-Temperature Superconductors Dominate Due to Proven High-Field Stability and Scalable Manufacturing

Low-Temperature Superconductors (LTS), led by Niobium-Titanium (NbTi) and Niobium-Tin (Nb₃Sn), hold an estimated 75% share of the global superconducting magnets market in 2025, reflecting their long-term commercial maturity, unmatched reliability, and cost-effective scalability for high-field magnet applications. Their continued dominance is anchored in decades of engineering refinement, stable global supply chains, and consistent performance in high-volume magnetic systems that require precise field uniformity. Unlike High-Temperature Superconductors (HTS), which still face manufacturing complexity and significantly higher material costs, LTS materials deliver a superior cost-to-performance ratio, especially for magnets operating below 9 Tesla, where the vast majority of medical and scientific systems are deployed. Their ability to generate exceptionally homogeneous magnetic fields makes them the preferred conductor material for MRI systems, nuclear magnetic resonance (NMR) instruments, and accelerator technologies, where field instability directly compromises imaging or research quality. Even though LTS magnets require liquid helium cooling at 4.2 K, the overall lifecycle cost remains more predictable and economical than HTS-based systems, sustaining LTS leadership in both revenue and installed-base share. As global demand for high-field systems expands across healthcare diagnostics, quantum research, and materials characterization, LTS remains the foundational technology enabling commercially deployable superconducting magnet systems.

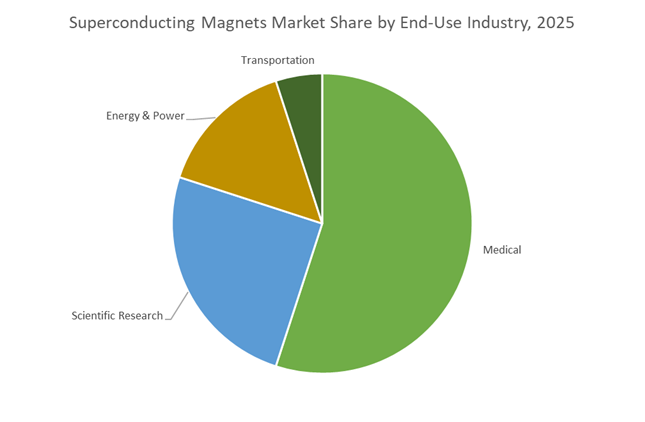

Market Share By End-Use Industry: Medical Sector Leads Through MRI System Dependence on High-Field Superconducting Magnets

The medical sector, representing approximately 55% of the total superconducting magnets market, is the uncontested leader in end-use share due to its complete reliance on superconducting magnet technology for Magnetic Resonance Imaging (MRI) systems. MRI remains one of the fastest-growing diagnostic modalities worldwide, driven by the rising incidence of chronic diseases, demand for early-stage detection, and expanding access to advanced imaging infrastructure across emerging economies. Superconducting magnets—primarily LTS-based—are indispensable for producing the 1.5 Tesla and 3.0 Tesla magnetic fields required for high-resolution soft tissue imaging. No alternative magnet technology provides the combination of field strength, stability, bore size compatibility, and operational uniformity needed for clinical MRI, ensuring that superconducting magnets remain the technical backbone of this multi-billion-dollar diagnostic industry. With the MRI superconducting magnet market valued at nearly $2 billion in 2024 and projected to grow steadily, the healthcare segment continues to generate the highest revenue share and the most consistent long-term demand. Moreover, emerging trends such as 7 Tesla clinical MRI adoption, portable superconducting MRI systems, and helium-free cooling innovations are expected to reinforce the medical sector’s dominance by expanding MRI deployment into new clinical and research environments.

Country Analysis: Global Superconducting Magnet Hotspots and Strategic Technology Leadership

United States: Fusion-Driven HTS Development and Next-Generation Superconducting Magnet Manufacturing

The United States has rapidly strengthened its position in the superconducting magnets market, driven by large-scale public investments in fusion energy, cryogenics, and high-temperature superconductors (HTS). A major milestone was achieved in August 2025, when General Atomics completed and delivered the final module of the ITER Central Solenoid, the world’s largest and most powerful pulsed superconducting magnet. This advancement underscores the U.S. commitment to next-generation fusion systems and validates domestic capability in high-precision superconducting coil engineering. Parallel to fusion R&D, the U.S. Department of Energy (DOE) has been funding HTS innovation, directing investment toward companies such as MetOx International to accelerate domestic production of rare and critical HTS conductors required for future fusion reactors and resilient smart grid networks.

The U.S. is also a leader in superconducting magnet innovation for medical imaging. In February 2025, GE HealthCare introduced the Freelium MRI platform, a sealed superconducting magnet design that uses less than 1% of the liquid helium required by traditional MRI systems—marking a transformative step toward sustainable, helium-independent magnets. Defense-related applications further strengthen the U.S. opportunity landscape. In November 2025, the Department of Commerce issued a preliminary intent to allocate $50 million under the CHIPS and Science Act to expand domestic production of rare earth materials supporting high-performance permanent magnet systems, a complementary technology essential in EUV lithography and advanced defense equipment. Collectively, the U.S. market benefits from strong policy support, advanced fusion programs, and aggressive commercialization of low-helium superconducting magnet platforms.

European Union / France: ITER Leadership and Large-Scale Nb₃Sn Magnet Innovation for Global Fusion Commercialization

The European Union—led by France as the host country for ITER—continues to shape the future of global superconducting magnet development through commanding participation in the world’s largest fusion experiment. In April 2025, the ITER Organization announced the completion of all pulsed superconducting magnet components, including massive Niobium-Tin (Nb₃Sn) coils engineered for the Tokamak’s central magnetic system. EU industry has been instrumental in designing, manufacturing, and testing a significant share of these magnets, reinforcing Europe’s dominance in large-scale superconducting coil fabrication and cryogenic integration.

Policy frameworks are rapidly evolving. The 2024 Draghi Report urged the European Commission to adopt a unified strategy for fusion energy commercialization, pushing for public-private partnerships that leverage ITER’s magnet expertise to accelerate next-generation reactor designs. Concurrently, European industrial capability in HTS manufacturing is strengthening. Germany’s Theva Dünnschichttechnik GmbH reached a milestone in March 2024, reporting over 1,000 km/year of HTS wire production—an achievement that directly supports European ambitions in superconducting cables, industrial magnets, and emerging power grid applications. The EU therefore combines the world’s most advanced fusion testbed with a maturing, strategically coordinated supply chain for high-field superconducting magnet technologies.

Japan: Ultra-High Field Magnet Leadership and Precision LTS/HTS Wire Manufacturing Capacity

Japan remains a global leader in low-temperature superconductors (LTS) and ultra-high-field superconducting magnet innovation, driving the most advanced scientific instruments and medical imaging systems. In July 2024, Japan Superconductor Technology (JASTEC) achieved a world record by producing an HTS magnet with a field strength of 45.5 Tesla, confirming its global leadership in extreme-field applications such as nuclear magnetic resonance (NMR), condensed-matter physics, and advanced MRI platforms. This milestone parallels Japan’s longstanding excellence in the polymer-derived precursor methods essential for producing high-purity SiC filaments and precision LTS wires.

Industrial expansion continues to accelerate. Fujikura Ltd. announced a 300% capacity increase in HTS conductor manufacturing in October 2024, targeting growing demand from smart grids, compact medical systems, and high-efficiency power electronics. Meanwhile, Sumitomo Electric Industries formed a joint venture in January 2024 to integrate next-generation superconductors into grid-level energy systems, highlighting Japan’s strategic shift from research-heavy activity toward scaled commercial deployment. Japan’s combination of manufacturing precision, material purity, and ultra-high field research strengthens its position as a global hub for premium superconducting wire and advanced magnet solutions.

China: Accelerating HTS Industrialization and Strategic Expansion of Maglev and Fusion Magnet Capabilities

China is aggressively scaling its superconducting magnet infrastructure through strategic government policy, major HTS conductor investments, and a national push to commercialize magnetic levitation (Maglev) transportation. In June 2024, Shanghai Superconductor Technology completed qualification testing for HTS conductors designed for fusion reactor magnets—signifying China’s readiness to support domestic fusion initiatives and reduce foreign reliance for critical superconducting inputs. These HTS advances align with broader state policies aimed at enabling China to develop proprietary superconductor supply chains and advance its ambitions in clean energy transformation.

China continues to dominate large-scale implementation of superconducting technologies, particularly in transportation. Ongoing investments into Maglev rail systems depend heavily on robust low-temperature superconducting (LTS) magnets capable of sustaining high operational stability and long-duration magnetic fields. The rapid industrialization of superconducting materials also supports applications in petrochemical processing, metallurgy, and power transmission. With expanding domestic capacity, strong policy incentives, and significant R&D investment, China is positioning itself as a strategic global supplier of HTS and LTS materials for fusion, infrastructure, and next-generation mobility.

South Korea: ITER Partnership and HTS Cable Innovation for Smart Grid and High-Power Infrastructure

South Korea expands its influence in the superconducting magnets market through deep participation in the ITER fusion program and focused development of high-temperature superconducting cables for modern energy infrastructure. Korean institutes are advancing HTS cable designs optimized for smart grids, where lightweight, low-loss conduction offers substantial benefits for high-density urban power networks. These technologies support Korea’s broader electrification strategy, which includes resilient renewable integration and high-capacity power transport.

As an ITER partner, South Korea contributes to complex engineering tasks and component development for fusion-class superconducting magnets, elevating its technical capabilities in cryogenics, magnet materials, and advanced cable systems. This dual expertise—fusion and power grid innovation—positions South Korea as a rising global competitor in HTS magnet technology and energy-efficient superconducting infrastructure solutions.

Germany: High-Precision HTS Magnet Systems and Industrial MRI Leadership

Germany’s superconducting magnet market is underpinned by a strong industrial base specializing in high-field MRI technologies, precision testing equipment, and specialized HTS magnet systems for industrial and research applications. German engineering firms leverage the country’s deep materials science ecosystem to develop compact, high-stability superconducting magnets that meet stringent performance requirements in nondestructive testing, materials diagnostics, and medical imaging.

German participation in the broader EU superconducting materials ecosystem—particularly through Horizon Europe and Fraunhofer institutes—strengthens national capability in superconducting coil manufacturing, cryogenic integration, and system-level magnet design. As Germany expands its expertise into HTS magnets for power systems, industrial testing, and compact MRI units, it remains a critical player in Europe’s high-field superconductivity landscape.

Competitive Landscape: Global Leaders Strengthening Superconducting Magnet Technology for MRI, Fusion, Energy Storage & Research

The competitive landscape is defined by companies specializing in LTS/HTS conductor manufacturing, MRI magnet production, fusion energy magnet systems, and cryogen-free scientific research platforms. Growth is increasingly shaped by material innovation, helium-free magnet architectures, vertical integration, and in-house wire production capabilities that allow suppliers to tailor magnetic field performance for specialized applications.

GE HealthCare – Advancing Low-Helium MRI Magnet Design

GE HealthCare is a global leader in superconducting MRI magnets, especially in the 1.5T and 3T clinical imaging categories. Its SIGNA™ Hero 3.0T platform incorporates a 67% reduction in helium usage, enabling lower siting costs and improving hospital installation efficiency. GE integrates deep learning reconstruction (AIR™ Recon DL) to improve image clarity while maintaining a 70 cm wide bore for patient comfort. Its strategic emphasis on low-helium and zero-boil-off magnet systems positions GE as a sustainability-focused innovator in the medical imaging magnet segment. The company’s focus on high-end clinical scanners reinforces its leadership in high-field healthcare applications.

Siemens Healthineers – Pioneering Dry-Cooled & Near-Zero Helium MRI Technologies

Siemens Healthineers stands out for its DryCool Technology, eliminating the conventional quench pipe and reducing helium content to just 0.7 liters in the Magnetom Flow 1.5T platform launched in February 2024. With vertical integration through Siemens Healthineers Magnet Technology (UK), the company designs and manufactures magnets ranging from 0.55T low-field systems to 7T ultra-high-field research platforms. This integration strengthens quality control and accelerates innovation cycles. Siemens is strategically focused on sustainable, cryogen-independent MRI technology, reinforcing its competitive position among healthcare providers seeking operational flexibility.

Bruker Corporation – Ultra-High-Field Magnet Specialist for NMR & FT-ICR

Bruker is a premier supplier of superconducting magnets for NMR spectroscopy, FT-ICR mass spectrometry, and advanced scientific research. The company leads in ultra-high-field magnet development, having built the world’s first 21.0 T FT-ICR magnet. Bruker’s competitive advantage is strengthened by its vertical integration in LTS and HTS wire production, including NbTi, Nb₃Sn, and Bi-2212 HTS conductors, enabling highly customized magnet solutions. Its systems deliver exceptional field uniformity and stability, making Bruker an essential technology provider for national laboratories and research institutions.

General Atomics – Global Leader in Fusion-Scale Pulsed Magnet Systems

General Atomics is recognized for engineering some of the world’s most demanding fusion magnet systems, particularly for ITER. The firm recently completed the ITER Central Solenoid, each module carrying >600 MJ of stored magnetic energy. GA’s expertise in high-temperature superconducting (HTS) magnet R&D positions it to supply future commercial fusion reactors. The company’s experience in manufacturing large-scale pulsed magnets provides a strategic advantage as nations expand investment in fusion infrastructure and high-field confinement systems.

Oxford Instruments NanoScience – Cryogen-Free Magnet Pioneer for Quantum & Materials Research

Oxford Instruments NanoScience specializes in Cryofree® superconducting magnets, offering systems up to 16 T cooled via pulse tube refrigeration without liquid helium. This positions the company as a pioneer in cryogen-free magnet technology, ideal for quantum research, condensed-matter physics, and low-temperature materials science. Oxford also supplies 20 T liquid-helium-cooled magnets and sophisticated vector magnet systems. Its integrated cryogenic platforms maximize experimental uptime and reduce operational complexity, making it a preferred partner for research institutions.

Sumitomo Electric Industries – World Leader in HTS Wire (DI-BSCCO) and Power Applications

Sumitomo Electric leads in BSCCO-based HTS conductor manufacturing, providing the DI-BSCCO wire used in power transmission systems, SMES units, and industrial magnet applications. The company holds world records for long-length HTS current density performance, reinforcing its role in next-generation energy storage and high-capacity superconducting cable systems. Sumitomo’s strategic focus on HTS systems for grid modernization and industrial power enhances its competitive positioning as demand for superconducting infrastructure grows globally.

Superconducting Magnets Market Report Scope

Superconducting Magnets Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.3 Billion

|

|

Market Size (2035)

|

$7.3 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Conductor Material (Low-Temperature Superconductors, High-Temperature Superconductors), By Cooling Technology (Liquid Helium Systems, Helium-Free/Zero Boil-Off Cryocooler Systems), By Field Strength (Low Field, Mid Field, High Field, Ultra-High Field), By End-Use Application (Medical, Scientific Research, Energy & Power, Transportation)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Bruker, Siemens Healthineers, GE HealthCare, Sumitomo Electric, JASTEC, ASG Superconductors, General Atomics, AMSC, Hitachi, Fujikura, Furukawa Electric/SuperPower, Oxford Instruments, Western Superconducting Technologies, Nexans, THEVA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Superconducting Magnets Market Segmentation

By Conductor Material

- Low-Temperature Superconductors

- High-Temperature Superconductors

By Cooling Technology

- Liquid Helium Systems

- Helium-Free / Zero Boil-Off Cryocooler Systems

By Field Strength

- Low Field (<1.5 T)

- Mid Field (1.5–3 T)

- High Field (3–7 T)

- Ultra-High Field (>7 T)

By End-Use Industry

- Medical

- Scientific Research

- Energy & Power

- Transportation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Superconducting Magnets Market

- Bruker

- Siemens Healthineers

- GE HealthCare

- Sumitomo Electric

- JASTEC

- ASG Superconductors

- General Atomics

- AMSC

- Hitachi

- Fujikura

- Furukawa Electric / SuperPower

- Oxford Instruments

- Western Superconducting Technologies

- Nexans

- THEVA.

*- List not Exhaustive

Research Coverage

The latest Superconducting Magnets Market report from USDAnalytics provides a rigorous, data-backed assessment of how low-temperature and high-temperature superconducting technologies are reshaping MRI, fusion research, particle accelerators, SMES grid assets, and cryogen-free scientific systems. Drawing on detailed project pipelines and technology case studies, this report investigates how NbTi, Nb₃Sn, and emerging REBCO/BSCCO conductors are changing performance benchmarks in field strength, stability, and total cost of ownership as helium-light and helium-free architectures gain traction. It maps material and system-level breakthroughs in high-field MRI, ITER-scale fusion coils, and ultra-stable magnets for quantum computing, while providing granular analysis reviews of conductor manufacturing capacity, cryogenic integration strategies, and field-homogeneity specifications that influence vendor selection. The study highlights the competitive positions of leading magnet OEMs, conductor suppliers, and HTS innovators, and assesses how decarbonization, grid modernization, and precision medicine are driving long-cycle demand. With its integrated view of application trends, technology roadmaps, and project-level investments, this report is an essential resource for OEM strategy teams, procurement leaders, R&D directors, and investors tracking the evolution of superconducting magnet platforms across healthcare, energy, and scientific research, etc……

Scope Highlights

- Segmentation:

• By Conductor Material – Low-Temperature Superconductors, High-Temperature Superconductors

• By Cooling Technology – Liquid Helium Systems, Helium-Free / Zero Boil-Off Cryocooler Systems

• By Field Strength – Low Field (<1.5 T), Mid Field (1.5–3 T), High Field (3–7 T), Ultra-High Field (>7 T)

• By End-Use Industry – Medical, Scientific Research, Energy & Power, Transportation

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies: In-depth analysis and profiles of 15+ leading superconducting magnet manufacturers, conductor suppliers, and system integrators.