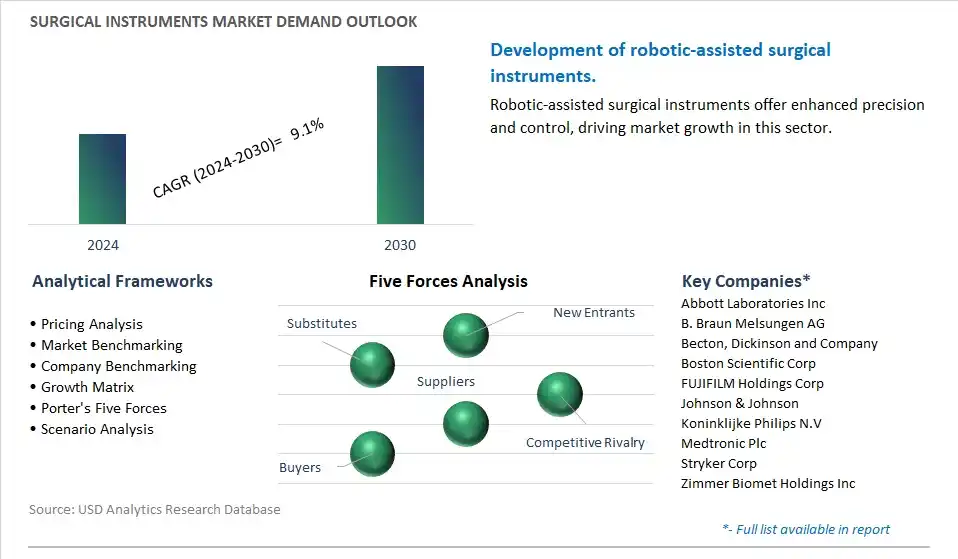

Surgical Instruments Market is estimated to increase at a growth rate of 9.1% CAGR over the forecast period from 2024 to 2030.

The global Surgical Instruments Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments including By Product (Handheld Devices, Sutures and Staplers, Inflation Devices, Cutting Instruments, Powered and Electrosurgical Devices, Others), By Category (Reusable, Disposable), By Application (Orthopedics, Plastic and Reconstructive Surgeries, Cardiovascular, Obstetrics and Gynecology, Neurology, Others), By End-User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Others).

An Introduction to Surgical Instruments Market in 2024

The Surgical Instruments Market includes handheld surgical tools, forceps, scissors, retractors, needle holders, and clamps used in surgical procedures, operating rooms, and sterile environments for tissue manipulation, dissection, hemostasis, and surgical technique execution across various medical specialties such as general surgery, orthopedics, cardiovascular surgery, and plastic surgery. Surgical instruments provide precision, durability, and ergonomic design features, supporting surgical efficiency, instrument functionality, and surgeon comfort during medical interventions. Market trends encompass minimally invasive instrument designs, robotic-assisted surgical instruments, sterilization-compatible materials, and instrument tracking technologies for optimized surgical instrument management and operating room workflows.

Surgical Instruments Market Competitive Landscape

The global Surgical Instruments Industry is highly competitive with a large number of companies focusing on niche market segments. Amidst intense competitive conditions, Surgical Instruments Companies are investing in new product launches and strengthening distribution channels. Key companies operating in the Surgical Instruments Industry include- Abbott Laboratories Inc, B. Braun Melsungen AG, Becton, Dickinson and Company, Boston Scientific Corp, FUJIFILM Holdings Corp, Johnson & Johnson, Koninklijke Philips N.V, Medtronic Plc, Stryker Corp, Zimmer Biomet Holdings Inc.

Surgical Instruments Market Trend: Advancements in Robotic-Assisted Surgical Instruments

One of the most prominent trends in the Surgical Instruments market is the rapid advancement of robotic-assisted surgical instruments. Robotic surgery has revolutionized the field of surgery by offering greater precision, dexterity, and control to surgeons during minimally invasive procedures. Recent technological advancements have led to the development of sophisticated robotic systems equipped with advanced instrumentation, including robotic arms, end effectors, and surgical tools. These robotic-assisted instruments incorporate features such as haptic feedback, tremor reduction, and intuitive control interfaces, enabling surgeons to perform complex procedures with enhanced accuracy and efficiency. Moreover, the integration of artificial intelligence (AI) algorithms into robotic surgical instruments allows for predictive analytics, real-time intraoperative guidance, and personalized surgical approaches. As robotic-assisted surgery becomes increasingly prevalent across various surgical specialties, the demand for advanced robotic instruments is expected to drive market growth in the Surgical Instruments segment.

Surgical Instruments Market Driver: Rise in Minimally Invasive Surgical Procedures

The primary driver for the Surgical Instruments market is the growing adoption of minimally invasive surgical procedures worldwide. Minimally invasive techniques offer several advantages over traditional open surgeries, including smaller incisions, reduced trauma to surrounding tissues, faster recovery times, and shorter hospital stays. Surgical instruments designed specifically for minimally invasive procedures, such as laparoscopic instruments, endoscopes, and robotic surgical tools, play a crucial role in enabling surgeons to perform these techniques safely and effectively. With advancements in technology and instrumentation, minimally invasive approaches are expanding to encompass a broader range of surgical procedures across various medical specialties, including gynecology, urology, gastroenterology, and orthopedics. The rising demand for minimally invasive surgeries is driving the adoption of specialized surgical instruments designed to optimize procedural outcomes, minimize patient discomfort, and improve overall surgical experience.

Surgical Instruments Market Opportunity: Development of Smart Surgical Instruments

An opportunity exists in the development of smart surgical instruments that leverage digital technologies to enhance surgical precision, workflow efficiency, and patient safety. Smart surgical instruments incorporate sensors, actuators, and connectivity features to provide real-time feedback, automate tasks, and enable remote monitoring during surgical procedures. These intelligent instruments can detect anatomical structures, measure tissue properties, and analyze surgical parameters in real time, allowing surgeons to make informed decisions and adjust their techniques accordingly. Additionally, smart surgical instruments can integrate with electronic health record (EHR) systems and surgical navigation platforms to capture procedural data, streamline documentation, and facilitate post-operative analysis. Manufacturers investing in the research and development of smart surgical instruments stand to capitalize on the growing demand for innovative technologies that improve surgical outcomes and optimize healthcare delivery. Collaboration with surgeons, healthcare institutions, and technology partners can accelerate the development and adoption of smart surgical instruments, positioning companies for success in the dynamic Surgical Instruments market.

Surgical Instruments Market Share Analysis: Powered and Electrosurgical Devices is the fastest growing market segment over the forecast period to 2030

Among the segmented categories, Powered and Electrosurgical Devices emerge as the fast-growing segment in the market for surgical instruments. Powered and electrosurgical devices encompass a wide range of instruments used in surgical procedures, including electrosurgical units, powered dissectors, drills, and saws. These devices offer precise tissue cutting, coagulation, and hemostasis capabilities, enhancing surgical precision and efficiency. With advancements in surgical techniques and the increasing demand for minimally invasive procedures, powered and electrosurgical devices are becoming essential tools across various surgical specialties, including orthopedics, plastic and reconstructive surgeries, cardiovascular procedures, and obstetrics and gynecology. Additionally, the growing preference for disposable instruments to reduce the risk of cross-contamination and surgical site infections further drives the demand for disposable powered and electrosurgical devices. As hospitals, specialty clinics, and ambulatory surgical centers prioritize investment in advanced surgical equipment to meet the evolving needs of patients and enhance surgical outcomes, the market for powered and electrosurgical devices is expected to continue its rapid growth trajectory, contributing to advancements in surgical practice and patient care.

Surgical Instruments Market Segmentation

By Product

Handheld Devices

Sutures and Staplers

Inflation Devices

Cutting Instruments

Powered and Electrosurgical Devices

Others

By Category

Reusable

Disposable

By Application

Orthopedics

Plastic and Reconstructive Surgeries

Cardiovascular

Obstetrics and Gynecology

Neurology

Others

By End-User

Hospitals

Specialty Clinics

Ambulatory Surgical Centers

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Surgical Instruments Companies

Abbott Laboratories Inc

B. Braun Melsungen AG

Becton, Dickinson and Company

Boston Scientific Corp

FUJIFILM Holdings Corp

Johnson & Johnson

Koninklijke Philips N.V

Medtronic Plc

Stryker Corp

Zimmer Biomet Holdings Inc

* List not Exhaustive

Reasons to Buy the Surgical Instruments Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Surgical Instruments Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Surgical Instruments Industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Surgical Instruments Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Analyzed

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Surgical Instruments Market Size Outlook, $ Million, 2021 to 2030

3.2 Surgical Instruments Market Outlook by Type, $ Million, 2021 to 2030

3.3 Surgical Instruments Market Outlook by Product, $ Million, 2021 to 2030

3.4 Surgical Instruments Market Outlook by Application, $ Million, 2021 to 2030

3.5 Surgical Instruments Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Surgical Instruments Industry

4.2 Key Market Trends in Surgical Instruments Industry

4.3 Potential Opportunities in Surgical Instruments Industry

4.4 Key Challenges in Surgical Instruments Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Surgical Instruments Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Surgical Instruments Market Outlook by Segments

7.1 Surgical Instruments Market Outlook by Segments, $ Million, 2021- 2030

By Product

Handheld Devices

Sutures and Staplers

Inflation Devices

Cutting Instruments

Powered and Electrosurgical Devices

Others

By Category

Reusable

Disposable

By Application

Orthopedics

Plastic and Reconstructive Surgeries

Cardiovascular

Obstetrics and Gynecology

Neurology

Others

By End-User

Hospitals

Specialty Clinics

Ambulatory Surgical Centers

Others

8 North America Surgical Instruments Market Analysis and Outlook To 2030

8.1 Introduction to North America Surgical Instruments Markets in 2024

8.2 North America Surgical Instruments Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Surgical Instruments Market size Outlook by Segments, 2021-2030

By Product

Handheld Devices

Sutures and Staplers

Inflation Devices

Cutting Instruments

Powered and Electrosurgical Devices

Others

By Category

Reusable

Disposable

By Application

Orthopedics

Plastic and Reconstructive Surgeries

Cardiovascular

Obstetrics and Gynecology

Neurology

Others

By End-User

Hospitals

Specialty Clinics

Ambulatory Surgical Centers

Others

9 Europe Surgical Instruments Market Analysis and Outlook To 2030

9.1 Introduction to Europe Surgical Instruments Markets in 2024

9.2 Europe Surgical Instruments Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Surgical Instruments Market Size Outlook by Segments, 2021-2030

By Product

Handheld Devices

Sutures and Staplers

Inflation Devices

Cutting Instruments

Powered and Electrosurgical Devices

Others

By Category

Reusable

Disposable

By Application

Orthopedics

Plastic and Reconstructive Surgeries

Cardiovascular

Obstetrics and Gynecology

Neurology

Others

By End-User

Hospitals

Specialty Clinics

Ambulatory Surgical Centers

Others

10 Asia Pacific Surgical Instruments Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Surgical Instruments Markets in 2024

10.2 Asia Pacific Surgical Instruments Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Surgical Instruments Market size Outlook by Segments, 2021-2030

By Product

Handheld Devices

Sutures and Staplers

Inflation Devices

Cutting Instruments

Powered and Electrosurgical Devices

Others

By Category

Reusable

Disposable

By Application

Orthopedics

Plastic and Reconstructive Surgeries

Cardiovascular

Obstetrics and Gynecology

Neurology

Others

By End-User

Hospitals

Specialty Clinics

Ambulatory Surgical Centers

Others

11 South America Surgical Instruments Market Analysis and Outlook To 2030

11.1 Introduction to South America Surgical Instruments Markets in 2024

11.2 South America Surgical Instruments Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Surgical Instruments Market size Outlook by Segments, 2021-2030

By Product

Handheld Devices

Sutures and Staplers

Inflation Devices

Cutting Instruments

Powered and Electrosurgical Devices

Others

By Category

Reusable

Disposable

By Application

Orthopedics

Plastic and Reconstructive Surgeries

Cardiovascular

Obstetrics and Gynecology

Neurology

Others

By End-User

Hospitals

Specialty Clinics

Ambulatory Surgical Centers

Others

12 Middle East and Africa Surgical Instruments Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Surgical Instruments Markets in 2024

12.2 Middle East and Africa Surgical Instruments Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Surgical Instruments Market size Outlook by Segments, 2021-2030

By Product

Handheld Devices

Sutures and Staplers

Inflation Devices

Cutting Instruments

Powered and Electrosurgical Devices

Others

By Category

Reusable

Disposable

By Application

Orthopedics

Plastic and Reconstructive Surgeries

Cardiovascular

Obstetrics and Gynecology

Neurology

Others

By End-User

Hospitals

Specialty Clinics

Ambulatory Surgical Centers

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Abbott Laboratories Inc

B. Braun Melsungen AG

Becton, Dickinson and Company

Boston Scientific Corp

FUJIFILM Holdings Corp

Johnson & Johnson

Koninklijke Philips N.V

Medtronic Plc

Stryker Corp

Zimmer Biomet Holdings Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise