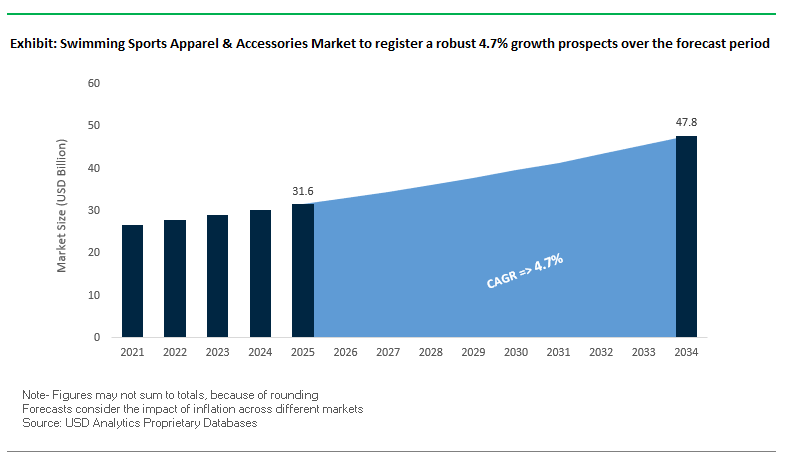

The global market for swimming sport equipment and accessories is projected to grow from USD 31.6 billion in 2025 to USD 47.8 billion in 2034, at a CAGR of 4.7%. The industry is a high-tech specialty within the sportswear industry catering to competitive swimmers, active consumers, triathletes, and water sport participants. Material innovation, sustainability, and performance-oriented design continue to be the industry hallmark, with the leading brands heavily investing in sustainable production, high-tech swimwear, and online retailing. The market growth is directly proportional to the rise in global participation in health and fitness, the popularity of swimming as a low-impact exercise, and rising demand for multi-functional aquatic equipment that blends functionality with fashion.

The swim sports fashion and accessories industry is changing in terms of brand acquisitions, celebrity endorsements, leadership, and product development. American Exchange Group, in August 2025, acquired VENUS Fashion, a swimwear heritage brand, marking a strategic expansion to its portfolio through VENUS's well-established consumer base. Likewise, in July 2025, L Catterton Asia announced a tie-up between GXG and 2XU, which aims at the high-end sportswear market in China's rapidly growing fitness sector.

Best performance swim wear brands are also making investments in competitive sport visibility. Arena, in July 2025, named Mark Pinger Chief Brand Officer and introduced the Indomitus Collection prior to the World Aquatics Championships, a collection inspired by determination and resilience. Previously, in January 2025, Arena launched the POWERSKIN Impulso, a competition swimsuit that extends elite swimming technology to more consumers.

Sports governance partnerships are enhancing brand trustworthiness. TYR Sport was named an official World Aquatics partner in June 2025, reinforcing its professional swimming status. TYR's retail expansion strategy has included its inaugural brick-and-mortar retail store on Long Island, New York (April 2023), enhancing direct consumer engagement. The trend of product innovation in the sector is shifting toward democratized access to high-performance gear, further emphasis on environmentally sustainable materials, and new penetration into fitness markets.

Advanced drag-reduction technologies, previously reserved for Olympic-level competition, are now available in the mass-market swimwear marketplace. Following on from the advances such as NASA collaboration on the "Fastskin" suit designed to replicate the shark's dermal denticles to achieve quantifiable drag reduction brands are transferring similar principles to consumer-level performance swimwear. Textile engineering studies verify that drag-reducing swimwear can shave off swim times by tiny but significant fractions, of interest to competitive amateurs, triathletes, and serious lap swimmers. Tech suits are being introduced with specific compression panels, hydrophobic finishes, and body-streamlining technologies, marketed not just for elite competition but for recreational swimmers as well who appreciate added speed, confidence, and water efficiency.

Smart fabrics with UV-responsive capabilities are revolutionizing sun-protective swimwear. Following research proving dramatic improvements in Ultraviolet Protection Factor (UPF) using advanced dyestuffs and UV-absorbing compounds, brands now manufacture swimwear that responds dynamically to sunlight by altering color or alerting when UV intensity hits dangerous levels. This technology addresses increasing consumer demand for active skin health precautions as skin cancer awareness continues to grow. With photochromic dyes and sensor-fabric integration, such products enable wearers to see their sun exposure, assisting them in determining when it is time to reapply sunscreen or get into the shade. The technology not only enhances functionality but also provides an interactive and informative swimwear experience.

Adaptive and inclusive swimwear is a low-developed but high-potential niche segment. A study on adaptive sports identifies the requirement for bespoke designs to improve comfort, minimize drag, and maximize mobility for para-athletes. Cross-industry collaborations between large swimwear brands and sporting organizations such as collaborations with Aquatics GB are resulting in bespoke compression garments for top-level para-athletes. The greater exposure of adaptive sports through the likes of the Paralympic Games is driving demand for fashionable yet functional swimwear that satisfies both competition and leisure requirements, offering a clear opportunity for growth for those brands that will innovate within this area.

The seasonality inherent in swimwear makes it perfectly suited to rental and subscription-driven retail models. Sustainability-conscious consumers and holidaymakers looking for novelty without purchase increasingly welcome such services. Research into apparel rental shows short-term, occasion-specific rentals are growing, and swimwear perfectly aligns with months 4–9 of the retail season. Platforms such as Rent the Runway and Nuuly have already demonstrated the sustainability of edited rental bundles, and likewise, models specifically designed for swimwear can provide access to high-end designs for resort occasions, competitions, and holiday affairs, curbing overconsumption and textile loss.

Swimwear leads the apparel segment with a 38% sector share, followed by women's one-piece swimsuits and bikinis with chlorine-resistant quick-drying material. Swim trunks follow with a 25% market sector, with men's board shorts with environmentally friendly material up 35% year on year being a growth driver. Wetsuits and rash guards are picking up as water sports such as surfing, triathlons, and paddleboarding become increasingly popular. These segments require UV protection and thermal insulation, so they are well-liked among competitive athletes and recreational swimmers. The Others segment, including swim leggings, burkinis, and competition tech suits, is picking up as consumers seek diverse styles to meet cultural, functional, and competitive needs.

.png)

Goggles are dominating the accessories segment with a 30% market share, fueled by technological innovation in anti-fog coatings, mirrored lenses, and prescription lenses. Swim caps account for 25% of sales, where 70% belongs to silicone caps, due to their comfort and durability and transition towards customizable designs for competitive swimming. Training aids such as fins, kickboards, and snorkels are becoming popular among professional and amateur swimmers short-blade fins and eco-composite materials are fueling replacement in this segment. The "Others" category, which comprises ear plugs, nose clips, and waterproof bags, is growing as consumers are investing in full swim kits to enhance performance, safety, and convenience.

Established heritage sport brands with strong positions in competitive sport lead the market, complemented by complementary strategic lifestyle extensions and creative product innovation. Speedo, Arena, Decathlon, Adidas, Nike, Tyr Sport, Under Armour, Finis, Zoggs, Funky Trunks, MP Michael Phelps, O'Neill, Billabong, Arena Water Instinct, Aqualung, Others are the leading players.

Speedo led the way in terms of fabric innovation, from the launch of nylon swimsuits in 1957 to chlorine-resistant fabric in 1994. Its range comprises the LZR Racer technical racing suits, more than 70 goggles models, and aquatic fitness equipment. Speedo has been devoted to sustainability, introducing an eco-range of 100% recycled ocean plastic, and partnered with BEAMS for an SS26 capsule that blurs sport and fashion. Speedo India's association with cult makes swimming a fitness lifestyle.

Arena's Powerskin competition swimming suit line is the benchmark in competitive swimming. The Powerskin Impulso launch in 2025 made advanced swim technology available to the masses. The company is well represented in the competitive ranks, continuing its KNZB sponsorship through LA 2028 and teaming with Brazil's CBDA. The Indomitus Collection launched in 2025 cemented its brand identity through designs symbolizing strength and courage. Its offerings span training swimwear through anti-fog goggles, swim bags, and open-water wetsuits.

TYR has strong heritage in triathlon and competitive swimming culture and offers specialized swim apparel, wetsuits, and equipment. It has extended its reach to fitness apparel and CrossFit, targeting the broader fitness market. TYR's partnership with World Aquatics adds to its professional credibility, and partnerships with New Balance and USA Swimming add to its sporting brand value. Product innovation encompasses intelligent swim apparel designs with integrated sensors to monitor performance.

The United States remains a global leader in high-performance swimming apparel and accessories, driven by its strong culture of competitive swimming and a growing athleisure trend. The integration of augmented reality (AR) in smart swimming goggles is transforming training by providing real-time performance metrics such as lap times, distance, and stroke rate directly in a swimmer’s line of sight. Parallel to tech innovation, brands are advancing material science, introducing high-performance fabrics that enhance flexibility, reduce drag, and provide UV protection. Compression suits for muscle support and quick-drying, chlorine-resistant fabrics are gaining prominence among competitive and recreational swimmers alike.

The U.S. market is also shaped by a sustainability push, with brands increasingly using recycled polyester (Repreve) from plastic bottles and regenerated nylon (ECONYL) from ocean waste. These eco-friendly materials are being integrated into both professional-grade swimwear and casual water apparel. A well-established network of public pools, collegiate leagues, and Olympic-level programs fuels continuous demand for performance gear, while the crossover appeal of swim-inspired athleisure extends the market reach into casual fashion.

China remains a manufacturing powerhouse for global swimming sports apparel and accessories, supported by an advanced supply chain and logistics network that enables rapid product development and large-scale distribution. The domestic market is expanding rapidly, driven by a rising middle class with increasing disposable incomes and a heightened focus on health, fitness, and wellness activities like swimming.

Government investment in sports infrastructure and physical education programs is encouraging broader participation in aquatic sports, creating a steady demand for swimwear and related accessories. Chinese brands are leveraging e-commerce platforms and livestreaming commerce to reach diverse consumer segments, offering both performance-focused products for competitive swimmers and affordable, fashionable options for casual users. This omnichannel retail approach, combined with local production efficiency, positions China as a key driver of both global exports and domestic consumption growth.

The European Union’s swimming sports apparel market is shaped by stringent regulatory frameworks such as the REACH directive on chemical safety and the Corporate Sustainability Reporting Directive (CSRD). These policies require brands to uphold transparency, traceability, and environmental responsibility across manufacturing processes. The EU’s commitment to a circular economy is pushing companies toward sustainable packaging, waste reduction, and compliance with bans on destroying unsold goods.

European swimwear brands are at the forefront of sustainable fabric innovation, experimenting with recycled plastics, bio-based fibers, and upcycled materials without compromising performance. R&D efforts focus on eco-friendly yet hydrodynamic materials, ensuring athletes receive top-tier functionality alongside environmental benefits. This combination of regulatory compliance, material innovation, and consumer demand for eco-conscious products positions the EU as a global sustainability benchmark in the sector.

Australia’s swimming apparel market thrives on a deep-rooted aquatic culture, fueled by its extensive coastline, year-round beach-going lifestyle, and strong competitive swimming programs. Local brands are recognized for pioneering UV-protective swimwear and accessories, with a strong emphasis on rash guards, long-sleeved swimsuits, and sun-safe children’s apparel.

The nation’s success in producing world-class competitive swimmers has spurred demand for performance-enhancing swimwear, including compression suits and training aids tailored for professional athletes. This dual market covering both recreational beachwear and elite competition gear is supported by a vibrant club network, frequent competitive events, and a national emphasis on sun safety, ensuring sustained consumer demand.

Brazil’s swimming sports apparel market is expanding due to its large population, rising middle class, and water-centric lifestyle. With its vast coastline and favorable climate, swimming and water sports are integral to Brazilian culture. Domestic production capabilities within its robust textile and apparel manufacturing sector enable quick responses to fashion trends and seasonal demands, giving local brands a competitive edge in speed-to-market.

Major sporting events and international competitions have boosted the visibility of aquatic sports, driving higher participation rates and increased demand for swimwear and accessories. The market is diversified, offering performance-oriented gear for athletes alongside fashionable, vibrant swimwear designs that cater to lifestyle consumers. Brazil’s blend of cultural affinity for water sports, local manufacturing agility, and event-driven demand makes it a strong regional player with growing global export potential.

|

Parameter |

Details |

|

Market Size (2025) |

$31.6 Billion |

|

Market Size (2034) |

$47.8 Billion |

|

Market Growth Rate |

4.7% |

|

Segments |

By Product (Apparel (Swimsuits, Swim Trunks, Wetsuits, Rash Guards, Others), Accessories (Goggles, Caps, Fins, Kickboards, Snorkels, Others)), By End User (Men, Women, Kids), By Application (Competition, Training, Recreation), By Distribution Channel (Online Stores, Exclusive Brand Outlets, Sporting Goods Retailers, Supermarkets & Hypermarkets), By Material (Polyester, Nylon, Spandex, Neoprene, Silicon, Others) |

|

Study Period |

2019- 2024 and 2025-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Speedo, Arena, Decathlon, Adidas, Nike, Tyr Sport, Under Armour, Finis, Zoggs, Funky Trunks, MP Michael Phelps, O'Neill, Billabong, Arena Water Instinct, Aqualung, Others. |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

* List Not Exhaustive

This report investigates the Swimming Sports Apparel & Accessories Market, delivering strategic breakthroughs, analysis reviews, and highlights that illustrate how high-performance innovation, sustainable material adoption, and advanced retail strategies are shaping the sector’s evolution through 2034. Developed by USDAnalytics, the study examines competitive brand positioning, regional performance, and emerging technologies—from drag-reduction textiles to UV-responsive fabrics—while mapping demand across competitive, training, and recreational swimming segments. This report is an essential resource for sports apparel executives, product developers, investors, and retailers seeking data-driven insights on performance, sustainability, and consumer behavior patterns in a market increasingly influenced by health, wellness, and lifestyle trends. Scope includes-

The market research methodology integrates a hybrid data-gathering approach combining primary and secondary research to ensure both accuracy and actionable insights. Primary research included structured interviews with competitive swimwear designers, sports federations, retail buyers, and materials engineers to uncover emerging product trends and performance requirements. Secondary research encompassed analysis of industry reports, sports equipment trade data, sustainability certifications, and company financial disclosures. Market sizing was performed using both bottom-up and top-down approaches, segmenting demand by product type, application, material, and region, then validating through triangulation against import/export figures and brand share data. Forecast modeling incorporated trendline extrapolation, performance innovation adoption rates, and scenario-based impact analysis of regulatory changes and sustainability mandates.

Table of Contents: Swimming Sports Apparel & Accessories Market

Growth is driven by rising global participation in swimming for fitness and rehabilitation, technological advancements like drag-reduction textiles, and increased demand for sustainable, eco-friendly swimwear materials such as recycled polyester and regenerated nylon.

In apparel, swimsuits and swim trunks lead due to high competitive and recreational demand, while in accessories, goggles and swim caps hold the largest market shares, supported by innovations in anti-fog, UV-protection, and ergonomic designs.

Brands are integrating recycled ocean plastics, bio-based fibers, and low-impact dyeing processes into high-performance swimwear. These innovations meet regulatory requirements in regions like the EU while appealing to eco-conscious consumers globally.

Asia Pacific, led by China and Australia, is experiencing rapid growth due to increasing sports infrastructure investments and strong aquatic sports cultures. North America and Europe remain strong due to competitive swimming traditions and regulatory-driven sustainability shifts.

Key companies include Speedo, Arena, Decathlon, Adidas, Nike, TYR Sport, Under Armour, Zoggs, Funky Trunks, and MP Michael Phelps, all of which are advancing performance design, sustainability initiatives, and digital retail engagement strategies.