Dyestuff Market to Reach $571.3 Million by 2034 at 6.4% CAGR Amid Consolidation, Bio-Based Innovation, and PFAS Reformulation

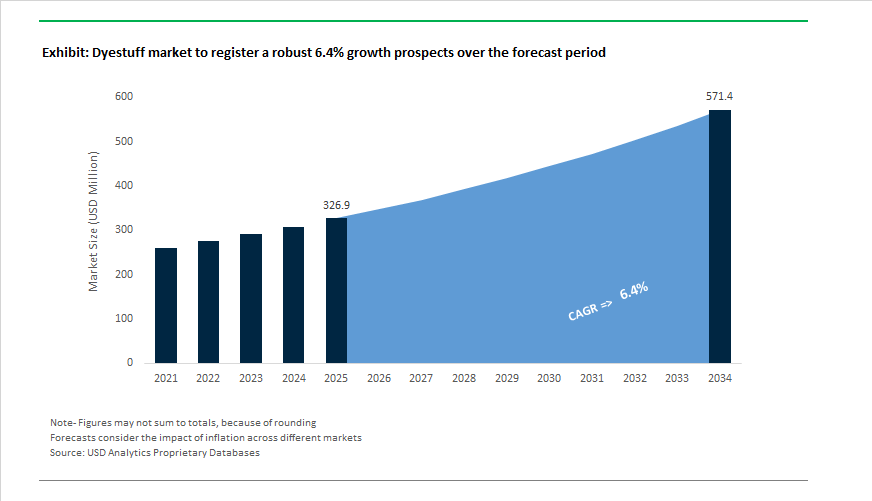

The Dyestuff Market is projected to expand from $326.9 Million in 2025 to $571.3 Million by 2034, registering a CAGR of 6.4%. Market expansion is increasingly shaped by structural consolidation, regulatory tightening on hazardous chemistries, and rapid innovation in sustainable textile coloration. A defining transaction occurred in October 2024, when Sudarshan Chemical Industries Limited entered into a definitive agreement to acquire the Heubach Group following its insolvency proceedings. This acquisition significantly strengthens Sudarshan’s global footprint across Europe, the Americas, and Asia, creating one of the largest pigment and dye platforms worldwide. The consolidation reflects a broader industry pattern in which financially resilient Asian producers are absorbing legacy European assets to optimize cost structures and secure advanced inorganic pigment technologies.

Pricing pressure remained a central theme through December 2024, when Sun Chemical announced a global pigment price increase citing persistent raw material inflation, particularly benzene-linked intermediates. The move underscored the volatility in aromatic feedstock supply and the continuing margin compression across dyestuff manufacturing. Meanwhile, Kiri Industries reported profitability gains in 2024, attributing improved performance to its focus on reactive dyes and H-acid intermediates, which benefited from sourcing diversification trends as global buyers shifted procurement away from high-cost European production bases.

Strategic integration and digital innovation have accelerated in textile chemicals. Throughout 2024, Archroma completed the operational consolidation of Huntsman’s Textile Effects division, acquired in late 2023. The integration significantly expanded Archroma’s share in reactive dyes and specialty textile chemicals, strengthening its position in ZDHC-compliant supply chains. Prior to full integration, Huntsman launched Innovance Smart Shade in 2024, a digitally enabled dye solution allowing real-time shade correction in digital textile printing environments. This innovation reduces water, energy, and reprocessing waste in high-speed industrial textile production. In January 2026, Archroma further expanded its sustainability footprint through a co-marketing partnership with HeiQ, integrating antimicrobial and anti-odor technologies for performance apparel and medical textiles.

Product innovation has intensified in high-performance synthetics and bio-based chemistries. DyStar introduced Dianix® Black XF3 300% in 2025, a disperse dye engineered for enhanced wet-fastness on polyester fabrics, addressing long-standing issues of color bleeding in sportswear and multi-colored garments. In 2024, Archroma launched EarthColors Reactive dyes that are 92% bio-based, derived from non-edible agricultural waste such as almond shells and rosemary leaves. This product line directly supports apparel brands seeking lower Scope 3 emissions and reduced fossil dependency in cotton dyeing processes.

Environmental regulation is reshaping formulation strategies across the dyestuff value chain. In August 2025, LANXESS introduced a low-VOC inorganic pigment portfolio tailored to comply with stricter EU architectural coating standards scheduled for 2026 enforcement. In January 2026, France began enforcing a ban on clothing containing PFAS chemicals, while the UK introduced its first national PFAS risk mitigation plan. These regulatory shifts are compelling dyestuff and finishing chemical producers to reformulate water-repellent and stain-resistant treatments using fluorine-free alternatives.

Capacity expansion in Asia continues to rebalance global supply. VOXCO Pigments announced a $60 million investment in September 2025 to expand chrome yellow and molybdate orange pigment production, targeting export growth in paints, plastics, and coatings. The cumulative effect of consolidation, sustainable dye chemistry innovation, digital shade management systems, and stricter environmental compliance frameworks is redefining competitive positioning within the global dyestuff market, particularly across textile, coatings, and specialty pigment segments.

Trends and Opportunities in the Dyestuff Market

Strategic Pivot to Bio-Based and Circular Feedstocks to Meet Brand-Led Compliance Mandates

- Global dyestuff producers are accelerating the shift from petrochemical intermediates toward bio-synthetic, fermentation-based, and circular feedstock pathways as apparel and footwear brands hardwire Scope 3 decarbonization into supplier qualification criteria. Color chemistry is now a core compliance parameter rather than a downstream formulation choice.

- In October 2024, Archroma launched the NTR Printing System, marking the first commercially scalable bio-based pigment printing platform. The system integrates PRINTOFIX® BLACK NTR-TF pigment with 79% renewable carbon content and binders containing roughly 40% renewable inputs. Bulk production trials with industrial textile partners demonstrated that these systems can achieve synthetic-grade color fastness while materially reducing fossil carbon intensity, removing a historical trade-off between sustainability and performance.

- Brand compliance pressure is intensifying. According to the 2025 Fossil Free Fashion Scorecard, more than 95% of leading global apparel groups including H&M and Kering have embedded circularity, resale, or repair mandates into their sourcing strategies. As a result, dyestuff suppliers are being compelled to replace petroleum-derived intermediates with renewable alternatives to retain Tier 1 supplier status.

- This transition is reinforced by the ZDHC 2025 Roadmap, which targets the elimination of hazardous substances from textile value chains. Compliance has driven capital investment toward customized bio-based binders and auxiliaries that enable renewable dyestuffs to meet industrial durability benchmarks. For dyestuff manufacturers, bio-based chemistry is a prerequisite for long-term market access.

Digitalization of Color Matching and AI-Driven On-Demand Production Models

- Digital transformation is reshaping dyestuff formulation, application, and inventory management. Physical swatches and iterative lab dyeing are being replaced by AI-driven color communication systems that ensure global consistency while sharply reducing waste.

- During 2025, companies such as Huntsman and Archroma scaled AI-enabled formulation platforms capable of harmonizing color output across geographically dispersed dye houses. These systems eliminate trial-and-error dyeing cycles that historically consumed large volumes of water, energy, and excess dyestuff. Industrial audits indicate that digital color matching significantly reduces reprocessing rates and improves right-first-time production yields.

- Regulation is accelerating adoption. The EU Ecodesign for Sustainable Products Regulation introduced in 2025 mandates Digital Product Passports for textiles. Dyestuff composition, chemical footprint, and environmental attributes must now be digitally traceable through QR-linked datasets. This requirement has made digital color management infrastructure essential rather than optional, particularly for suppliers serving European fashion and home textile brands.

- Operationally, digital textile printing is benefiting most from this shift. By late 2025, industrial data showed that reactive ink-based digital printing reduced dyestuff and water waste by close to 40% compared with conventional screen-printing. This efficiency advantage supports the rise of micro-factories and on-demand manufacturing models, where dyestuffs are produced and applied in smaller batches aligned directly with demand signals.

Development of Functional Dyestuffs for Technical and High-Performance Textiles

- The expansion of technical textiles across automotive, medical, defense, and energy applications is creating a high-margin growth avenue for dyestuffs that deliver functional performance beyond aesthetics. Colorants are increasingly expected to contribute to thermal stability, flame retardancy, UV resistance, and long-term durability.

- In September 2024, Asahi Kasei introduced LASTAN, a flame-retardant nonwoven engineered for EV battery safety applications. This development highlights rising demand for dyestuffs and finishes compatible with extreme thermal environments, where color stability must be maintained under sustained heat exposure.

- Automotive demand is also evolving. BASF Coatings unveiled its 2025–2026 automotive color trends featuring advanced metallic and multidimensional pigments engineered for UV resistance and long-term weatherability. These dyestuffs are tailored to the durability requirements of electric vehicles, where lightweight materials and extended service lifetimes place higher stress on color performance.

- Policy support is reinforcing this opportunity. Under India’s Production Linked Incentive scheme, approved with incentives of roughly USD 1 billion as of 2025, technical textiles are a priority segment. This framework is encouraging dyestuff manufacturers to invest in high-performance formulations for medical, protective, and agrotech textiles, where margins and entry barriers are structurally higher than in commodity apparel dyeing.

Enabling Plastic-to-Plastic Recycling Through NIR-Detectable and Circular Colorants

- The transition toward a circular plastics economy is unlocking a critical opportunity for dyestuff innovation. Traditional carbon black pigments absorb near-infrared light, rendering black plastics invisible to automated sorting systems and effectively unrecyclable at scale. Solving this limitation has become a strategic priority for packaging and automotive OEMs.

- In December 2025, UPM launched the world’s first bio-based, NIR-detectable, carbon-negative black pigment derived from renewable lignin at its EUR 1.3 billion biorefinery in Germany. This innovation allows black packaging to be identified and sorted by NIR scanners, unlocking recycling streams that were previously excluded from circular systems.

- Parallel developments from BASF are enabling similar advances. Conventional carbon black has long disrupted automated recycling, but new NIR-transparent formulations are now reaching commercial scale. BASF’s 2025 pilot projects with Porsche and Mercedes-Benz demonstrated that chemically recycled polyamides from automotive shredder residue can be re-pigmented for high-quality interior components without compromising mechanical or aesthetic performance.

Dyestuff Market Share and Segmentation Insights

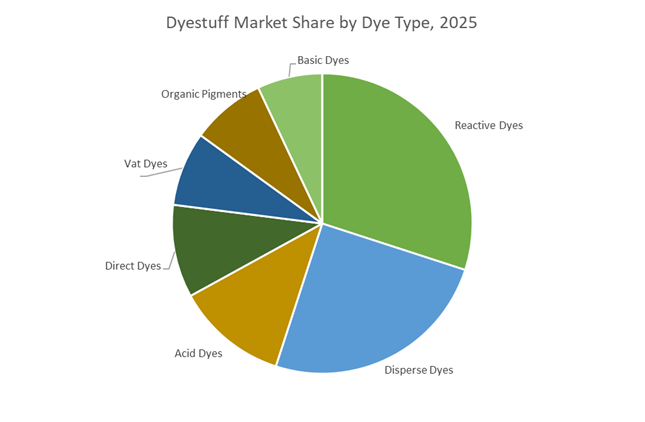

Reactive Dyes Capture the Largest Share Driven by Cotton and Cellulosic Fiber Demand

Reactive dyes account for 30% of the global dyestuff market share in 2025, supported by their dominant use in cotton, viscose, and linen textiles. Their ability to form covalent bonds with cellulosic fibers ensures superior wash fastness, color vibrancy, and durability, making them the preferred choice for apparel and home textile manufacturing. Disperse dyes represent a significant portion of the market, fueled by rising polyester consumption across sportswear, fast fashion, and automotive textiles, where high-temperature dyeing ensures strong fiber affinity and color stability. Acid dyes maintain importance in nylon, wool, silk, and leather processing due to their brightness and leveling properties. Direct dyes remain relevant for cost-sensitive textile and paper applications, while vat dyes serve niche segments requiring exceptional light and wash fastness. Organic pigments are gaining traction in textile printing, plastics, and inks, whereas basic dyes cater to acrylic fibers and specialty coloration needs.

Apparel and Fashion Industry Drives Nearly Half of Global Dyestuff Consumption

The apparel and fashion sector represents 48% of total dyestuff demand in 2025, reflecting continuous color innovation cycles, seasonal trends, and high-volume textile production worldwide. Rapid fashion turnover and consumer preference for diverse color palettes sustain strong consumption across reactive, disperse, acid, and direct dyes. Home textiles form a major secondary segment, encompassing bed linens, curtains, upholstery, and carpets where colorfastness and long-term durability are critical for brand positioning and customer satisfaction. Technical textiles are emerging as a high-growth segment, integrating dyestuffs into protective clothing, medical fabrics, geotextiles, and performance materials requiring UV resistance and functional enhancements. Paper and pulp applications remain significant for packaging and specialty papers, while leather and fur industries rely on specialized dye classes for substrate compatibility. Automotive textiles demand high-performance dyes with exceptional lightfastness, and food, drug, and cosmetic applications constitute a niche but highly regulated segment requiring certified, safety-compliant colorants.

Competitive Landscape of the Dyestuff Market

The global dyestuff market in 2026 is being reshaped by sustainability-driven innovation, consolidation among Tier-1 players, and rising demand from textiles, denim, automotive fabrics, and digital printing, with leading manufacturers competing on low-impact dyes, reactive color performance, and vertically integrated supply chains.

Sustainable specialty dye leadership anchored by circular textile innovation at Archroma

Archroma has strengthened its position as a global leader in sustainable textile dyes following its 2023 acquisition of Huntsman’s Textile Effects business. Its patented EarthColors® range converts non-edible agricultural waste into high-performance dyestuffs, aligning with circular economy targets. In early 2026, Archroma showcased low-impact denim solutions at Denimsandjeans Egypt, targeting the fast-growing Egyptian sourcing hub. The launch of DIRESUL® EVOLUTION BLACK, claimed as the cleanest sulfur black dye, delivers a 57% synthesis impact reduction versus conventional grades. Anchored by “The Archroma Way,” the company integrates AVITERA® SE and BLUE MAGIC systems to cut water and energy use, positioning Archroma at the forefront of eco-friendly reactive and sulfur dye technologies.

High-performance reactive dyes and digital color services define DyStar Group strategy

DyStar entered 2026 as a fully owned subsidiary of Zhejiang Longsheng Group, completing its ownership transition in January and streamlining governance for faster innovation. The company is doubling down on internationalization and operational resilience, supported by new board leadership appointed in February 2026. DyStar’s Levafix® and Remazol® reactive dyes remain industry benchmarks for lightfastness and wash durability, especially in sportswear and performance textiles. A key differentiator is Color Solutions International (CSI), which delivers digital color management and consulting to global fashion brands. With sustainability embedded across operations, DyStar continues to expand its footprint in eco-friendly dyestuffs and smart coloration services.

Performance materials pivot reshapes specialty dye applications at Huntsman Corporation

Following the divestment of its Textile Effects unit to Archroma, Huntsman has refocused on high-performance polyurethanes and TPU elastomers serving advanced technical textiles. Its 2026 strategy emphasizes regional optimization, producing in China for Asia and North America for domestic markets to mitigate tariff and raw material volatility. Huntsman now concentrates on automotive and aerospace applications, where lightweighting and durability are critical for EV efficiency and fuel savings. Deep integration into MDI-based rigid foams and thermoplastic polyurethanes supports cold-chain insulation and building materials, positioning Huntsman as a specialty performance supplier rather than a traditional dyestuff volume player.

Strategic transformation accelerates diversification at Kiri Industries Ltd

Kiri Industries reached a pivotal milestone in early 2026, announcing a strategic pivot backed by $688 million in DyStar sale proceeds to develop a Copper and Fertilizer Complex in Gujarat. Despite industry headwinds, the company posted 9M FY26 consolidated revenue of INR 589.15 crore, reflecting 10% year-on-year growth. While pursuing “Greenfield Transformation,” Kiri continues to supply reactive dyes and intermediates under the Kirirom and Kiractive brands, supported by zero liquid discharge dye manufacturing. This dual-track strategy enables Kiri to monetize legacy dyestuff capabilities while aligning with India’s long-term industrial and infrastructure priorities.

Vertically integrated reactive dye production scales globally at Jay Chemical Industries Private Limited

Jay Chemical stands among the world’s largest producers of reactive dyes, leveraging full backward integration to maintain quality control and global cost competitiveness. Its Jakazol and Jakofix portfolios support exhaust, cold pad-batch, and digital textile printing processes. The company has expanded into digital textile inks through its German subsidiary, marketing the Antelos® range for natural and synthetic fibers. In 2026, Jay also broadened its SURTEN specialty chemicals line into water treatment and construction additives. With in-house intermediates manufacturing, Jay Chemical continues to strengthen its position as a high-volume merchant supplier across apparel, home textiles, and emerging digital print applications.

China: Waterless Dyeing Scale-Up and Vertical Integration Momentum

China’s dyestuff market is entering a decisive phase marked by radical process innovation and upstream-downstream consolidation. At Intertextile Shanghai in September 2025, Exponent Envirotech showcased its ECOHUES™ waterless dyeing technology, followed by the announcement of a full-scale commercial plant in Northwest China. This facility eliminates salt usage and achieves near-zero wastewater discharge, directly addressing long-standing environmental bottlenecks in cellulose and biomass fiber dyeing. The technology is strategically aligned with China’s tightening water-use quotas and is expected to reshape cost structures for inland textile clusters that face acute water stress.

Parallel to process innovation, China is reinforcing petrochemical integration to secure dyestuff intermediates. BASF confirmed in October 2025 that its Zhanjiang Verbund site remains on track for a late-2025 startup. The site will supply high-performance intermediates for reactive dyes and dispersants, cutting logistics complexity and delivering an estimated €1.3 billion reduction in capital intensity through integrated production. Regulatory pressure is accelerating portfolio shifts. Under the MIIT 2025 Green Packaging and Chemical Regime, domestic mills are phasing out sulfur black dyes in favor of eco-certified alternatives, driving a 25% rise in aniline-free indigo adoption in denim manufacturing. Structurally, the June 2025 move by Zhejiang Longsheng Group toward full ownership of DyStar Group resolves governance uncertainty and strengthens China’s control over global reactive and disperse dye supply chains. Looking ahead, the National Champion initiative targets 70% domestic content in ultra-high-purity dyes for electronics and digital printing by 2026, signaling a strategic push into premium applications.

India: Infrastructure-Led Scale and Digital Printing Acceleration

India’s dyestuff market evolution is being shaped by large-scale infrastructure investment and policy-backed capacity expansion. The confirmation of ₹4,445 crore funding for seven PM MITRA textile parks through 2028 provides dyestuff producers with plug-and-play access to common effluent treatment plants. This shared infrastructure reduces upfront compliance capital by roughly 20%, materially improving the economics of new dye manufacturing projects. These parks are emerging as integrated hubs where dyestuff, textile processing, and apparel units co-locate, shortening lead times and improving export readiness.

Policy incentives are translating into tangible capacity additions. By March 2025, the Production Linked Incentive scheme for chemicals had mobilized ₹1.76 lakh crore in investments, enabling firms such as Kiri Industries and Dorf Ketal to expand high-performance reactive dye output. Sustainability-led R&D is also gaining prominence. In December 2025, Archroma supported the Institute of Chemical Technology in Mumbai to establish a laboratory focused on low-temperature, neutral-pH dyeing systems, aligning with national carbon-reduction goals. Export competitiveness received a boost when the Ministry of Textiles extended export obligation timelines from 6 to 18 months in November 2025, easing pressure from Quality Control Orders. Demand-side momentum is strongest in digital textiles, with water-based pigment inks seeing rapid uptake as digital printing capacity in Surat and Tirupur rose 14% year over year by Q4 2025.

Germany (European Union): Regulatory Tightening and Process Reinvention

Germany’s dyestuff market reflects the EU’s broader pivot toward regulatory stringency and process efficiency. In September 2025, BASF announced its exit from the hydrosulfites business and the closure of its Ludwigshafen facility, signaling a structural move away from energy- and emission-intensive reducing agents toward electrolytic and bio-based alternatives. This decision underscores how sustainability considerations are reshaping legacy dyeing chemistries across Europe.

Regulatory change remains a dominant force. The European Commission is preparing a targeted REACH recast for 2026 that will impose stricter controls on Substances of Very High Concern in dye mixtures. Complementing this, Commission Regulation (EU) 2025/1090 restricts solvents such as DMAC and NEP, compelling dye manufacturers to redesign synthesis routes before December 2026. Innovation is emerging as a competitive response. In December 2025, CHT Group received the German Sustainability Award for its PIGMENTURA process, which eliminates steaming and washing steps and cuts energy use by up to 50%. These advances position Germany as a hub for low-energy, low-water dyeing technologies tailored to high-value European textiles.

United States: Manufacturing Consolidation and Brand-Led Sustainability

The U.S. dyestuff market is characterized by consolidation and downstream sustainability partnerships rather than large-scale capacity expansion. In April 2025, DyStar Group announced the shutdown of its Hilton Davis facility in Cincinnati, integrating FD&C dye and pigment dispersion production into its Reidsville and Cheyenne plants. This rationalization reflects a focus on operational efficiency and regulatory compliance within a smaller domestic manufacturing footprint.

Sustainability-driven differentiation is increasingly brand-led. In October 2025, Archroma won the ITMF Sustainability Award for its DENIM HALO aniline-free indigo system, which reduces water use by 40 to 56% and aligns with 2030 ESG targets of U.S. apparel brands. Further, the December 2025 partnership between Archroma and Innovo Fiber to scale the Fibre52 low-temperature bleaching system highlights a shift toward integrated dye-bleach solutions. On the regulatory front, the U.S. EPA’s 2025 expansion of the Safer Chemical Ingredients List to include 12 new dyestuff intermediates is encouraging the use of biodegradable colorants in household and institutional cleaning applications, opening adjacent demand streams beyond textiles.

Dyestuff Market: Country-Level Strategic Snapshot

Dyestuff Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Focus Areas

|

Structural Direction

|

|

China

|

Waterless dyeing and vertical integration

|

Reactive, disperse, digital printing dyes

|

Domestic self-sufficiency, eco-certified scale

|

|

India

|

Textile park infrastructure and PLI incentives

|

Reactive dyes, pigment inks

|

Capacity expansion with compliance efficiency

|

|

Germany

|

REACH tightening and energy efficiency

|

Pigments, sustainable processes

|

Process reinvention and solvent substitution

|

|

United States

|

Manufacturing consolidation and ESG demand

|

Indigo systems, FD&C dyes

|

Brand-driven sustainability adoption

|

Dyestuff Market Report Scope

Dyestuff market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$326.9 Million

|

|

Market Size (2034)

|

$571.3 Million

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Dye Type (Reactive Dyes, Disperse Dyes, Direct Dyes, Acid Dyes, Vat Dyes, Basic Dyes, Organic Pigments), By Application Technique (Exhaust Dyeing, Continuous Dyeing, Printing, Mass Coloration), By Fiber Type (Natural Fibers, Synthetic Fibers, Blended Fibers, Cellulose-Based Fibers), By End-Use Industry (Apparel and Fashion, Home Textiles, Automotive Textiles, Technical Textiles, Paper and Pulp, Leather and Fur, Food, Drug, and Cosmetic)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huntsman Corporation, Archroma, Zhejiang Longsheng Group, Kiri Industries Ltd., BASF SE, Zhejiang Runtu Co., Ltd., Kyung-In Synthetic Corporation, CHT Group, Everlight Chemical Corporation, Atul Ltd., Dorf Ketal Chemicals, Bodal Chemicals Ltd., Jay Chemical Industries Private Limited, Yorkshire Group, Meghmani Organics Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dyestuff Market Segmentation

By Dye Type

- Reactive Dyes

- Disperse Dyes

- Direct Dyes

- Acid Dyes

- Vat Dyes

- Basic Dyes

- Organic Pigments

By Application Technique

- Exhaust Dyeing

- Continuous Dyeing

- Printing

- Mass Coloration

By Fiber Type

- Natural Fibers

- Synthetic Fibers

- Blended Fibers

- Cellulose-Based Fibers

By End-Use Industry

- Apparel and Fashion

- Home Textiles

- Automotive Textiles

- Technical Textiles

- Paper and Pulp

- Leather and Fur

- Food, Drug, and Cosmetic

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dyestuff Industry

- Huntsman Corporation

- Archroma

- Zhejiang Longsheng Group

- Kiri Industries Ltd.

- BASF SE

- Zhejiang Runtu Co., Ltd.

- Kyung-In Synthetic Corporation

- CHT Group

- Everlight Chemical Corporation

- Atul Ltd.

- Dorf Ketal Chemicals

- Bodal Chemicals Ltd.

- Jay Chemical Industries Private Limited

- Yorkshire Group

- Meghmani Organics Ltd.

*- List not Exhaustive