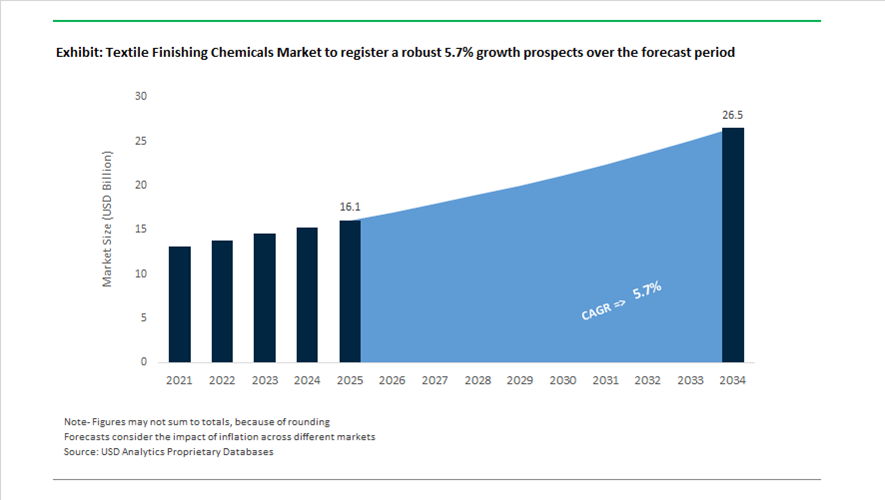

Textile Finishing Chemicals Market 2025–2034: $16.1 Billion to $26.5 Billion at 5.7% CAGR Driven by PFAS-Free Reformulation, ZDHC Compliance, and Integrated Application Technologies

The global textile finishing chemicals market is valued at $16.1 billion in 2025 and is projected to reach $26.5 billion by 2034, expanding at a CAGR of 5.7%. The segment covers softeners, fixing agents, repellents, antimicrobial treatments, wrinkle-free agents, and high-performance polymeric finishes applied to apparel, home textiles, automotive fabrics, and technical fibers. Market expansion is being shaped by regulatory elimination of PFAS, growing adoption of ZDHC MRSL Level 3 standards, and brand-driven sustainability mandates across global apparel supply chains. Manufacturers are prioritizing bio-based content, low-temperature curing systems, waterless application technologies, and digitalized production platforms to reduce carbon intensity and effluent discharge.

Sustainability-led partnerships and distribution consolidation accelerated in 2025–2026. On February 1, 2026, RUDOLF GmbH assumed exclusive global distribution rights for Sanitized® technologies, consolidating antimicrobial and odor-control finishing solutions within its global supply chain. In January 2026, Archroma entered a strategic partnership with HeiQ to scale bio-based antimicrobial and freshness technologies for performance apparel. Archroma further strengthened its compliance profile in December 2025 by securing “Champion” status at the adiFormulator Awards, reflecting progress toward 80% ZDHC MRSL Level 3 alignment. In January 2026, Pulcra Chemicals launched STABIFIX® NBF, a next-generation fixing agent engineered to meet 2026 environmental standards while enhancing polyamide color fastness. Earlier, in January 2024, RUDOLF introduced bio-based HYDROCOOL® technologies with up to 87% renewable content, signaling structural migration away from petroleum-derived auxiliaries.

Process integration and operational restructuring are reshaping cost structures and innovation cycles. In February 2026, Rieter Holding AG completed the acquisition of Barmag, integrating fiber extrusion and finishing technologies to enable in-line application of specialized chemical finishes. In February 2026, Rossari Biotech partnered with Sadara Chemical Company to localize textile chemical production in Saudi Arabia, supporting Middle Eastern supply chain resilience. In December 2025, CHT Group received the German Sustainability Award for PIGMENTURA, a binder-free pigment dyeing and finishing process that significantly lowers water and energy consumption. Meanwhile, Dow Inc. launched its “Transform to Outperform” restructuring initiative in January 2026 to improve EBITDA through AI-driven automation, influencing global finishing intermediate production efficiency. Evonik Industries advanced its “Evonik Tailor Made” program during 2025–2026 to streamline operations and concentrate on high-margin sustainable textile polymers.

Regulatory-Led Reformulation and Functional Value Creation in the Textile Finishing Chemicals Market

PFAS-Based DWR Phase-Out Forces Structural Shift Toward Fluorine-Free Chemistries

The textile finishing chemicals market entered a compliance-driven transformation phase in 2025 as PFAS elimination moved from brand-level sustainability commitments to enforceable law. Regulations such as California AB 1817 and Minnesota’s Amara’s Law have made the use of intentionally added PFAS in textiles commercially untenable across North America. Under California’s framework, apparel sold from January 2025 must remain below 100 ppm of total organic fluorine, with an already legislated tightening to 50 ppm by 2027. These thresholds effectively exclude all legacy C6 and C8 fluorocarbon-based Durable Water Repellents, accelerating a market-wide pivot toward silicone-based, paraffin-based, and dendrimer DWR systems.

Certification bodies are reinforcing this shift. bluesign implemented a full PFAS ban across all bluesign® APPROVED chemistries from January 2025, while OEKO-TEX® replaced extractable fluorine testing with total fluorine limits, closing prior compliance loopholes. As a result, fluorine-free finishing chemistries are no longer positioned as eco-premium alternatives but as the baseline requirement for market access, particularly in performance apparel, outdoor wear, and children’s textiles. Chemical suppliers that cannot demonstrate fluorine-free compliance at scale are increasingly excluded from long-term sourcing agreements with global brands and tier-one mills.

Bio-Based Softeners Scale Beyond Niche Use Into Premium and Circular Fashion

Alongside water repellents, fabric softeners are undergoing a parallel transformation driven by scrutiny over petrochemical surfactants and wastewater toxicity. Luxury apparel, babywear, and circular fashion brands are explicitly specifying plant-derived and low-toxicity softeners to support ESG disclosures and extended producer responsibility requirements. In September 2025, Archroma launched SILIGEN® D2W LIQ C, positioned as a high-durability bio-silicone softener capable of maintaining softness over repeated wash cycles. Its cross-linkable microemulsion architecture directly addresses one of the key historical limitations of bio-based softeners, namely poor wash permanence.

Innovation is also extending into polysaccharide-derived additives. In October 2025, Syensqo introduced Easysoft PA, a guar-based sensory enhancer that allows mills to reduce quaternary ammonium compound usage without compromising hand-feel. This is particularly relevant in regions with tightening effluent discharge limits, where quats are increasingly flagged for aquatic toxicity. Collectively, these developments indicate that bio-based softeners are transitioning from compliance-driven substitutions to performance-equal solutions suitable for premium positioning and long garment life cycles.

Verification-Centric Antimicrobial Finishes for Activewear and Healthcare Textiles

The convergence of wellness-driven consumer demand and institutional infection control has created a high-growth opportunity for antimicrobial textile finishes that are both non-leaching and verifiable. Hospital-grade textiles are setting the benchmark. Peer-reviewed studies validated by institutions such as Johns Hopkins Hospital demonstrate that silver-treated surgical gowns and bed linens significantly reduce bacterial surface loads in high-contact environments. By 2025, hospitals in Germany and Italy had standardized silver-based antimicrobial finishes for staff uniforms and drapes, embedding antimicrobial performance into procurement criteria rather than treating it as an optional add-on.

At the same time, bio-based antimicrobials are scaling rapidly in consumer applications. While silver compounds still account for more than 60% of the functional antimicrobial segment, bio-derived agents such as chitosan and plant-based extracts are expanding at a faster rate due to their non-toxic, non-leaching profiles. By 2025, the bio-based antimicrobial finishing segment reached an estimated value of $1.5 billion, driven largely by activewear brands seeking odor control solutions that align with clean-label and skin-safety narratives. For chemical suppliers, third-party validation and durability testing are now critical differentiators in securing contracts across both healthcare and lifestyle segments.

Conductive and ESD-Control Finishes Enable the Transition to Smart and Medical Textiles

The evolution of textiles into active electronic platforms is unlocking demand for conductive and electrostatic discharge control finishes that preserve breathability and mechanical flexibility. Research breakthroughs in 2024 and 2025 accelerated this shift. In February 2025, researchers at IIT Guwahati demonstrated water-repellent conductive textiles capable of converting electrical and solar inputs into heat, positioning fabrics as functional energy interfaces rather than passive substrates.

Commercial development is moving beyond metallic coatings toward conductive polymers such as polyaniline and hybrid polymer-fiber systems. In December 2024, researchers at Washington University reported a polymer-cotton hybrid that maintains textile flexibility while enabling stable electrical conductivity. These advances are particularly relevant for ECG-monitoring garments, rehabilitation wearables, and defense applications where electromagnetic interference control and signal integrity are mission-critical. As the global conductive textile market surpasses $3 billion, finishing chemical suppliers that can deliver durable, washable, and certification-ready conductive finishes are positioned to capture a disproportionate share of future value creation.

Textile Finishing Chemicals Market Share and Segmentation Insights

Chemical Type Market Share: Softeners Lead with High-Volume Consumption and Hydrophilic Innovation

Softeners dominate the textile finishing chemicals market with a 32.80% share in 2025, driven by their essential role in enhancing fabric hand feel, smoothness, and overall comfort across apparel and home textiles. Silicone-based softeners remain the industry standard due to their ability to deliver a premium tactile experience and durability. Other chemical types such as repellent and release agents, anti-wrinkle agents, flame retardants, antimicrobial agents, moisture management agents, and other functional finishes serve specialized performance needs. A key trend is the rise of hydrophilic softeners, which combine softness with improved absorbency and moisture management, supporting demand in activewear, towels, and next-to-skin textile applications.

End-Use Industry Market Share: Apparel Segment Anchors Demand with Performance Finishing Requirements

Apparel accounts for 48.60% of the textile finishing chemicals market in 2025, reflecting the extensive use of finishing agents to enhance comfort, durability, and functionality in garments. The segment requires diverse chemical treatments including softeners, anti-wrinkle agents, repellents, and antimicrobial finishes to meet evolving consumer expectations. Home textiles and technical textiles contribute additional demand with application-specific requirements. A major growth driver is the expansion of performance apparel and athleisure segments, where advanced finishes such as moisture management, UV protection, odor control, and durable water repellency are increasingly integrated, with formulations engineered to maintain effectiveness after repeated washing cycles.

Textile Finishing Chemicals Market Competitive Landscape

The textile finishing chemicals market in 2026 is shaped by formula transparency and low-impact curing technologies. Leading players are deploying bio-based silicones, probiotic finishes, and nanotechnology-driven agents to achieve performance parity with legacy chemistries while enabling Right-First-Time (RFT) processing and reducing VOC emissions, water usage, and curing energy intensity.

Archroma Integrates Legacy Chemical Giants into SUPER SYSTEMS+ for Ultra-Low Resource Textile Finishing

Archroma dominates the textile finishing chemicals market as a technology powerhouse following the integration of Huntsman Textile Effects and legacy brands like Ciba, Sandoz, Hoechst, and BASF. Its SUPER SYSTEMS+ platform enables up to 80% water savings through fiber-specific optimized finishing recipes. The exclusive global distribution of Fibre52® chemistry in 2026 establishes a benchmark for low-temperature, neutral-pH processing of cotton/polyester blends. Collaboration with HeiQ strengthens antimicrobial and odor-control capabilities for athleisure and hygiene textiles. As a founding SCTI member, Archroma is advancing traceable, eco-compliant finishing chemistries. Its integrated portfolio supports scalable RFT processing across fashion, automotive, and technical textiles.

DyStar Enhances Cost-Efficient Finishing with Integrated Supply Chain and ISO-Certified Operations

DyStar has reinforced its global position after becoming a fully integrated subsidiary of Zhejiang Longsheng Group in 2026. This transition enhances upstream-downstream synergies and resolves long-standing ownership complexities. The company’s regional restructuring supports growth in medical textiles and high-durability workwear segments. ISO 14001 certification of its Gabus plant strengthens its environmental compliance credentials. Consolidation of North American operations has reduced fixed costs and improved profitability in its finishing chemicals division. DyStar continues to leverage its integrated manufacturing backbone to deliver high-performance, resource-efficient textile finishing solutions.

RUDOLF Advances PFAS-Free Finishing with BIONIC-FINISH® and Certified Carbon Transparency Programs

RUDOLF leads the PFAS-free textile finishing transition through its BIONIC-FINISH® ECO platform and advanced hygiene technologies. The 2026 integration of Sanitized® solutions expands its portfolio with Silvertec™, Puretec™, and Odorex™ for antimicrobial and odor-neutralizing applications. Its OX20 technology introduces non-biocidal odor control using physical adsorption, maintaining durability over 50+ wash cycles with GOTS compliance. The PCF-certified platform provides verified carbon footprint data aligned with PACT and TfS standards. Leadership restructuring under CEO Marcos Furrer is accelerating expansion in Asia and North America. RUDOLF is targeting high-performance segments requiring durable, sustainable finishing chemistries.

CHT Sets Benchmark in Waterless Dyeing and Bio-Based Fixation for Circular Textile Processing

CHT is a specialized leader in sustainable textile finishing, recognized for its PIGMENTURA process, which reduces water consumption by over 90% and eliminates energy-intensive pad-steam operations. Its PAFIX BOND bio-based fixing agent meets ZDHC MRSL standards while delivering high wash and perspiration fastness for polyamide fabrics. ARRISTAN rAIR introduces a circular finishing solution derived from recycled PET, supporting textile-to-textile recyclability. Recognition from adidas through the adiFORMULATOR AWARD highlights its innovation leadership in performance apparel. CHT continues to focus on low-impact, high-efficiency finishing chemistries aligned with circular economy goals.

Pulcra Expands Bio-Based Finishing Portfolio with Advanced Fixation and PFAS-Free Water Repellents

Pulcra Chemicals is strengthening its position through tailor-made finishing solutions and bio-based auxiliaries. The launch of STABIFIX® NBF enhances wet fastness in polyamide textiles without hazardous crosslinkers. Its PULCRA TEC® NFS platform addresses the performance gap in PFAS-free DWR finishes, eliminating yellowing while maintaining high water repellency. Integration of Devan Chemicals has expanded capabilities in thermoregulation and probiotic finishes for home textiles. EcoVadis Silver recognition reflects strong ESG performance across global operations. Pulcra’s portfolio supports sustainable, high-performance finishing in technical and consumer textile segments.

Evonik Targets High-Purity Additives and Silicone Polymers for Advanced Textile Applications

Evonik is repositioning its textile finishing chemicals portfolio toward high-margin specialty additives within its Advanced Technologies segment. Achieving €1.87 billion EBITDA in 2025, the company is reinvesting in silicone-based polymers and high-purity crosslinkers. Its Tailor Made efficiency program accelerates commercialization of advanced materials for polyurethane foams and technical textiles. Growth in high-performance plastics supports applications in 3D printing, membranes, and performance apparel. Evonik is targeting a medium-term ROCE of 11% by shifting away from commodity chemicals. Its finishing solutions are critical for durability, breathability, and functional performance in next-generation textile systems.

India Textile Finishing Chemicals Market Driven by Park-Level Infrastructure and R&D Localization

India’s textile finishing chemicals market is entering a structurally upgraded phase, anchored by the integration of finishing operations into PM MITRA mega parks during 2025–2026. These seven parks, backed by ₹28,711 crore of committed investment under the PLI framework, are designed with centralized Zero Liquid Discharge infrastructure engineered specifically to manage the high Chemical Oxygen Demand associated with modern resins, softeners, antimicrobials, and functional coatings. This configuration is materially shifting demand toward low-liquor-ratio, high-exhaustion finishing chemicals that are compatible with centralized effluent treatment and real-time compliance monitoring.

Policy alignment is reinforcing this transition. The revised PLI 2.0 scheme lowered entry thresholds for manufacturers of man-made fiber and technical textiles, accelerating adoption of advanced moisture-management, anti-microbial, and durability-enhancing finishes. On the innovation side, domestic capability building is visible in the R&D redirection by Balaji Amines toward enzymatic synthesis of specialty amines for bio-polishing applications, directly addressing export-led demand for sustainable denim finishing. Academic–industry collaboration is also gaining momentum, with Archroma entering a strategic research partnership with V.J.T.I. Mumbai in late 2025 to accelerate green chemistry solutions for the domestic finishing chemicals market. Complementing this, the Amended Technology Upgradation Fund Scheme enabled 10–15% capital subsidies in 2025 for stenter and padding equipment upgrades, allowing precise dosing of next-generation finishing formulations.

China Textile Finishing Chemicals Market Shaped by Mega-Integration and PFAS-Free Export Readiness

China continues to recalibrate its textile finishing chemicals market through scale integration and regulatory-driven efficiency. In 2025, Sinopec’s Yizheng Chemical Fiber complex reached full operational status, integrating short-process polyester intermediates with downstream finishing chemical production. This integration has delivered an estimated 15% reduction in energy intensity, favoring finishing formulations optimized for short-process and continuous application environments.

Looking ahead, fiscal signals under the preparatory phase of the 15th Five-Year Plan point to expanded state support in 2026 for “New Quality Productive Forces,” explicitly including high-purity textile chemical synthesis and intelligent manufacturing. Regulatory enforcement is already shaping plant design. MIIT’s 2025 Green Manufacturing Roadmap mandates low-temperature oxidation and wastewater heat recovery for all new finishing units, structurally favoring chemicals that perform effectively under reduced thermal loads. Market signaling from China Interdye 2025 further confirms this shift, where PFAS-free and non-formaldehyde DWR systems such as the PHOBOTEX range were positioned as baseline requirements for export-oriented textile finishing.

Germany Textile Finishing Chemicals Market Defined by Award-Led Innovation and EU Regulatory Leadership

Germany represents the compliance and innovation benchmark within the global textile finishing chemicals market. Recognition such as the 2025 German Sustainability Award awarded to CHT Group for its PIGMENTURA solution underscores the market’s emphasis on solvent-free, energy-efficient pigment dyeing and finishing systems. These technologies are increasingly preferred by European mills seeking to reduce Scope 1 and Scope 2 emissions without compromising color fastness or surface uniformity.

Regulatory preparedness is a defining feature. German suppliers have moved decisively toward fluorine-free DWR systems, with firms such as Rudolf Group completing a full transition of their portfolios by late 2025 to comply with EU PFHxA thresholds. At the same time, advanced functional finishes are scaling through patented platforms such as Archroma’s Pyroshell flame-retardant technology, which began wider deployment across German sites from November 2025. Upstream decarbonization is also influencing finishing chemistry, as BASF SE expanded methane pyrolysis pilots in Ludwigshafen to supply low-carbon hydrogen for amine and ammonia synthesis used in textile auxiliaries.

France Textile Finishing Chemicals Market Accelerated by Statutory PFAS Exit Timelines

France has emerged as one of the most regulation-intensive markets for textile finishing chemicals following the enactment of Law No. 2025-188. This legislation mandates a ban on PFAS in clothing textiles and waterproofing agents effective January 2026, creating an immediate substitution cycle across the finishing value chain. Unlike phased approaches elsewhere in Europe, the French framework applies direct fiscal pressure through a polluter-pays tax of €100 per 100 grams of PFAS released, making continued use of fluorinated finishes economically unviable.

The regulatory trajectory is unambiguous. France has established a 2030 deadline to extend the PFAS ban to all textile applications, including industrial and technical textiles, with only narrow safety-related exemptions. This has structurally increased demand for silicone-based, hydrocarbon-based, and bio-derived waterproofing and stain-resistance finishes that can meet durability requirements under repeated laundering and abrasion without regulatory exposure.

Bangladesh Textile Finishing Chemicals Market Anchored in Green Factory Certification

Bangladesh’s textile finishing chemicals market is increasingly driven by factory-level sustainability credentials rather than purely cost competitiveness. In 2025, the country recorded 36 new international LEED certifications, including 22 Platinum-rated factories, a milestone that directly elevates demand for eco-certified finishing chemicals with documented life-cycle performance. These factories are prioritizing low-formaldehyde resins, enzymatic pre-treatments, and finishing agents capable of operating at reduced process temperatures.

Access to sustainability-linked finance is accelerating adoption. The Asian Development Bank’s $30 million sustainability-linked loan to Envoy Textiles in October 2025 is emblematic of how financing is being tied to energy-efficient finishing and processing upgrades. With the Ready-Made Garment sector targeting a 50% reduction in greenhouse gas emissions by 2030, finishing chemicals that enable effective processing at 40°C–50°C are becoming standard specifications rather than premium options.

Vietnam Textile Finishing Chemicals Market Positioned Around Trade-Driven Upgrading

Vietnam’s textile finishing chemicals market is closely aligned with its export upgrade strategy. With garment and textile exports reaching $46 billion in 2025, manufacturers are shifting toward higher value-added product lines that require advanced technical finishes for durability, comfort, and compliance in EU and U.S. markets. This transition is elevating demand for low-VOC, non-toxic finishing chemicals capable of meeting stringent buyer audits.

Infrastructure alignment under the VTG 2025 initiative is reinforcing this trend. To remain competitive under the EU-Vietnam Free Trade Agreement, Vietnamese mills are accelerating adoption of eco-compliant finishing agents that support traceability, reduced emissions, and consistent batch-to-batch performance. As a result, finishing chemistry is increasingly treated as a strategic enabler of trade access rather than a downstream consumable.

Comparative Snapshot: Textile Finishing Chemicals Market by Country

Textile Finishing Chemicals Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Regulatory or Infrastructure Trigger

|

Structural Impact on Finishing Chemicals

|

|

India

|

PM MITRA parks, PLI 2.0

|

ZLD infrastructure, ATUFS upgrades

|

Shift to low-liquor, high-exhaustion formulations

|

|

China

|

Mega-unit integration

|

MIIT green manufacturing mandates

|

Demand for energy-efficient, PFAS-free finishes

|

|

Germany

|

Innovation and compliance leadership

|

EU PFHxA thresholds, ZDHC Level 3

|

Premium solvent-free and fluorine-free systems

|

|

France

|

Statutory PFAS bans

|

Law No. 2025-188, polluter-pays tax

|

Rapid substitution of fluorinated finishes

|

|

Bangladesh

|

Green factory certification

|

LEED adoption, sustainability-linked finance

|

Growth in eco-certified, low-temperature finishes

|

|

Vietnam

|

Export upgrading

|

EVFTA compliance requirements

|

Increased uptake of low-VOC technical finishes

|

Textile Finishing Chemicals Market Report Scope

Textile Finishing Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16.1 Billion

|

|

Market Size (2034)

|

$26.5 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Chemical Type (Softeners, Repellent and Release Agents, Flame Retardants, Anti-Wrinkle Agents, Antimicrobial Agents, Moisture Management Agents, Other Functional Finishes), By Substrate Type (Natural Fibers, Synthetic Fibers, Blended Fibers), By Application Process (Pad-Dry-Cure Method, Exhaust Processing, Coating and Lamination, Spray and Foam Application), By End-Use Industry (Apparel, Home Textiles, Technical Textiles)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archroma, BASF SE, Huntsman Corporation, CHT Group, Rudolf GmbH, DyStar Group, Evonik Industries AG, Tanatex Chemicals, Pulcra Chemicals, Wacker Chemie AG, Dow Chemical Company, Solvay S.A., Zydex Group, HeiQ Materials AG, NICCA Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Textile Finishing Chemicals Market Segmentation

By Chemical Type

- Softeners

- Repellent and Release Agents

- Flame Retardants

- Anti-Wrinkle Agents

- Antimicrobial Agents

- Moisture Management Agents

- Other Functional Finishes

By Substrate Type

- Natural Fibers

- Synthetic Fibers

- Blended Fibers

By Application Process

- Pad-Dry-Cure Method

- Exhaust Processing

- Coating and Lamination

- Spray and Foam Application

By End-Use Industry

- Apparel

- Home Textiles

- Technical Textiles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Textile Finishing Chemicals Market

- Archroma

- BASF SE

- Huntsman Corporation

- CHT Group

- Rudolf GmbH

- DyStar Group

- Evonik Industries AG

- Tanatex Chemicals

- Pulcra Chemicals

- Wacker Chemie AG

- Dow Chemical Company

- Solvay S.A.

- Zydex Group

- HeiQ Materials AG

- NICCA Chemical Co., Ltd.

*- List not Exhaustive