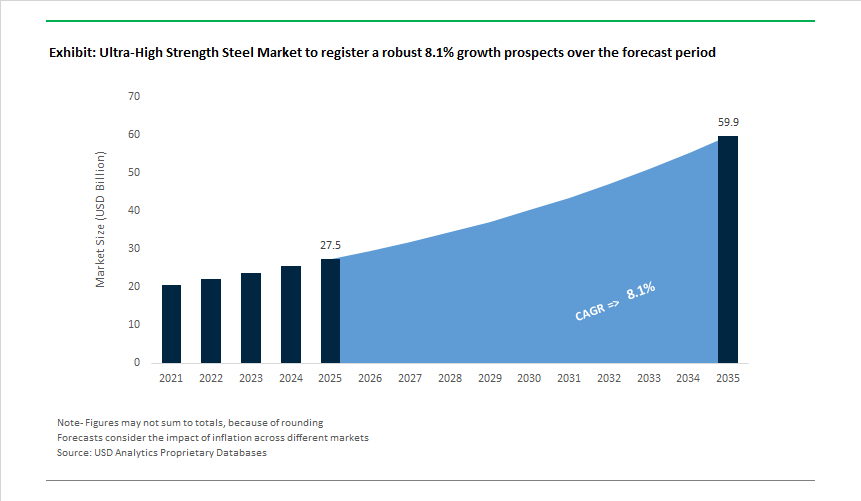

Market Value (2025): USD 27.5 Billion | CAGR (2025–2035): 8.1% | Forecast Value (2035): USD 59.9 Billion

The Ultra-High Strength Steel (UHSS) market has entered a structurally important growth phase as automotive OEMs, infrastructure developers, and defense manufacturers intensify their shift toward lightweight, crash-optimized, and low-emission material systems. By 2025, UHSS is no longer specified purely for strength; it is procured as a system-level enabler for regulatory compliance, platform modularity, and life-cycle carbon reduction. The industry benchmark has now moved decisively beyond legacy 1,500 MPa hot-stamped grades to 2,000 MPa tensile-strength steels, exemplified by hot-forming solutions such as Usibor® 2000. This step-change allows automakers to achieve 10–15% component weight reduction versus 1,500 MPa grades while maintaining identical crash-intrusion performance—directly supporting electrified vehicle range extension and multi-material BIW optimization.

From a procurement and manufacturing standpoint, UHSS adoption is increasingly justified through mass-efficiency and emissions economics rather than material substitution alone. OEM life-cycle assessments indicate that every 100 kg of UHSS integrated into a vehicle BIW delivers ~2.5 tonnes of CO₂ reduction over the vehicle’s lifetime, making UHSS one of the most cost-effective decarbonization levers available for the 2025–2030 regulatory cycle. At the same time, advances in continuous annealing furnace technologies have tightened yield-strength variation to below ±20 MPa per coil, materially reducing springback during complex cold-forming operations. This level of structural homogeneity directly lowers die-rework rates and tooling maintenance costs by an estimated ~12%, improving total cost of ownership for Tier-1 stampers.

Material innovation is also redefining design freedom. Third-generation UHSS grades now achieve a strength–ductility balance exceeding 30 GPa% (tensile strength × elongation)—a threshold that enables highly energy-absorbing crash boxes, B-pillars, and side-impact structures that previously required thicker, lower-strength steels or aluminum reinforcements. For manufacturers, this “golden ratio” unlocks thinner gauges without sacrificing formability, enabling platform standardization across ICE, hybrid, and battery-electric architectures while maintaining consistent crash performance.

Ultra-High Strength Steel Market Analysis — Strategic Alliances, Automation, and Green Steel Commitments Reshape Supply

The market landscape has been defined by consolidation, geopolitical intervention, and accelerated investment in intelligent and low-carbon steelmaking—each with direct implications for UHSS availability and pricing. In December 2025, Jindal Steel International submitted a non-binding offer exceeding €2 billion to acquire the steel division of Thyssenkrupp, coupled with commitments to deploy electric arc furnaces and execute a full green-steel transformation at the Duisburg site. The transaction signals a broader pivot toward EAF-based UHSS production in Europe, aligning structural steel supply with tightening EU carbon-border and emissions regulations.

In October 2025, Cleveland-Cliffs Inc. formalized POSCO as its strategic partner under a new Memorandum of Understanding following the U.S.–Korea trade agreement. The alliance is designed to secure domestic U.S. supply of automotive-grade UHSS while leveraging POSCO’s advanced metallurgy and hot-stamping expertise. During the same month, Cleveland-Cliffs reported a marked rebound in automotive steel demand, with Q3 2025 automotive sales reaching USD 1.4 billion, accounting for 30% of total steelmaking revenue—a clear indicator that OEM platforms are re-accelerating UHSS procurement after earlier volatility.

Asia-centric capacity and technology partnerships also gained momentum. In August 2025, JSW Steel and POSCO signed a Heads of Agreement to evaluate a 6 MTPA integrated steel plant in India, structured as a 50:50 joint venture focused on high-quality UHSS for domestic automotive hubs and export markets. Earlier, in May 2025, POSCO completed automation of its converter refining process at Gwangyang Works, reducing manual intervention steps from 25 to one through AI-driven heat-balance models—an advance that materially improves alloying precision for ultra-high-strength grades. Meanwhile, Baosteel announced in April 2025 a strategic shift toward “efficiency over expansion,” prioritizing high-value specialty steels within an 80-million-tonne capacity framework to mitigate domestic overcapacity and tariff exposure.

Policy intervention has further reshaped market dynamics. In June 2025, the U.S. government finalized the acquisition of a golden share in U.S. Steel, following the blocked Nippon Steel merger, ensuring federal oversight of security-critical steel supply. This was followed in February 2025 by the UK government’s launch of its comprehensive Steel Strategy, which explicitly models Direct Reduced Iron (DRI) and hydrogen-based routes to stimulate demand for domestically produced green UHSS across infrastructure and defense procurement.

Ultra-High Strength Steel Market Trends and Opportunities

Trend 1: 2.0 GPa+ Press-Hardened Steels Redefining EV Crash Architectures

The shift to 800V EV platforms has structurally altered crash-management requirements. Battery packs add 300–600 kg of concentrated mass, forcing OEMs to adopt 2.0 GPa-class press-hardened steels (PHS) that can deliver intrusion resistance without penalizing curb weight.

By late 2024 and into 2025, General Motors Global Research validated next-generation PHS grades such as 34MnBV approaching 2.0 GPa ultimate tensile strength while preserving a VDA bending angle of ~55° at 1.4 mm gauge. This combination is critical: earlier 2.0 GPa concepts failed due to brittle fracture in A- and B-pillars. The new generation absorbs impact energy through controlled bending rather than catastrophic cracking—directly improving side-pole and small-overlap crash outcomes.

Parallel progress in oxidation-resistant 20MnCr-based alloys, incorporating chromium and silicon, is eliminating the need for post-forming shot blasting. This process simplification is strategically important for high-volume EV producers such as Tesla and BYD, where takt time and surface consistency directly affect cost per vehicle.

Steelmakers including SSAB and ArcelorMittal are advancing Tailored Welded Blanks (TWB) that integrate 2.0 GPa intrusion zones with 1000–1200 MPa energy-absorbing regions. This multi-zone “integrated safety cage” is now central to meeting Euro NCAP 2025 battery protection protocols without resorting to thicker sections or aluminum substitution.

Trend 2: Isothermal Forging Accelerates Adoption of UHSS in Aerospace Load Paths

In aerospace, ultra-high strength steels are regaining strategic relevance as fatigue, damage tolerance, and landing-load reliability outweigh the absolute weight advantages of titanium. The industry is increasingly adopting isothermal forging for alloys such as 300M and AERMET 100, particularly in landing gear and arrestment-critical components.

By maintaining a constant thermal envelope throughout deformation, isothermal forging produces uniform martensitic microstructures with minimal residual stress. In 2025, aerospace adoption of this process increased by ~14.6%, driven by its ability to reliably meet ~300 ksi (≈2.07 GPa) tensile strength requirements without compromising fracture toughness. This consistency is essential for wide-body aircraft and next-generation fighters, where landing gear must survive extreme sink rates and carrier-based arrestment loads.

Equipment suppliers such as SMS Group and materials specialists like ATI are deploying real-time thermal and strain monitoring to reduce scrap and machining allowances. For premium alloys like AERMET 100, near-net-shape isothermal forging materially lowers buy-to-fly ratios, improving both cost efficiency and supply chain resilience.

Fatigue testing conducted through 2025 confirms that isothermally forged UHSS components exhibit slower crack-growth rates and higher endurance limits than conventionally forged equivalents—making them indispensable for sixth-generation fighter and Next-Generation Air Dominance (NGAD) programs.

Opportunity 1: Boron-Alloyed Martensitic UHSS for Military Lightweighting

Defense modernization programs are creating a high-value opportunity for boron-alloyed martensitic UHSS as replacements for traditional Rolled Homogeneous Armor (RHA). Under the U.S. Army’s Next Generation Combat Vehicle (NGCV) initiative, vehicle mass targets are falling from ~60 tons toward the 30–40 ton class, without compromising ballistic protection.

High-hardness steels exceeding HB 550 are enabling ~35% reductions in armor thickness while maintaining resistance to 7.62 mm AP threats. Unlike legacy armor steels, modern UHSS grades balance hardness with weldability, allowing for monocoque hull construction that improves stiffness and reduces part count.

R&D investments in 2025 are accelerating nano-crystalline and dual-hard architectures, where an ultra-hard strike face is metallurgically bonded to a tougher backing layer. These materials shatter projectiles on impact while suppressing spall—one of the most dangerous secondary failure modes for vehicle crews. The result is lighter, faster platforms with improved strategic mobility across bridges, roads, and expeditionary terrain.

Opportunity 2: Hydrogen-Resistant UHSS for High-Pressure Gas Storage and Transport

The scale-up of green hydrogen is opening a specialized but critical opportunity for hydrogen-tolerant quenched & tempered UHSS, particularly in Type I all-metal cylinders and emerging pipeline systems.

In February 2025, researchers at National Cheng Kung University introduced 416B and 420L weldable steels engineered with acicular microstructures that are ~2× more resistant to atomic hydrogen penetration than conventional 316L stainless steel. This directly addresses hydrogen embrittlement—the primary failure risk in compressed gas storage.

Commercial manufacturers such as heiserTEC are already deploying monolithic UHSS cylinders that are 10–30% lighter than standard designs while meeting ISO 9809-1 and UN/DOT certification. These tanks enable transport payloads exceeding 1,400 kg of compressed hydrogen per truck, materially improving logistics efficiency.

Beyond cylinders, weldable UHSS grades with >950 MPa yield strength are being qualified for hydrogen pipelines. Consumable innovation from voestalpine Böhler Welding in 2025 is ensuring that welded joints retain ductility and resist stress corrosion cracking even under 100% hydrogen service, positioning UHSS as a cornerstone material for future hydrogen networks.

Market Share Analysis: Ultra-High Strength Steel Market

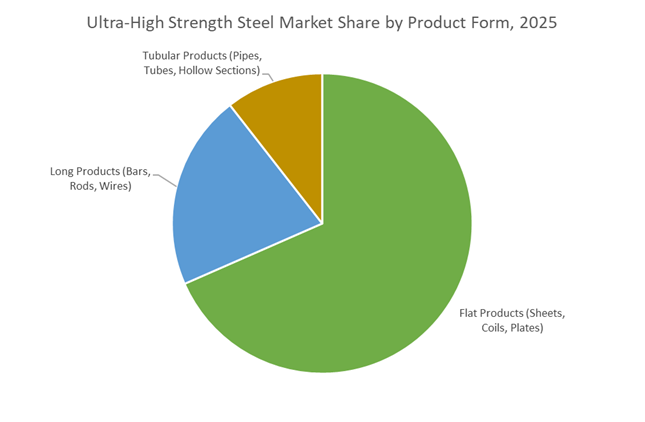

Market Share by Product Form: Flat UHSS Products Anchor Body-in-White Lightweighting Economics

Flat ultra-high strength steel (UHSS) products command approximately 65% of total market share because they sit at the center of 2025 vehicle platform economics—specifically Body-in-White (BIW) mass optimization under EV range constraints. The commercial inflection point is the 2,000 MPa tensile strength ceiling, now achieved at scale in flat formats such as ArcelorMittal’s Usibor® 2000 and SSAB’s Docol® 2000M. This strength level enables sub-0.8 mm gauge components without compromising crash load paths, delivering an incremental 10–15% weight reduction per structural part versus 1,500 MPa press-hardened solutions. Critically, flat UHSS has crossed the cost-performance threshold: POSCO’s GIGA STEEL flat products—rated to withstand ~100 kg/mm² load—are now ~20% more cost-efficient than aluminum for equivalent stiffness and intrusion resistance, eliminating the traditional lightweighting cost penalty. The segment’s dominance is further reinforced by process compatibility with hot stamping, roll forming, and laser welding—allowing OEMs to consolidate parts and reduce downstream joining complexity. Finally, procurement is accelerating around low-carbon flat steel: SSAB Zero™ flat products (<0.05 kg CO₂e/kg steel) allow automakers to meet 2025 Scope 3 emissions targets without re-engineering BIW architectures, a decisive advantage over carbon-intensive substitutes.

Market Share by Application: Automotive Drives Structural Demand Through EV Safety and Range Mandates

Automotive applications account for around 60% of UHSS demand, reflecting the sector’s non-negotiable requirements for anti-intrusion performance, battery protection, and manufacturability at scale. By 2025, UHSS (>780 MPa) represents ~30% of total BIW mass, doubling its penetration in five years as OEMs redesign platforms for 800V EV architectures. Battery enclosure frames and safety cages now require steels capable of resisting >1,000 kN impact forces during side-pole and offset crashes to prevent cell puncture and thermal propagation—performance that UHSS delivers without the thickness penalties of conventional grades. At the same time, advances in high-formability UHSS (e.g., ArcelorMittal Fortiform®) achieving ≥90° bend angles at ~1,000 MPa enable single-piece geometries such as door rings, cutting part counts and weld operations by ~25% and directly lowering assembly cost. Safety-critical zones (A/B pillars) continue to standardize around press-hardened martensitic steels; 2025-spec PHS grades can be hot-formed and quenched within seconds to create structures that are effectively non-crushable in high-energy impacts. Combined with the need to offset battery mass while meeting stringent crash protocols, these factors make automotive the structural and economic anchor of the ultra-high strength steel market.

United States: CHIPS-Style Steel Reshoring and Infrastructure-Grade UHSS

The United States UHSS market in 2025 is being reshaped by federal reshoring policy, EV lightweighting demand, and infrastructure renewal, positioning ultra-high strength steel as a strategic industrial input rather than a commodity alloy. The landmark Nippon Steel–U.S. Steel integration finalized in June 2025 marks a pivotal shift, with nearly ¥4 trillion (~$26 billion) allocated toward modernizing U.S. and Indian operations. A key focus area is the expansion of UHSS finishing, coating, and galvanizing lines in Pennsylvania and Indiana to serve domestic EV OEMs seeking high-strength, crash-resistant steels compatible with 800V vehicle platforms.

Parallel to corporate consolidation, U.S. industrial policy is reinforcing low-carbon EAF-based UHSS production. Through 2024–2025, the U.S. Department of Energy disbursed funding from a $171 million industrial decarbonization pool, including the ASPEN LEAF project led by National Renewable Energy Laboratory and Nucor, targeting EAF efficiency and hydrogen-ready operations. Reinforced Buy American procurement rules in 2025—particularly for bridges, grid towers, and renewable substructures—are further anchoring UHSS demand to domestic supply chains, insulating U.S. producers from external volatility.

China: “New Quality Productivity” and Structural Output Discipline

China’s UHSS strategy in 2025 reflects a decisive shift from volume dominance to quality-driven steel sovereignty. Under the 2025–2026 Steel Industry Growth Plan jointly issued by the Ministry of Industry and Information Technology and allied ministries, the sector is explicitly directed to abandon scale-led expansion in favor of UHSS, bearing steels, and high-temperature alloys designated as “New Quality Productive Forces.” This policy pivot is accelerating investment in high-ductility AHSS and multiphase UHSS tailored for EV body-in-white and drivetrain components.

Environmental enforcement is acting as a powerful market filter. China’s mandate for 80% of steel capacity to complete ultra-low-emissions upgrades by end-2025 is forcing consolidation, pushing inefficient mills out while leaders such as China Baowu Steel Group scale premium UHSS output. Notably, China’s crude steel production is tracking well below 1 billion tonnes in 2025, a historic inflection that stabilizes global pricing while aligning with the country’s 2060 carbon-neutrality roadmap. For UHSS buyers, this means tighter supply but materially higher average quality, especially in automotive-grade steels.

India: PLI-Driven Specialty Steel Localization

India’s UHSS market is expanding rapidly on the back of Production Linked Incentive (PLI) schemes and Atmanirbhar Bharat procurement reforms, transforming the country from an importer of advanced grades into a localized metallurgy hub. By January 2025, the second phase of the PLI Scheme for Specialty Steel had secured ₹25,200 crore (~$3 billion) in fresh commitments from 35 companies, explicitly targeting UHSS and AHSS grades for automotive and EV applications.

Capacity expansion is being matched with green-aligned production. In April 2025, ArcelorMittal Nippon Steel India announced a ₹60,000 crore (~$7.2 billion) investment to lift Hazira’s capacity to 15 MTPA, with 70% of output aligned to India’s Green Steel Taxonomy—primarily high-strength cold-rolled and galvanized UHSS. Policy reinforcement came with the July 25, 2025 revision of the Domestically Manufactured Iron & Steel Products (DMI&SP) policy, mandating that government procurement use 100% domestically produced steel, structurally locking in demand for Indian UHSS producers across infrastructure and mobility programs.

Sweden: Commercial Leadership in Fossil-Free UHSS

Sweden remains the global reference point for carbon-neutral UHSS, moving decisively from pilot validation to commercial delivery in 2025. The HYBRIT partnership—led by SSAB, LKAB, and Vattenfall—has begun limited commercial shipments of hydrogen-reduced Docol® UHSS, produced via fossil-free direct reduction that emits water vapor instead of CO₂. This milestone establishes a credible green premium market for UHSS, particularly among European automotive OEMs.

Innovation extends beyond flat products. SSAB’s launch of the world’s first emission-free steel powder for additive manufacturing (March 2024–2025) enables 3D-printed UHSS components with exceptional strength-to-weight ratios for aerospace and advanced automotive uses. By 2025, multiple European OEMs had signed binding offtake agreements prioritizing Swedish fossil-free steel, effectively anchoring Sweden’s UHSS sector at the high-value end of global supply chains.

Japan: GX 2040 and High-Ductility Alloy Engineering

Japan’s UHSS market is structured around material science leadership and export-oriented value creation, supported by the national GX 2040 Green Transformation agenda. In December 2025, Nippon Steel unveiled a ¥6 trillion (~$40 billion) investment plan through 2030, emphasizing overseas growth while consolidating domestic blast furnaces (from 15 to 10) to focus on high-margin UHSS and AHSS for global automotive customers.

A defining differentiator is Japan’s focus on ductility at ultra-high strength levels. Collaborative development by Nippon Steel and JFE Steel has led to commercialization of jetQ® 980 and 1180 grades, engineered for complex crash geometries where formability, hole expansion, and elongation at break are critical. Concurrently, government-backed hydrogen metallurgy research under the GX Promotion Act is subsidizing the conversion of blast furnaces to EAF-based routes, ensuring that future Japanese UHSS carries a green certification premium.

Germany: Steel Realignment and Euro 7 Compliance

Germany’s UHSS landscape in 2025 is defined by structural restructuring and regulatory-driven innovation, as producers adapt to EU decarbonization and mobility standards. Thyssenkrupp Steel reached a landmark “Steel Realignment” agreement in July 2025, transitioning toward a financial holding model and seeking third-party investment to accelerate its green transformation. Central to this effort is the tkH2Steel® hydrogen-capable direct reduction project, positioning Germany for low-carbon UHSS production at scale.

Regulatory pull is equally influential. Compliance with Euro 7 standards has pushed German mills to ramp up ceramic-coated UHSS and specialty alloys for brake and exhaust systems, targeting reductions in non-exhaust particulate emissions. At Blechexpo 2025 (October) in Stuttgart, German producers showcased multiphase UHSS grades such as CH-W® 700Y950T, optimized for hole expansion and controlled elongation—properties essential for mass-produced EV chassis and safety-critical structures.

2025 Strategic Matrix: Ultra-High Strength Steel (UHSS) National Comparison

Ultra-High Strength Steel (UHSS) Strategic Matrix

|

Country

|

Strategic Driver

|

2025 Key Milestone

|

Primary UHSS Focus

|

|

United States

|

Supply-chain reshoring & infrastructure

|

Nippon Steel–U.S. Steel $26B integration

|

EAF-based UHSS finishing & coatings

|

|

China

|

“New Quality Productivity”

|

Crude steel output <1 Bt

|

High-ductility AHSS & gear steels

|

|

India

|

PLI & Atmanirbhar Bharat

|

₹25,200 Cr PLI 2.0 commitments

|

EV-grade specialty UHSS

|

|

Sweden

|

Fossil-free leadership

|

Commercial HYBRIT steel deliveries

|

Hydrogen-reduced Docol® UHSS

|

|

Japan

|

GX 2040 & export growth

|

¥6T multi-year investment plan

|

jetQ® highly ductile UHSS

|

|

Germany

|

Decarbonization & Euro 7

|

tkH2Steel® hydrogen DR project

|

Multiphase & coated chassis steels

|

Ultra-High Strength Steel Market Report Scope

Ultra-High Strength Steel Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.5 Billion

|

|

Market Size (2035)

|

$59.9 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Grade Type (DP Steel, TRIP Steel, CP Steel, Martensitic Steel, Press-Hardened Steel, TWIP Steel, Q&P Steel), By Tensile Strength (780–980 MPa, 980–1200 MPa, 1200–1500 MPa, Above 1500 MPa), By Product Form (Flat Products, Long Products, Tubular Products), By Application (Automotive, Aerospace & Defense, Construction & Infrastructure, Energy, Industrial Machinery)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ArcelorMittal S.A., Nippon Steel Corporation, SSAB AB, POSCO Holdings Inc., China Baowu Steel Group Corp. Ltd., Thyssenkrupp AG, United States Steel Corporation, Tata Steel Limited, JFE Steel Corporation, Hyundai Steel Co. Ltd., Cleveland-Cliffs Inc., Voestalpine AG, JSW Steel Limited, Nucor Corporation, Shagang Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ultra-High Strength Steel Market Segmentation

By Grade Type

- Dual-Phase (DP) Steel

- Transformation-Induced Plasticity (TRIP) Steel

- Complex Phase (CP) Steel

- Martensitic (MS) Steel

- Press-Hardened Steel (PHS)

- Twinning-Induced Plasticity (TWIP) Steel

- Quenching & Partitioning (Q&P) Steel

By Tensile Strength

- 780 MPa – 980 MPa

- 980 MPa – 1200 MPa

- 1200 MPa – 1500 MPa

- Above 1500 MPa

By Product Form

- Flat Products

- Long Products

- Tubular Products

By Application

- Automotive

- Aerospace & Defense

- Construction & Infrastructure

- Energy

- Industrial Machinery

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Ultra-High Strength Steel Market

- ArcelorMittal S.A.

- Nippon Steel Corporation

- SSAB AB

- POSCO Holdings Inc.

- China Baowu Steel Group Corp., Ltd.

- Thyssenkrupp AG

- United States Steel Corporation

- Tata Steel Limited

- JFE Steel Corporation

- Hyundai Steel Co., Ltd.

- Cleveland-Cliffs Inc.

- Voestalpine AG

- JSW Steel Limited

- Nucor Corporation

- Shagang Group

*- List not Exhaustive