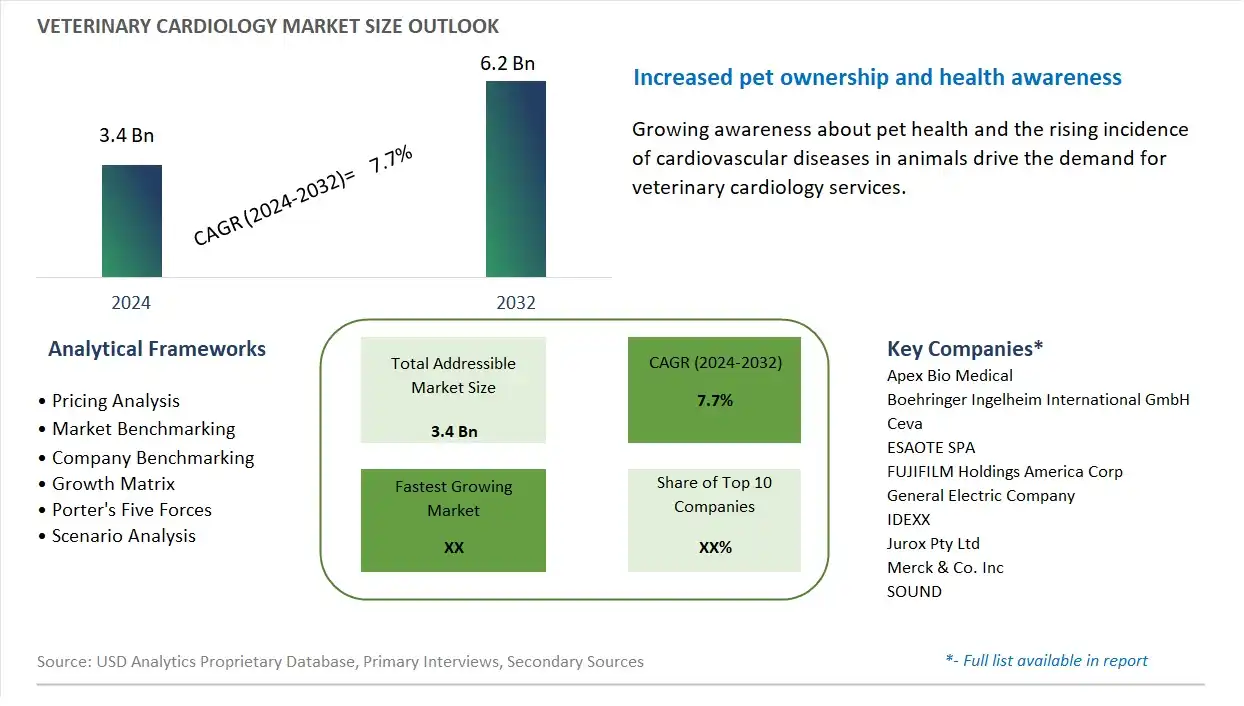

Global Veterinary Cardiology Market Size is valued at $3.4 Billion in 2024 and is forecast to register a growth rate (CAGR) of 7.7% to reach $6.2 Billion by 2032.

The global Veterinary Cardiology Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Animal (Companion Animals, Production Animals), By Product (Pharmaceuticals, Diagnostics, Congestive Heart Failure, Myocardial (Heart Muscle) Disease, Arrhythmias, Others), By End-User (Veterinary Hospitals, Clinics, Others), By Distribution Channel (Hospitals, Pharmacy, Retail, E-Commerce).

An Introduction to Veterinary Cardiology Market in 2024

The veterinary cardiology market is experiencing significant growth, driven by the increasing prevalence of cardiovascular diseases in pets and advancements in diagnostic and therapeutic technologies. As pet owners become more aware of the health needs of their animals, there is a growing demand for specialized cardiology services to address conditions such as heart murmurs, congestive heart failure, and arrhythmias in dogs and cats. The market is bolstered by advancements in veterinary imaging techniques, such as echocardiography, electrocardiography, and cardiac MRI, which enable more accurate diagnosis and management of heart diseases. Additionally, the development of innovative treatments, including advanced pharmaceuticals, surgical interventions, and minimally invasive procedures, is enhancing the effectiveness of cardiovascular care for pets. The expansion of veterinary cardiology services is also supported by increasing investments in veterinary clinics and the rise of specialty practices focused on cardiology. As pet owners prioritize the well-being of their animals and seek advanced care options, the veterinary cardiology market is poised for continued growth, reflecting broader trends in the humanization of pet care and the advancement of veterinary medical technologies.

Veterinary Cardiology Competitive Landscape

The market report analyses the leading companies in the industry including Apex Bio Medical, Boehringer Ingelheim International GmbH, Ceva, ESAOTE SPA, FUJIFILM Holdings America Corp, General Electric Company, IDEXX, Jurox Pty Ltd, Merck & Co. Inc, SOUND, and others.

Veterinary Cardiology Market Dynamics

Market Trend: Increasing Use of Advanced Diagnostic Imaging Technologies

The Veterinary Cardiology Market is experiencing a prominent trend towards the increasing use of advanced diagnostic imaging technologies. Innovations such as high-resolution echocardiography, cardiac MRI, and advanced electrocardiography are becoming more prevalent in veterinary practices. These technologies enable more accurate and detailed assessment of cardiac conditions in animals, leading to better diagnosis and treatment planning. The trend reflects a broader movement towards integrating advanced medical technologies in veterinary care to enhance diagnostic capabilities and improve patient outcomes.

Market Driver: Rising Incidence of Cardiac Diseases in Pets and Companion Animals

The rising incidence of cardiac diseases in pets and companion animals is a significant driver for the Veterinary Cardiology Market. Factors such as an aging pet population, increased awareness of pet health, and improved diagnostic capabilities contribute to the growing recognition and treatment of cardiac conditions in animals. As pet owners and veterinarians become more aware of the prevalence and impact of heart diseases in animals, the demand for specialized cardiology services and treatments is increasing. This driver is supported by the broader trend of increasing investment in pet healthcare and advanced veterinary treatments.

Market Opportunity: Development of Innovative Treatment Solutions and Telemedicine Integration

A notable opportunity for the Veterinary Cardiology Market lies in the development of innovative treatment solutions and the integration of telemedicine. Advances in cardiology treatments, such as minimally invasive procedures, novel pharmaceuticals, and personalized care plans, can address a range of cardiac conditions more effectively. Additionally, incorporating telemedicine into veterinary cardiology services allows for remote consultations, follow-up care, and second opinions, expanding access to specialized care for pet owners in remote or underserved areas. By focusing on these areas, companies can enhance their service offerings and capture growth opportunities in the evolving veterinary cardiology landscape.

Veterinary Cardiology Market Share Analysis: Pharmaceuticals generated the highest revenue in 2024

In the Veterinary Cardiology Market, the Pharmaceuticals segment is the largest. This dominance is primarily driven by the increasing prevalence of cardiovascular diseases in pets, such as congestive heart failure and myocardial diseases, which require ongoing medication for management. The development and availability of advanced pharmaceuticals, coupled with rising pet ownership and the humanization of pets, have led to higher expenditure on pet healthcare. Furthermore, the growing awareness among pet owners about the importance of cardiac health and the advancements in veterinary medicine have contributed to the significant market share held by the pharmaceuticals segment.

Veterinary Cardiology Market Share Analysis: Companion Animals is poised to register the fastest CAGR over the forecast period

The Companion Animals segment is the fastest-growing market segment in the Veterinary Cardiology Market over the forecast period to 2032. This growth is driven by several factors, including the increasing pet ownership rates and the growing trend of pet humanization, where pets are considered part of the family. Pet owners are becoming more conscious of their pets' health and are willing to invest in advanced veterinary care. Additionally, advancements in diagnostic technologies and treatments for cardiovascular diseases in companion animals, coupled with an increase in disposable incomes, enable more pet owners to afford specialized care. The rising prevalence of cardiovascular issues in pets and the growing availability of pet insurance further support the rapid expansion of this segment.

Veterinary Cardiology Market Share Analysis: Veterinary Hospitals generated the highest revenue in 2024

In the Veterinary Cardiology Market, the Veterinary Hospitals segment is the largest. This prominence is attributed to the comprehensive range of services offered by veterinary hospitals, including advanced diagnostic capabilities, specialized cardiology treatments, and surgical interventions. Veterinary hospitals are typically well-equipped with state-of-the-art technology and staffed with highly trained veterinary cardiologists, making them the preferred choice for pet owners seeking high-quality cardiac care for their animals. Additionally, the ability to handle emergency cases and provide 24/7 care further enhances the appeal of veterinary hospitals. The increasing prevalence of cardiovascular diseases in pets and the growing awareness among pet owners about the importance of specialized cardiac care contribute to the dominance of veterinary hospitals in this market segment.

Veterinary Cardiology Market Segmentation

By Animal

Companion Animals

-Dogs

-Cats

-Horses

-Others

Production Animals

-Cattle

-Poultry

-Others

By Product

Pharmaceuticals

Diagnostics

Congestive Heart Failure

Myocardial (Heart Muscle) Disease

Arrhythmias

Others

By End-User

Veterinary Hospitals

Clinics

Others

By Distribution Channel

Hospitals

Pharmacy

Retail

E-Commerce

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Veterinary Cardiology Companies Profiled in the Study

Apex Bio Medical

Boehringer Ingelheim International GmbH

Ceva

ESAOTE SPA

FUJIFILM Holdings America Corp

General Electric Company

IDEXX

Jurox Pty Ltd

Merck & Co. Inc

SOUND

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Veterinary Cardiology Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Veterinary Cardiology Market Size Outlook, $ Million, 2021 to 2032

3.2 Veterinary Cardiology Market Outlook by Type, $ Million, 2021 to 2032

3.3 Veterinary Cardiology Market Outlook by Product, $ Million, 2021 to 2032

3.4 Veterinary Cardiology Market Outlook by Application, $ Million, 2021 to 2032

3.5 Veterinary Cardiology Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Veterinary Cardiology Industry

4.2 Key Market Trends in Veterinary Cardiology Industry

4.3 Potential Opportunities in Veterinary Cardiology Industry

4.4 Key Challenges in Veterinary Cardiology Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Veterinary Cardiology Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Veterinary Cardiology Market Outlook by Segments

7.1 Veterinary Cardiology Market Outlook by Segments, $ Million, 2021- 2032

By Animal

Companion Animals

-Dogs

-Cats

-Horses

-Others

Production Animals

-Cattle

-Poultry

-Others

By Product

Pharmaceuticals

Diagnostics

Congestive Heart Failure

Myocardial (Heart Muscle) Disease

Arrhythmias

Others

By End-User

Veterinary Hospitals

Clinics

Others

By Distribution Channel

Hospitals

Pharmacy

Retail

E-Commerce

8 North America Veterinary Cardiology Market Analysis and Outlook To 2032

8.1 Introduction to North America Veterinary Cardiology Markets in 2024

8.2 North America Veterinary Cardiology Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Veterinary Cardiology Market size Outlook by Segments, 2021-2032

By Animal

Companion Animals

-Dogs

-Cats

-Horses

-Others

Production Animals

-Cattle

-Poultry

-Others

By Product

Pharmaceuticals

Diagnostics

Congestive Heart Failure

Myocardial (Heart Muscle) Disease

Arrhythmias

Others

By End-User

Veterinary Hospitals

Clinics

Others

By Distribution Channel

Hospitals

Pharmacy

Retail

E-Commerce

9 Europe Veterinary Cardiology Market Analysis and Outlook To 2032

9.1 Introduction to Europe Veterinary Cardiology Markets in 2024

9.2 Europe Veterinary Cardiology Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Veterinary Cardiology Market Size Outlook by Segments, 2021-2032

By Animal

Companion Animals

-Dogs

-Cats

-Horses

-Others

Production Animals

-Cattle

-Poultry

-Others

By Product

Pharmaceuticals

Diagnostics

Congestive Heart Failure

Myocardial (Heart Muscle) Disease

Arrhythmias

Others

By End-User

Veterinary Hospitals

Clinics

Others

By Distribution Channel

Hospitals

Pharmacy

Retail

E-Commerce

10 Asia Pacific Veterinary Cardiology Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Veterinary Cardiology Markets in 2024

10.2 Asia Pacific Veterinary Cardiology Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Veterinary Cardiology Market size Outlook by Segments, 2021-2032

By Animal

Companion Animals

-Dogs

-Cats

-Horses

-Others

Production Animals

-Cattle

-Poultry

-Others

By Product

Pharmaceuticals

Diagnostics

Congestive Heart Failure

Myocardial (Heart Muscle) Disease

Arrhythmias

Others

By End-User

Veterinary Hospitals

Clinics

Others

By Distribution Channel

Hospitals

Pharmacy

Retail

E-Commerce

11 South America Veterinary Cardiology Market Analysis and Outlook To 2032

11.1 Introduction to South America Veterinary Cardiology Markets in 2024

11.2 South America Veterinary Cardiology Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Veterinary Cardiology Market size Outlook by Segments, 2021-2032

By Animal

Companion Animals

-Dogs

-Cats

-Horses

-Others

Production Animals

-Cattle

-Poultry

-Others

By Product

Pharmaceuticals

Diagnostics

Congestive Heart Failure

Myocardial (Heart Muscle) Disease

Arrhythmias

Others

By End-User

Veterinary Hospitals

Clinics

Others

By Distribution Channel

Hospitals

Pharmacy

Retail

E-Commerce

12 Middle East and Africa Veterinary Cardiology Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Veterinary Cardiology Markets in 2024

12.2 Middle East and Africa Veterinary Cardiology Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Veterinary Cardiology Market size Outlook by Segments, 2021-2032

By Animal

Companion Animals

-Dogs

-Cats

-Horses

-Others

Production Animals

-Cattle

-Poultry

-Others

By Product

Pharmaceuticals

Diagnostics

Congestive Heart Failure

Myocardial (Heart Muscle) Disease

Arrhythmias

Others

By End-User

Veterinary Hospitals

Clinics

Others

By Distribution Channel

Hospitals

Pharmacy

Retail

E-Commerce

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Apex Bio Medical

Boehringer Ingelheim International GmbH

Ceva

ESAOTE SPA

FUJIFILM Holdings America Corp

General Electric Company

IDEXX

Jurox Pty Ltd

Merck & Co. Inc

SOUND

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

Veterinary Cardiology Market Segmentation

By Animal

Companion Animals

-Dogs

-Cats

-Horses

-Others

Production Animals

-Cattle

-Poultry

-Others

By Product

Pharmaceuticals

Diagnostics

Congestive Heart Failure

Myocardial (Heart Muscle) Disease

Arrhythmias

Others

By End-User

Veterinary Hospitals

Clinics

Others

By Distribution Channel

Hospitals

Pharmacy

Retail

E-Commerce

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)