2K Protective Coatings Market Size and Industrial Demand Acceleration Across Infrastructure and Energy Sectors

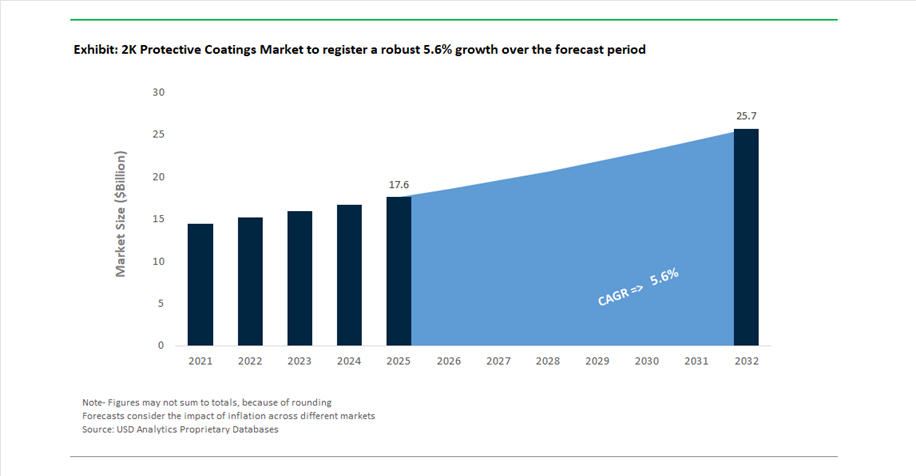

The 2K Protective Coatings Market is positioned for sustained expansion, projected to grow from USD 17.6 billion in 2025 to USD 25.8 billion by 2032, registering a CAGR of 5.6%. The rapid market growth outlook is driven by the increasing reliance on two-component (2K) coating systems across high-performance industrial environments where durability, chemical resistance, and lifecycle cost optimization are critical decision parameters.

In particular, 2K protective coatings formulated through the combination of a base resin and a curing agent are widely used to deliver superior adhesion, corrosion resistance, and mechanical strength compared to single-component systems. These properties are widely marketed by vendors across oil & gas, marine, infrastructure, power generation, and heavy manufacturing sectors. The market is also experiencing strong demand momentum from aging infrastructure rehabilitation projects, offshore exploration activities, and expansion of energy transmission networks, all of which require coatings capable of withstanding aggressive environmental and operational stressors.

Over the forecast period, leading companies are increasing R&D investments in low-VOC, environmentally compliant epoxy and polyurethane systems, aligning with stringent global regulatory frameworks. Additionally, the integration of advanced resin chemistries and zinc-rich formulations is enhancing performance in extreme conditions such as high salinity, temperature fluctuations, and chemical exposure. Growth is further reinforced by urbanization and industrialization in Asia-Pacific, where large-scale construction and industrial projects are driving consumption of high-performance protective coatings.

The competitive environment is increasingly shaped by strategic consolidation, capacity expansion, and product innovation, enabling manufacturers to strengthen their foothold in high-growth application segments while optimizing production efficiencies and global supply chains.

Strategic Consolidation, Product Innovation, and Capacity Expansion Reshaping the 2K Protective Coatings Market

The 2K protective coatings market is undergoing a significant transformation driven by large-scale mergers, strategic expansions, and next-generation product launches. A defining moment occurred in March 2026, when AkzoNobel and Axalta announced a merger, forming a global coatings leader with enhanced R&D depth in industrial and marine 2K coatings. The combined entity is targeting $600 million in annual synergies, reflecting a strong push toward technological integration and operational scale. Complementing this consolidation trend, RPM International’s January 2026 acquisition of a manufacturing plant in Malaysia highlights the strategic importance of Southeast Asia as a high-growth hub for infrastructure coatings demand.

In addition, leading manufacturers are aggressively advancing product innovation tailored to extreme industrial environments. PPG Industries’ launch of STEELGUARD® 652 addresses structural steel protection in high-visibility infrastructure such as airports and stadiums, balancing fire resistance with aesthetic durability. Similarly, Sherwin-Williams’ Heat-Flex® AEB, introduced in September 2025, specifically targets corrosion under insulation (CUI) in oil and gas assets, a critical challenge in energy infrastructure maintenance. Earlier innovations such as Pipeclad™ Frac-Shun ERC further fuel the sales volume in abrasion-resistant internal pipe coatings, particularly in hydraulic fracturing and wastewater systems.

Technological advancements are also evident in formulation chemistry and environmental compliance. In November 2025, Jotun introduced advanced zinc-rich epoxy coatings engineered for offshore platforms and power plants, offering enhanced corrosion resistance in saline environments alongside ultra-low VOC emissions. BASF’s 2025–2026 Driving the Proxy collection also supports the role of 2K systems in achieving high-performance finishes with advanced visual effects, particularly in automotive and industrial machinery applications. Additionally, PPG’s March 2026 fast-drying 2K clearcoat is addressing productivity bottlenecks in refinish operations by significantly reducing curing times.

Strategic direction is further reinforced by corporate initiatives such as Hempel’s focus on marine and energy sector penetration, and AkzoNobel’s $20 million capacity expansion in Italy to strengthen its European coatings ecosystem.

REACH Diisocyanate Restrictions Driving Ultra-Low Monomer Innovation and Cost Realignment

The implementation of the EU REACH restriction (Entry 74) has transitioned from a regulatory milestone into a structural transformation within the 2K protective coatings market. As of late 2023, mandatory certification for handling diisocyanates above 0.1% monomer concentration has imposed a new compliance framework across industrial and professional applications. This regulatory tightening has led to a measurable 15% increase in compliance and administrative costs, primarily driven by workforce training mandates, revised labeling protocols, and stricter handling procedures. Beyond cost implications, nearly 32% of global diisocyanate production capacity has been directly influenced or constrained, accelerating a decisive shift toward Ultra-Low Monomer (ULM) polyurethane systems.

From a technological standpoint, over 40% of chemical manufacturers have already adopted advanced catalytic synthesis processes aimed at minimizing free monomer content and aligning formulations below regulatory thresholds. This pivot is not merely compliance-driven but is also reshaping competitive positioning, as producers capable of delivering low-emission, high-performance coatings gain preferential access to regulated markets. Despite regulatory friction, demand for aliphatic isocyanates—critical for high-durability and UV-resistant 2K topcoats—is projected to grow at approximately 8% annually through 2030, outperforming the broader specialty chemicals sector. This reflects a dual-market dynamic where regulatory pressure coexists with rising performance expectations, particularly in automotive refinishing, aerospace coatings, and offshore infrastructure protection.

Scaling Bio-Based Hardeners: From Pilot Innovation to Industrial Adoption

The transition toward sustainable chemistry in 2K protective coatings has moved beyond experimental validation into scalable commercialization, particularly in the segment of bio-based hardeners. Derived from renewable feedstocks such as pentamethylene diisocyanate (PDI), these next-generation curing agents are increasingly replacing petroleum-based counterparts. The global bio-based hardeners market is projected to reach approximately $500 million in 2025, supported by accelerating demand from OEMs seeking to reduce Scope 3 emissions across their supply chains.

R&D investment patterns further reinforce this trajectory, with over 24% of coatings-related chemical research in 2024 focused exclusively on renewable isocyanates and sustainable hardener systems. Importantly, advancements in PDI trimer technology have enabled up to 35% reduction in carbon footprint during the coating phase, a critical metric for industries under ESG scrutiny. Performance concerns—historically a barrier to adoption—have largely been mitigated. Industrial-scale trials confirm that bio-based 2K polyurethane coatings now achieve full parity in UV stability, chemical resistance, and mechanical durability compared to conventional systems.

This convergence of sustainability and performance is unlocking high-value applications in automotive OEM coatings, marine environments, and industrial protective systems. As regulatory frameworks tighten globally and carbon accounting becomes integral to procurement decisions, bio-based 2K coatings are transitioning from niche offerings to mainstream solutions, creating a structurally expanding addressable market.

Hydrogen Infrastructure Expansion Creating Demand for Advanced 2K Protective Systems

The rapid acceleration of hydrogen economy investments is creating a specialized and technically demanding growth avenue for the 2K protective coatings market. Global hydrogen project spending is expected to reach $7.8 billion in 2026, marking a 70% increase and triggering parallel demand for high-performance protective coatings tailored to hydrogen-specific risks. Unlike conventional hydrocarbons, hydrogen introduces challenges such as embrittlement, micro-permeation, and extreme combustion temperatures, necessitating a new class of coating technologies.

Testing data indicates that unprotected carbon steel can fail in under 60 seconds when exposed to hydrogen jet fires, underscoring the critical need for 2K intumescent Passive Fire Protection (PFP) coatings. Additionally, the repurposing of existing natural gas pipeline infrastructure for hydrogen blending introduces demand for epoxy-based internal liners capable of acting as high-integrity gas barriers. These liners must mitigate leakage risks while maintaining structural integrity under cyclic pressure conditions.

Material innovation is central to capturing this opportunity. 2K composite systems, including glass-flake reinforced epoxies and advanced polymer matrices, are emerging as preferred solutions due to their low hydrogen permeability and enhanced mechanical resilience. Notably, traditional 1K coatings lack the crosslink density and barrier performance required for hydrogen applications, positioning 2K systems as indispensable in next-generation energy infrastructure. This creates a high-margin, technically specialized segment with long-term growth visibility tied to global decarbonization strategies.

Industrial IoT Integration Revolutionizing Precision, Traceability, and Coating Lifecycle Efficiency

The integration of Industrial IoT (IIoT) technologies into 2K coating processes represents a transformative opportunity centered on process optimization, quality assurance, and lifecycle management. The global IoT-based industrial monitoring market is projected to exceed $5.6 billion in 2025, with coatings and manufacturing sectors leading adoption due to their sensitivity to process variability. In 2K systems, improper mixing ratios and suboptimal curing conditions remain primary causes of coating failure, making real-time monitoring a critical value driver.

Advanced sensor systems now enable continuous tracking of key environmental and process parameters, including temperature, humidity, induction time, and A:B mixing ratios. This real-time data integration can reduce coating waste and rework by 20% to 25%, particularly in high-precision sectors such as aerospace, defense, and offshore energy. Furthermore, digital twin technology allows manufacturers to create a fully traceable “digital fingerprint” of each coating application, ensuring complete transparency in quality control and compliance documentation.

Cloud-enabled platforms are extending this capability to a global scale, allowing centralized monitoring of multiple application sites from a single dashboard. This ensures uniform coating performance across geographically dispersed operations while enabling predictive maintenance and proactive process adjustments. As asset owners increasingly prioritize lifecycle cost optimization and reliability, IoT-integrated 2K coating systems are evolving from operational enhancements into strategic differentiators, unlocking new revenue streams in smart coatings and performance-based service models.

2K Protective Coatings Market Share Analysis

2K Protective Coatings Market Share by Technology in 2025: Solvent-Borne Leadership Meets Waterborne Disruption

The 2K protective coatings market by technology in 2025 is defined by a clear yet evolving hierarchy, with solvent-borne coatings commanding 47.50% market share, followed by water-borne coatings at 34.00%, and powder-based coatings at 18.50%. Solvent-borne systems continue to dominate due to their unmatched performance in marine coatings, oil & gas infrastructure, and heavy industrial maintenance, where resistance to harsh environments and low-temperature curing is critical. However, tightening VOC regulations and environmental compliance standards are steadily reshaping demand. In contrast, water-borne 2K coatings are the fastest-growing segment, driven by rising adoption in infrastructure projects and automotive refinish applications, supported by innovations in waterborne epoxy and polyurethane technologies that deliver competitive corrosion resistance. Meanwhile, powder-based 2K coatings, particularly fusion bonded epoxy (FBE), maintain a strong niche in pipeline anti-corrosion and automotive components, benefiting from zero VOC emissions and superior mechanical durability, reinforcing their strategic importance in sustainable coating solutions.

2K Protective Coatings Market Share by End-Use Industry in 2025: Infrastructure Boom Reshaping Demand Dynamics

The 2K protective coatings market by end-use industry in 2025 highlights Infrastructure & Civil Building as the leading segment with a 26.00% share, surpassing Oil & Gas at 21.50%, followed by Industrial Manufacturing (16.00%) and Marine & Shipbuilding (13.50%). The infrastructure sector’s dominance is fueled by large-scale investments in bridge rehabilitation, commercial steel structures, and long-life corrosion protection systems, primarily utilizing epoxy zinc-rich primers and polyurethane topcoats. Despite volatility in upstream activities, the oil & gas coatings market remains resilient, supported by stable demand from midstream pipelines and downstream refinery maintenance, which heavily rely on high-solids solvent-borne 2K epoxy coatings. The marine coatings segment is undergoing a technological shift, with increasing adoption of waterborne coatings for topside applications, while underwater hulls still depend on solvent-based anti-corrosive systems. Notably, the water & wastewater treatment segment (6.00%) is emerging as the fastest-growing niche, driven by stringent EPA and DWI regulations, accelerating the transition toward solvent-free epoxies and polyurea coatings for potable water systems.

2K Protective Coatings Market Competitive Landscape Driven by Consolidation, Sustainability, and High-Performance Innovation

The competitive landscape of the 2K protective coatings industry is characterized by consolidation, sustainability-driven innovation, and advanced epoxy and polyurethane technologies. Key players are expanding global production capacity, enhancing VOC-compliant formulations, and strengthening high-performance coatings portfolios across automotive, marine, infrastructure, and industrial applications.

AkzoNobel expands powder coatings capacity while advancing low-VOC 2K innovations

AkzoNobel remains a dominant player in epoxy coatings and polyurethane coatings, supported by strategic investments and consolidation initiatives. In 2025, the company approved a $20 million expansion of powder coating capacity in Como, Italy, targeting high-durability architectural coatings demand in Europe. The proposed merger with Axalta Coating Systems, expected by 2026, focuses on building a global leader in automotive coatings and industrial 2K systems with expanded distribution networks. The company achieved a 47% reduction in Scope 1 and 2 emissions compared to its 2018 baseline, aligning with 2030 sustainability targets. Its newly launched waterborne 2K coatings for automotive refinishing deliver rapid curing performance while meeting strict VOC regulations across EU and North America. Continuous innovation in environmentally compliant coatings supports its strong presence in high-performance segments.

PPG Industries integrates digital tools and sustainable formulations in 2K coatings

PPG Industries continues to lead through advanced protective coatings technologies and digital integration across aerospace and marine coatings segments. The company reported $15.9 billion in net sales in 2025, supported by 2% organic growth and strong demand in performance coatings. Sustainably advantaged coatings contributed 43% of total revenue, reflecting increased adoption of low-VOC 2K formulations with high chemical resistance. Its digital color-matching platform tailored for industrial coatings reduces application downtime by 15–20% in maintenance and repair operations. The company also returned $1.4 billion to shareholders, including $790 million in share repurchases, indicating strong financial performance and capital allocation discipline. Its portfolio continues to evolve toward environmentally advanced and high-efficiency coating systems.

Sherwin-Williams leverages infrastructure pipeline with high-performance architectural 2K systems

Sherwin-Williams maintains strong positioning in construction coatings and infrastructure coatings through its extensive North American distribution network. The company supplies specialized 2K primers and topcoats across the US $1.4 trillion infrastructure pipeline, particularly for bridges and highways. Its vertically integrated model reduces exposure to raw material price volatility, including key inputs such as Bisphenol A (BPA) and isocyanates used in epoxy and polyurethane coatings. The HiPAC product line addresses demand for abrasion-resistant coatings in high-traffic industrial environments such as warehouses and commercial spaces. Eco-friendly High-Performance (EFHP) coatings combine low-odor characteristics with durability required for institutional and interior applications. Product development continues to align with performance-driven and environmentally compliant coating requirements.

Jotun strengthens marine coatings leadership with anti-fouling and offshore energy solutions

Jotun A/S delivers strong performance in marine coatings and energy coatings, supported by rising shipbuilding and offshore energy activity. The company reported operating revenues exceeding NOK 34 billion ($3.1 billion) in 2025. Its Hull Skating Solutions and advanced 2K anti-fouling coatings improve vessel fuel efficiency and contribute to significant CO2 emission reductions. Operations span more than 100 countries with over 11,000 employees, supported by a localized manufacturing strategy that enhances supply chain stability. Participation in the EOLMED floating wind project in France includes supplying corrosion-resistant 2K protective coatings designed for offshore wind turbine environments. The portfolio continues to address high-performance requirements in extreme marine conditions.

Hempel drives profitability and decarbonization through advanced 2K marine coatings

Hempel A/S is advancing through its “Accelerate to Win” strategy launched in 2026, focusing on operational efficiency and sustainability integration. The company reported free cash flow of €259 million in 2025, increasing from €139 million in 2024, with an adjusted EBITDA margin of 18.2%. Its Marine segment recorded 9.8% organic growth, reaching €750 million, supported by strong demand for protective coatings in maritime applications. Sustainability-focused procurement includes a 20% emissions weighting in supplier selection, promoting value chain decarbonization. The Hempaguard product line has enabled customers to reduce 35.9 million tonnes of CO2 through improved efficiency and extended asset lifespan in harsh marine environments. Innovation efforts remain centered on high-performance and environmentally advanced 2K coating technologies.

United States 2K Protective Coatings Market: Infrastructure Modernization and CUI-Resistant Innovations Driving Demand

The United States 2K protective coatings market is experiencing robust expansion, primarily fueled by large-scale infrastructure modernization initiatives and increased investments in aerospace and petrochemical sectors. Government-backed funding under the Bipartisan Infrastructure Law has significantly accelerated the deployment of heavy-duty epoxy protective coatings across bridges, structural steel frameworks, and water treatment facilities. This sustained investment pipeline is reinforcing the demand for high-performance two-component coatings designed for long-term corrosion resistance and durability.

Technological advancements and product innovation are further reshaping the market landscape. The introduction of advanced CUI (Corrosion Under Insulation) mitigation coatings, such as next-generation heat-resistant systems, is addressing critical asset integrity challenges in energy infrastructure. Additionally, the expansion of aerospace coatings manufacturing capacity and ongoing merger activities among leading players are intensifying competition. Regulatory pressure from environmental agencies is also accelerating the transition toward ultra-high-solids and water-borne 2K coatings, reducing hazardous emissions while maintaining superior protective performance.

China 2K Protective Coatings Market: Renewable Energy Expansion and Low-VOC Transformation

China dominates the global 2K protective coatings market in terms of volume, driven by aggressive industrialization, renewable energy expansion, and mega-infrastructure projects. The country’s push toward smart cities and decentralized energy grids has created significant demand for advanced protective coatings, particularly in construction and power generation sectors. Strict regulatory frameworks targeting VOC emissions have catalyzed a rapid shift toward environmentally compliant, high-solid polyurethane coatings.

The rapid growth of the electric vehicle (EV) industry is also contributing to market expansion, with increasing reliance on thermal-resistant 2K coatings for battery safety. Additionally, China’s leadership in wind energy installations has boosted the demand for specialized epoxy coatings designed for UV resistance and edge protection in turbine blades. Expanding shipbuilding capacity further supports the consumption of anti-corrosive marine coatings, while innovations in bio-based architectural coatings are enhancing sustainability and indoor air quality standards across infrastructure projects.

Germany 2K Protective Coatings Market: Automotive Excellence and Bio-Based Coating Innovations

Germany’s 2K protective coatings market is characterized by its strong focus on automotive OEM applications and sustainable material innovation. The country remains a hub for advanced coating technologies, particularly in premium automotive finishes that demand high UV stability, scratch resistance, and aesthetic performance. Continuous innovation in multi-layer coating systems is enhancing surface durability while meeting stringent environmental standards.

Regulatory compliance under the EU REACH framework is accelerating the shift toward safer chemical formulations, including the adoption of aliphatic isocyanates and bio-attributed raw materials. Strategic collaborations between chemical manufacturers and material science firms are further advancing low-emission coating technologies. In addition to automotive demand, increased investments in building renovation and retrofitting are driving the adoption of intumescent fire protection coatings, while ongoing R&D in fast-curing epoxy systems supports applications in extreme weather conditions.

India 2K Protective Coatings Market: Infrastructure Boom and Cost-Effective Coating Solutions

India represents one of the fastest-growing markets for 2K protective coatings, driven by rapid urbanization and extensive infrastructure development initiatives. Large-scale government programs focused on transportation, housing, and industrial expansion are creating substantial demand for epoxy-based protective coatings in civil construction and metro rail projects. The country’s expanding petrochemical sector is also fueling the need for specialized coatings used in pipelines, storage tanks, and water treatment systems.

Local manufacturing expansions and increased foreign investments are enhancing production capabilities, particularly for fast-curing polyaspartic coatings. Given the region’s climatic challenges, moisture-cured coatings are gaining traction due to their ability to perform effectively in high-humidity environments. Cost sensitivity remains a critical factor, encouraging the adoption of hybrid acrylic-epoxy formulations that offer a balance between performance and affordability. Government initiatives promoting domestic manufacturing are further accelerating the demand for industrial-grade floor coatings and structural protection systems.

Norway 2K Protective Coatings Market: Maritime Leadership and Decarbonization Technologies

Norway’s 2K protective coatings market is deeply rooted in its global leadership in maritime and offshore industries. The country’s strong focus on sustainability and decarbonization is driving the adoption of advanced marine coatings designed to reduce fuel consumption and emissions. High-performance epoxy and silicone-based coatings are widely used in ship hulls and cargo containers to enhance corrosion resistance and operational efficiency.

Innovation is a key market driver, with the development of frictionless, biocide-free coatings that improve vessel hydrodynamics. Additionally, increasing investments in offshore oil and gas exploration are supporting demand for ultra-durable polyurethane coatings capable of withstanding extreme environmental conditions. Regulatory mandates enforcing low-VOC and solvent-free formulations are further strengthening the shift toward environmentally sustainable coating solutions, positioning Norway as a leader in green marine coatings technology.

Denmark 2K Protective Coatings Market: Offshore Wind Energy and Sustainable Coating Technologies

Denmark is emerging as a global leader in the application of 2K protective coatings within renewable energy infrastructure, particularly offshore wind energy. The country’s ambitious climate goals and investments in energy islands are generating significant demand for UV-resistant and weather-durable polyurethane coatings used in turbine blades and structural components. These coatings play a crucial role in extending asset lifespan under harsh marine conditions.

Sustainability remains at the core of Denmark’s coatings market, with a rapid transition toward water-borne and low-emission technologies. Innovations such as graphene-enhanced epoxy coatings are improving mechanical strength and durability, while advanced intumescent coatings are being developed to provide fire protection for offshore energy installations. Strategic industry initiatives aimed at reducing emissions are further accelerating the adoption of next-generation 2K coating systems across industrial and energy sectors.

South Korea 2K Protective Coatings Market: Shipbuilding Dominance and Advanced Siloxane Technologies

South Korea stands as a global powerhouse in the 2K protective coatings market, largely due to its dominance in shipbuilding and heavy industrial manufacturing. The country’s extensive shipyard operations drive massive demand for saltwater-resistant epoxy coatings used in marine vessels and cargo containers. Continuous advancements in automated coating application technologies are improving efficiency, safety, and coating precision across large-scale projects.

The market is also benefiting from growth in semiconductor and petrochemical industries, which require highly specialized coatings for cleanrooms, storage tanks, and industrial flooring. Local manufacturers are innovating with fast-curing siloxane coatings that offer superior weatherability and reduced downtime. Regulatory measures aimed at limiting hazardous emissions are pushing the industry toward low-VOC and bio-based coating solutions, reinforcing South Korea’s position as a leader in advanced protective coatings technologies.

2K Protective Coatings Market Report Scope

2K Protective Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17.6 Billion

|

|

Market Size (2032)

|

$25.8 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Resin (Epoxy, Polyurethane, Alkyd, Acrylic, Others)), By Technology (Solvent-borne, Water-borne, Powder-based)), By Function (Corrosion Protection, Abrasion Resistance, Chemical Resistance, Fire Protection, Heat Resistance)), By End-Use Industry (Oil & Gas, Infrastructure & Civil Building, Marine & Shipbuilding, Power Generation, Industrial Manufacturing, Automotive & Transportation, Water & Wastewater Treatment)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Jotun A/S, Hempel A/S, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd, Axalta Coating Systems Ltd., RPM International Inc., Sika AG, BASF SE, Chugoku Marine Paints, Ltd, Carboline Company, Tnemec Company, Inc, Berger Paints India Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

2K Protective Coatings Market Segmentation

By Resin

- Epoxy

- Polyurethane

- Alkyd

- Acrylic

- Others

By Technology

- Solvent-borne

- Water-borne

- Powder-based

By Function

- Corrosion Protection

- Abrasion Resistance

- Chemical Resistance

- Fire Protection

- Heat Resistance

By End-Use Industry

- Oil & Gas

- Infrastructure & Civil Building

- Marine & Shipbuilding

- Power Generation

- Industrial Manufacturing

- Automotive & Transportation

- Water & Wastewater Treatment

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in 2K Protective Coatings Market

- Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Jotun A/S

- Hempel A/S

- Nippon Paint Holdings Co., Ltd

- Kansai Paint Co., Ltd

- Axalta Coating Systems Ltd

- RPM International Inc

- Sika AG

- BASF SE

- Chugoku Marine Paints, Ltd.

- Carboline Company

- Tnemec Company, Inc.

- Berger Paints India Limited

*- List not Exhaustive

Table of Contents: 2K Protective Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. 2K Protective Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to 2K Protective Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Industrial Demand Across Infrastructure and Energy Sectors

2.4. Performance Advantages of Two-Component Coating Systems

2.5. Regulatory Compliance and Low-VOC Coating Developments

3. Innovations Reshaping the 2K Protective Coatings Market

3.1. Trend: Strategic Consolidation and Capacity Expansion

3.2. Trend: REACH Diisocyanate Restrictions and Ultra-Low Monomer Innovation

3.3. Opportunity: Bio-Based Hardeners and Sustainable Coating Chemistry

3.4. Opportunity: Hydrogen Infrastructure and Advanced Protective Systems

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: 2K Protective Coatings Market

5.1. By Resin

5.1.1. Epoxy

5.1.2. Polyurethane

5.1.3. Alkyd

5.1.4. Acrylic

5.1.5. Others

5.2. By Technology

5.2.1. Solvent-borne

5.2.2. Water-borne

5.2.3. Powder-based

5.3. By Function

5.3.1. Corrosion Protection

5.3.2. Abrasion Resistance

5.3.3. Chemical Resistance

5.3.4. Fire Protection

5.3.5. Heat Resistance

5.4. By End-Use Industry

5.4.1. Oil & Gas

5.4.2. Infrastructure & Civil Building

5.4.3. Marine & Shipbuilding

5.4.4. Power Generation

5.4.5. Industrial Manufacturing

5.4.6. Automotive & Transportation

5.4.7. Water & Wastewater Treatment

6. Country Analysis and Outlook of 2K Protective Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. 2K Protective Coatings Market Size Outlook by Region (2025–2032)

7.1. North America 2K Protective Coatings Market Size Outlook to 2032

7.1.1. By Resin

7.1.2. By Technology

7.1.3. By Function

7.1.4. By End-Use Industry

7.2. Europe 2K Protective Coatings Market Size Outlook to 2032

7.2.1. By Resin

7.2.2. By Technology

7.2.3. By Function

7.2.4. By End-Use Industry

7.3. Asia Pacific 2K Protective Coatings Market Size Outlook to 2032

7.3.1. By Resin

7.3.2. By Technology

7.3.3. By Function

7.3.4. By End-Use Industry

7.4. South America 2K Protective Coatings Market Size Outlook to 2032

7.4.1. By Resin

7.4.2. By Technology

7.4.3. By Function

7.4.4. By End-Use Industry

7.5. Middle East and Africa 2K Protective Coatings Market Size Outlook to 2032

7.5.1. By Resin

7.5.2. By Technology

7.5.3. By Function

7.5.4. By End-Use Industry

8. Company Profiles: Leading Players in the 2K Protective Coatings Market

8.1. Sherwin-Williams Company

8.2. PPG Industries, Inc.

8.3. Akzo Nobel N.V.

8.4. Jotun A/S

8.5. Hempel A/S

8.6. Nippon Paint Holdings Co., Ltd

8.7. Kansai Paint Co., Ltd

8.8. Axalta Coating Systems Ltd

8.9. RPM International Inc

8.10. Sika AG

8.11. BASF SE

8.12. Chugoku Marine Paints, Ltd.

8.13. Carboline Company

8.14. Tnemec Company, Inc.

8.15. Berger Paints India Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures