Abrasion Resistant Coatings Market Size and Industrial Demand Driven by Heavy-Duty Wear Protection Applications

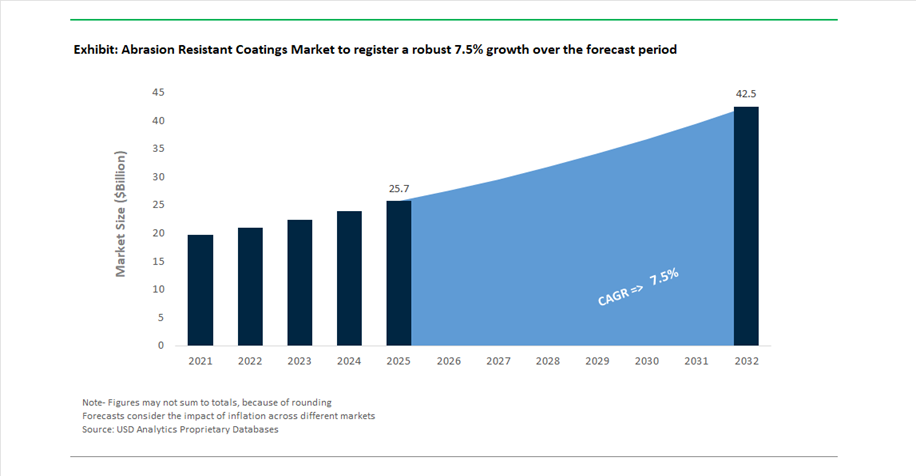

The Abrasion Resistant Coatings Market is witnessing strong momentum, valued at USD 25.7 billion in 2025 and projected to reach USD 42.6 billion by 2032, expanding at a CAGR of 7.5%. The robust market growth rate is driven by the critical role of abrasion-resistant coatings in asset lifecycle extension, maintenance cost reduction, and operational efficiency optimization across high-intensity industrial environments.

Abrasion resistant coatings are engineered to withstand mechanical wear, frictional forces, and particle erosion, making them indispensable in sectors such as mining, power generation, oil & gas, marine, and heavy manufacturing. Equipment including pipelines, conveyor systems, crushers, turbines, and industrial flooring are constantly exposed to abrasive materials and high-velocity particles, necessitating advanced coating systems that can preserve substrate integrity under extreme stress conditions. As industrial operators increasingly prioritize predictive maintenance and total cost of ownership (TCO), these coatings are transitioning from optional upgrades to mission-critical investments.

The market is further benefiting from rapid industrialization in emerging economies and ongoing investments in infrastructure modernization and energy transition projects, including offshore wind and renewable energy installations. These applications demand coatings that combine abrasion resistance with corrosion protection and chemical stability, particularly in harsh and variable environments. Technological advancements are also reshaping the landscape, with manufacturers developing hybrid epoxy systems, high-performance powder coatings, and water-based formulations that meet stringent environmental regulations while maintaining superior durability.

Additionally, the increasing complexity of coating applications is driving demand for skilled applicators and advanced surface preparation techniques, highlighting a parallel evolution in workforce training and technical service ecosystems. The competitive landscape is characterized by portfolio expansion, strategic restructuring, and targeted regional investments, positioning leading players to capitalize on high-growth industrial segments while addressing evolving performance and sustainability requirements.

Product Innovation, Strategic Realignment, and Capacity Expansion Accelerating Abrasion Resistant Coatings Adoption

The abrasion resistant coatings market is being actively reshaped by next-generation product launches, strategic mergers, and regional manufacturing expansions, reflecting a clear shift toward high-performance, application-specific solutions. A key development occurred in November 2025, when PPG launched Envirocron® Extreme Protection Edge Plus, a patent-pending powder coating designed to deliver enhanced abrasion and corrosion resistance on sharp edges of laser-cut metal parts. This innovation eliminates the need for mechanical edge preparation, significantly improving production efficiency and cost optimization in industrial manufacturing workflows.

Industry consolidation is also influencing competitive dynamics. The AkzoNobel and Axalta merger announcement represents a major strategic move to create a global coatings leader with strengthened R&D capabilities in abrasion-resistant and performance coatings. Further, AkzoNobel’s December 2025 divestment of its decorative paints business in India signals a focused pivot toward high-margin performance coatings, including abrasion-resistant industrial applications, supported by its regional research and manufacturing infrastructure.

On the product development front, manufacturers are prioritizing formulation advancements tailored to extreme operating environments. In January 2026, Jotun introduced its New Era Hybrid Epoxy Systems, engineered for higher abrasion tolerance and chemical resistance in sectors such as mining and offshore energy. Similarly, Kansai Nerolac’s Excel Total Floor Coat addresses the growing need for durable, high-traffic industrial flooring solutions, combining abrasion resistance with environmental durability. Sherwin-Williams’ expanded ARC portfolio further underscores demand for coatings capable of protecting pipelines and mining equipment from abrasive slurries and high-impact wear, reducing downtime and maintenance cycles.

Strategic capacity expansion is another defining trend. RPM International’s 2026 acquisition of a manufacturing facility in Malaysia highlights the importance of Southeast Asia as a growth engine for abrasion-resistant coatings, particularly in mining and infrastructure sectors. Meanwhile, Hempel’s “Accelerate to Win” strategy (January 2026) reinforces a targeted push into energy and infrastructure coatings, including solutions for offshore wind installations where abrasion and corrosion resistance are critical.

Complementing product and capacity strategies, industry players are addressing application complexity and workforce capability gaps. In March 2026, PPG committed $10 million toward skilled trades and applicator training, recognizing that proper application is essential to achieving optimal coating performance and longevity. Innovations such as BASF’s Phygital Magnetar further illustrate the convergence of aesthetic performance and functional durability, leveraging advanced 2K technologies to deliver both visual appeal and abrasion resistance in automotive and industrial coatings.

PFAS Restrictions Accelerating Shift Toward Fluorine-Free Abrasion Resistant Coatings

The abrasion resistant coatings industry is undergoing a structural transition as regulatory frameworks tighten around per- and polyfluoroalkyl substances (PFAS). By 2025, the European Chemicals Agency (ECHA) has advanced a universal restriction proposal, while multiple U.S. states have enacted legislation similar to Amara’s Law, targeting intentionally added PFAS in industrial coatings. This regulatory momentum is introducing strict compliance thresholds, including a 50 ppm limit for total PFAS content in several jurisdictions, effectively rendering conventional fluoropolymer coatings such as PTFE and FEP non-compliant across a wide range of non-critical applications.

This shift is forcing coatings manufacturers to rapidly reconfigure formulation strategies, triggering a reallocation of approximately 24% of total chemical R&D budgets in 2025 toward PFAS-free alternatives. Emerging material systems such as thermoplastic polyurethanes (TPU), parylene-based dry films, and Universal Lubricious Materials (ULM) are gaining traction as viable substitutes, particularly in applications requiring low friction and moderate wear resistance. However, performance parity remains a critical challenge. Laboratory and field testing indicate that silicone-modified polyethers—one of the leading PFAS-free candidates—currently fall short by 15–20% in chemical resistance compared to legacy fluoropolymer systems.

To compensate for this performance gap, the market is witnessing increased adoption of hybrid coating architectures, particularly sol-gel matrices and SiO₂-based topcoats, which enhance surface hardness and chemical stability. This hybridization trend is becoming a key innovation vector, enabling manufacturers to balance regulatory compliance with performance requirements. As global regulatory pressure intensifies, PFAS-free abrasion resistant coatings are expected to transition from niche alternatives to industry standards, creating significant opportunities for material innovation and premium product positioning.

Laser Cladding Replacing Hard Chrome Plating in Heavy-Duty Wear Protection

The industrial shift away from Hard Chrome Plating (HCP) is accelerating, driven by both environmental concerns surrounding hexavalent chromium (Cr6+) and the inefficiencies associated with traditional electroplating processes. Laser Cladding, also known as Laser Metal Deposition (LMD), is emerging as a high-performance alternative for abrasion resistant surface engineering, particularly in sectors such as mining, oil & gas, power generation, and heavy machinery.

Unlike chrome plating, which relies on a mechanical bond, laser cladding forms a metallurgical bond with the substrate, significantly enhancing adhesion strength and durability. This results in up to 40% reduction in delamination risk under high-impact and abrasive operating conditions, a critical factor for components exposed to extreme mechanical stress. Additionally, the process offers superior operational efficiency, particularly in repair and refurbishment applications. Laser cladding can restore worn components to original dimensions using only 10% of the material waste associated with conventional thermal spray or re-plating methods, making it both cost-effective and resource-efficient.

Technological advancements in high-power fiber lasers have further improved process control, enabling dilution rates below 5%. This ensures that the hardness and abrasion resistance of cladding materials—such as tungsten carbide and nickel-based alloys—are preserved without compromising the integrity of the base substrate. As industries increasingly prioritize sustainability, lifecycle extension, and operational efficiency, laser cladding is rapidly becoming the preferred solution for high-performance abrasion resistant coatings, displacing traditional chrome plating across multiple industrial verticals.

Offshore Wind Blade Protection Unlocking High-Value LEP Coatings Demand

The expansion of offshore wind energy infrastructure is creating a specialized demand segment for abrasion resistant coatings, particularly in the form of Leading Edge Protection (LEP) systems. As wind farms are deployed in increasingly harsh marine environments, Leading Edge Erosion (LEE) has emerged as a critical operational challenge. High-velocity rain droplets striking turbine blades at speeds approaching 90 m/s act as continuous abrasive forces, rapidly degrading conventional coating systems and reducing aerodynamic efficiency.

This degradation has direct financial implications. Leading-edge erosion can result in an annual energy production (AEP) loss of 2% to 5%, translating to approximately $30,000 to $50,000 in lost revenue per year for a single 10MW offshore turbine. Consequently, asset operators are prioritizing advanced abrasion resistant coatings that can extend maintenance intervals and minimize downtime. Rotor blades now account for around 35.5% of total wind turbine maintenance (MRO) expenditure, highlighting the scale of this opportunity.

Recent innovations in UV-curable 2K polyurethane-based LEP coatings are significantly improving operational efficiency. These systems have reduced repair times from seven days to as little as two days, enabling faster turnaround and lower downtime costs. Furthermore, next-generation LEP coatings are being engineered to withstand over 30 hours in Rain Erosion Testing (RET) at wind speeds of 120 m/s—an industry benchmark that was previously unattainable. As offshore wind capacity continues to expand globally, high-performance LEP coatings represent a rapidly growing, high-margin segment within the abrasion resistant coatings market.

Space Exploration Driving Demand for Ultra-Durable Dust-Resistant Coating Systems

The resurgence of lunar and Martian exploration programs, including NASA’s Artemis missions and a wave of commercial lunar landers scheduled through 2026 and beyond, is creating a niche but technologically demanding opportunity for abrasion resistant coatings. The “lunar dust problem” has emerged as a critical engineering constraint, driven by the highly abrasive nature of lunar regolith. Unlike terrestrial dust, lunar particles are sharp, jagged, and electrostatically charged, leading to severe material degradation.

NASA studies indicate that unprotected aluminum surfaces exposed to lunar simulants can experience surface roughness increases exceeding 200%, along with significant material loss during mechanical articulation. This has intensified demand for specialized ceramic coatings capable of withstanding extreme abrasion and environmental stress. Air Plasma-Sprayed (APS) alumina and 8% Yttria-Stabilized Zirconia (8YSZ) have emerged as leading material candidates, with alumina demonstrating superior performance in three-body abrasion scenarios involving lunar dust simulants.

However, performance in extraterrestrial environments is not solely dependent on surface hardness. Thermal cycling on the lunar surface—ranging over 300°C between day and night—introduces significant mechanical stress, necessitating the use of advanced bond coat systems. These metallic interlayers are critical for preventing spallation and ensuring long-term adhesion of ceramic coatings, enabling operational lifespans exceeding 10 years in mission-critical applications.

As space exploration transitions from government-led missions to commercial ecosystems, the demand for high-performance abrasion resistant coatings is expected to expand, creating a specialized but high-value market segment driven by extreme performance requirements and long lifecycle expectations.

Abrasion Resistant Coatings Market Competitive Landscape Focused on High-Durability Technologies and Industrial Expansion

The abrasion resistant coatings market is shaped by high-performance epoxy systems, ceramic coatings, and polyaspartic technologies. Leading companies are advancing durability, impact resistance, and sustainability while expanding manufacturing footprints and targeting marine, infrastructure, aerospace, and energy applications.

AkzoNobel accelerates circular coatings strategy with high-impact IPN technology

AkzoNobel continues to shape the abrasion resistant coatings market through advanced circularity and high-durability epoxy coatings. Its Performance Coatings segment remains a core revenue driver, with powder coatings and abrasion resistant technologies contributing significantly to growth. During 2025, the company completed multiple mid-sized acquisitions in the APAC region to strengthen local manufacturing for the International® brand, targeting marine coatings and mining coatings applications. In early 2026, AkzoNobel introduced interpenetrating polymer network (IPN) coatings offering 30% higher impact resistance than conventional 2K epoxy coatings in abrasive slurry environments. The company also reduced non-recovered waste by 27% compared to its 2017 baseline, reinforcing its green coatings strategy. Innovation efforts continue to focus on extending coating lifecycle and improving performance in high-wear industrial environments.

PPG Industries expands high-solids abrasion coatings and aerospace applications

PPG Industries maintains leadership in abrasion resistant coatings through technology-driven solutions across aerospace coatings and industrial infrastructure coatings. The company reported $15.9 billion in net sales in 2025, supported by 2% organic growth led by the Protective and Marine Coatings segment. Its technology-advantaged portfolio includes the PPG AMERLOCK® series, recognized for high-solids abrasion resistance and long-term corrosion protection. In January 2026, PPG announced $50 million in restructuring savings focused on consolidating European manufacturing to enhance delivery efficiency of high-wear coatings. The company also achieved record fourth-quarter aerospace coatings sales in 2025, driven by lightweight abrasion resistant coatings that improve fuel efficiency and reduce drag. Product development continues to align with high-performance industrial coatings and sustainability requirements.

Sherwin-Williams strengthens infrastructure coatings with multi-threat protection systems

Sherwin-Williams dominates the abrasion resistant coatings market in infrastructure and industrial flooring through its extensive North American distribution network. The company supplies specialized 2K abrasion resistant primers for the US $1.4 trillion infrastructure pipeline, particularly for bridges, highways, and heavy-duty assets. In 2025, it expanded its FIRETEX® and Magnalux™ product lines to include multi-threat coatings that provide combined fire resistance, chemical resistance, and abrasion resistance for offshore oil and gas applications. R&D investment increased by 4.5%, focusing on polyaspartic coatings that enable faster curing and reduced downtime in high-traffic environments. Its vertically integrated resin supply chain protected margins from 10–15% raw material cost fluctuations during 2025. The portfolio continues to address durability and rapid return-to-service requirements in industrial environments.

Jotun advances EV battery and marine abrasion resistant coatings with AI-driven support

Jotun A/S strengthens its position in abrasion resistant coatings through specialized solutions for energy, marine, and EV battery applications. The company reported revenues exceeding NOK 34 billion ($3.1 billion) in 2025, supported by strong demand from offshore wind and shipbuilding sectors. In June 2025, Jotun launched powder coatings for EV batteries, providing electrical insulation and abrasion resistance against mechanical stress and road debris. Its Hull Skating Solutions and SeaQuantum coatings remain industry benchmarks for friction reduction, supporting fuel efficiency and emission reduction in marine fleets. The company is also deploying AI-driven digital tools under its customer-centric initiative to predict coating failure points and optimize maintenance cycles. Product innovation continues to focus on high-performance coatings for extreme operational environments.

Hempel expands global footprint with silicone-based abrasion resistant marine coatings

Hempel A/S continues to advance in abrasion resistant coatings through profitability growth, geographic expansion, and product innovation. The company more than doubled net profit to €168 million in 2025, with total revenues reaching €2.165 billion. It introduced Hempaguard NB, a silicone-based hull coating designed for marine newbuilds, offering high resistance to mechanical wear during docking and operation. Expansion in APAC includes a new technical center in Pune, India, and full-capacity production at its Zhangjiagang facility in China to support infrastructure coatings demand. The partnership with CVC Funds has strengthened capital availability for mergers and acquisitions expected to accelerate through 2026. Product development continues to focus on extending coating durability and improving lifecycle performance in harsh marine environments.

Saint-Gobain scales ceramic and thermal spray coatings for high-wear industrial applications

Saint-Gobain differentiates its position in the abrasion resistant coatings market through ceramic coatings and thermal spray technologies. The company reported €46.5 billion in total sales in 2025, with its High-Performance Solutions segment contributing significantly to wear-resistant materials demand. It achieved a 35% reduction in Scope 1 and 2 CO2 emissions compared to 2017, aligning its coatings portfolio with green building and sustainability standards. The 2026 “Lead & Grow” strategy focuses on expanding high-value coating solutions for non-residential construction and infrastructure sectors. Its core expertise includes ceramic overlays and thermal spray coatings that deliver exceptional heat resistance and abrasion protection in heavy processing, mining, and power generation industries. The portfolio continues to address extreme wear conditions and high-temperature industrial environments.

Abrasion Resistant Coatings Market Share by Technology in 2025: Solvent-Borne Systems Dominate High-Performance Applications

Solvent-Borne Coatings Lead with Superior Abrasion Resistance and Field Applicability

The abrasion resistant coatings market by technology in 2025 is strongly led by solvent-borne coatings, capturing 51.00% market share, driven by their unmatched performance in high-wear industrial environments. These coatings, particularly solvent-borne epoxies and polyurethanes, offer superior film integrity, cross-link density, and filler loading capacity, enabling the integration of ceramic beads, alumina, and silicon carbide without compromising flow or adhesion. This makes them indispensable in demanding sectors such as mining equipment coatings, oilfield drill pipe protection, and heavy-duty industrial maintenance. A key competitive advantage lies in their field-application flexibility, allowing on-site repairs using brush or spray systems—critical for large-scale assets like haul trucks and pipelines where oven curing is impractical. Unlike powder coatings, solvent-borne systems excel in sub-optimal surface preparation conditions and provide excellent wet-edge retention, reinforcing their dominance in both new installations and maintenance-driven coating demand across global industrial markets.

Abrasion Resistant Coatings Market Share by End-Use Industry in 2025: Oil & Gas Sector Drives Premium Demand

Oil & Gas Industry Leads with High-Value, Performance-Critical Coating Applications

The abrasion resistant coatings market by end-use industry in 2025 is spearheaded by the oil & gas sector, holding a 27.00% market share, underpinned by the critical need to prevent costly equipment failure in extreme operating environments. Demand is concentrated in midstream pipeline infrastructure and downstream refining operations, where coatings must withstand high-pressure abrasion, cavitation erosion, and continuous mechanical stress. Key applications include drill pipe hardbanding replacement using tungsten carbide-filled 2K epoxy coatings, frac pump fluid ends exposed to sand slurry, and internal pipeline flow coatings designed to enhance flow efficiency and resist pigging wear. Notably, while other sectors like construction and infrastructure consume higher coating volumes, the price per liter in oil & gas applications is 4x to 7x higher, making it the leading segment by market revenue and value share. This positions oil & gas as a cornerstone for premium, high-performance abrasion resistant coating technologies in 2025.

China Abrasion Resistant Coatings Market: Mega-Infrastructure Investments and EV Export Powerhouse Driving Advanced Coatings Demand

China dominates the global abrasion resistant coatings market, propelled by massive infrastructure investments and its leadership in next-generation export industries. Under the “14th Five-Year Plan,” extensive funding directed toward high-speed rail networks and smart grid infrastructure has significantly increased the adoption of ceramic-based abrasion resistant coatings designed for high-friction and high-velocity applications. These coatings play a critical role in enhancing the durability and operational efficiency of key infrastructure assets.

The rapid expansion of China’s “New Three” industries—electric vehicles (EVs), lithium batteries, and solar energy—has further accelerated demand for high-performance protective coatings. Leading manufacturers such as BYD and CATL are deploying advanced 2K polyurethane abrasion coatings to safeguard battery enclosures from mechanical stress and environmental damage. Additionally, stringent regulatory updates to GB 30981-2020 are driving a shift toward waterborne and high-solid coatings, while innovations such as self-healing polyurea coatings and graphene-enhanced marine systems are redefining performance benchmarks. Large-scale projects like the South-to-North Water Diversion initiative further amplify demand for heavy-duty epoxy coatings to combat silt erosion in critical infrastructure.

United States Abrasion Resistant Coatings Market: Aerospace Precision and Re-Shoring Accelerating High-Performance Coating Adoption

The United States abrasion resistant coatings market is undergoing significant transformation, driven by re-shoring of manufacturing and strong demand from infrastructure and defense sectors. The Bipartisan Infrastructure Law has catalyzed increased usage of thermal-spray abrasion coatings in bridge rehabilitation and municipal water systems, reinforcing the need for long-lasting protective solutions in public infrastructure.

Aerospace and defense applications remain key growth drivers, with advanced nanostructured carbide coatings being deployed to enhance turbine blade durability in military aircraft programs. Strategic investments in R&D and manufacturing, particularly in polyaspartic and fluoropolymer coatings, are strengthening the country’s technological edge. Furthermore, the emergence of smart coatings with embedded sensors is enabling real-time wear monitoring in pipelines, while stricter environmental and occupational safety regulations are accelerating the transition toward safer alternatives such as HVOF-applied tungsten carbide coatings. In parallel, shale gas operations continue to drive demand for cermet coatings in high-pressure equipment, reinforcing the market’s industrial backbone.

India Abrasion Resistant Coatings Market: Infrastructure Boom and Policy-Driven Industrial Expansion

India’s abrasion resistant coatings market is expanding rapidly, supported by large-scale infrastructure development and strong government initiatives. The National Infrastructure Pipeline and major highway development programs are generating substantial demand for wear-resistant coatings in bridges, roadways, and industrial corridors. These coatings are essential for improving the lifespan and durability of infrastructure exposed to heavy mechanical stress.

Government-backed initiatives such as the Production Linked Incentive (PLI) scheme are encouraging domestic manufacturing of specialized abrasion-resistant materials, strengthening the local supply chain. Technological advancements, particularly in moisture-cured urethane coatings, are enabling effective application in India’s high-humidity environments. Additionally, increasing investments and strategic acquisitions are consolidating the market, while the expansion of metro rail networks is driving demand for high-friction, abrasion-resistant flooring systems in urban transit infrastructure.

Germany Abrasion Resistant Coatings Market: Industry 4.0 Integration and Sustainable Material Innovation

Germany’s abrasion resistant coatings market is defined by its leadership in advanced manufacturing and sustainable chemistry. The integration of Industry 4.0 technologies is enabling precise application techniques and enhanced coating performance, particularly in high-value sectors such as automotive, wind energy, and precision engineering.

German manufacturers are pioneering bio-attributed resins that significantly reduce carbon emissions without compromising hardness and durability. Strict compliance with EU REACH regulations is also driving the development of cobalt-free and isocyanate-free coating systems. Innovations such as laser cladding are enabling ultra-thin, highly durable coatings for automotive and industrial components, while the country’s dominance in diamond-like carbon (DLC) coatings continues to support precision tooling and OEM applications. Additionally, demand from semiconductor manufacturing hubs and wind energy installations is further strengthening the market outlook.

Brazil Abrasion Resistant Coatings Market: Mining Revival and Offshore Energy Investments Fueling Demand

Brazil’s abrasion resistant coatings market is witnessing strong growth, driven by a resurgence in mining activities and increased offshore energy exploration. The country’s rich natural resources and expanding infrastructure investments are creating substantial demand for heavy-duty protective coatings capable of withstanding extreme abrasion and corrosion.

Major mining companies are adopting ceramic-epoxy liners to protect conveyor systems from the intense wear caused by iron ore transportation. Simultaneously, investments in manufacturing capacity are enhancing the availability of advanced marine and protective coatings. Technological innovations such as cold spray repair techniques are improving maintenance efficiency in offshore platforms, while large-scale infrastructure programs are boosting demand for coatings in ports, railways, and logistics networks. Compliance with international marine standards is also reinforcing the need for high-performance abrasion-resistant coatings in ballast tanks and coastal operations.

Japan Abrasion Resistant Coatings Market: Advanced Materials and Hydrogen Economy Driving Next-Gen Coatings

Japan’s abrasion resistant coatings market is driven by cutting-edge material science and strong government support for sustainable technologies. Innovations in nano-silica coatings are delivering exceptional hardness and flexibility, making them ideal for high-performance applications in aerospace and advanced manufacturing.

The country’s strategic focus on hydrogen infrastructure is opening new avenues for abrasion-resistant coatings capable of operating under extreme cryogenic conditions. Additionally, the development of photocatalytic coatings is enhancing both durability and self-cleaning properties for architectural applications. High-speed rail projects such as the Maglev Shinkansen are further driving demand for coatings that can withstand extreme aerodynamic abrasion. Investments in semiconductor manufacturing materials and stricter regulations on solvent usage are also accelerating the shift toward UV-curable and environmentally friendly coating technologies.

South Korea Abrasion Resistant Coatings Market: Shipbuilding Leadership and High-Precision Coating Technologies

South Korea remains a global leader in the abrasion resistant coatings market, primarily due to its dominance in shipbuilding and heavy industrial manufacturing. The country’s shipyards are major consumers of high-solid epoxy coatings used to protect vessel hulls from saltwater abrasion and mechanical wear, ensuring long-term operational efficiency.

Technological advancements in robotic spray systems are enabling highly precise and efficient application of thick protective coatings, significantly improving productivity and safety. The growing focus on LNG carrier construction is also driving demand for specialized pipe coatings and tank linings. Local manufacturers are introducing fast-curing siloxane coatings that offer superior weatherability and reduced downtime, while regulatory frameworks are promoting the adoption of low-emission, bio-based coating systems. Additionally, investments in smart manufacturing and nanotechnology-infused coatings are expanding applications in electronics and semiconductor industries, further strengthening South Korea’s market position.

Abrasion Resistant Coatings Market Report Scope

Abrasion Resistant Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.7 Billion

|

|

Market Size (2032)

|

$42.6 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Material (Polymer-Based Coatings, Ceramic-Based Coatings, Metallic & Cermet Coatings)), By Technology (Solvent-borne, Water-borne, Powder Coatings)), By Application Method (Thermal Spray, Physical Vapor Deposition (PVD), Chemical Vapor Deposition (CVD))), By Substrate (Metal, Concrete & Masonry, Plastics & Composites, Glass, Other Substrates)), By End-Use Industry (Oil & Gas, Power Generation, Mining & Metallurgy, Transportation & Automotive, Marine, Construction & Infrastructure, Industrial Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Akzo Nobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Saint-Gobain Performance Plastics, Jotun A/S, Hempel A/S, Arkema Group, Bodycote plc, Praxair Surface Technologies, Inc., 3M Company, Sika AG, Hardide Coatings, Axalta Coating Systems Ltd., Kansai Paint Co., Ltd., ASB Industries, Inc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Abrasion Resistant Coatings Market Segmentation

By Material

- Polymer-Based Coatings

- Ceramic-Based Coatings

- Metallic & Cermet Coatings

By Technology

- Solvent-borne

- Water-borne

- Powder Coatings

By Application Method

- Thermal Spray

- Physical Vapor Deposition (PVD)

- Chemical Vapor Deposition (CVD)

By Substrate

- Metal

- Concrete & Masonry

- Plastics & Composites

- Glass

- Other Substrates

By End-Use Industry

- Oil & Gas

- Power Generation

- Mining & Metallurgy

- Transportation & Automotive

- Marine

- Construction & Infrastructure

- Industrial Manufacturing

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Abrasion Resistant Coatings Market

- Akzo Nobel N.V.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Saint-Gobain Performance Plastics

- Jotun A/S

- Hempel A/S

- Arkema Group

- Bodycote plc

- Praxair Surface Technologies, Inc

- 3M Company

- Sika AG

- Hardide Coatings

- Axalta Coating Systems Ltd.

- Kansai Paint Co., Ltd.

- ASB Industries, Inc

*- List not Exhaustive

Table of Contents: Abrasion Resistant Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Abrasion Resistant Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Abrasion Resistant Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Industrial Demand Across Heavy-Duty Wear Protection Applications

2.4. Role in Asset Lifecycle Extension and Maintenance Optimization

2.5. Regulatory Compliance and Sustainable Coating Developments

3. Innovations Reshaping the Abrasion Resistant Coatings Market

3.1. Trend: Product Innovation, Strategic Realignment, and Capacity Expansion

3.2. Trend: PFAS Restrictions Driving Fluorine-Free Coating Development

3.3. Opportunity: Laser Cladding Replacing Hard Chrome Plating

3.4. Opportunity: Offshore Wind LEP Coatings and Space-Grade Coating Systems

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Abrasion Resistant Coatings Market

5.1. By Material

5.1.1. Polymer-Based Coatings

5.1.2. Ceramic-Based Coatings

5.1.3. Metallic & Cermet Coatings

5.2. By Technology

5.2.1. Solvent-borne

5.2.2. Water-borne

5.2.3. Powder Coatings

5.3. By Application Method

5.3.1. Thermal Spray

5.3.2. Physical Vapor Deposition (PVD)

5.3.3. Chemical Vapor Deposition (CVD)

5.4. By Substrate

5.4.1. Metal

5.4.2. Concrete & Masonry

5.4.3. Plastics & Composites

5.4.4. Glass

5.4.5. Other Substrates

5.5. By End-Use Industry

5.5.1. Oil & Gas

5.5.2. Power Generation

5.5.3. Mining & Metallurgy

5.5.4. Transportation & Automotive

5.5.5. Marine

5.5.6. Construction & Infrastructure

5.5.7. Industrial Manufacturing

6. Country Analysis and Outlook of Abrasion Resistant Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Abrasion Resistant Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Abrasion Resistant Coatings Market Size Outlook to 2032

7.1.1. By Material

7.1.2. By Technology

7.1.3. By Application Method

7.1.4. By Substrate

7.1.5. By End-Use Industry

7.2. Europe Abrasion Resistant Coatings Market Size Outlook to 2032

7.2.1. By Material

7.2.2. By Technology

7.2.3. By Application Method

7.2.4. By Substrate

7.2.5. By End-Use Industry

7.3. Asia Pacific Abrasion Resistant Coatings Market Size Outlook to 2032

7.3.1. By Material

7.3.2. By Technology

7.3.3. By Application Method

7.3.4. By Substrate

7.3.5. By End-Use Industry

7.4. South America Abrasion Resistant Coatings Market Size Outlook to 2032

7.4.1. By Material

7.4.2. By Technology

7.4.3. By Application Method

7.4.4. By Substrate

7.4.5. By End-Use Industry

7.5. Middle East and Africa Abrasion Resistant Coatings Market Size Outlook to 2032

7.5.1. By Material

7.5.2. By Technology

7.5.3. By Application Method

7.5.4. By Substrate

7.5.5. By End-Use Industry

8. Company Profiles: Leading Players in the Abrasion Resistant Coatings Market

8.1. Akzo Nobel N.V.

8.2. PPG Industries, Inc.

8.3. The Sherwin-Williams Company

8.4. Saint-Gobain Performance Plastics

8.5. Jotun A/S

8.6. Hempel A/S

8.7. Arkema Group

8.8. Bodycote plc

8.9. Praxair Surface Technologies, Inc

8.10. 3M Company

8.11. Sika AG

8.12. Hardide Coatings

8.13. Axalta Coating Systems Ltd.

8.14. Kansai Paint Co., Ltd.

8.15. ASB Industries, Inc

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures