Market Overview: High-Temperature Insulation, Fire Safety Compliance, and Industrial Reliability Anchor the Active Calcium Silicate Market

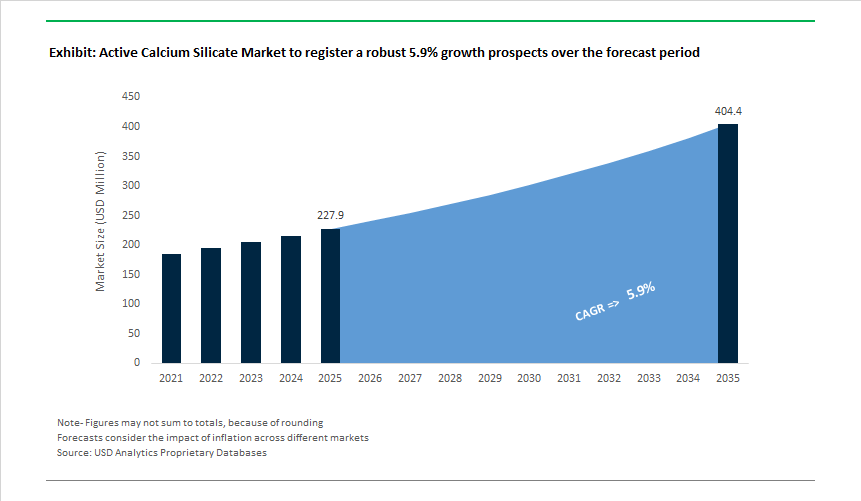

The Active Calcium Silicate Market, valued at USD 227.9 million in 2025 and forecast to reach USD 404.3 million by 2035 at a 5.9% CAGR, is gaining structural relevance as industries prioritize thermal efficiency, fire resistance, and long-life insulation performance. Demand is concentrated in industrial furnaces, refractory back-up linings, power generation assets, petrochemical processing units, and fire-rated building systems, where materials must perform reliably under sustained high temperatures and mechanical loads.

From a buyer and specifier perspective, active calcium silicate is increasingly selected because it solves multiple operational constraints simultaneously: continuous service temperatures up to ~1,100°C, low thermal conductivity that reduces heat loss and operating costs, high compressive strength for load-bearing insulation, and dimensional stability that limits cracking and shrinkage during thermal cycling. These attributes directly translate into lower energy consumption, longer maintenance intervals, and improved asset uptime, making calcium silicate a preferred insulation and structural insulation choice in energy-intensive environments.

Regulatory and sustainability dynamics further reinforce adoption. Tightening fire safety codes, non-combustibility requirements, and industrial decarbonization mandates are pushing end users away from combustible or short-life insulation materials. Active calcium silicate’s asbestos-free composition, moisture resistance, and low smoke generation align well with modern safety standards in both industrial facilities and commercial buildings. In parallel, the push for energy-efficient retrofits, government incentives for safer construction materials, and the integration of digital condition-monitoring in industrial insulation systems are strengthening long-term demand visibility.

Market Analysis: Capacity Expansions, Sustainability Policies, and High-Performance Product Launches

Global developments highlight a decisive shift toward higher-performance, environmentally compliant, and digitally enhanced calcium silicate insulation solutions. In December 2025, Etex Group (Promat) supplied its calcium silicate panels to major hospital and airport projects across Latin America, emphasizing improved fire resistance, durability, and building code compliance-demonstrating growing adoption in mission-critical infrastructure. In November 2025, Japanese leaders NICHIAS Corporation and A&A Material Corporation launched fiber-reinforced CaSi boards tailored for power generation and petrochemical facilities, reinforcing the sector's move toward materials engineered for extreme operating conditions and extended service life.

Momentum continued in October 2025, when Skamol Group announced new investments in advanced production automation to minimize manufacturing variability and reduce waste-reflecting an industry-wide push for quality consistency in high-density CaSi boards. In September 2025, a major Chinese producer increased CaSi capacity by 40,000 cubic meters, responding to APAC’s accelerating construction and industrial furnace demand. This was followed in August 2025 by METI’s approval of new subsidies and standards promoting low-emission and fire-resistant insulation, positioning Japan as a regulatory driver for eco-friendly CaSi adoption.

Consolidation trends continued, with a notable June 2025 merger between two Japanese insulation firms, combining their sustainable materials research capabilities. Additional product innovations appeared in April 2025, as global manufacturers unveiled lightweight, eco-friendly CaSi pipe Sections for industrial and chemical sectors-addressing installation efficiency and decarbonization goals. Strategic expansion also shaped the year: in March 2025, a Japanese CaSi manufacturer acquired a chemical materials producer to strengthen R&D and extend its footprint in industrial thermal management markets.

Active Calcium Silicate Market: Trends and Opportunities

Ultra-High-Temperature Calcium Silicate Insulation Enables Hydrogen and Low-Carbon Steelmaking

The acceleration of green hydrogen, hydrogen-ready furnaces, and low-carbon steelmaking is pushing insulation materials into temperature regimes where conventional mineral wool and legacy calcium silicate grades fail. Active calcium silicate is now being engineered as a primary or secondary thermal barrier in hydrogen electrolyzers, reheating furnaces, and DRI-EAF steel plants, where chemical inertness, dimensional stability, and resistance to hydrogen-rich atmospheres are critical.

By 2025, refractory engineering disclosures confirmed that microporous active calcium silicate grades can operate continuously at ~1100 °C with ≤2% linear shrinkage after 16 hours, a step-change from legacy ~650 °C products. This performance leap allows furnace designers to reduce lining thickness, reclaim internal volume, and improve thermal efficiency in glass, iron, and hydrogen-fired systems. The demand signal is being reinforced by large-scale hydrogen investments—final investment decisions on 100 MW+ electrolyzer projects, including industrial hubs linked to players such as Shell, are increasing requirements for insulation that minimizes heat loss in high-temperature ducts and exhaust systems.

Decarbonization policies are tightening the case further. As steelmakers migrate toward DRI and EAF routes to comply with EU carbon rules, active calcium silicate boards are increasingly specified as backup linings in annealing and soaking furnaces. With thermal conductivity as low as ~0.102 W/m·K at 200 °C, these boards directly reduce energy intensity—an essential lever for producers exposed to mechanisms such as Carbon Border Adjustment Mechanism.

Functional Calcium Silicate Fillers Replace Carbon-Intensive Reinforcements

Beyond boards and pipe sections, active calcium silicate is gaining momentum as a functional additive in construction materials, polymers, and elastomers. Acicular calcium hydrosilicates—such as xonotlite and tobermorite—are being adopted as mineral reinforcements that improve mechanical performance while lowering embodied carbon relative to carbon black and synthetic fibers.

Peer-reviewed research in 2025 confirmed that adding ~4% by mass of acicular calcium silicate can increase compressive and flexural strength by more than 50% in fine-grained concrete and selected polymer matrices. The mechanism is structural: nanoscale needle-like crystals create bridge-linking networks that arrest crack propagation and distribute stress more evenly. This effect is attracting attention in functionally graded materials (FGMs), where weight-to-stiffness optimization is a priority for both automotive plastics and infrastructure components.

Sustainability advantages are compounding adoption. Surface-modified calcium silicate fillers are increasingly used to replace a portion of virgin polymer resin without compromising toughness, lowering both material cost and carbon footprint. Hydrothermal synthesis advances between 2023 and 2025 have also improved fiber–matrix compatibility in recycled plastics such as PET and PVC. The result is a new class of polymer concrete that converts plastic waste into durable, water-resistant construction materials—aligning circular-economy goals with performance requirements.

Active Calcium Silicate Becomes Central to EV Battery Fire Protection

Escalating safety standards for electric vehicles are opening one of the most compelling growth avenues for active calcium silicate: thermal runaway propagation (TRP) mitigation. As battery energy density rises, OEMs are under regulatory pressure to delay or prevent fire spread between cells and modules.

Scientific studies published in 2025 demonstrated that calcium silicate-based thermal barriers inserted between cells can effectively block conductive and radiative heat transfer during a runaway event. Active calcium silicate is particularly valued for its A-grade non-combustibility, high melting point, and ability to withstand flame jetting—the high-velocity gas ejection that accompanies cell failure.

Regulatory frameworks are tightening globally. UNECE-aligned standards are extending required occupant escape times well beyond the historical five-minute benchmark. To meet emerging targets, OEMs are specifying calcium silicate barriers capable of delaying fire spread for up to 240 minutes, a performance envelope that polymers and foams cannot reach. The shift toward cell-to-pack (CTP) architectures further strengthens demand: with module housings removed, materials must combine fire resistance with structural integrity. Calcium silicate meets this need with compressive strength ≥1.0 MPa, enabling it to act as a load-bearing thermal firewall without excessive mass penalties.

CCUS Infrastructure Drives Long-Run Demand for Calcium Silicate Insulation

The global expansion of carbon capture, utilization, and storage (CCUS) is creating sustained demand for high-performance pipe insulation, positioning active calcium silicate as a preferred material for both hot and cold CO₂ transport networks. CCUS systems rely on extensive insulated piping to move captured CO₂ between emitters, hubs, and storage sites while preventing heat loss, condensation, and corrosion.

Policy momentum is strong. Strategic reviews from energy agencies and institutions such as NITI Aayog emphasize that CCUS economics depend on infrastructure efficiency, elevating the value of insulation materials that combine moisture resistance, corrosion control, and long-term dimensional stability. Calcium silicate has emerged as the industry standard for these requirements.

Pipeline scale is increasing under new legal and cooperative frameworks, including Japan’s CCS legislation and multilateral initiatives under the Clean Energy Ministerial. Demonstration and commercial projects—such as offshore and hub-and-spoke CCS systems—specify calcium silicate for its ability to maintain low thermal conductivity over long distances, ensuring CO₂ remains within controlled temperature and pressure envelopes.

A differentiated opportunity is also emerging in carbonation-curing technologies. Non-hydraulic dicalcium silicate can chemically absorb CO₂ during curing, turning insulation and precast construction products into permanent carbon sinks. This dual function—insulation plus carbon sequestration—directly aligns active calcium silicate with net-zero construction strategies, expanding its relevance well beyond traditional thermal applications.

Market Share Analysis: Active Calcium Silicate Market

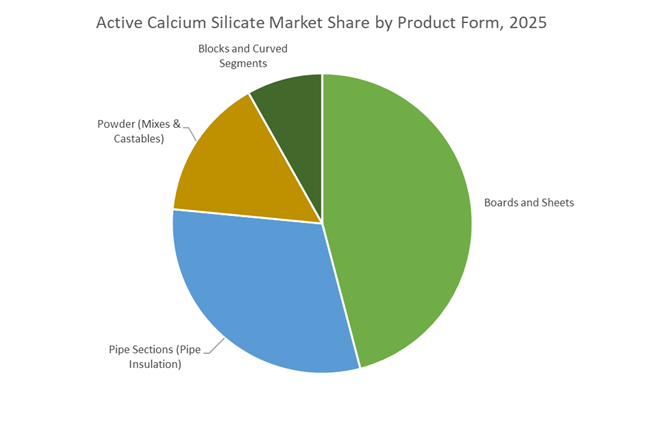

Market Share by Product Form: Calcium Silicate Boards and Sheets Set the Standard for Passive Fire Protection

Boards and sheets account for approximately 45% of the global Active Calcium Silicate Market, reflecting their role as the most versatile and performance-dense product format across fire protection and high-temperature insulation applications. This segment dominates because calcium silicate boards integrate fire resistance, thermal insulation, moisture stability, and structural strength into a single, easy-to-install system, eliminating the need for multi-layer assemblies. High-density boards deliver multi-hour fire ratings at relatively low thickness, enabling compliance with stringent building codes for high-rise steel structures, transport tunnels, and industrial facilities while minimizing added weight. Market share is further reinforced by the unique hydrothermal microstructure of active calcium silicate, which creates a high air-content matrix that drives extremely low thermal conductivity without sacrificing mechanical integrity. Unlike fibrous insulation materials, calcium silicate boards retain their insulating and dimensional properties even in high-humidity environments, ensuring predictable performance over long service lives. Their ability to carry compressive loads also allows use as backing insulation in demanding industrial settings, expanding their addressable market beyond conventional building envelopes. Together, these durability, safety, and performance advantages position boards and sheets as the default product choice for active calcium silicate applications, securing their leading share in the market.

Market Share by End-Use Industry: Building and Construction Drive Sustained Adoption of Calcium Silicate Systems

The building and construction sector represents approximately 35% of total demand in the Active Calcium Silicate Market, making it the largest and most stable end-use segment. This leadership is driven by the sector’s focus on fire-safe, moisture-resistant, and energy-efficient building materials as urban density increases and green building regulations tighten. Calcium silicate boards are increasingly specified for interior wall linings, ceilings, and structural fire protection because they naturally regulate indoor humidity, preventing mold and mildew without chemical additives—a critical health and compliance advantage in residential and healthcare facilities. Market share is further supported by the material’s contribution to HVAC energy efficiency, as its thermal mass and insulating properties reduce temperature fluctuations and lower overall heating and cooling loads. From a construction workflow perspective, dry-install calcium silicate systems shorten project timelines by eliminating curing delays associated with sprayed fireproofing, improving contractor productivity. Acoustic performance also strengthens adoption in multi-family housing and institutional buildings, where noise control is a priority.

Competitive Landscape: High-Temperature Insulation, Fire Protection, and Industrial Performance

Competition in the Active Calcium Silicate Market centers on companies offering advanced high-temperature insulation, fire-resistant building materials, refractory backup solutions, and industrial thermal management boards with superior mechanical and chemical stability. Leading manufacturers differentiate through proprietary CaSi chemistries, automation-enhanced production, high compressive strength performance, and compliance with global fire safety standards. Their ability to support clients across construction, power, petrochemical, metal refining, and marine sectors strengthens their global positioning.

Promat (Etex Group) - Leader in Passive Fire Protection and High-Performance Calcium Silicate Boards

Promat utilizes proprietary PROMAXON® synthetic hydrated calcium silicate technology to manufacture PROMATECT®-100 boards known for exceptional passive fire protection. These boards provide 0.164 W/m·K thermal conductivity at 20°C and meet EN 13501-1 A1 non-combustibility standards, essential for building code compliance. Promat solutions are widely used in fire-rated partitions, structural steel protection, and high-performance commercial construction systems. With strong resistance to moisture and age-induced degradation, PROMATECT®-100 ensures long-term fire performance stability, making it a preferred solution for critical building applications.

Skamol Group - Specialist in High-Temperature Lightweight Calcium Silicate For Industrial Furnaces

Skamol is recognized for its high-temperature calcium silicate insulating boards such as Skamol S-1100E, engineered for refractory backup linings in industrial furnaces and kilns. These boards offer excellent chemical resistance to CO and hydrocarbons, enabling safe operation in demanding reducing atmospheres typical of metal and petrochemical processing. With continuous classification temperatures up to 1100°C, Skamol supports energy-efficient operation in ethylene reformers, gasifiers, and high-temperature reactors. The company further demonstrates sustainability leadership through early adoption of microsilica reuse, reducing material waste in CaSi production.

NICHIAS Corporation - Provider Of Advanced Fiber-Reinforced Casi For Power & Marine Applications

NICHIAS leverages extensive expertise in industrial insulation to deliver customized calcium silicate solutions optimized for LNG facilities, power generation plants, and shipbuilding-sectors requiring lightweight, non-combustible, and dimensionally stable insulation. Recent developments include integrating digital monitoring technologies into its fiber-reinforced boards, enabling real-time thermal diagnostics and predictive maintenance for large industrial installations. NICHIAS maintains strict production tolerances, ensuring reliable performance in high-efficiency equipment linings and regulated marine firewalls.

Johns Manville - North American Leader in High-Temperature Pipe & Block Calcium Silicate Insulation

Johns Manville produces premium CaSi solutions such as Micro-Lok® and Zeston®, widely used in petrochemical refineries, high-pressure steam lines, and energy facilities. Micro-Lok® pipe insulation is rated for up to 816°C (1500°F), supporting high-heat industrial systems. The company maintains one of the strongest North American supply chains, ensuring reliable delivery for large-scale construction and industrial projects. With soluble chloride content below 10 ppm, JM’s CaSi products help mitigate Corrosion Under Insulation (CUI), a major concern in chemical and refinery operations.

HIL Limited - APAC Leader in Fire-Resistant Casi For Infrastructure and Modular Construction

HIL Limited is a major regional producer of Aarthisil® calcium silicate boards, engineered for fire protection and acoustic performance in commercial and industrial facilities. Its extensive manufacturing network strengthens its leadership in India’s fast-growing construction market, where non-combustible materials have become regulatory priorities. Aarthisil® boards are used in data center fire partitions, HVAC systems, and modular construction. HIL continues to invest in expanding its CaSi portfolio to meet rising demand for lightweight, durable, and fire-resistant building materials across the APAC region.

India represents one of the fastest-expanding national markets for active calcium silicate, underpinned by infrastructure megaprojects and tighter building material appraisal frameworks. The certification of 84 innovative construction materials under the Performance Appraisal Certification Scheme (PACS) in 2025 has materially accelerated the acceptance of asbestos-free, high-purity calcium silicate boards in public housing, logistics parks, and industrial facilities. Rising real estate activity-supported by national development programs and long-term urbanization targets-is translating into consistent tender volumes for high-temperature insulation blocks used in power plants, refineries, and bulk storage terminals. State-issued tenders for replacing legacy insulation in turbines and tank farms further reinforce demand for active calcium silicate with low thermal conductivity and superior fire resistance, positioning India as a structurally strong consumption market through the decade.

China’s Dual-Carbon Mandate and Advanced Manufacturing Scale

China’s active calcium silicate market is being shaped by its “Dual Carbon” objectives and the rapid rollout of advanced manufacturing ecosystems. Fire safety codes mandating non-combustible cladding in mega-science parks and AI-driven industrial zones are driving large-scale adoption of calcium silicate panels and powders. Despite government efforts to stabilize construction material pricing, demand fundamentals remain firm due to sustained civil engineering activity and industrial retrofitting. Capacity expansions by regional leaders such as Luyang Energy-Saving Materials illustrate how calcium silicate is increasingly tied to high-growth segments like N-type solar cell manufacturing and energy-efficient industrial furnaces, reinforcing China’s role as both a volume producer and application innovator.

Germany’s Energy Renovation Push Under the EU Green Deal

Germany anchors the European active calcium silicate market through energy renovation mandates and sustainable building directives. The rebound in building permits in 2025 reflects renewed momentum in residential and commercial refurbishment, where calcium silicate-based interior insulation is favored for moisture control, mold prevention, and thermal efficiency. Rising import prices at major ports highlight steady demand rather than supply stress, while German processors are increasingly exporting value-added silicate solutions across the EU. This export-oriented strategy aligns with the bloc’s Sustainable-by-Design (SSbD) material philosophy, positioning Germany as a premium market focused on performance-certified, low-emission insulation materials rather than commodity volumes.

United States’ Industrial Revitalization and OSHA Compliance

In the United States, the active calcium silicate market is closely linked to industrial revitalization under the Infrastructure Investment and Jobs Act (IIJA). Upgrades to aging oil & gas assets, power generation units, and heavy manufacturing facilities are sustaining demand for reinforced calcium silicate blocks capable of withstanding extreme temperatures. Rising price indices in 2025 reflect strong industrial insulation demand rather than speculative pressure. Stricter OSHA standards on dust and particulates are also reshaping procurement preferences toward low-dust, engineered calcium silicate systems. Product innovation by companies such as Morgan Advanced Materials signals a broader shift toward hybrid insulation solutions that enhance durability while maintaining non-combustibility.

Japan’s Materials DX and ASEAN Infrastructure Linkages

Japan’s active calcium silicate market is characterized by precision engineering and export-led growth. The application of Materials Research DX platforms allows manufacturers to digitally model calcium silicate performance under seismic and thermal stress, supporting its use in high-spec domestic applications. Beyond Japan’s borders, infrastructure financing across Southeast Asia has become a critical demand lever, with Japanese-grade asbestos-free calcium silicate specified in transport, energy, and industrial projects. Firms such as KCC Corporation are optimizing particle size and purity levels to meet cleanroom and pharmaceutical standards, reinforcing Japan’s positioning as a high-value supplier rather than a mass producer.

United Kingdom’s Building Safety Act and Passive Fire Protection Shift

The UK active calcium silicate market is undergoing a regulatory-driven transformation following the enforcement of the Building Safety Act. Stricter certification “gateways” for high-rise construction have elevated demand for Euroclass A1-rated, non-combustible boards, making calcium silicate a preferred substrate in passive fire protection systems. Urban regeneration and façade remediation projects are increasingly specifying calcium silicate for internal partitions and cladding backers. Market participants such as RCM Products Ltd are expanding integrated building envelope solutions, underscoring how regulation is structurally embedding calcium silicate into the UK construction value chain.

Summary of Regional Market Drivers for Active Calcium Silicate (2025)

Active Calcium Silicate Development Matrix by Country

|

Country

|

Strategic Focus

|

Key 2025 Development

|

Demand Implication

|

|

India

|

Infrastructure & PACS certification

|

84 new materials certified

|

Public housing, power & industrial insulation

|

|

China

|

Dual-carbon & advanced manufacturing

|

Fire code enforcement in science parks

|

Large-scale panels & industrial additives

|

|

Germany

|

Energy-efficient renovation

|

Building permit recovery

|

Interior insulation & EU exports

|

|

United States

|

Industrial revitalization

|

IIJA-driven upgrades & OSHA tightening

|

Heavy-duty blocks for O&G and power

|

|

Japan

|

Materials DX & ASEAN exports

|

Digital performance modeling

|

Cleanroom & overseas infrastructure

|

|

United Kingdom

|

Fire safety compliance

|

Building Safety Act enforcement

|

Passive fire protection systems

|

Active Calcium Silicate Market Report Scope

Active Calcium Silicate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$227.9 Million

|

|

Market Size (2035)

|

$404.3 Million

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Product Form (Boards & Sheets, Blocks, Pipe Sections, Curved Segments, Powder), By Density Type (Low, Medium, High Density), By Temperature Grade (Mid-Temperature, High-Temperature, Ultra-High Temperature), By Application (Passive Fire Protection, High-Temperature Industrial Insulation, Soundproofing & Acoustic Protection, Structural Cladding, Refractory Linings), By End-Use Industry (Building & Construction, Industrial Manufacturing, Petrochemicals & Oil & Gas, Power Generation, Transportation)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Etex Group SA, Skamol A/S, Nichias Corporation, A&A Material Corporation, BNZ Materials Inc., PABCO Building Products LLC, Zhejiang Advanced Materials Co., Ltd., Taisui Corporation, VILAS GmbH, Ramco Industries Limited, Soben Board Company Limited, Newkem Engineers Pvt. Ltd., Anglitemp Limited, Luoyang Blue Star Refractory Co., Ltd., Maryland Refractories Company Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Active Calcium Silicate Market Segmentation

By Product Form

- Boards and Sheets

- Blocks

- Pipe Sections

- Curved Segments

- Powder

By Density Type

- Low Density

- Medium Density

- High Density

By Temperature Grade

- Mid-Temperature

- High-Temperature

- Ultra-High Temperature

By Application

- Passive Fire Protection

- High-Temperature Industrial Insulation

- Soundproofing and Acoustic Protection

- Structural Cladding

- Refractory Linings

By End-Use Industry

- Building and Construction

- Industrial Manufacturing

- Petrochemicals and Oil and Gas

- Power Generation

- Transportation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Active Calcium Silicate Market

- Etex Group SA

- Skamol A/S

- Nichias Corporation

- A&A Material Corporation

- BNZ Materials, Inc.

- PABCO Building Products, LLC

- Zhejiang Advanced Materials Co., Ltd.

- Taisui Corporation

- VILAS GmbH

- Ramco Industries Limited

- Soben Board Company Limited

- Newkem Engineers Pvt. Ltd.

- Anglitemp Limited

- Luoyang Blue Star Refractory Co., Ltd.

- Maryland Refractories Company, Inc.

*- List not Exhaustive