Market Overview: Adipic Acid Market to Reach $12.5 Billion by 2034 Amid Capacity Shifts, Decarbonization Technologies, and Feedstock Volatility

The global adipic acid market is forecast to expand from $8.5 billion in 2025 to $12.5 billion by 2034, advancing at a 4.4% CAGR. Market dynamics are shaped by demand from Nylon 6,6 engineering plastics, polyurethane intermediates, plasticizers, coatings resins, and PBAT biodegradable polymers, alongside structural realignment of production geography and tightening environmental performance expectations. Adipic acid remains a critical C6 dicarboxylic acid within the polyamide value chain, yet producers are under pressure to reduce nitrous oxide emissions, product carbon footprint, and fossil feedstock dependency while navigating persistent oversupply and raw material price volatility. Competitive advantage is increasingly linked to process efficiency, emissions abatement systems, bio-based feedstocks, and access to low-cost benzene supply.

Decarbonization and sustainability initiatives gained traction in March 2024 when BASF secured ISCC PLUS certification for its South Korean sites, enabling mass-balance certified adipic acid supply to Asian automotive and textile customers. Environmental mitigation advanced further in December 2024 as Ascend Performance Materials activated a thermal reduction unit at Pensacola capable of eliminating about 98% of N₂O emissions associated with adipic acid production. In the same month, Ascend launched its Bioserve portfolio using used cooking oil feedstocks, marking commercial production of lower carbon adipic acid and Nylon 6,6. Portfolio restructuring followed in April 2025 when LANXESS divested its Urethane Systems business to UBE, finalizing its shift away from integrated adipic acid chains. Specialty-grade capability expansion occurred in May 2025 as Ascend upgraded purification systems at Chocolate Bayou to support high-purity chemical output relevant for medical and aerospace polymers. Breakthrough green chemistry research emerged in June 2025 when biotech firm OzoneBio demonstrated wood waste to adipic acid conversion with minimal N₂O generation.

Structural supply adjustments intensified in November 2025 as the EU imposed provisional anti-dumping duties on Chinese adipic acid imports, while in December 2025 BASF announced closure of adipic acid production at Ludwigshafen, shifting supply reliance to its Onsan site and Chalampé joint venture. Feedstock pressures rose in January 2026 when Sinopec increased benzene prices, lifting cost floors for adipic acid producers. The same month, China accelerated bio-based adipic acid industrialization at demonstration scale to address carbon border tariff risks. Market fundamentals point to oversupply, confirmed in February 2026 by industry forecasts indicating global utilization near 60%. Capacity expansion remains underway, with Rongsheng New Materials expected to commission a 450,000-ton plant in China in the second half of 2026, pushing domestic capacity above 4.45 million tons and reinforcing pricing pressure across global adipic acid markets.

Strategic Market Trends and Emerging Growth Opportunities Transforming the Adipic Acid Market Landscape

Market Trend: Nylon 66 Supply-Chain Constraints Forcing Structural Reallocation of Adipic Acid Output

A defining trend impacting the adipic acid value chain is the persistent upstream constraint in Adiponitrile (ADN), which is forcing global producers to prioritize captive Nylon 66 production over non-integrated derivatives such as polyurethane polyols, synthetic lubricants, and plasticizers. This imbalance creates a competitive advantage for vertically integrated players, establishing output control as a pricing lever rather than a volume-driven strategy.

INVISTA’s planned USD 500 million investment (Summer 2025) toward reinforcing its global Nylon 6,6 polymer and intermediates production is strategically aligned with a wider USD 2 billion commitment to stabilize ADN and AA supply in North America, Europe, and China. The February 2025 opening of INVISTA’s USD 13 million Houston technology hub demonstrates a shift toward process optimization IP as a market differentiator, improving ADN-to-HMD conversion efficiency and protecting adipic acid throughput reliability.

Regional supply disparities are shaping trade dynamics. While European producers face elevated energy pricing and nitrous oxide (N₂O) abatement mandates, China has maintained strong adipic acid operating rates. However, due to downstream PA66 capacity utilization at only 69% in China (late 2025), excess adipic acid supply there remains subject to EU anti-dumping tariffs ranging 28.6% to 46.8 percent, reshaping trade routes and positioning China increasingly as a price taker rather than a supply determinant.

Market Trend: Transition From Lab R&D to Pilot and Commercial Scale for Bio-Based Adipic Acid

The shift to plant-based carbon feedstock is now moving into commercialized pilot deployment as major chemical firms accelerate the decarbonization of polyamide value chains. Covestro’s February 2025 pilot facility in Leverkusen, which utilizes biological conversion of industrial sugars, is a key milestone signaling that fossil benzene replacement is no longer theoretical—it is transitioning into ton-level feasibility.

Global alliances are emerging as the commercialization backbone. Asahi Kasei and Genomatica (Geno) expanded their biotechnology partnership in 2025 to integrate bio-HMDA and bio-adipic acid into full-scale Nylon 6,6 processing. Strategic sourcing alliances are multiplying, driven by downstream brand commitments. A major specialty-chemicals company publicly disclosed mid-2025 investment into new adipic capacity built specifically for advanced purification of bio-based grades, targeting consumer-facing brands aligned with the Geno-led initiative (L’Oréal, lululemon, others).

By 2030, bio-based adipic acid will likely move from pilot-phase novelty to a premium-priced revenue band, particularly for apparel, luxury textiles, and automotive OEM sustainability programs.

Market Opportunity: Adipic Acid as a Strategic Precursor for Lithium-Ion Battery Electrolyte Additives

The electrification of mobility and scaling of gigafactories are opening an entirely new demand pool for adipic acid, where it is positioned not as a polymer intermediate but as a functional chemical enabling battery performance longevity. The U.S. DOE Argonne Laboratory (Feb 2025) underscores that next-generation electrolyte mixtures—particularly for silicon anodes—require new additives capable of stabilizing the Solid Electrolyte Interphase (SEI) layer.

AA-derived dicarboxylate additives are being studied for thermal stability above 180°C, enabling operation at voltages where traditional electrolytes degrade. As global EV output is expected to exceed 30 million units by 2032, demand for adipic-derived SEI chemicals could become a structurally price-inelastic segment, given its direct correlation to battery lifespan, safety, and warranty economics.

Strategically, producers like BASF and Ascend Performance Materials are positioning their adipic acid and hexamethylenediamine (HMD) assets to serve not only nylon but battery housings, connectors, and thermal-resistant components, leveraging Nylon 66’s mechanical and heat-resistance profile within EV platforms.

Market Opportunity: Adipic Acid Enabling Sustainable Polyamide Alternatives (PA 5,6) for Apparel and Technical Textiles

A major commercial horizon for adipic acid lies in new-generation bio-polyamides, particularly PA 5,6, where adipic acid is paired with bio-based pentamethylenediamine. These resins represent drop-in substitutes for Nylon 66 while offering superior sustainability profiles.

Cathay Biotech is leading industrial adoption. According to its February 27, 2025 results, revenue grew 39.84% largely due to its TERRYL bio-based polyamide portfolio. Its Northwest China production complex—backed by USD 596.5 million investment—supports 100,000-ton annual output of long-chain diacids and PA 5,6, underpinning Asia Pacific as the fastest-scaling region for decarbonized engineering materials.

Property benchmarks strengthen commercial viability: PA 5,6 achieves 252°C melting point and better moisture-management vs PA66, positioning it for high-performance apparel, outdoor gear, automotive fibers, and filtration media. As global brands redesign procurement toward science-backed sustainability metrics, adipic acid’s role will evolve into a foundational molecule enabling low-emission fiber supply chains.

Adipic Acid Market Share and Segmentation Insights

Market Share by Raw Material: Cyclohexane Dominates While Bio-Adipic Acid Accelerates

Cyclohexane accounts for approximately 64% of global adipic acid production in 2025, maintaining dominance as the most cost-effective and industrially established route, typically integrated into large-scale benzene hydrogenation complexes. Despite its scale advantages, this pathway carries elevated carbon intensity and exposure to benzene price volatility, influencing margin cycles. KA Oil, comprising cyclohexanol and cyclohexanone, represents a significant but smaller share, often utilized by producers with captive intermediate capacity or those optimizing cyclohexane oversupply. The KA Oil route offers marginally higher yields but involves greater operational complexity. Renewable feedstocks represent roughly 5% of supply yet are expanding, driven by regulatory frameworks such as the EU Emissions Trading System and the US Inflation Reduction Act. Technologies using glucose, lignin, and waste oils are achieving polymer-grade purity, enabling bio-based Nylon 6,6 adoption. Notably, over 60% of adipic acid consumption remains tied to Nylon 6,6 production, with recent stabilization in butadiene-based adiponitrile supply easing pricing pressures.

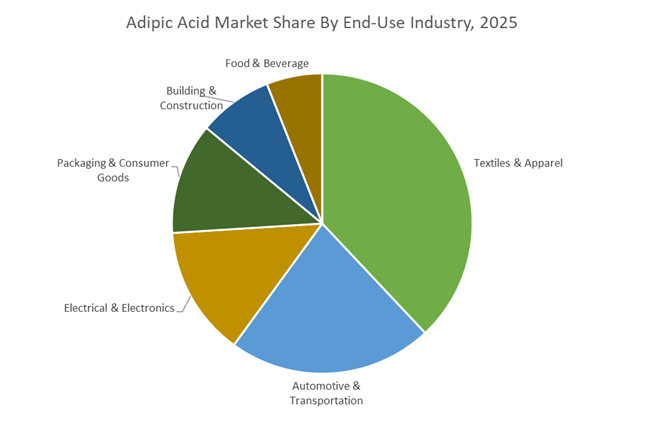

Market Share by End-Use Industry: Textiles Lead While Electronics Delivers Fastest Expansion

Textiles & apparel represent approximately 38% of global adipic acid demand in 2025, primarily through Nylon 6,6 fiber production, valued for superior durability, elasticity, and thermal resistance compared to Nylon 6. Activewear, athleisure, and premium fashion segments continue to drive volume, with increasing adoption of bio-based adipic acid aligned with Scope 3 decarbonization commitments. Automotive & transportation rank second, where Nylon 6,6 engineering plastics are essential for under-hood components, connectors, and EV battery systems, sustaining steady 3 to 4% annual growth. Electrical & electronics is the fastest-growing segment, supported by rising demand for high-melting-point, dimensionally stable polymers in connectors, LED reflectors, and 5G infrastructure. Packaging & consumer goods leverage adipic acid for high-barrier nylon films and appliance-grade plastics, benefiting from stable e-commerce demand. Building & construction remains interest-rate sensitive, while food & beverage applications, primarily as an acidulant, exhibit GDP-linked growth with minimal volatility.

Competitive Landscape: Circular Nylon Integration and Energy-Optimized Production Reshaping the Adipic Acid Market

The global Adipic Acid Market is undergoing structural transformation as producers pivot from commodity volume toward circular polyamide systems, energy-efficient production hubs, and high-purity specialty grades. Competitive leadership now hinges on vertical integration across the nylon 6,6 value chain, bio-based adipic acid development, and proximity to automotive, electronics, and engineering plastics manufacturing clusters. Major players are reallocating capacity from Europe to Asia, accelerating chemical recycling of polyamides, and embedding biomass-balanced feedstocks to meet decarbonization targets. Below is a detailed assessment of how leading companies are repositioning adipic acid portfolios for EV mobility, sustainable textiles, and advanced polymer applications.

BASF SE restructures adipic acid operations toward China-centered Verbund efficiency

BASF SE remains a dominant adipic acid producer while executing a major strategic reset of its European footprint. In 2025, BASF announced the closure of its remaining Ludwigshafen adipic acid plants to preserve competitiveness under high regional energy costs. Production is shifting toward Zhanjiang and Caojing in China, leveraging lower-cost utilities and proximity to global electronics and automotive hubs. BASF also commissioned its first commercial loopamid® facility in Shanghai, enabling textile-to-textile recycling of PA6 via purified monomers. Its portfolio includes high-purity adipic acid for polyurethanes, coatings, and adhesives, increasingly aligned with BMBcert™ biomass-balance certification.

Invista leads high-purity adipic acid for electronics, medical, and specialty chemicals

Invista, a subsidiary of Koch Industries, anchors the nylon 6,6 value chain with proprietary Adi-pure® technology that delivers ultra-low impurity adipic acid for demanding electronics and medical applications. Beyond fibers, Invista commands strong positions in synthetic lubricants and paper wet-strength resins where chemical stability is critical. Its vertically integrated platform spans cyclohexane feedstocks through finished engineering resins for airbags and automotive components. The company also supplies pharmaceutical excipient grades and adipic acid sequestrants for industrial metal ion control, reinforcing its role as a specialty-focused adipic acid supplier rather than a bulk commodity producer.

Ascend Performance Materials accelerates bio-based adipic acid following financial restructuring

Ascend Performance Materials is one of the few fully integrated nylon 6,6 producers globally, emerging from Chapter 11 in December 2025 after a $1.3 billion debt reduction. This reset enabled renewed R&D and capital investment across Alabama and Florida. In April 2025, Ascend acquired a compounding facility in San Jose Iturbide, Mexico, strengthening its Latin American automotive footprint. The company introduced its Bioserve portfolio using used cooking oil feedstocks to produce adipic acid with a 25% lower carbon footprint. Strategically, Ascend is targeting leadership in engineering thermoplastics for E-mobility and high-voltage electrical components.

Lanxess AG integrates adipic acid into high-performance nylon and green building materials

Lanxess is repositioning adipic acid within specialty materials through strategic partnerships and portfolio optimization. In 2025, the company finalized a EUR 3.7 billion joint venture with Advent International integrating DSM Engineering Materials, elevating Lanxess into a key supplier of high-performance nylon intermediates. Backward integration into phosphorus-based chemistries supports adipic acid-derived non-phthalate plasticizers and polyurethane insulation resins. Lanxess leverages its European network to supply closed-cell PU systems for green buildings and implemented a global adipic acid price adjustment in January 2026 to offset rising energy and feedstock costs while maintaining supply continuity.

Asahi Kasei Corporation pioneers circular PA66 and high-purity adipic acid for advanced mobility

Asahi Kasei Corporation is advancing circular adipic acid production through a microwave-based nylon 6,6 recycling process developed with Microwave Chemical, enabling depolymerization back to high-yield monomers. Under its Trailblaze Together 2025–2027 strategy, Asahi Kasei prioritizes electronic materials and automotive components requiring ultra-pure adipic acid. Key offerings include Leona™ PA66 engineering plastics and newly launched PFAS-free PA66 for low-friction automotive parts. In early 2026, the company partnered with Mitsui and Mitsubishi Chemicals to decarbonize ethylene and propylene production in western Japan, securing more sustainable upstream feedstocks.

RadiciGroup strengthens textile and engineering plastics integration across Europe and Asia

RadiciGroup is a vertically integrated European player spanning adipic acid, HMD, fibers, and engineering plastics. The company leads in technical textiles, supplying adipic acid for airbags, parachutes, and high-durability sports apparel. RadiciGroup is actively developing bio-based nylon 6,6 routes using fully renewable intermediates to differentiate from commodity suppliers. During 2025–2026, it expanded operations in India and Turkey to support rising demand for lightweight automotive plastics. Full control of its production chain enables rapid customization across textiles and engineering polymers, positioning RadiciGroup as a flexible supplier to both mobility and performance apparel markets.

China Adipic Acid Market: Capacity Discipline, Nylon 6,6 Expansion, and Digitalized Operations

China remains the largest demand center for adipic acid, underpinned by policy-led growth targets and strong nylon 6,6 expansion. In September 2025, the Ministry of Industry and Information Technology released the Work Plan for Stabilizing Growth in the Petrochemical and Chemical Industry (2025–2026), targeting average annual growth of more than 5%. At the same time, Beijing has tightened approvals for new refining and coal-to-chemical projects to mitigate overcapacity risks in traditional adipic acid production routes, signaling a clear preference for high-end and specialty supply.

Demand fundamentals remain robust. Between 2024 and 2025, Chinese producers added more than 300,000 metric tons of nylon 6,6 capacity, creating a localized and structural pull for adipic acid feedstock used in automotive components, industrial fibers, and engineering plastics. Infrastructure synergy is further reinforced by China’s expansion into high-end polyolefins and electronic chemicals, where nylon 6,6 plays a critical role. Despite these strengths, pricing pressure persisted in Q4 2025 due to ample spot inventories and temporarily softened downstream demand during the Golden Week holiday period. On the operational front, the late-2025 “AI plus Petrochemicals” initiative is accelerating the adoption of digital twins in adipic acid plants, enabling real-time emission tracking, predictive maintenance, and process yield optimization.

Germany Adipic Acid Market: Structural Exit, Emission Compliance, and Margin Pressure

Germany’s adipic acid landscape is undergoing a structural reset driven by energy economics and regulatory stringency. BASF formally announced the cessation of adipic acid production at its Ludwigshafen complex by 2025 as part of a broader profitability overhaul in response to persistently high European energy costs. The shutdown also includes downstream units for cyclododecanone and cyclopentanone, shifting regional supply focus toward BASF’s joint venture operations in France.

Regulatory compliance remains a defining theme. German producers are integrating advanced catalytic reduction systems to meet the European Chemicals Agency mandate of reducing nitrous oxide emissions by 50% by 2030. Sustainability differentiation is increasing, with German sites leading the adoption of ISCC PLUS mass-balance certification for bio-based adipic acid aimed at green automotive supply chains. However, export competitiveness has weakened. By late 2025, producers reported margin strain due to aggressive pricing from Chinese imports and cautious procurement behavior among European automakers navigating uncertain demand conditions.

United States Adipic Acid Market: Trade Protection, Low-Emission Production, and Automotive Stability

The United States adipic acid market is characterized by trade-driven sourcing shifts and strong sustainability positioning. Elevated tariffs on petrochemical intermediates introduced in spring 2025 significantly raised the landed cost of imported adipic acid, accelerating a pivot toward domestic supply. This shift has reinforced the strategic relevance of U.S.-based production assets.

Sustainability investments are advancing in parallel. Invista announced in 2025 that its Victoria, Texas facility is pursuing recertification for bio-circular and renewable adipic acid, supporting downstream partners such as Celanese in producing lower-carbon nylon 6,6. In February 2025, Invista also inaugurated a 13 million dollar Technology Hub near Houston to accelerate R and D across the nylon and propylene value chains, with a focus on process efficiency and emission reduction. Despite broader retail softness, adipic acid pricing remained stable through December 2025, supported by consistent automotive demand for airbags and under-the-hood components. Leading producers are advancing low-emission adipic acid programs targeting a 60% reduction in CO₂-equivalent emissions per ton by the end of 2025.

India Adipic Acid Market: Import Substitution, Automotive Momentum, and Regulatory Clarity

India is emerging as a structurally important growth market for adipic acid as domestic capacity plans align with rising downstream consumption. Reliance Industries is progressing plans to establish a new adipic acid facility by late 2025, targeting demand from the automotive and textile sectors. This investment supports India’s long-term objective of reducing reliance on imports from China and Singapore.

Demand-side fundamentals are compelling. India’s automotive component market reached a valuation of 74.1 billion dollars in 2024, underpinning sustained nylon 6,6 consumption for engineering plastics and fibers. Regulatory updates are also shaping the market. The Food Safety and Standards Authority of India has notified new food additive regulations effective February 2026, tightening purity standards for adipic acid used as an acidulant. Combined with fiscal incentives under the Make in India program, these measures are improving supply security while encouraging higher-quality domestic production.

Japan Adipic Acid Market: Bio-Based R and D and High-Purity Market Focus

Japan’s adipic acid industry is increasingly defined by green chemistry innovation and selective market participation. In 2025, Sumitomo Chemical launched collaborative programs with academic institutions to commercialize bio-based adipic acid solutions by 2026. These initiatives emphasize microbial fermentation routes that convert non-food biomass into adipic acid precursors, bypassing conventional cyclohexane oxidation and reducing lifecycle emissions.

Commercial strategy in Japan is deliberately selective. Producers are prioritizing high-purity adipic acid grades for electronics, specialty polyurethanes, and precision applications, avoiding exposure to volatile commodity segments. This approach reflects Japan’s broader strategy of competing on quality, performance consistency, and environmental credentials rather than scale.

France Adipic Acid Market: Western Europe’s Supply Anchor and Bio-Circular Integration

France has become the primary production anchor for adipic acid in Western Europe following Germany’s structural exit. The Chalampé site, operated as a joint venture between BASF and DOMO Chemicals, now plays a central role in regional supply security. The facility has undergone major upgrades in nitrous oxide abatement, achieving more than 90% emission reduction compared with 2020 benchmarks.

Sustainability integration is accelerating. In April 2025, French operations were included in expanded ISCC PLUS certification programs, enabling traceable bio-circular adipic acid supply for fashion, textile, and automotive customers. These credentials are strengthening France’s position as a preferred supplier to European brands with strict sustainability sourcing requirements.

Country-Level Positioning in the Adipic Acid Industry

Adipic Acid Market County Level Snapshot

|

Country

|

Strategic Focus

|

Market Impact

|

|

China

|

Capacity discipline, nylon 6,6 expansion, digital twins

|

Volume leadership with managed oversupply

|

|

Germany

|

Structural exit, emission compliance, certification

|

Reduced capacity with sustainability differentiation

|

|

United States

|

Tariff protection, low-emission production

|

Stable pricing and domestic sourcing resilience

|

|

India

|

New capacity, automotive growth, import substitution

|

Emerging demand-driven production base

|

|

Japan

|

Bio-based R and D, high-purity focus

|

Specialty-grade leadership

|

|

France

|

Regional anchoring, ISCC PLUS integration

|

Secure Western European supply

|

Adipic Acid Market Report Scope

Adipic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.5 Billion

|

|

Market Size (2034)

|

$12.5 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Raw Material (Cyclohexane (Petroleum-based), Cyclohexanol & Cyclohexanone (KA Oil), Renewable Feedstocks (Glucose, Lignocellulosic Biomass, Waste Carbon)), By Application (Nylon 6,6 Fibers, Nylon 6,6 Engineering Resins, Polyurethane (PU), Adipate Esters, Wet Paper Resins, Food Additives), By End-Use Industry (Automotive & Transportation, Textiles & Apparel, Electrical & Electronics, Building & Construction, Packaging & Consumer Goods, Food & Beverage), By Sales Channel (Direct Sales, Indirect/Distribution Channels)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Invista, Ascend Performance Materials, Domo Chemicals, Asahi Kasei Corporation, LanzaTech Global, Inc., Sumitomo Chemical Co., Ltd., LG Chem Ltd., Huafon Group, Shenma Industrial Co., Ltd., PetroChina Company Limited, Radici Partecipazioni SpA, Lanxess AG, Reliance Industries Limited, Geno

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Adipic Acid Market Segmentation

By Raw Material

- Cyclohexane (Petroleum-based)

- Cyclohexanol & Cyclohexanone (KA Oil)

- Renewable Feedstocks (Glucose

- Lignocellulosic Biomass

- Waste Carbon

By Application

- Nylon 6,6 Fibers

- Nylon 6,6 Engineering Resins

- Polyurethane (PU)

- Adipate Esters

- Wet Paper Resins

- Food Additives

By End-Use Industry

- Automotive & Transportation

- Textiles & Apparel

- Electrical & Electronics

- Building & Construction

- Packaging & Consumer Goods

- Food & Beverage

By Sales Channel

- Direct Sales

- Indirect/Distribution Channels

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Adipic Acid Market

- BASF SE

- Invista

- Ascend Performance Materials

- Domo Chemicals

- Asahi Kasei Corporation

- LanzaTech Global Inc.

- Sumitomo Chemical Co. Ltd.

- LG Chem Ltd.

- Huafon Group

- Shenma Industrial Co. Ltd.

- PetroChina Company Limited

- Radici Partecipazioni SpA

- Lanxess AG

- Reliance Industries Limited

- Geno

*- List not Exhaustive