Market Overview: Aero Engine Coatings Market to Reach $654 Million by 2034 as High-Temperature Protection, Fuel Efficiency, and Chrome-Free Technologies Drive Growth

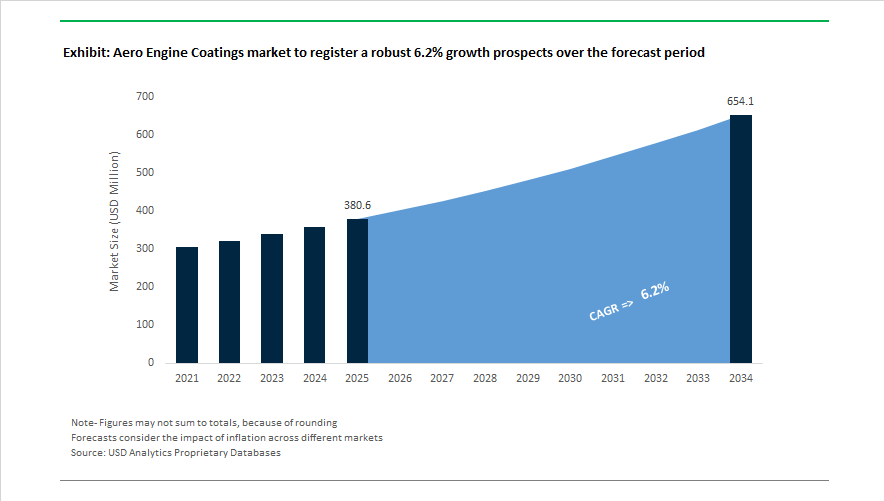

The global aero engine coatings market is projected to expand from $380.6 Million in 2025 to $654 Million by 2034, advancing at a 6.2% CAGR supported by rising aircraft production, fleet modernization, and increasing MRO activity. Aero engine coatings play a critical role in thermal protection, oxidation resistance, corrosion control, wear mitigation, and aerodynamic efficiency, particularly within turbine hot sections operating under extreme temperatures and pressure cycles. Demand is intensifying for thermal barrier coatings (TBC), environmental barrier coatings (EBC), diffusion coatings, PVD coatings, and advanced thermal spray solutions that extend component life while reducing fuel burn and emissions. Regulatory pressure to eliminate hexavalent chromium, combined with sustainability mandates and the push for higher turbine operating temperatures, is accelerating development of chrome-free, low-VOC, and bio-based coating chemistries.

Technology advancement began gaining momentum in July 2024 when Oerlikon Balzers introduced BALORA TECH PRO environmental barrier coating designed for high-temperature turbine protection. Expansion into emerging aerospace hubs followed in January 2025 with Oerlikon inaugurating its Smart Integrated Surface Solutions Centre in India to support domestic aerospace manufacturing. Sustainable coating adoption accelerated in February 2025 as AkzoNobel launched an environmentally responsible wood coating line for business jets, reflecting a broader portfolio shift. Chrome-free innovation gained recognition in January 2025 when Indestructible Paint won a major surface engineering award and reported a 19% turnover rise linked to adoption of green diffusion coatings. MRO coating capability expanded in mid-2025 as ATL Turbine Services invested in advanced thermal spray systems supplied by Oerlikon.

Regulatory and capacity developments reshaped the competitive landscape. In August 2025, aerospace suppliers secured a 12-year REACH re-authorisation for legacy chrome-based products, allowing time for qualification of alternatives. Market momentum strengthened in January 2026 when PPG Industries reported record aerospace sales and strong forward guidance tied to fuel-efficiency coatings. Regional supply chains advanced in January 2026 with AkzoNobel establishing a Dubai aerospace coatings hub to serve Middle Eastern airlines and MRO operators. Engine OEM investment intensified in February 2026 as RTX expanded coating capabilities in Singapore for GTF engine components. The same month, Oerlikon completed structural divestment to focus exclusively on surface solutions, while Indestructible Paint showcased chrome-free CFIPAL diffusion coatings rated for 1,000°C operation. Hentzen Coatings marked its centenary in January 2026, reaffirming focus on waterborne and chrome-free primers for military aviation platforms. These developments underscore the strategic role of advanced surface engineering in next-generation aero engine performance and lifecycle cost reduction.

Trends and Opportunities Shaping the Aero Engine Coatings Market

The Global Aero Engine Coatings Market is entering a high-innovation phase, driven by additive manufacturing adoption, Sustainable Aviation Fuel (SAF) certification, and the emergence of next-generation open fan engine architectures. Demand is accelerating for thermal barrier coatings (TBCs), environmental barrier coatings (EBCs), erosion resistant coatings (ERCs), and smart aerospace coatings as OEMs push engines to higher operating temperatures while pursuing aggressive decarbonization targets. These dynamics are reshaping coating qualification cycles, material science roadmaps, and supplier value chains across commercial aviation, defense aerospace, and space propulsion programs.

Additive Manufacturing Adoption Forces Advanced Internal Coating Technologies for Flight-Critical Components

The rapid transition of metal additive manufacturing (AM) from prototyping to certified production is fundamentally altering aero engine coating requirements. According to Eurostat (2025), a 19.3% rise in air passenger traffic has intensified OEM pressure to deploy AM for rapid component production, accelerating certification of 3D-printed fuel nozzles and structural brackets that require high-performance thermal barrier coatings to preserve fatigue resistance and thermal stability.

Public project disclosures from America Makes and the Air Force Research Laboratory’s PADAM 2.0 initiative (early 2026) confirm over $6 million directed toward high-temperature powder alloy development for laser powder bed fusion (L-PBF). These advanced alloys exhibit intrinsic surface porosity, driving demand for complementary thin-film aerospace coatings engineered to seal micro-defects without negating AM’s lightweight advantages. Direct industry benchmarks indicate AM-enabled lightweight components can reduce production costs by up to 30%, reinforcing market pull for low-mass ceramic coatings, bond coats, and precision internal spray deposition technologies optimized for complex cooling channels.

Sustainable Aviation Fuel Compatibility Pushes Aero Engine Coatings Beyond Traditional Thermal Limits

As engine platforms move toward 100% Sustainable Aviation Fuel readiness, combustion chemistry is changing, reshaping corrosion and wear profiles across hot-section components. Rolls-Royce validated maximum-power operation of its UltraFan demonstrator on 100% SAF in late 2024, confirming that next-generation aero engine coatings must withstand altered hot-corrosion signatures associated with low-aromatic fuels.

Data from the U.S. Department of Energy shows SAF can cut lifecycle emissions by up to 80%, but reduced sulfur and aromatic content also changes fuel lubricity, necessitating new wear-resistant coatings for fuel-wetted systems. Simultaneously, the World Economic Forum Global Aviation Sustainability Outlook 2025 highlights regulatory pressure from International Civil Aviation Organization targets for a 5% carbon intensity reduction by 2030. To meet efficiency mandates, OEMs are running engine cores at higher temperatures, frequently exceeding 1,482°C, pushing conventional TBCs to phase-stability limits and accelerating R&D in next-generation ceramic matrix coatings, rare-earth stabilized TBCs, and oxidation-resistant bond layers.

Integrated Post-Processing and Coating Workflows Create New Revenue Streams for AM Engine Parts

The “as-printed” surface roughness of additively manufactured components remains a major barrier to aerodynamic efficiency and coating adhesion, opening a sizable opportunity for specialized post-processing combined with advanced coating application. Academic-industry collaborations published in late 2025 emphasize that tailored finishing steps, including Hot Isostatic Pressing (HIP) and electropolishing, are now prerequisites for applying environmental barrier coatings on AM parts to prevent delamination and premature spallation.

In early 2026, Manufacturing USA launched a $2 million AIM-4AM initiative using AI to establish material allowables, creating a parallel opportunity for coating suppliers to deploy AI-driven coating thickness optimization across complex internal lattices. Regionally, the commissioning of large-format aerospace AM facilities by Agnikul Cosmos underscores rising demand for scalable automated spray systems capable of coating large 3D-printed engine housings, reinforcing growth prospects for robotic plasma spray, HVOF, and advanced slurry-based ceramic deposition platforms.

Open Fan Engine Architectures Accelerate Demand for Erosion-Resistant and Smart Coating Systems

Next-generation propulsion programs are introducing radically different exposure environments. The CFM RISE initiative is pioneering Open Fan architectures that leave more components vulnerable to atmospheric particulates and high-velocity debris, amplifying the need for ultra-durable erosion resistant coatings on fan blades and leading edges. A 2025 technology update from GE Aerospace showed GEnx durability upgrades delivered a 2.5x improvement in time-on-wing under harsh operating conditions, setting performance benchmarks for future Open Fan platforms.

On the thermal front, NASA Glenn Research Center has patented advanced environmental barrier coatings capable of protecting ceramic matrix composites at temperatures up to 1,482°C, specifically engineered for compact, high-pressure cores envisioned in RISE-class engines. With over 3,000 endurance cycles already logged on new high-pressure turbine technologies, validation intensity is rising sharply, creating a high-value opportunity for smart aerospace coatings embedded with predictive maintenance sensors. These intelligent coating layers enable real-time degradation monitoring, positioning suppliers at the center of condition-based maintenance strategies for future commercial and defense aero engines.

Aero Engine Coatings Market Share and Segmentation Insights

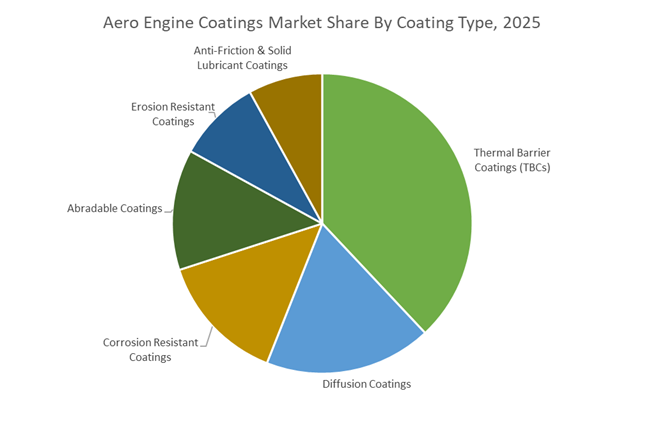

Market Share by Coating Type: Thermal Barrier Coatings Dominate as Next-Gen Chemistries Enter Service

Thermal barrier coatings (TBCs account for approximately 38% of the aero engine coatings market in 2025, driven by the industry’s push toward higher turbine inlet temperatures to improve fuel efficiency and thrust. Advanced 7–8YSZ ceramic topcoats applied via EB-PVD and APS remain standard, with CMAS-resistant and ultra-high-temperature formulations entering service on next-generation engines. Diffusion coatings rank second, forming the foundation of oxidation and hot corrosion protection through aluminide and platinum-aluminide bond coats, with MRO demand particularly strong. Corrosion resistant coatings support compressor durability in marine and high-salinity environments, while abradable coatings enable tight tip clearances, directly improving engine efficiency. Erosion resistant coatings protect against sand and ash ingestion on desert and long-haul routes. Anti-friction and solid lubricant coatings represent the smallest segment but remain essential for bearings and linkages, with MoS₂ and DLC adoption rising amid environmentally driven lubricant reformulations.

Market Share by Component: Turbine Blades Lead as Combustors and Compressors Gain Technical Complexity

Turbine blades and vanes capture nearly 47% of total aero engine coating revenues in 2025, reflecting their operation in extreme gas-path environments exceeding 1400°C. These components require multilayer systems combining diffusion bond coats, ceramic TBCs, and coated internal cooling channels, with high-pressure turbine blades individually processed in vacuum chambers using single-crystal superalloys, making this the highest-value application. Combustion chambers rank second, relying heavily on TBCs to withstand thermal cycling, with additive manufacturing reshaping coating approaches for complex internal geometries. Compressor blades are high-volume but lower value per part, primarily requiring erosion and corrosion protection, while the shift toward blisks reduces part count but increases coating complexity. Bearings and shafts depend on anti-friction coatings to extend time-on-wing, linking growth to flight hours. Afterburners remain niche but command premium pricing due to extreme temperature and oxidation resistance requirements.

Competitive Landscape: Advanced Surface Engineering Driving Durability and Efficiency in the Aero Engine Coatings Market

The Aero Engine Coatings Market is being reshaped by next-generation thermal barrier coatings, PFAS-free surface treatments, ceramic matrix composite protection, and AI-enabled inspection systems. Competitive advantage increasingly depends on vertically integrated coating ecosystems, proprietary materials science, and close alignment with OEM and MRO networks. Market leaders are channeling capital toward hot-section durability, environmental barrier coatings, and retrofit programs for next-generation turbofans, while regulatory pressure accelerates adoption of chrome-free and sustainable aviation–ready coating platforms. Below is a structured analysis of the companies defining performance benchmarks across turbine blades, combustors, and engine nacelles.

Oerlikon concentrates surface technologies into a unified global coating platform

Oerlikon operates one of the world’s most comprehensive surface engineering ecosystems, with over 140 coating centers delivering everything from Metco™ thermal spray powders to Balzers™ thin-film systems and robotic plasma spray equipment. In early 2026, Oerlikon divested its Barmag business to Rieter, sharpening focus on Surface Solutions and Additive Manufacturing. The company pioneered a PFAS-free PVD coating line in 2025, now widely adopted as a hard-chrome replacement for engine components. Its advanced wear-resistant and thermal barrier coatings are critical for high-pressure turbine blades, reinforcing Oerlikon’s position as a preferred partner for OEMs seeking higher temperature capability and extended engine life.

GE Aerospace embeds AI inspection and ceramic composites into next-generation engine coatings

GE Aerospace, now operating independently, is redefining aero engine durability through deep integration of materials science and digital diagnostics. In 2026, the company committed over $1 billion to its global MRO network, emphasizing proprietary coating retrofits for LEAP and GEnx engines. GE Aerospace recently completed altitude testing of its GEK800 lightweight engine using advanced sub-surface inspection and coating validation. Its leadership in Ceramic Matrix Composites requires specialized environmental barrier coatings capable of surviving temperatures above 1,300°C. An AI-enabled inspection platform deployed in late 2025 now detects early-stage coating degradation in hot sections, reducing unplanned removals.

Pratt & Whitney advances GTF durability through smart hot-section coating systems

Pratt & Whitney, part of RTX Corporation, is leveraging advanced coatings to stabilize its Geared Turbofan platform under the GTF Advantage program. The HS+ retrofit package, rolling out in early 2026, incorporates next-generation turbine blade coatings designed to nearly double time on wing. The company is expanding its GATORWORKS rapid prototyping unit to accelerate coating development for emerging defense and collaborative aircraft engines. Recent innovations include software-integrated coating management that dynamically adjusts climb thrust to prevent thermal overstress. High-performance coatings for the PW1100G-JM specifically address hot corrosion in polluted and saline environments.

Rolls-Royce bridges Trent engines to UltraFan® with durability-focused coating upgrades

Rolls-Royce is using coating innovation to transition from its Trent platform toward UltraFan® architectures. In late 2025, the company introduced the Trent 1000 XE build standard, delivering a 30% durability improvement in high-pressure turbines through Phase 1 coating upgrades. During 2026, Rolls-Royce expanded coating capacity at Dahlewitz and Singapore to support global XE retrofits. The company is also pioneering 100% Sustainable Aviation Fuel operation, requiring redesigned combustor coatings to manage altered heat profiles. Its Advance3 core integrates next-generation thermal barrier coatings enabling higher bypass ratios and materially improved fuel efficiency.

Chromalloy challenges OEM norms with advanced repair coatings and DER solutions

Chromalloy is the world’s leading independent provider of alternative engine parts and specialty repairs, frequently extending component life beyond OEM standards. In January 2026, new leadership accelerated the Chromalloy Value initiative, targeting up to 20% reductions in engine shop visit costs through advanced coatings and restorations. The company received FAA approval in February 2026 for its V2500 Select 8th Stage Compressor Blade featuring proprietary coatings for midlife maintenance. Chromalloy specializes in HPT blade restoration using DER-approved processes and operates a fully integrated supply chain spanning casting, forging, and coating to maintain strict airfoil gas-path quality.

PPG Aerospace expands chrome-free and heat-management coatings for engine structures

PPG Aerospace supplies engineered materials and specialty coatings for engine nacelles and internal components, complementing its airframe portfolio. Products such as Aerocron™ electrocoat primers and Desothane® HD basecoats are increasingly used to reduce weight and drag on engine housings. In 2026, PPG expanded investment in Solar Heat Management Coatings that reflect infrared radiation, lowering component temperatures on hot tarmacs. The company leads in transparent and chemically resistant coatings protecting sensors from jet fuel and de-icing fluids. Its chrome-free primer systems launched in late 2025 provide chromate-level corrosion resistance while supporting ECHA and EPA compliance.

United States: Large-Scale Capital Investment and Hot-Section Coating Leadership

The United States remains the largest and most technologically advanced market for aero engine coatings, supported by substantial capital expenditure and defense-driven demand. In March 2025, GE Aerospace announced nearly $1 billion in investments across its U.S. manufacturing and supply chain, including around $70 million allocated to a new Muskegon, Michigan facility dedicated to hot-section engine components that require advanced thermal barrier and environmental coatings. This investment strengthens domestic capability for next-generation widebody engines.

Production infrastructure has also scaled rapidly. Pratt & Whitney completed the ramp-up of its $1 billion turbine airfoil facility in Asheville, North Carolina, featuring a $285 million advanced casting foundry with automated systems for drilling and applying ceramic matrix composite coatings to GTF and F135 engine blades. Material innovation is delivering measurable gains. Boron nitride protective coatings integrated with silicon carbide matrices have reduced component weight by 66% versus titanium, enabling engines such as the GE9X to operate at temperatures roughly 500°C higher than prior generations. Regulatory momentum is accelerating change, as the EPA’s January 2025 amendment to National VOC Emission Standards is pushing coating formulators toward high-solids and waterborne systems. Defense spending reinforces demand, with $200 million allocated in 2025 to scale coating applications for T901 helicopter engines. Durability validation remains a benchmark, highlighted by GE Aerospace completing 1,600 hours of dust ingestion testing for GE9X thermal barrier coatings in late 2025.

United Kingdom Aero Engine Coatings Market: Durability Extension and Chrome-Free Coating Transition

The United Kingdom plays a strategic role in aero engine coatings through its focus on durability enhancement and environmentally safer technologies. In late 2025, Rolls-Royce launched a £1 billion durability enhancement program aimed at doubling the Time on Wing for Trent 1000 engines. Phase two of this program, entering service in early 2026, incorporates advanced coatings on combustor tiles and nozzle guide vanes to improve resistance to oxidation and thermal fatigue.

Research into extreme operating environments is a core differentiator. At Rolls-Royce’s Derby facility, engineers are validating sand-protection coatings designed to prevent blockage of cooling holes by fine dust encountered in Middle Eastern flight corridors. Supply chain modernization is also evident. In late 2025, Indestructible Paint received additional OEM approval for CFIPAL, a chrome-free diffusion coating for high-temperature turbine applications, accelerating the phase-out of hexavalent chromium. Sustainability leadership was recognized at the UK SEA Awards 2025, which highlighted process innovations that lower the carbon footprint of thermal spray operations. Technically, new coating-hole alignment techniques have enabled a 40% increase in turbine blade cooling efficiency by repositioning apertures within hair-width tolerances.

France Aero Engine Coatings Market: Industrial Scale-Up and Next-Generation Engine Architectures

France remains a core European center for aero engine coating production and innovation. The Ceramic Coating Center in Châtellerault, a joint venture between Safran Aircraft Engines and MTU Aero Engines, is undergoing a 3,000 square meter expansion that will double production capacity by late 2026. This expansion supports rising demand for advanced ceramic coatings across commercial and military platforms.

Infrastructure investment is reinforcing this role. In October 2025, Safran initiated construction of a $382 million aircraft engine complex that includes a dedicated facility for maintenance and coating repair of LEAP engines. Environmental performance is embedded in the design, with the CCC expansion expected to save around 1,800 tonnes of CO₂ equivalent annually through low-carbon construction materials and optimized materials management. France is also central to the RISE open-fan program, where radically new aerodynamic and thermal conditions require entirely new classes of heat-resistant and erosion-tolerant coatings. Supply chain localization extends beyond Europe, as Safran’s strategy has driven Moroccan aerospace exports to 26.4 billion dirhams in 2024 through localized component finishing and coating activities.

Canada Aero Engine Coatings Market: Accelerated Qualification and Academic-Industry Collaboration

Canada’s aero engine coatings ecosystem is distinguished by rapid qualification pathways and strong academic collaboration. In 2025, Pratt & Whitney Canada partnered with Concordia University on a $1.8 million ACTec project that fast-tracked a new aluminum-silicon abradable coating, reducing traditional qualification timelines from nearly ten years to under three. This breakthrough is particularly relevant for regional and business jet engines where time-to-market is critical.

Testing innovation underpins this progress. Researchers developed a custom tribological test rig that accurately simulates blade-to-casing friction, allowing early-stage screening of coatings designed to wear predictably during hard landings without damaging engine casings. Quebec’s aerospace strategy has amplified research output, with seven peer-reviewed publications in 2025 examining how hexagonal boron nitride enhances the performance and stability of AlSi-based abradable coatings. This academic-industrial synergy positions Canada as a leader in validation science rather than pure production scale.

Germany Aero Engine Coatings Market: MRO-Led Growth and Low-Emission Coating Processes

Germany’s aero engine coatings market is increasingly driven by maintenance, repair, and overhaul economics. MTU Aero Engines raised its 2025 revenue guidance to €8.6 to €8.8 billion, citing strong growth in spare parts and services where high-margin recoating activities are a key contributor. The growing installed base of Geared Turbofan engines is central to this trend.

Environmental targets are shaping process choices. MTU has committed to reducing Scope 1 and 2 emissions by 60% versus 2024 levels by 2035, necessitating adoption of more energy-efficient plasma spray and physical vapor deposition technologies. By 2026, GTF maintenance is expected to represent 40% of MTU’s commercial MRO revenue, driving sustained demand for advanced ceramic coatings that extend blade life and improve thermal efficiency. Germany’s position is therefore anchored in high-value recoating services rather than greenfield engine production.

Singapore Aero Engine Coatings Market: MRO Scale and Regional Coating Services Hub

Singapore has consolidated its role as a leading Asia-Pacific hub for aero engine coatings and MRO services. The Singapore Economic Development Board’s Aerospace Industry Transformation Map 2025 targets S$4.6 billion in value-add, with engine MRO and coating services identified as priority growth areas. This policy focus has translated into tangible capacity expansion.

By 2025, aerospace production levels in Singapore had surpassed pre-pandemic benchmarks, supported by the Seletar Aerospace Park ecosystem that hosts major engine OEMs, coating applicators, and specialized surface treatment providers. The concentration of capabilities enables rapid turnaround for high-value recoating and repair of turbine components, reinforcing Singapore’s attractiveness as a regional service base for widebody and narrowbody fleets operating across Asia.

Country-Level Positioning in the Aero Engine Coatings Industry

Aero Engine Coatings Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Competitive Impact

|

|

United States

|

Hot-section coatings, defense scale, CMC adoption

|

Global technology and volume leadership

|

|

United Kingdom

|

Durability extension, chrome-free systems

|

High-reliability and sustainable coatings

|

|

France

|

Ceramic coating scale, RISE program

|

Next-generation engine architecture support

|

|

Canada

|

Rapid qualification, abradable testing

|

Validation and materials science leadership

|

|

Germany

|

MRO-driven recoating, emission reduction

|

High-margin aftermarket dominance

|

|

Singapore

|

Engine MRO and regional services

|

Asia-Pacific coating services hub

|

Aero Engine Coatings Market Report Scope

Aero Engine Coatings market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$380.6 Million

|

|

Market Size (2034)

|

$654 Million

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Coating Type (Thermal Barrier Coatings, Abradable Coatings, Erosion Resistant Coatings, Corrosion Resistant Coatings, Anti Friction and Solid Lubricant Coatings, Diffusion Coatings), By Technology (Air Plasma Spray, High Velocity Oxy Fuel, Physical Vapor Deposition, Chemical Vapor Deposition, Cold Spray), By Material (Ceramics, Metals and Alloys, Polymers and Epoxies, Composites), By Component (Turbine Blades and Vanes, Combustion Chambers, Compressor Blades, Bearings and Shafts, Afterburners), By Engine Type (Turbofan, Turboshaft, Turbojet, Turboprop)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

GE Aerospace, Pratt and Whitney, Rolls Royce Holdings, Safran, MTU Aero Engines, AkzoNobel, PPG Industries, Praxair Surface Technologies, Oerlikon Balzers, IHI Corporation, Honeywell International, Lufthansa Technik, Indestructible Paint, Hentzen Coatings, Aero Engine Corporation of China

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aero Engine Coatings Market Segmentation

By Coating Type

- Thermal Barrier Coatings

- Abradable Coatings

- Erosion Resistant Coatings

- Corrosion Resistant Coatings

- Anti Friction and Solid Lubricant Coatings

- Diffusion Coatings

By Technology

- Air Plasma Spray

- High Velocity Oxy Fuel

- Physical Vapor Deposition

- Chemical Vapor Deposition

- Cold Spray

By Material

- Ceramics

- Yttria Stabilized Zirconia

- Rare Earth Pyrochlores

- Metals and Alloys

- MCrAlY

- Nickel Based Superalloys

- Polymers and Epoxies

- Composites

By Component

- Turbine Blades and Vanes

- Combustion Chambers

- Compressor Blades

- Bearings and Shafts

- Afterburners

By Engine Type

- Turbofan

- Turboshaft

- Turbojet

- Turboprop

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Aero Engine Coatings Industry

- GE Aerospace

- Pratt and Whitney

- Rolls Royce Holdings

- Safran

- MTU Aero Engines

- AkzoNobel

- PPG Industries

- Praxair Surface Technologies

- Oerlikon Balzers

- IHI Corporation

- Honeywell International

- Lufthansa Technik

- Indestructible Paint

- Hentzen Coatings

- Aero Engine Corporation of China

*- List not Exhaustive