Aerospace Coatings Market Size and Growth Anchored in High-Performance, Lightweight Aircraft Solutions

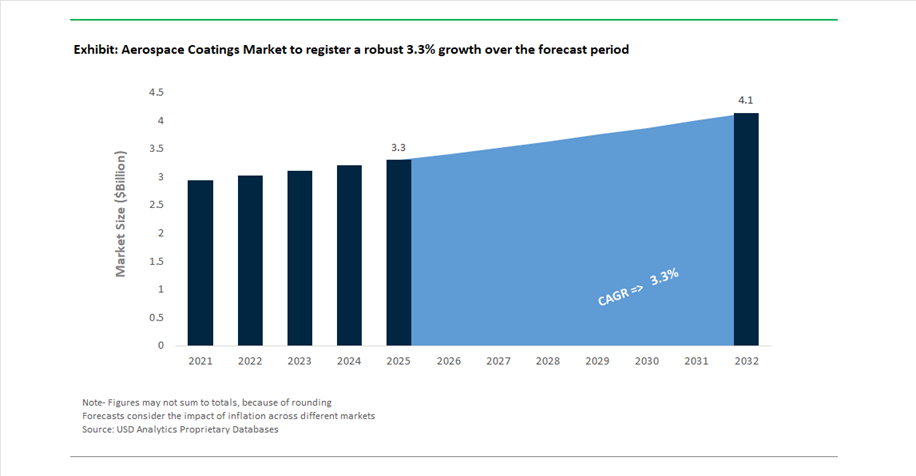

The Aerospace Coatings Market is projected to grow from USD 3.3 billion in 2025 to USD 4.1 billion by 2032, reflecting a CAGR of 3.3%. The market is supported by demand for high-value, technologically advanced formulations tailored for critical aerospace applications. The emphasis is more on performance optimization, regulatory compliance, and lifecycle efficiency.

Aerospace coatings continue to play a vital role in ensuring aircraft durability, safety, and operational efficiency. These coatings are engineered to provide extreme temperature resistance, UV protection, corrosion resistance, and lightning strike protection, all while contributing to weight reduction and fuel efficiency. As airlines and aircraft manufacturers intensify their focus on reducing carbon emissions and operating costs, lightweight coating systems with high solids and low-density formulations are gaining traction. Even marginal weight reductions achieved through advanced coatings can translate into significant fuel savings over an aircraft’s lifecycle.

The market is further supported by rising global air traffic, fleet expansion, and increasing MRO (Maintenance, Repair, and Overhaul) activities, particularly in Asia-Pacific and the Middle East. Demand is also being driven by the production ramp-up of next-generation aircraft platforms, including narrow-body and regional jets. Additionally, stringent environmental regulations, especially in Europe and North America, are accelerating the transition toward chromium-free, low-VOC, and REACH-compliant coating systems.

Technological evolution is centered on multi-functional coatings, integrating properties such as anti-static behavior, erosion resistance, and thermal stability, alongside improved aesthetics such as high gloss retention and color durability. The competitive landscape is characterized by strong OEM relationships, regulatory certifications, and continuous R&D investment, making aerospace coatings one of the most technically demanding segments within the global coatings industry.

Strategic Consolidation, Regulatory Milestones, and Digital Innovation Reshaping Aerospace Coatings Market

The aerospace coatings market is undergoing a transformation driven by strategic mergers, regulatory advancements, and next-generation product innovation. Regulatory approvals and geographic expansion are playing a critical role in market penetration. AkzoNobel secured extended approval from the Civil Aviation Administration of China (CAAC), enabling broader participation in China’s domestic aviation ecosystem, particularly supporting the COMAC C919 program. The company also expanded its technical support and distribution network in the Middle East, targeting rapidly growing aviation hubs and MRO facilities that require fast turnaround and high-performance coating solutions.

Innovation remains central to competitive differentiation. Indestructible Paint’s chromium-free coating technology represents a significant step toward environmentally compliant aerospace coatings, meeting stringent UK and EU REACH standards while maintaining high-temperature oxidation resistance. Similarly, Sherwin-Williams’ SKYscapes® basecoat-clearcoat systems, highlighted in its December 2024 aerospace color visualizer launch, deliver faster drying times and enhanced gloss retention, critical for both commercial and military aircraft applications.

Digital transformation is also emerging as a key trend. PPG Industries showcased advancements in digital monitoring for electrocoat (e-coat) systems, enabling real-time quality control and improved material efficiency during coating processes. This aligns with broader industry efforts to integrate smart manufacturing and predictive maintenance technologies into aerospace production and servicing.

Strategic initiatives from manufacturers are further accelerating market evolution. Hempel’s Hempafire Extreme for enhanced safety and performance. Meanwhile, Mankiewicz’s recognition at Airbus’ 2025 SQIP awards highlights the growing importance of digital supply chain integration and quality optimization in aerospace coatings delivery.

Additionally, customization and aesthetic innovation are gaining importance, as demonstrated by AkzoNobel’s multi-color coating achievement on the COMAC C919 (November 2025), showcasing the ability to deliver complex, high-performance finishes for modern aircraft. Leadership movements, such as Indestructible Paint’s February 2026 appointment of new sales leadership, further indicate strategic expansion into high-growth regions like Asia-Pacific.

Elimination of Hexavalent Chromium Reshaping Aerospace Primer Technologies

The aerospace coatings industry is undergoing a fundamental shift as global regulatory authorities mandate the elimination of hexavalent chromium (Cr6+) from primer systems. Driven by stringent frameworks such as REACH under the European Chemicals Agency (ECHA), this transition is redefining corrosion protection standards for aluminum airframes and structural components. Hexavalent chromium, long valued for its superior corrosion inhibition properties, is being phased out due to its carcinogenic classification and associated environmental hazards.

The regulatory impact is substantial. ECHA estimates that the restriction on Cr(VI) substances will prevent approximately 17 tonnes of chromium emissions annually across the European Union, significantly reducing environmental contamination in aerospace manufacturing and maintenance ecosystems. From a human health perspective, the transition to chrome-free primers is projected to prevent up to 195 cancer cases per year among aerospace technicians, translating into societal cost savings ranging from €331 million to €1.07 billion over a 20-year horizon.

Technologically, the industry has made notable progress in developing viable alternatives. Magnesium-rich and lithium-based primer systems have achieved performance parity with legacy chromated coatings, delivering salt-spray resistance exceeding 3,000 hours without relying on hazardous heavy metals. This advancement is critical for maintaining structural integrity and long-term durability in harsh operating environments. Reflecting the urgency of this transition, approximately 40% of aerospace chemical R&D budgets in 2025 have been allocated toward validating non-chromate coatings and ensuring compatibility with legacy aircraft materials and surface preparation processes.

This regulatory-driven innovation cycle is reshaping supplier strategies and accelerating the adoption of environmentally compliant coating technologies, positioning chrome-free systems as the new industry benchmark for corrosion protection in aerospace applications.

Next-Generation Radar-Absorbing Coatings Advancing Stealth and Thermal Performance

The evolution of modern military aviation is driving rapid advancements in radar-absorbing materials (RAM), positioning aerospace coatings at the forefront of stealth technology innovation. Fifth-generation fighter programs and next-generation bomber platforms require coatings that can deliver broadband electromagnetic absorption while withstanding extreme aerodynamic and thermal stresses encountered during high-speed flight.

Epoxy-based RAM formulations are emerging as the dominant material platform, expected to capture approximately 36% of the resin market share in stealth coating applications by late 2026. Their superior adhesion properties and ability to accommodate high filler loading make them ideal for integrating advanced conductive materials such as carbon nanotubes and graphene. These nanostructured coatings are achieving reflection loss values of -20 dB or greater across multiple frequency bands, including X, S, and L bands, enabling comprehensive radar signature reduction.

In parallel, advancements in application technology are improving maintainability and lifecycle efficiency. Sprayable RAM systems are replacing earlier adhesive-backed tile approaches, reducing repair and maintenance time by approximately 30%. This shift enhances operational readiness while lowering maintenance complexity for stealth aircraft fleets. Additionally, high-performance polyimide-based RAM coatings are demonstrating the ability to retain radar-cross-section (RCS) reduction properties even after prolonged exposure to surface temperatures exceeding 250°C during supersonic flight conditions.

Ice-Phobic Nano-Coatings Enhancing Passive Ice Protection and Flight Efficiency

The increasing adoption of Passive Ice Protection (PIP) systems is creating a high-growth opportunity for ice-phobic nano-coatings in the aerospace sector. These advanced coatings are designed to reduce ice adhesion on critical surfaces such as engine nacelles and wing leading edges, complementing or partially replacing traditional active anti-icing systems based on bleed air or electro-thermal heating.

Experimental data from wind tunnel testing indicates that superhydrophobic coatings (SHC) applied to nacelle lip skins can reduce ice accumulation thickness by up to 49% at temperatures around -12°C. This reduction significantly lowers the risk of ice ingestion into engines, enhancing operational safety. Additionally, by preserving smooth aerodynamic profiles, ice-phobic coatings help mitigate the 5% to 10% increase in fuel consumption typically associated with ice-induced drag, delivering measurable efficiency gains for both commercial and military aircraft.

From an engineering perspective, the integration of passive coatings reduces reliance on energy-intensive active systems, lowering power consumption by up to 30%. This enables the use of smaller and lighter electrical systems, which is particularly advantageous in next-generation composite airframes where weight optimization is critical. Commercial aviation is expected to dominate adoption, accounting for nearly 60% of end-use demand, as airlines seek to reduce maintenance costs and improve reliability in cold-weather operations.

Thermal Barrier and Environmental Coatings Enabling Hydrogen-Powered Aviation

The transition toward hydrogen-powered aircraft is introducing unprecedented thermal and chemical challenges, creating a significant opportunity for advanced high-temperature ceramic coatings. Hydrogen combustion generates flame temperatures reaching up to 2,100°C, substantially higher than conventional aviation fuels, necessitating the development of next-generation thermal barrier coatings (TBCs) capable of withstanding extreme heat flux.

Rare-earth zirconate materials, such as gadolinium zirconate, are emerging as leading candidates for hydrogen-compatible TBC systems due to their thermal conductivity, which is approximately 20% lower than that of traditional yttria-stabilized zirconia (YSZ). This improved insulation capability is critical for protecting turbine components and maintaining engine efficiency under high-temperature operating conditions. Additionally, the increased water vapor content in hydrogen combustion environments accelerates oxidation and degradation of ceramic matrix composites (CMCs), driving demand for specialized environmental barrier coatings (EBCs) that prevent material recession and extend component lifespan.

From a structural perspective, advanced thin-film ceramic coatings are enabling the use of lighter materials such as nickel-based superalloys and CMCs, supporting the aerospace industry’s goal of achieving up to 25% weight reduction to offset the mass of hydrogen storage systems. Furthermore, the development of calcia-magnesia-alumina-silica (CMAS) resistant coatings is enhancing durability by preventing molten debris infiltration, effectively doubling the service life of turbine blades in extreme environments.

Aerospace Coatings Market Share by Aviation Sector in 2025: Commercial Aviation Drives Volume and Innovation

Commercial Aviation Dominance Fueled by Narrowbody Production and MRO Repainting Cycles

The aerospace coatings market by aviation sector in 2025 is led by commercial aviation, accounting for 53.00% market share, driven by the unprecedented production rates of Airbus A320neo and Boeing 737 MAX aircraft and a robust maintenance, repair, and overhaul (MRO) repainting cycle. With over 1,400 commercial aircraft deliveries expected in 2025, and each aircraft requiring approximately 80–120 gallons of primer and polyurethane topcoat, this segment forms the backbone of global coating demand. Additionally, commercial aviation is spearheading the transition toward chrome-free aerospace coatings, as regulatory frameworks such as REACH and EPA guidelines phase out strontium chromate primers, accelerating innovation in lithium silicate and zirconium-based corrosion inhibitors. The increasing complexity of airline branding is also elevating demand for high-solids basecoat/clearcoat systems, particularly in multi-stripe livery designs, making this segment the primary driver of both volume consumption and high-value coating technologies in the aerospace industry.

Aerospace Coatings Market Share by Substrate in 2025: Aluminum Alloys Remain the Core Revenue Generator

Aluminum & Aluminum Alloys Lead Due to Legacy Fleet Maintenance and Corrosion Protection Needs

The aerospace coatings market by substrate in 2025 is dominated by aluminum and aluminum alloys, holding 48.00% market share, primarily due to the extensive global fleet of over 25,000 in-service aircraft, which still rely heavily on aluminum structures. Despite the growing adoption of composite materials in next-generation aircraft like Boeing 787 and Airbus A350, aluminum remains critical for wing structures, landing gear components, and fuselage elements, particularly alloys such as 2024 and 7075, which are highly susceptible to exfoliation and filiform corrosion. This sustains strong demand for epoxy polyamide primers, anodize sealers, and corrosion-resistant aerospace coatings. Moreover, specialized applications such as fuel tank coatings in integral wing tanks represent a high-value sub-segment, requiring advanced formulations that resist microbial growth and jet fuel exposure. This reinforces aluminum substrates as the largest contributor to aerospace coatings revenue and technology innovation in 2025.

Aerospace Coatings Market Competitive Landscape Led by Lightweight Technologies and OEM Integration

The aerospace coatings market is driven by lightweight coating systems, chromate-free formulations, and high-performance polyurethane and epoxy technologies. Key players are focusing on OEM integration, MRO efficiency, sustainability, and advanced coating systems to enhance aircraft durability, fuel efficiency, and lifecycle performance.

PPG Industries dominates aerospace coatings with electrocoat innovation and OEM integration

PPG Industries holds 20% of the global aerospace coatings market, supported by strong OEM partnerships and advanced coating technologies. The company reported $15.9 billion in net sales in 2025, with the aerospace segment contributing significantly to growth. Its PPG AEROCRON™ electrocoat primer system delivers 100% coverage on complex aircraft components through a dip-tank process while reducing coating weight by up to 30%. Sustainably advantaged coatings account for 43% of total sales, supported by continuous R&D investments funded through its $1.4 billion capital allocation program. PPG operates more than 16 Aerospace Application Support Centers globally, enabling localized technical services and rapid-response solutions for MRO operations. Its portfolio focuses on lightweight coatings, corrosion protection, and high-performance aerospace finishing systems.

AkzoNobel strengthens aerospace refinish leadership with chromate-free and time-saving systems

AkzoNobel commands a significant market share in aerospace coatings, driven by strong performance in commercial and business jet refinish segments. The company advanced its proposed merger with Axalta Coating Systems in 2026, targeting expanded distribution and R&D capabilities in aerospace and automotive refinish coatings. It reported €1.44 billion in adjusted EBITDA in 2025, supported by €98 million in cost efficiencies across high-performance coatings operations. Sustainability initiatives include a 27% reduction in non-recovered waste, supporting the adoption of chromate-free primers aligned with regulatory standards in Europe and North America. The Aerodur Professional coating system reduces application time by 25% compared to traditional high-solids systems, improving operational efficiency for MRO facilities. Product innovation continues to focus on compliant, high-performance aerospace coatings.

Sherwin-Williams expands global aerospace coatings presence with fast-dry polyurethane systems

Sherwin-Williams is expanding its aerospace coatings footprint across military and general aviation segments through high-performance polyurethane coatings. Its Jet Glo Express™ and SKYscapes® systems are recognized for fast-dry technology, enabling MRO facilities to increase throughput by 15–20%. The company strengthened global engagement through trade initiatives and partnerships with over 5,000 aircraft paint facilities. In 2025, it introduced an Aircraft Color Visualizer tool that enables real-time simulation of 2K acrylic and polyurethane coatings for design optimization. Vertical integration in resin production ensured stable pricing for polyurethane topcoats, which account for nearly 60% of aerospace coatings demand, despite raw material volatility. Product development focuses on efficiency, durability, and aesthetic performance in aerospace applications.

Mankiewicz leads aircraft interior coatings with advanced aesthetic and functional surfaces

Mankiewicz Gebr. & Co. specializes in high-end aerospace coatings for cabin interiors and executive jet exteriors, with a strong emphasis on design and functionality. Its ALEXIT® product range delivers anti-glare, scratch-resistant, and flame-retardant coatings that meet FAR/JAR 25.853 fire safety standards. The company introduced its “Colors of the Year 2026” palette, reflecting evolving design trends using advanced pigment technologies. Expansion of its Functional Surface laboratory in Hamburg in 2025 supports development of anti-microbial coatings for high-touch cabin environments. Strategic collaborations with seat and galley manufacturers enable integrated coating systems that reduce cabin interior weight by up to 5%. Innovation efforts remain focused on combining aesthetics with performance and safety compliance.

IHI Ionbond advances aerospace engine coatings with high-temperature thin-film technologies

IHI Ionbond operates in the high-tech aerospace coatings segment, focusing on PVD and CVD thin-film coatings for engine components and critical parts. In 2025, the company expanded its global footprint across seven key hubs, including Toulouse and the United States, to support demand for advanced engine coatings. The Ionbond™ 357 duplex coating was introduced for extreme forging and high-temperature turbine applications, addressing next-generation engine requirements. Its metallurgical coatings extend component lifespan by up to 40%, contributing to reduced maintenance cycles and lower CO2 emissions. Recognition through the Bosch Global Supplier Award in 2025 highlights its role in high-performance materials and industrial supply chains. Product innovation continues to target durability, efficiency, and thermal resistance in aerospace propulsion systems.

United States Aerospace Coatings Market: Automation-Driven Capacity Expansion and MRO Sector Surge

The United States aerospace coatings market is undergoing rapid transformation, driven by advanced manufacturing automation and the expansion of Maintenance, Repair, and Operations (MRO) infrastructure. Major capacity upgrades, including the modernization of large-scale aerospace coating facilities, are enhancing production efficiency through automated batching systems and high-speed processing technologies. Simultaneously, the expansion of widebody aircraft hangars is strengthening the country’s position as a global MRO hub, supporting rising demand for aircraft repainting and refurbishment services.

Technological advancements are accelerating innovation across the aerospace coatings value chain. The deployment of rapid service units for localized coating supply is reducing turnaround times for specialized 2K polyurethane topcoats, while the introduction of chrome-free, waterborne primers is enabling compliance with stringent environmental regulations. Increasing demand for radar-absorbent coatings and stealth technologies, particularly in defense programs, is further driving market growth. Additionally, strict enforcement of low-VOC standards is reshaping formulation strategies, pushing manufacturers toward sustainable, high-performance aerospace coatings solutions.

France Aerospace Coatings Market: Eco-Compliant Innovations and Airbus-Led Services Expansion

France stands as a key European hub for aerospace coatings, supported by strong government initiatives and a thriving aerospace services ecosystem. Investments under national innovation programs are accelerating the development of bio-based coating materials, reducing reliance on fossil-derived inputs and enhancing sustainability across the value chain. The expansion of aircraft maintenance and repainting services, particularly around major aerospace clusters, is driving sustained demand for high-performance coating solutions.

Technological advancements are transforming coating application processes, with the adoption of direct-to-metal systems eliminating traditional primer layers and reducing overall aircraft weight. Regulatory leadership in Europe is also accelerating the transition to environmentally compliant formulations, including the phase-out of hazardous substances. In addition, innovations such as nanotechnology-based anti-static coatings and laser-based stripping techniques are improving operational efficiency while aligning with decarbonization goals, positioning France as a leader in next-generation aerospace coatings technologies.

China Aerospace Coatings Market: Domestic Aircraft Production and Green Coating Infrastructure

China’s aerospace coatings market is expanding rapidly, fueled by the commercialization of domestic aircraft programs and investments in localized production capabilities. The scaling of aircraft manufacturing, particularly for narrowbody and regional jets, is generating strong demand for epoxy primers and high-gloss polyurethane finishes produced within the country. This shift toward domestic self-sufficiency is reducing reliance on imported coating technologies and strengthening the local supply chain.

Infrastructure investments, including the development of environmentally advanced paint facilities, are supporting the transition toward sustainable coating practices. The integration of robotic spray systems is improving application precision and reducing material waste, while government-led initiatives are promoting the use of solvent-free and eco-friendly coatings. Innovations such as anti-icing coatings and advanced materials for aircraft interiors are further enhancing performance and safety standards, reinforcing China’s growing influence in the global aerospace coatings market.

India Aerospace Coatings Market: MRO Growth and Government-Led Localization Initiatives

India’s aerospace coatings market is gaining momentum, driven by expanding MRO infrastructure and strong government support for domestic manufacturing. Policy initiatives aimed at boosting local production of aerospace components are encouraging the development of advanced coating technologies within the country. The establishment of new MRO facilities is positioning India as a regional hub for aircraft maintenance and repainting services, catering to both domestic and international fleets.

Innovation is playing a critical role in addressing the unique demands of aerospace applications. The development of high-temperature-resistant coatings for military aircraft and the adoption of UV-curable systems for interior refurbishments are improving operational efficiency and reducing downtime. Additionally, increased airport modernization efforts are driving demand for durable industrial coatings in hangars and maintenance facilities. Simplified regulatory processes are further enabling new entrants to participate in the aerospace coatings supply chain, accelerating market growth.

Germany Aerospace Coatings Market: Smart Coatings and Hydrogen-Ready Material Development

Germany’s aerospace coatings market is characterized by its focus on sustainability, advanced material science, and digital innovation. The development of self-healing coatings and 3D-printed coating technologies is enhancing durability and performance, particularly in high-stress aerospace components. These innovations are enabling predictive maintenance and extending the lifespan of critical aircraft systems.

Regulatory leadership is also shaping the market, with initiatives promoting transparency in chemical usage and lifecycle impact. Significant investments in hydrogen-compatible coatings are supporting the transition toward zero-emission aircraft technologies. Additionally, demand for high-performance interior coatings with antimicrobial and fire-retardant properties is growing, driven by fleet modernization programs. Innovations such as infrared-reflective coatings are further contributing to energy efficiency and passenger comfort, positioning Germany at the forefront of sustainable aerospace coatings development.

Canada Aerospace Coatings Market: Business Jet Finishing Excellence and Climate-Adapted Coatings

Canada’s aerospace coatings market is driven by its leadership in business jet manufacturing and specialized coating applications. Expansions in high-end aircraft finishing facilities are supporting increased demand for premium coatings that deliver superior aesthetics and performance. Advanced application technologies, including electrostatic spray systems, are enabling highly efficient coating processes and achieving the high-quality finishes required in private aviation.

Innovation is also focused on adapting coatings to extreme environmental conditions. The development of low-temperature curing primers is enabling efficient operations in colder climates, while impact-resistant coatings are essential for aircraft operating on challenging terrains. Infrastructure investments in aerospace hubs and the adoption of eco-friendly stripping technologies are further strengthening the market. Cross-border regulatory alignment is ensuring seamless integration with global supply chains, enhancing Canada’s competitiveness in the aerospace coatings sector.

Japan Aerospace Coatings Market: Hydrogen Aviation and Nano-Material Coating Technologies

Japan’s aerospace coatings market is advancing through its focus on next-generation aviation technologies and material innovation. Strategic developments in hydrogen-resistant coatings are supporting the transition toward hydrogen-powered aircraft, addressing the need for durability under extreme storage and operating conditions. These innovations are critical for enabling the future of sustainable aviation.

The integration of nano-materials, including carbon nanotube-based coatings, is enhancing electromagnetic shielding and overall aircraft performance. Additionally, the development of low-drag surface coatings is improving fuel efficiency by reducing aerodynamic resistance. Demand for cryogenic insulation coatings is also increasing, driven by the country’s involvement in space exploration programs. Government-backed sustainability initiatives and regulatory updates are further accelerating the adoption of environmentally compliant coating solutions, reinforcing Japan’s leadership in advanced aerospace coatings technologies.

Aerospace Coatings Market Report Scope

Aerospace Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.3 Billion

|

|

Market Size (2032)

|

$4.1 Billion

|

|

Market Growth Rate

|

3.3%

|

|

Segments

|

By Resin (Polyurethane (PU), Epoxy, Acrylics, Silicone, Fluoropolymers, Specialized Hybrids)), By Coating Technology (Solvent-borne, Water-borne, Powder Coatings)), By Aviation Sector (Commercial Aviation, Military & Defense, General Aviation, Helicopters / Rotary Wing, Space & Satellite)), By Function (Corrosion Protection, Erosion & Abrasion Resistance, Thermal Management, Stealth & EMI/RFI Shielding, Aesthetic & Branding)), By Substrate (Aluminum & Aluminum Alloys, Composite Materials, Titanium & Steel Alloys, Interior Thermoplastics & Honeycomb Structures)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, Axalta Coating Systems Ltd., BASF SE, Henkel AG & Co. KGaA, 3M Company, Hempel A/S, Mankiewicz Gebr. & Co., Jotun A/S, Socomore, Hentzen Coatings, Inc., IHI Ionbond AG, Kansai Paint Co., Ltd., International Aerospace Coatings

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aerospace Coatings Market Segmentation

By Resin

- Polyurethane (PU)

- Epoxy

- Acrylics

- Silicone

- Fluoropolymers

- Specialized Hybrids

By Coating Technology

- Solvent-borne

- Water-borne

- Powder Coatings

By Aviation Sector

- Commercial Aviation

- Military & Defense

- General Aviation

- Helicopters / Rotary Wing

- Space & Satellite

By Function

- Corrosion Protection

- Erosion & Abrasion Resistance

- Thermal Management

- Stealth & EMI/RFI Shielding

- Aesthetic & Branding

By Substrate

- Aluminum & Aluminum Alloys

- Composite Materials

- Titanium & Steel Alloys

- Interior Thermoplastics & Honeycomb Structures

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Aerospace Coatings Market

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- BASF SE

- Henkel AG & Co. KGaA

- 3M Company

- Hempel A/S

- Mankiewicz Gebr. & Co.

- Jotun A/S

- Socomore

- Hentzen Coatings, Inc.

- IHI Ionbond AG

- Kansai Paint Co., Ltd.

- International Aerospace Coatings

*- List not Exhaustive

Table of Contents: Aerospace Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Aerospace Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Aerospace Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Growth Drivers: Lightweight Coatings and Fuel Efficiency Optimization

2.4. Regulatory Compliance and Transition to Low-VOC and Chromium-Free Systems

2.5. Fleet Expansion, MRO Growth, and Next-Generation Aircraft Demand

3. Innovations Reshaping the Aerospace Coatings Market

3.1. Trend: Strategic Consolidation, Regulatory Milestones, and Digital Innovation

3.2. Trend: Elimination of Hexavalent Chromium and Chrome-Free Primer Technologies

3.3. Opportunity: Radar-Absorbing Coatings and Ice-Phobic Nano-Coatings

3.4. Opportunity: Thermal Barrier Coatings for Hydrogen-Powered Aviation

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Aerospace Coatings Market

5.1. By Resin

5.1.1. Polyurethane (PU)

5.1.2. Epoxy

5.1.3. Acrylics

5.1.4. Silicone

5.1.5. Fluoropolymers

5.1.6. Specialized Hybrids

5.2. By Coating Technology

5.2.1. Solvent-borne

5.2.2. Water-borne

5.2.3. Powder Coatings

5.3. By Aviation Sector

5.3.1. Commercial Aviation

5.3.2. Military & Defense

5.3.3. General Aviation

5.3.4. Helicopters / Rotary Wing

5.3.5. Space & Satellite

5.4. By Function

5.4.1. Corrosion Protection

5.4.2. Erosion & Abrasion Resistance

5.4.3. Thermal Management

5.4.4. Stealth & EMI/RFI Shielding

5.4.5. Aesthetic & Branding

5.5. By Substrate

5.5.1. Aluminum & Aluminum Alloys

5.5.2. Composite Materials

5.5.3. Titanium & Steel Alloys

5.5.4. Interior Thermoplastics & Honeycomb Structures

6. Country Analysis and Outlook of Aerospace Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Aerospace Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Aerospace Coatings Market Size Outlook to 2032

7.1.1. By Resin

7.1.2. By Coating Technology

7.1.3. By Aviation Sector

7.1.4. By Function

7.1.5. By Substrate

7.2. Europe Aerospace Coatings Market Size Outlook to 2032

7.2.1. By Resin

7.2.2. By Coating Technology

7.2.3. By Aviation Sector

7.2.4. By Function

7.2.5. By Substrate

7.3. Asia Pacific Aerospace Coatings Market Size Outlook to 2032

7.3.1. By Resin

7.3.2. By Coating Technology

7.3.3. By Aviation Sector

7.3.4. By Function

7.3.5. By Substrate

7.4. South America Aerospace Coatings Market Size Outlook to 2032

7.4.1. By Resin

7.4.2. By Coating Technology

7.4.3. By Aviation Sector

7.4.4. By Function

7.4.5. By Substrate

7.5. Middle East and Africa Aerospace Coatings Market Size Outlook to 2032

7.5.1. By Resin

7.5.2. By Coating Technology

7.5.3. By Aviation Sector

7.5.4. By Function

7.5.5. By Substrate

8. Company Profiles: Leading Players in the Aerospace Coatings Market

8.1. PPG Industries, Inc.

8.2. Akzo Nobel N.V.

8.3. The Sherwin-Williams Company

8.4. Axalta Coating Systems Ltd.

8.5. BASF SE

8.6. Henkel AG & Co. KGaA

8.7. 3M Company

8.8. Hempel A/S

8.9. Mankiewicz Gebr. & Co.

8.10. Jotun A/S

8.11. Socomore

8.12. Hentzen Coatings, Inc.

8.13. IHI Ionbond AG

8.14. Kansai Paint Co., Ltd.

8.15. International Aerospace Coatings

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures