Aircraft Paint Market Size and Growth Driven by Fleet Expansion and High-Performance Coating Demand

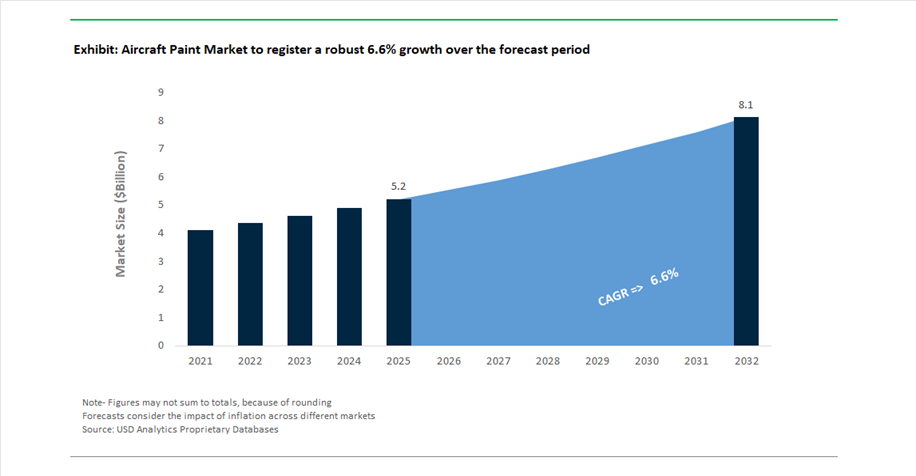

The Aircraft Paint Market is projected to expand from USD 5.2 billion in 2025 to USD 8.1 billion by 2032, registering a CAGR of 6.6%. This growth forecast is driven by increasing demand for advanced aircraft paint systems aligned with global fleet expansion, rising aircraft deliveries, and growing maintenance, repair, and overhaul (MRO) activities. Unlike conventional coatings, aircraft paints are engineered for extreme altitude conditions, aerodynamic efficiency, UV resistance, and long-term durability, making them a critical component of aircraft performance and lifecycle management.

A key market driver is the global surge in commercial aviation and private aircraft usage, particularly across Asia-Pacific and the Middle East. Airlines are prioritizing fuel efficiency and operational cost reduction, where modern paint systems contribute by reducing drag and minimizing aircraft weight. Innovations such as lightweight coating systems and high-solid, low-VOC formulations are enabling airlines to optimize fuel consumption while complying with environmental standards. Additionally, aircraft paints play a crucial role in protecting airframes from corrosion, temperature extremes, and atmospheric exposure, ensuring structural integrity over extended service periods.

The market is also witnessing strong momentum from OEM production backlogs and fleet modernization programs, particularly for next-generation aircraft such as fuel-efficient narrow-body jets. At the same time, branding and livery customization are becoming increasingly important, driving demand for coatings that deliver superior color retention, gloss stability, and aesthetic longevity. Sustainability trends are further accelerating the adoption of chrome-free primers, water-based coatings, and low-emission technologies, aligning with stringent regulatory frameworks such as REACH.

Technological advancements in coating chemistry, application techniques, and digital process monitoring are enhancing performance while reducing application time and maintenance cycles. Accordingly, the aircraft paint market is evolving toward high-efficiency, environmentally compliant, and performance-optimized coating systems, supported by strong collaboration between OEMs, coating manufacturers, and MRO service providers

Strategic Investments, OEM Partnerships, and Next-Generation Coating Technologies Transforming Aircraft Paint Market

The aircraft paint market is undergoing a structural shift driven by large-scale capital investments, strategic mergers, and continuous product innovation. Capacity expansion and supply chain strengthening are central to meeting rising demand. In April 2026, PPG Industries announced a $380 million investment in a new aerospace coatings manufacturing facility in North Carolina, one of the largest investments in its history. This facility is designed to support increasing demand from major OEMs such as Boeing and Lockheed Martin, reflecting strong growth in aircraft production and aftermarket services. Similarly, AkzoNobel’s €50 million expansion of its U.S. aerospace coatings facility (2025) is aimed at boosting production capacity for key product lines such as Alumigrip and Aviox, ensuring supply continuity in North America.

Product innovation is focused on performance optimization and sustainability compliance. AkzoNobel’s Aerobase NextGen system, developed for the Airbus A350, delivers 15% weight reduction, directly contributing to improved fuel efficiency while maintaining durability and color performance. In parallel, Sherwin-Williams’ chrome-free epoxy primer (June 2025) addresses stringent environmental regulations while preserving high corrosion resistance standards required in aviation. These innovations highlight the industry’s transition toward eco-efficient, high-performance coating solutions.

OEM partnerships and long-term contracts are further shaping market dynamics. PPG Aerospace’s multi-year agreement with Ryanair (July 2025) underscores the importance of high-solid, low-VOC coating systems that reduce downtime during MRO cycles and improve operational efficiency. Regional expansion strategies are also evident, with AkzoNobel’s Dubai facility launch (January 2026) enabling faster delivery of custom livery solutions and technical support across Middle Eastern aviation hubs.

Regulatory approvals and digital advancements are enhancing market penetration and operational efficiency. AkzoNobel’s CAAC approval extension in China (February 2026) strengthens its position in supporting domestic aircraft programs such as COMAC’s C919 and ARJ21. Meanwhile, Mankiewicz’s recognition for digitalization (June 2025) reflects growing adoption of digital material tracking and supply chain optimization technologies within aerospace coatings.

Strategic acquisitions are also reinforcing sustainability and innovation pipelines. Henkel’s January 2026 acquisition of ATP Adhesive Systems supports the integration of water-based, zero-VOC technologies into aerospace surface treatments, aligning with industry-wide environmental goals.

Mandatory VOC Reduction Driving Shift to Low-Emission Aircraft Paint Technologies

The aircraft paint industry is experiencing a regulatory-driven transformation as environmental agencies enforce stricter limits on Volatile Organic Compound (VOC) emissions. The U.S. EPA’s finalized amendments to the National VOC Emission Standards, effective January 17, 2025, alongside parallel actions from European regulators, have established new performance benchmarks for aerospace coatings. These regulations require manufacturers to reduce VOC levels to below 250 g/L for topcoats and 350 g/L for primers, significantly constraining the use of traditional solvent-borne chemistries.

This regulatory tightening has triggered a notable surge—approximately 20%—in R&D investment focused on water-reducible, high-solids, and low-reactivity acrylic-urethane formulations. As compliance deadlines aligned with Clean Air Act updates roll through 2025–2026, nearly 15% of legacy solvent-based product portfolios are being phased out or reformulated. The industry response has been technologically robust, with next-generation low-VOC aircraft coatings achieving approximately 98% performance parity with conventional systems in critical metrics such as Skydrol fluid resistance and UV durability. This milestone addresses historical concerns regarding chemical resistance and long-term weatherability.

In parallel, sustainability considerations are extending beyond emissions control into raw material sourcing. By 2026, biodegradable paint systems and eco-chemistry binders account for around 12% of new product introductions in commercial aviation coatings, signaling a broader shift toward lifecycle sustainability. These developments are redefining competitive dynamics, where compliance, environmental performance, and durability must be delivered simultaneously, positioning low-VOC aircraft coatings as the new industry baseline.

Robotic Automation Redefining Aircraft Painting Efficiency and Cost Structures

Automation is rapidly transforming aircraft painting and stripping processes, traditionally among the most labor-intensive and time-consuming operations within Maintenance, Repair, and Overhaul (MRO) facilities. The integration of robotic autonomous systems—combining laser-based decoating with precision electrostatic spray technologies—is fundamentally altering productivity benchmarks across the industry.

Modern multi-axis robotic painting systems can complete a full narrow-body aircraft repaint in just 4 to 6 days, representing a 60% reduction compared to the 14 to 21 days typically required using manual methods. This dramatic improvement in turnaround time directly enhances aircraft availability and operational efficiency for airlines. Material utilization has also improved significantly. Robotic electrostatic application reduces paint waste to below 12%, compared to the 40%–60% overspray commonly observed in manual High Volume Low Pressure (HVLP) systems.

Precision is another critical advantage. AI-driven robotic systems maintain Dry Film Thickness (DFT) within a tolerance of ±2 microns relative to OEM specifications across the entire fuselage. This level of control minimizes excess coating weight, which directly impacts fuel efficiency due to reduced parasitic load. From a cost perspective, automation has reduced labor expenses per repaint cycle from approximately $55,000 to as low as $9,000–$18,000, enabling higher throughput and improved profitability for MRO operators.

Electroluminescent Coatings Enabling Lightweight and Aerodynamically Efficient Lighting Systems

Electroluminescent (EL) paint technology is emerging as a disruptive innovation in aircraft exterior systems, offering a functional alternative to conventional lighting assemblies such as logo lights and emergency egress indicators. By transforming the aircraft skin into an active light-emitting surface, EL coatings eliminate the need for bulky lighting fixtures, wiring systems, and protective housings.

This transition delivers measurable weight reduction benefits. EL paint systems, typically applied as ultra-thin layers under 0.5 mm thickness, can remove between 20 kg and 50 kg of traditional lighting hardware from the airframe. This reduction contributes directly to improved fuel efficiency, particularly on long-haul flights where weight savings accumulate into significant operational cost advantages. Additionally, the elimination of external lighting protrusions reduces aerodynamic drag, with studies indicating up to a 0.5% decrease in skin friction drag—further enhancing fuel economy.

From a durability standpoint, EL coatings offer superior resistance to vibration-induced failures, a common issue with conventional bulbs and LED systems. Current prototypes developed in 2026 demonstrate operational lifespans exceeding 10,000 hours before significant luminosity degradation occurs. Beyond efficiency, these coatings introduce safety enhancements. Integrated EL path-marking systems on aircraft exteriors provide high-visibility guidance during emergency evacuations in low-light conditions, without the risk of electrical sparking in fuel-sensitive environments.

Anti-Microbial Interior Coatings Enhancing Cabin Hygiene and Passenger Confidence

The growing emphasis on passenger health and cabin hygiene has transformed anti-microbial coatings from a niche application into a standard specification within aircraft interiors. Advanced coating systems incorporating silver-ion and copper nanoparticle technologies are now widely applied to high-contact surfaces, including tray tables, armrests, seatbacks, and overhead storage compartments.

Performance benchmarks for these coatings have advanced significantly. Next-generation anti-microbial formulations achieve a 99.9% reduction in common pathogens within two hours of surface contact, addressing both bacterial and viral contamination risks. Durability has also improved, with coatings engineered to withstand over 1,000 cleaning cycles using industrial-grade disinfectants without degradation in efficacy, ensuring long-term functionality in high-use environments.

From a market perspective, passenger perception is a key adoption driver. Surveys conducted in 2026 indicate that approximately 72% of frequent flyers prioritize airlines that publicly disclose the use of certified anti-microbial treatments, highlighting the role of hygiene as a differentiating factor in airline branding and customer retention. Operationally, the integration of these coatings is shifting upstream, with over 30% of new narrow-body aircraft deliveries in 2026 featuring factory-applied anti-microbial finishes. This transition from aftermarket retrofitting to line-fit installation reflects the growing importance of cabin wellness as a core design parameter.

Aircraft Paint Market Share by Paint Type in 2025: Polyurethane Coatings Dominate High-Performance Topcoat Applications

Polyurethane Paints Lead with Superior UV Resistance and High-Value Revenue Share

The aircraft paint market by paint type in 2025 is dominated by polyurethane paints, accounting for 44.00% market share, establishing themselves as the industry-standard topcoat for commercial aircraft fuselages. Specifically, 2K high-solids polyurethane coatings are universally mandated due to their exceptional UV resistance at cruising altitudes (35,000 ft), gloss retention, and resistance to Skydrol hydraulic fluid erosion, outperforming epoxy, acrylic, and enamel systems. While epoxy primers and polyurethane topcoats are typically applied at similar thickness levels, polyurethane commands a 50–70% higher price per gallon, resulting in an even stronger revenue share dominance (~60% of total aircraft paint spend). In 2025, the growing adoption of basecoat/clearcoat polyurethane systems for complex airline liveries is further amplifying demand, effectively increasing material consumption per aircraft. This positions polyurethane coatings as a cornerstone of advanced aerospace coating technologies, balancing performance, durability, and premium value in the global aviation sector.

Aircraft Paint Market Share by Aircraft Type in 2025: Narrow-Body Aircraft Drive Volume Demand and Efficiency Innovations

Narrow-Body Aircraft Segment Leads with High Production Rates and Cost Optimization Trends

The aircraft paint market by aircraft type in 2025 is led by narrow-body aircraft, holding 47.00% market share, fueled by the high production volumes of Airbus A320neo and Boeing 737 MAX families, which collectively exceed 100 aircraft per month. Despite larger aircraft like wide-bodies consuming more paint per unit, the sheer number of narrow-body deliveries and frequent 6-year repainting cycles during heavy maintenance checks make this segment the largest consumer of coating volumes globally. This segment is highly sensitive to material efficiency, weight reduction, and cost optimization, driving adoption of electrostatic paint application technologies that minimize overspray and waste. Notably, every 1 kg reduction in paint weight can save airlines approximately $1,000 in fuel costs, reinforcing demand for ultra-high solids, low-density polyurethane coatings. Additionally, the prevalence of white-dominant liveries (around 70%) has created strong demand for titanium dioxide (TiO2)-based polyurethane topcoats, ensuring long-term resistance to UV-induced yellowing and thermal stress.

Aircraft Paint Market Competitive Landscape Driven by Lightweight Coatings and MRO Efficiency

The aircraft paint market is shaped by lightweight coating technologies, fast-dry polyurethane systems, and chromate-free formulations. Leading players are enhancing OEM integration, expanding MRO capabilities, and advancing sustainable aviation coatings to improve aircraft performance, reduce turnaround time, and ensure long-term corrosion protection.

PPG Industries leads aircraft paint innovation with electrocoat primers and global MRO support

PPG Industries maintains a dominant position in the aircraft paint market through its multi-engine growth strategy and strong aerospace segment performance. The company reported record aerospace sales in 2025 within its $15.9 billion total revenue, supported by a 19% EBITDA margin in the segment. In February 2025, PPG expanded its aerospace coatings facility in Georgia, U.S., to support high-volume contracts with Boeing and the U.S. Air Force. Its PPG AEROCRON™ electrocoat primer utilizes a chrome-free, water-based dip process that reduces aircraft weight by up to 30% compared to traditional spray systems. The company operates more than 16 Aerospace Application Support Centers globally, delivering localized expertise and just-in-time mixing for MRO operations. Product development continues to emphasize lightweight coatings, corrosion resistance, and operational efficiency.

AkzoNobel strengthens aircraft paint production with facility upgrades and sustainable coatings

AkzoNobel continues to expand its aircraft paint capabilities through operational excellence and large-scale manufacturing investments. The company announced a €50 million upgrade to its Waukegan, Illinois facility in late 2025, adding automation and a rapid-service unit for the MRO segment. It is advancing toward a proposed merger with Axalta Coating Systems in 2026, expected to generate $600 million in cost synergies across aerospace coatings and refinish markets. The Aerodur® Professional basecoat/clearcoat system reduces application time by 25% while maintaining high UV resistance and chemical durability. Sustainability initiatives include a 27% reduction in non-recovered waste compared to 2017, with nearly 40% of its portfolio classified as eco-friendly or low-VOC. Innovation continues to focus on compliant, high-performance aircraft coatings.

Sherwin-Williams expands aircraft paint applications with fast-dry polyurethane systems

Sherwin-Williams leverages its extensive North American distribution network to lead in general aviation and military aircraft paint segments. The company operates within a $23 billion+ revenue base, with aerospace coatings benefiting from infrastructure investments in airport and hangar upgrades. Its Aircraft Color Visualizer tool enables real-time simulation of SKYscapes® and Jet Glo Express™ finishes, accelerating livery design and approval processes. Vertical integration in resin supply ensures stable lead times for polyurethane topcoats, which account for 48% of the aircraft paint market, despite raw material volatility. The company’s focus on fast-dry coating systems allows MRO facilities to increase hangar throughput by 15–20%. Product development aligns with efficiency, durability, and high-performance coating requirements.

Mankiewicz delivers high-end aircraft paint systems with long-term structural protection

Mankiewicz Gebr. & Co. specializes in premium aircraft paint solutions for cabin interiors and exterior finishes, emphasizing aesthetics and durability. The company supplies coatings across ALEXIT® FST interior systems, exterior basecoat/clearcoat technologies, and structural component coatings. Its BaseCoat/ClearCoat systems are applied on more than 3,000 aircraft globally, utilizing advanced spraying techniques to enhance color stability and application speed. The introduction of 2026 coating concepts includes anti-microbial cabin coatings and new pigment technologies designed to improve passenger comfort and visual appeal. Its SEEVENAX structural coatings provide corrosion protection exceeding 30 years, supporting long lifecycle aircraft assets. Product innovation continues to combine design-driven performance with long-term protection.

Hempel expands aircraft paint footprint with decarbonization strategy and emerging market focus

Hempel A/S is strengthening its position in the aircraft paint market through its “Accelerate to Win” strategy launched in 2026. The company reported €259 million in free cash flow in 2025 with an adjusted EBITDA margin of 18.2%, supporting expansion initiatives in aerospace coatings. Leadership restructuring in marine and strategy divisions aligns with growing demand for decarbonized coatings in transportation sectors. The company is adapting its Hempaguard NB technology for aerospace drag-reduction trials, targeting improved fuel efficiency in aircraft applications. Geographic expansion includes a new office in Pune, India, supporting demand in the APAC region driven by frequent repainting cycles of narrow-body aircraft. Product development focuses on performance efficiency and sustainability in aircraft coating technologies.

United States Aircraft Paint Market: Shelby Mega Facility and Chromate-Free Transition Accelerating Innovation

The United States aircraft paint market is witnessing significant growth, driven by large-scale manufacturing expansions and a rapid transition toward environmentally compliant coating technologies. A major investment in a new aerospace coatings facility in North Carolina is centralizing production capabilities for advanced sealants and aircraft paints, strengthening supply chain efficiency for OEMs across North America. Simultaneously, infrastructure expansion in aircraft painting hangars equipped with semi-autonomous robotic systems is enhancing coating precision and reducing material waste.

Technological advancements are redefining aircraft paint performance and application efficiency. The adoption of basecoat-clearcoat (BCCC) systems is reducing painting time and aircraft weight, delivering both operational and fuel efficiency benefits. Regulatory pressure from stricter emission standards is accelerating the shift toward waterborne and high-solid primers, while innovations such as carbon-nanotube anti-static coatings are enhancing aircraft safety and performance. Additionally, the growing use of infrared-reflective topcoats in military fleets is improving thermal management and reducing operational costs, reinforcing the United States’ leadership in advanced aircraft paint technologies.

France Aircraft Paint Market: Toulouse Cluster Expansion and REACH-Compliant Coating Leadership

France has emerged as a central hub in the global aircraft paint market, supported by strategic expansions and strong regulatory leadership. The consolidation of aircraft painting facilities in Toulouse has created one of the highest-density aerospace coating clusters in Europe, significantly boosting service capacity for commercial aircraft repainting and maintenance operations. This expansion is aligned with increasing demand from major OEMs and airlines for high-performance and eco-compliant coating solutions.

Innovation and sustainability remain at the forefront of the French market. Advanced research initiatives are driving the development of next-generation corrosion-resistant coatings, including alternatives to traditional chromate systems. The near-complete phase-out of hexavalent chromium ahead of EU deadlines demonstrates France’s leadership in regulatory compliance. Additionally, the adoption of drag-reduction riblet coatings is improving fuel efficiency, while investments in laser decoating technologies are enabling environmentally friendly paint removal processes. These developments are positioning France as a pioneer in sustainable aircraft paint technologies.

India Aircraft Paint Market: MRO Cost Optimization and Domestic Defense Coating Innovations

India’s aircraft paint market is rapidly evolving, driven by government initiatives aimed at reducing operational costs and strengthening domestic aerospace capabilities. Policy measures, including customs duty exemptions for raw materials, are significantly lowering the cost of aircraft painting and maintenance, encouraging local production and adoption of advanced coating systems. The expansion of MRO facilities is further supporting the country’s emergence as a regional hub for aircraft painting services.

Technological advancements are enabling India to address both commercial and defense sector requirements. The development of indigenous radar-absorbing paints is enhancing stealth capabilities for military aircraft, while moisture-cured urethane coatings are improving application efficiency in high-humidity environments. Infrastructure investments in surface treatment facilities are strengthening the aerospace manufacturing ecosystem. Additionally, the adoption of photoluminescent paints for safety applications is increasing compliance with aviation regulations, highlighting the growing sophistication of India’s aircraft paint market.

China Aircraft Paint Market: C919 Production Scaling and Green Coating Mandates Driving Localization

China’s aircraft paint market is expanding rapidly, supported by the scaling of domestic aircraft production and stringent environmental regulations. The establishment of advanced aerospace coating centers is enabling the adoption of low-VOC, electrostatic spray systems, ensuring compliance with strict regional emission standards. This shift toward sustainable coating technologies is aligning with the country’s broader environmental objectives.

Innovation and localization are key market drivers, with domestic manufacturers developing advanced coatings such as solar-reflective topcoats that improve thermal performance in aircraft operating in high-temperature environments. The enforcement of green coating policies is encouraging airlines to transition toward lead-free and chromate-free systems, supported by financial incentives. Additionally, technological advancements such as AI-driven color matching and digital modeling are enhancing consistency in aircraft livery applications. Increased demand for anti-erosion coatings in amphibious aircraft further underscores the importance of high-performance protective coatings in China’s aerospace sector.

Germany Aircraft Paint Market: Circular Economy Innovations and Hydrogen-Ready Coating Technologies

Germany’s aircraft paint market is characterized by its strong emphasis on sustainability, advanced material innovation, and digital inspection technologies. The development of bio-based interior coatings is supporting circular economy initiatives within the aerospace sector, aligning with the sustainability goals of major airlines. These innovations are reducing reliance on fossil-based raw materials while maintaining high performance standards.

Technological advancements are also driving the development of coatings tailored for next-generation aircraft systems, including hydrogen-powered aviation. Research into cryogenic-stable coatings is addressing the challenges associated with liquid hydrogen storage, while automated inspection technologies are improving maintenance efficiency. Demand for high-temperature-resistant coatings is growing in response to advancements in engine design, and the adoption of cool-paint technologies is enhancing energy efficiency. These developments position Germany as a leader in future-ready aircraft paint solutions.

Japan Aircraft Paint Market: Nano-Coatings and Next-Generation Aerodynamic Enhancements

Japan’s aircraft paint market is advancing through its focus on nanotechnology and next-generation aerospace innovations. The commercialization of nano-silica infused coatings is delivering exceptional hardness and durability while maintaining the flexibility required for aircraft structures. These coatings are increasingly being adopted in high-performance aviation applications where both strength and adaptability are critical.

The country is also investing heavily in aerodynamic and functional coating technologies. The development of riblet film-paint hybrids is improving fuel efficiency by reducing drag, while government-supported programs are advancing foul-release coatings that minimize contamination on aircraft surfaces. Additionally, the growing demand for electromagnetic shielding coatings in emerging sectors such as eVTOL is driving innovation in multifunctional coatings. Regulatory updates promoting environmentally safe materials and investments in advanced resin production are further strengthening Japan’s position in the global aircraft paint market.

Aircraft Paint Market Report Scope

Aircraft Paint Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.2 Billion

|

|

Market Size (2032)

|

$8.1 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Paint Type (Polyurethane Paints, Epoxy Paints, Enamel & Acrylic Systems, Fluoropolymers, Chrome-Free Primers, Specialized Smart Coatings)), By Technology (Solvent-borne Coatings, Water-borne Coatings, Powder Coatings, Bio-based Coatings)), By Application Area (Exterior Coatings, Interior Coatings, Engine & Specialized Components, Touch-up & Refinish)), By Aircraft Type (Narrow-body Aircraft, Wide-body Aircraft, Regional & Turboprop Aircraft, Business & Private Jets, Military Aircraft, Rotary Wing)), By User Segment (OEM, MRO)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, Mankiewicz Gebr. & Co., Axalta Coating Systems Ltd., BASF SE, Hentzen Coatings, Inc., Jotun A/S, Henkel AG & Co. KGaA, Hempel A/S, Socomore, Indestructible Paint Ltd., Nycote Laboratories Corporation, IHI Ionbond AG, HMG Paints Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aircraft Paint Market Segmentation

By Paint

- Polyurethane Paints

- Epoxy Paints

- Enamel & Acrylic Systems

- Fluoropolymers

- Chrome-Free Primers

- Specialized Smart Coatings

By Technology

- Solvent-borne Coatings

- Water-borne Coatings

- Powder Coatings

- Bio-based Coatings

By Application Area

- Exterior Coatings

- Interior Coatings

- Engine & Specialized Components

- Touch-up & Refinish

By Aircraft Type

- Narrow-body Aircraft

- Wide-body Aircraft

- Regional & Turboprop Aircraft

- Business & Private Jets

- Military Aircraft

- Rotary Wing

By User Segment

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Aircraft Paint Market

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Mankiewicz Gebr. & Co.

- Axalta Coating Systems Ltd.

- BASF SE

- Hentzen Coatings, Inc.

- Jotun A/S

- Henkel AG & Co. KGaA

- Hempel A/S

- Socomore

- Indestructible Paint Ltd.

- Nycote Laboratories Corporation

- IHI Ionbond AG

- HMG Paints Ltd.

*- List not Exhaustive

Table of Contents: Aircraft Paint Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Aircraft Paint Market Landscape & Outlook (2025–2032)

2.1. Introduction to Aircraft Paint Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Growth Drivers: Fleet Expansion and MRO Demand

2.4. Lightweight Coatings and Fuel Efficiency Optimization

2.5. Regulatory Compliance and Sustainable Coating Technologies

3. Innovations Reshaping the Aircraft Paint Market

3.1. Trend: Strategic Investments and OEM Partnerships

3.2. Trend: VOC Reduction and Low-Emission Paint Technologies

3.3. Opportunity: Robotic Automation in Aircraft Painting

3.4. Opportunity: Electroluminescent and Anti-Microbial Coatings

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Aircraft Paint Market

5.1. By Paint

5.1.1. Polyurethane Paints

5.1.2. Epoxy Paints

5.1.3. Enamel & Acrylic Systems

5.1.4. Fluoropolymers

5.1.5. Chrome-Free Primers

5.1.6. Specialized Smart Coatings

5.2. By Technology

5.2.1. Solvent-borne Coatings

5.2.2. Water-borne Coatings

5.2.3. Powder Coatings

5.2.4. Bio-based Coatings

5.3. By Application Area

5.3.1. Exterior Coatings

5.3.2. Interior Coatings

5.3.3. Engine & Specialized Components

5.3.4. Touch-up & Refinish

5.4. By Aircraft Type

5.4.1. Narrow-body Aircraft

5.4.2. Wide-body Aircraft

5.4.3. Regional & Turboprop Aircraft

5.4.4. Business & Private Jets

5.4.5. Military Aircraft

5.4.6. Rotary Wing

5.5. By User Segment

5.5.1. OEM

5.5.2. MRO

6. Country Analysis and Outlook of Aircraft Paint Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Aircraft Paint Market Size Outlook by Region (2025–2032)

7.1. North America Aircraft Paint Market Size Outlook to 2032

7.1.1. By Paint

7.1.2. By Technology

7.1.3. By Application Area

7.1.4. By Aircraft Type

7.1.5. By User Segment

7.2. Europe Aircraft Paint Market Size Outlook to 2032

7.2.1. By Paint

7.2.2. By Technology

7.2.3. By Application Area

7.2.4. By Aircraft Type

7.2.5. By User Segment

7.3. Asia Pacific Aircraft Paint Market Size Outlook to 2032

7.3.1. By Paint

7.3.2. By Technology

7.3.3. By Application Area

7.3.4. By Aircraft Type

7.3.5. By User Segment

7.4. South America Aircraft Paint Market Size Outlook to 2032

7.4.1. By Paint

7.4.2. By Technology

7.4.3. By Application Area

7.4.4. By Aircraft Type

7.4.5. By User Segment

7.5. Middle East and Africa Aircraft Paint Market Size Outlook to 2032

7.5.1. By Paint

7.5.2. By Technology

7.5.3. By Application Area

7.5.4. By Aircraft Type

7.5.5. By User Segment

8. Company Profiles: Leading Players in the Aircraft Paint Market

8.1. PPG Industries, Inc.

8.2. Akzo Nobel N.V.

8.3. The Sherwin-Williams Company

8.4. Mankiewicz Gebr. & Co.

8.5. Axalta Coating Systems Ltd.

8.6. BASF SE

8.7. Hentzen Coatings, Inc.

8.8. Jotun A/S

8.9. Henkel AG & Co. KGaA

8.10. Hempel A/S

8.11. Socomore

8.12. Indestructible Paint Ltd.

8.13. Nycote Laboratories Corporation

8.14. IHI Ionbond AG

8.15. HMG Paints Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures