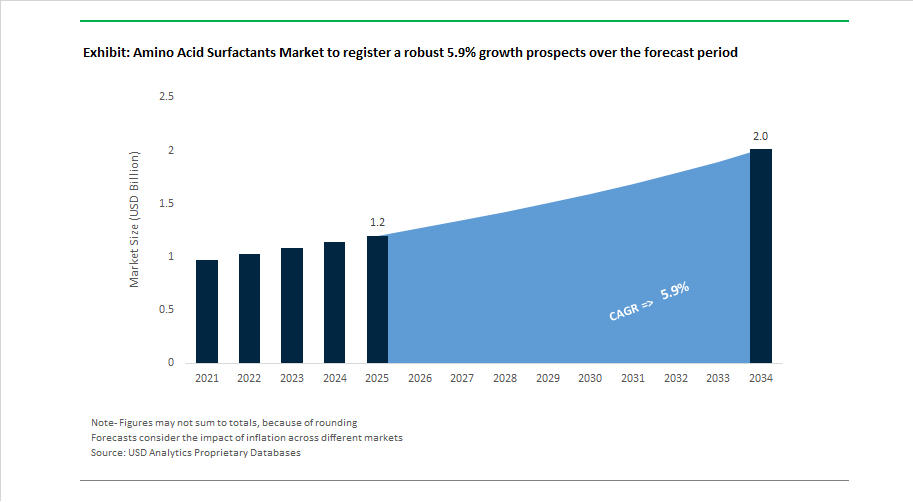

Market Overview: Amino Acid Surfactants Market to Reach $2 Billion by 2034 as Mild Bio-Based Cleansing Agents Gain Mass Adoption

The global amino acid surfactants market is projected to grow from $1.2 billion in 2025 to $2 billion by 2034, registering a 5.9% CAGR driven by rising demand for mild, biodegradable, sulfate-free surfactants across personal care, home care, and specialty industrial formulations. These surfactants, derived from glutamic acid, glycine, sarcosine, and other amino acids, offer low irritation potential, superior skin compatibility, and strong foaming performance, making them central to clean beauty, hypoallergenic skincare, baby care products, and dermatological cleansers. Market expansion is reinforced by regulatory pressure to reduce aquatic toxicity, consumer preference for plant-derived ingredients, and advances in enzymatic synthesis that lower production costs. Verified adoption data in late 2024 from U.S. agencies showed thousands of new product formulations incorporating amino acid surfactants to meet hypoallergenic and low-toxicity standards, marking a transition from niche premium ingredients to broader market penetration.

Industrial capacity and formulation innovation accelerated in March 2024 when Dow and DuPont initiated collaboration on bio-based surfactant systems for agrochemical applications. Portfolio expansion followed in May 2024 as Clariant completed the acquisition of Huntsman’s specialty additives, strengthening its position in mild surfactant intermediates. Production scaling advanced in January 2025 with Planet Chemical Company doubling anionic capacity in Ohio. Performance refinement emerged in January 2025 when Ajinomoto upgraded its Amisoft surfactant line using enzymatic purification for clearer formulations. Regulatory progress in February 2025 enabled Lonza Group to expand European production of high-purity surfactants. Cost efficiency improved in mid-2025 as enzymatic synthesis breakthroughs reduced production costs by up to 22%, while purity enhancements were highlighted in July 2025 by Sino Lion.

Sustainability-led capacity expansion strengthened through November 2025 when BASF inaugurated a bio-based surfactant facility in Thailand to serve Asia’s personal and home care sectors. Formulation compatibility advances were introduced in October 2025 with Clariant’s TexCare One Terra polymer supporting concentrated detergent systems. Ingredient crossover innovation followed in July 2025 as Sino Lion registered cosmetic bioactives compatible with amino acid surfactant systems. Global supply balancing progressed in January 2026 as BASF confirmed the start-up schedule for its Cincinnati production line, ensuring regional supply security.

Strategic Trends and High-Value Opportunities Transforming the Amino Acid Surfactants Market

Market Trend: Regulatory Pressure Shifts Surfactant Demand Toward Mild, Biodegradable Amino Acid Chemistries

Government-led chemical safety mandates are directly reshaping surfactant portfolios, particularly in cosmetics, toiletries, and skin-contact applications. Sulfate-based surfactants such as SLS and SLES are under scrutiny due to 1,4-dioxane residuals and documented irritation levels, prompting formulators to replace a portion of their volume with gentler glutamate- and glycine-derived systems. Clinical personal-care technical papers published in 2025 indicate 25 to 30% reduction in irritancy indices when Sodium Cocoyl Glutamate and related amino acid surfactants replace synthetic sulfates. This consumer health benefit translates commercially into stronger dermatologist-approved branding and repeat-purchase loyalty.

Regulatory enforcement is amplifying this transition. The EU REACH 2025 update elevates “green chemistry compliance” from optional to required in several product categories, forcing cosmetic manufacturers to demonstrate biodegradability and wastewater compatibility. Major ingredient suppliers are adjusting upstream strategies accordingly. Galaxy Surfactants’ FY24-25 report outlines a targeted pivot toward “Clean Beauty chemistry” portfolios, indicating that up to 15% of global surfactant volume is now transitioning toward amino-acid based technologies to maintain eco-label and hypoallergenic claims across top-tier cosmetic SKUs.

Market Trend: Fermentation-Enabled Scale Lowers Cost Barriers and Expands Market Access

Historically, amino acid surfactants were cost-prohibitive, relying on hydrolysis of animal or plant-based proteins. Industry strategy is now shifting toward biotechnological fermentation, which offers higher production efficiency, purity, and microbial control, unlocking the ability to scale competitively. Ajinomoto’s January 2025 AminoScience announcement highlights a dedicated focus on L-Glutamic acid–derived surfactants to serve the premium Asian personal-care sector, where skin barrier-friendly products command price premiums and high usage frequency.

Meanwhile, Evonik’s organizational restructuring marks a deliberate consolidation of its amino acid capacity at major fermentation hubs in Ham, France and Wuming, China, creating cost-competitive supply that supports long-term contracts with personal-care multinationals. Sustainability is emerging as a commercial differentiator: several producers achieved EcoVadis Gold ratings in June 2025 by integrating renewable energy and mass-balance biological feedstocks, reducing Scope 3 emissions by between 5 and 10% per ton of output. This ESG-linked positioning is now influencing procurement, especially among corporate customers with 2030 Net Zero commitments.

High-Value Growth Opportunities

Market Opportunity: Foundational Ingredient in Ultra-Mild Baby Care, Dermocosmetics and Preservative-Free Formulations

Global skin-sensitivity prevalence is rising. Industry analysts estimate that nearly 70% of consumers self-identify as having sensitive skin, reshaping ingredient selection priorities. Amino acid surfactants such as alanine-based and glycine-based systems provide measurable soothing effects at skin-neutral pH levels around 5.5, making them ideal inputs for baby-care and dermatologist-endorsed skincare. Their biochemical behavior offers a secondary value proposition: self-preserving surfactant systems. Clariant’s Hostapon™ range demonstrates how amino acid–derived glycinates support mild acidic formulations that suppress microbial growth, allowing formulators to reduce traditional preservative loading by up to 40% without sacrificing shelf life.

At the same time, the “premium cleansing” trend is redefining pricing power. Sarcosinate-based surfactants consistently command 30 to 40% higher pricing due to their ability to deliver rich, creamy foam even in electrolyte-heavy systems such as dermocosmetic cleansers, acne products, and micellar waters. This premiumization effect is expected to drive revenue growth disproportionate to volume growth across major skincare-focused segments.

Market Opportunity: Essential Excipient for Lipid Nanoparticle (LNP) Delivery in mRNA and Gene-Therapy Platforms

Amino acid–derived surfactants also play a strategic role outside consumer care, particularly within pharmaceutical-grade lipid nanoparticle (LNP) delivery, a domain expected to expand as mRNA platforms move beyond vaccines into oncology, metabolic disease, and rare-disease therapeutics. In November 2025, MIT-affiliated research groups validated amino-lipid structures (including AMG1541) with ester-based linkages that biodegrade more cleanly in vivo, enabling a therapeutic effect at 1/100th the active dose required by early LNP formulations. This is reshaping the economics of RNA-based medicine, lowering side effects, and enabling decentralized global distribution.

Industry strategy is shifting accordingly. Evonik’s corporate roadmap identifies lipids for mRNA and gene therapies as a core growth vertical, aligning with the discontinuation of lower-margin legacy keto acids by late-2025. Academic research published in August 2025 confirms that amino-lipid nanoparticle composition is the single most critical determinant of mRNA thermostability, enabling vaccine transport into regions lacking cold-chain capacity and opening markets across LATAM, Africa, and Southeast Asia.

Amino Acid Surfactants Market Share and Segmentation Insights

Market Share by Product Type: Glutamic Acid Surfactants Lead While Alanine Variants Accelerate

Glutamic acid based surfactants account for approximately 38% of the global amino acid surfactants market in 2025, led by acylglutamates such as sodium cocoyl glutamate and disodium stearoyl glutamate. These ingredients are widely regarded as the benchmark for sulfate-free cleansing due to creamy foam texture, near-neutral pH compatibility, and superior skin after-feel, making them dominant in premium facial cleansers and baby care. Glycine based surfactants rank second and lead volumes across Asia-Pacific, offering strong foaming comparable to SLS at lower cost, supporting mass-market sulfate-free shampoos and shower gels. Sarcosine based surfactants remain stable, serving toothpaste and multifunctional cleansing systems. Alanine based surfactants are the fastest-growing segment, driven by ultra-mildness and formulation flexibility in dermatological and infant applications. Other amino acid derivatives remain niche, limited to high-end cosmeceutical and prescription formulations due to elevated synthesis costs.

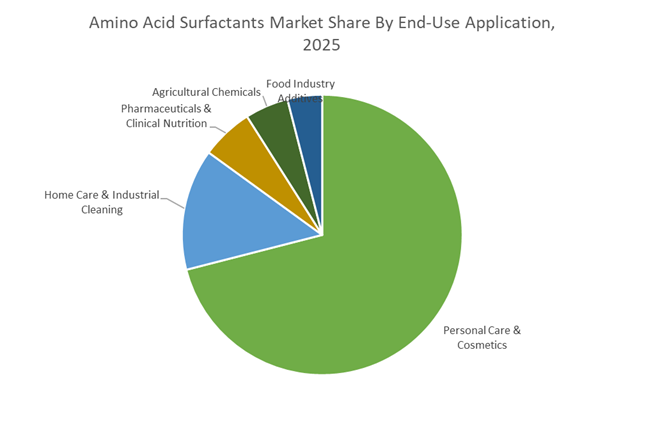

Market Share by End-Use Application: Personal Care Dominates Amid Sulfate Phase-Out

Personal care and cosmetics represent roughly 71% of global amino acid surfactant consumption in 2025, encompassing facial cleansers, shampoos, body washes, baby care, and oral care. The structural phase-out of sodium lauryl sulfate and sodium laureth sulfate in premium and increasingly mass-market formulations remains the single most powerful demand catalyst, supported by ECO, COSMOS, and Ecolabel certification standards. This segment sustains 8 to 10% annual growth and commands premium pricing. Home care and industrial cleaning remain significantly smaller, with amino acid surfactants limited to environmentally positioned dishwashing and delicate fabric care products where APG and betaine chemistries compete on cost. Pharmaceuticals and clinical nutrition represent a high-margin niche requiring cGMP and USP-grade purity. Agricultural chemicals show gradual substitution of APEOs at 5 to 6% growth, while food industry applications remain minimal due to stringent regulatory approval pathways.

Competitive Landscape: Fermentation-Derived Mildness, Cold-Process Manufacturing, and Bio-Based Scale Redefining the Amino Acid Surfactants Market

The Amino Acid Surfactants Market is rapidly shifting toward fermentation-derived feedstocks, cold-process manufacturing, and biomass-balanced production as brands prioritize sulfate-free, ultra-mild, and low-carbon cleansing systems. Competitive advantage increasingly hinges on vertical integration into amino acids, proprietary foam engineering, digital formulation tools, and the ability to scale bio-based surfactants across personal care, oral care, and sensitive-skin applications. Market leaders are investing heavily in Asia-Pacific capacity, AI-enabled formulation platforms, and “green chemistry” pathways to make amino acid surfactants cost-competitive with legacy synthetics such as SLES.

Ajinomoto Co., Inc. anchors global innovation with fermentation-integrated amino surfactants

Ajinomoto Co., Inc. remains the technological cornerstone of amino acid surfactants, having pioneered AMISOFT™ in 1972. In late 2025, the company launched its AminoScience 2030 Roadmap, targeting personal care to represent 25% of specialty chemical revenue by 2030. Its AMISOFT™ ECS-22SB, introduced in 2025, enables cold-process manufacturing, cutting energy use for CPG producers by roughly 30%. Ajinomoto’s unmatched vertical integration, producing its own amino acid feedstocks via proprietary fermentation, creates a closed-loop supply chain insulated from raw material volatility. Its AMILITE™ series continues to set the global benchmark for creamy foam in premium facial cleansers, backed by deep expertise in L-glutamic acid and alanine chemistry.

Clariant AG localizes low-carbon amino surfactants for China’s premium beauty market

Clariant AG has repositioned as a specialty pure player, emphasizing ultra-low carbon surfactant systems for Europe and China. In November 2025, Clariant completed an CHF 80 million expansion of its Daya Bay site, transforming it into a multi-purpose plant for high-performance surfactants, including amino-acid-based derivatives. Under its Greater Chemistry 2025 initiative, Clariant is targeting 50% local production in China to serve booming demand for bio-based skincare. Its GlucoPure® and GlucoTain® platforms combine sugar and amino acid synergies for high cleansing performance without harsh ethoxylates, while its Shanghai innovation hub enables real-time co-creation with Chinese beauty brands.

Sino Lion democratizes amino surfactants through zero-waste, high-volume production

Sino Lion has emerged as a global leader in green, cost-competitive amino acid surfactants, specializing in glycinate and sarcosinate systems. In 2025, the company launched Eversoft™ YCS-100, a sodium cocoyl glycinate powder produced via a patented zero-emission, zero-waste process. Its products are valued for delivering a silky after-feel that mimics natural moisturizing factors, making Sino Lion dominant in oral care and lens cleaning where extreme mildness is essential. The company’s “Affordable Green” strategy focuses on aggressive capacity scaling to position amino acid surfactants as viable alternatives to SLES across emerging markets.

Miwon Commercial Co., Ltd. applies electronic-grade purification to next-generation amino surfactants

Miwon Commercial Co., Ltd. has rapidly specialized in high-purity surfactants serving K-Beauty and electronics hygiene applications. In 2025, Miwon earned a Bronze EcoVadis rating, reflecting upgrades in sustainability and supply chain transparency. Its unique cross-industry integration applies electronic-grade purification standards to cosmetic surfactants, delivering exceptionally low impurity profiles. The company expanded its Banwol R&D Center to develop next-generation anionic amino surfactants for the sulfate-free shampoo market. Miwon also leads in taurate and isethionate derivatives, increasingly blended with amino acid surfactants to stabilize foam under hard water conditions.

BASF SE scales biomass-balanced amino surfactants with AI-driven formulation

BASF SE leverages its Verbund infrastructure to industrialize sustainable surfactant systems at global scale. In 2025, BASF introduced the Surfactant Navigator, an AI-powered tool that predicts synergies between APGs and amino acid surfactants to optimize foam volume and bubble structure. Its Plantapon® range features 100% bio-based amino surfactants, while the Endinol® Mild SCG line was scaled in 2026 to meet tightening dioxane-free regulations in California and New York. BASF’s strategy centers on transitioning its entire surfactant portfolio to Biomass Balance certification by 2030, supported by unmatched logistics capability across EU, North America, and APAC.

Galaxy Surfactants Ltd. drives mass-market adoption through solid formats and conscious chemistry

Galaxy Surfactants Ltd. is rapidly gaining global share by tailoring amino acid surfactants for mass and mass-prestige personal care. In 2025, Galaxy ramped production of its Galseer® Tresscon platform, a sustainable shampoo bar base formulated with high amino surfactant content to support waterless beauty. Guided by its Conscious Chemistry strategy, Galaxy targets solid and concentrated formats to reduce plastic use and transport emissions. The company is a key supplier to global FMCG brands reformulating baby care and sensitive skin lines for 2026–2027, supported by strong backward integration into oleochemicals that stabilizes pricing despite palm and coconut oil volatility.

China Amino Acid Surfactants Market: Integrated Capacity Scaling and Clean Beauty Localization

China has emerged as a central production and formulation hub for amino acid surfactants, supported by large-scale investments and stricter quality enforcement. In November 2025, Clariant finalized an 80 million CHF strategic expansion at its Daya Bay site in Huizhou. The project transformed the facility into an integrated Multi-Purpose Plant, adding new reactors dedicated to high-performance specialty chemicals, including mild amino acid surfactants for personal care and home care applications.

Regulatory tightening in 2025 introduced mandatory limits on hazardous chemical residues, accelerating the transition toward fermentation-derived and high-purity surfactants among domestic leaders such as Tinci and Sino Lion. At the same time, multinational and local players are localizing R&D and technical service teams to support China’s fast-growing clean beauty e-commerce segment, enabling rapid customization of amino acid-based formulations for sensitive skin, baby care, and premium facial cleansers.

India Amino Acid Surfactants Market: BioE3 Policy and Capital Incentives Fuel Indigenous Surfactant Platforms

India’s amino acid surfactants landscape is being reshaped by policy-driven biomanufacturing priorities. The approval of the BioE3 Policy in late 2024 positioned bio-based chemicals and enzymes as strategic industrial pillars, directly supporting fermentation-based surfactant development. This framework is being operationalized through funded Biomanufacturing Hubs and Biofoundries designed to scale green chemistry solutions aligned with India’s net-zero ambitions.

Financial incentives have reinforced this momentum. By 2025, realized investments under the Production Linked Incentive scheme enabled domestic leaders such as Galaxy Surfactants to accelerate expansion of green and mild surfactant portfolios. In parallel, the Ministry of Chemicals introduced a 20% Capex subsidy for new bio-based manufacturing units commissioned by 2026, reducing import dependency on amino acid intermediates and strengthening India’s position as an export-oriented production base for sulfate-free personal care ingredients.

United States Amino Acid Surfactants Market: Regulatory Scrutiny and Domestic Manufacturing Rebalancing

In the United States, regulatory and trade dynamics are reshaping sourcing strategies for amino acid surfactants. Revised import tariffs in early 2025 increased costs for certain fermentation-derived and synthetic amino acid precursors, prompting formulators to re-evaluate overseas dependency and accelerate domestic manufacturing investments to enhance supply chain resilience.

At the innovation level, BASF announced a biotechnology partnership in late 2024 focused on enzymatic synthesis of sustainable surfactants for North American personal care and cleaning markets. Regulatory scrutiny has also intensified, with the U.S. Food and Drug Administration expanding surveillance of sulfate-based surfactants in 2025. This shift has pushed premium skincare brands toward amino acid surfactants to support hypoallergenic and dermatologist-tested claims. Adjacent demand is emerging in pet care, particularly within the Kansas Animal Health Corridor, where amino acid surfactants are increasingly used in tearless and skin-barrier-safe grooming products.

Japan Amino Acid Surfactants Market: Precision Manufacturing and Enzymatic Efficiency Gains

Japan continues to lead in high-purity amino acid chemistry and process optimization. In early 2025, Ajinomoto Co., Inc. completed the modernization of its Tokai Plant, commissioning a fully automated production line for amino acid-based surfactants. The upgrade strengthened supply reliability for glutamic acid and glycine derivatives used in premium global formulations.

Innovation is extending into synthesis efficiency. In 2025, Japanese research institutes, working alongside industry partners, demonstrated enzyme-catalyzed surfactant synthesis routes that cut energy consumption by 15% compared to traditional condensation processes. Ajinomoto also reported a 10% reduction in greenhouse gas emissions within its surfactant division through the use of biomass-derived raw materials and optimized fermentation cycles, reinforcing Japan’s leadership in low-footprint specialty ingredients.

Germany Amino Acid Surfactants Market: Regulatory Leadership and Ultra-Sustainable Surfactant Systems

Germany is anchoring the regulatory and sustainability framework for amino acid surfactants in Europe. In 2024–2025, Evonik Industries commercialized industrial-scale rhamnolipid biosurfactants under the REWOFERM® RL series. These biosurfactants are increasingly positioned as synergistic companions to amino acid surfactants in ultra-sustainable laundry and hard-surface cleaning formulations.

Regulatory leadership is reinforcing this transition. Following approval of the New EU Detergents and Surfactants Regulation in late 2025, German manufacturers began implementing Digital Product Passports to ensure full traceability and biodegradability compliance. Operational decarbonization is progressing in parallel, with major German chemical hubs reporting a shift to renewable-powered steam generation for surfactant distillation during 2025, aligning amino acid surfactant production with Europe’s net-zero industrial objectives.

Country-Level Strategic Positioning in Amino Acid Surfactants

Amino Acid Surfactants Market County Level Snapshot

|

Country

|

Strategic Focus

|

Industry Implication

|

|

China

|

Integrated capacity and localized clean beauty R&D

|

Rapid scale-up of high-purity, fermentation-derived surfactants

|

|

India

|

BioE3 policy and capital incentives

|

Indigenous biomanufacturing and export-ready green surfactants

|

|

United States

|

Regulatory scrutiny and supply chain rebalancing

|

Shift toward domestic, enzymatic, mild surfactant production

|

|

Japan

|

Precision automation and enzymatic synthesis

|

High-purity, low-energy amino acid surfactant platforms

|

|

Germany

|

Regulatory leadership and biosurfactant synergy

|

Traceable, ultra-sustainable surfactant systems for EU markets

|

Amino Acid Surfactants Market Report Scope

Amino Acid Surfactants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.2 Billion

|

|

Market Size (2034)

|

$2 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Product Type (Glutamic Acid Based Surfactants, Glycine Based Surfactants, Sarcosine Based Surfactants, Alanine Based Surfactants, Other Amino Acid Based Surfactants), By Form (Liquid, Powder, Granular, Paste and Gel), By Feedstock Source (Fully Bio Based, Partially Bio Based), By End Use Application (Personal Care and Cosmetics, Home Care and Industrial Cleaning, Pharmaceuticals and Clinical Nutrition, Agricultural Chemicals, Food Industry Additives)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ajinomoto, Clariant AG, BASF SE, Evonik Industries AG, Sino Lion, Galaxy Surfactants, Innospec, Croda International, Solvay, Miwon Commercial, Tinci Materials Technology, Zschimmer and Schwarz, Stepan Company, Kao Corporation, Changsha Puji Biotech

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Amino Acid Surfactants Market Segmentation

By Product Type

- Glutamic Acid Based Surfactants

- Glycine Based Surfactants

- Sarcosine Based Surfactants

- Alanine Based Surfactants

- Other Amino Acid Based Surfactants

By Form

- Liquid

- Powder

- Granular

- Paste and Gel

By Feedstock Source

- Fully Bio Based

- Partially Bio Based

By End Use Application

- Personal Care and Cosmetics

- Home Care and Industrial Cleaning

- Pharmaceuticals and Clinical Nutrition

- Agricultural Chemicals

- Food Industry Additives

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Amino Acid Surfactants Industry

- Ajinomoto

- Clariant AG

- BASF SE

- Evonik Industries AG

- Sino Lion

- Galaxy Surfactants

- Innospec

- Croda International

- Solvay

- Miwon Commercial

- Tinci Materials Technology

- Zschimmer and Schwarz

- Stepan Company

- Kao Corporation

- Changsha Puji Biotech

*- List not Exhaustive