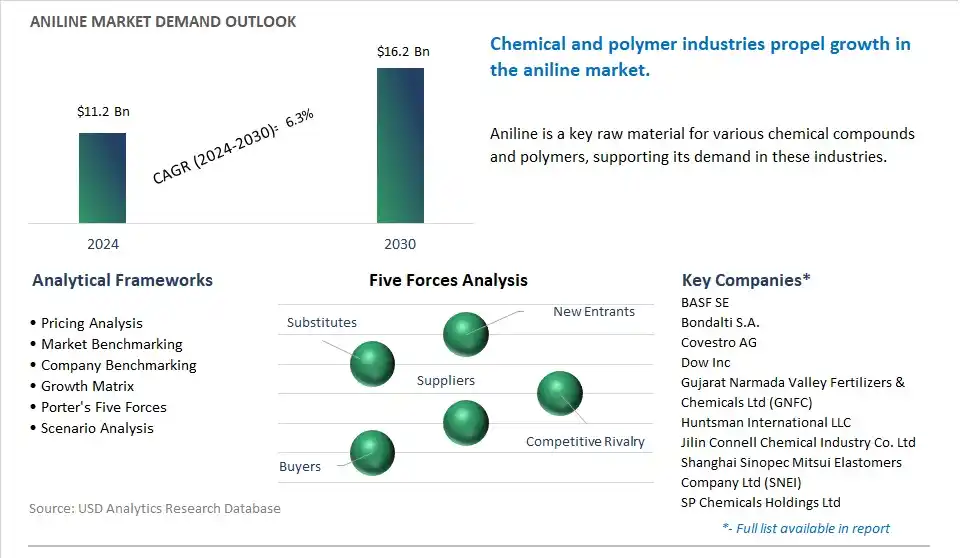

The global Aniline Market is poised to register a 6.3% CAGR from $11.2 Billion in 2024 to $16.2 Billion in 2030.

The global Aniline Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Application (Methylene Diphenyl Diisocyanate, Rubber-Processing Chemicals, Agricultural Chemicals, Dyes and Pigments, Specialty Fibers, Others), By End-User (Building and Construction, Rubber, Consumer Goods, Automotive, Packaging, Agriculture, Others).

An Introduction to Global Aniline Market in 2024

The aniline market is witnessing steady growth driven by increasing demand in the production of dyes, pharmaceuticals, and rubber chemicals. Key trends shaping the future of the industry include the growing adoption of environmentally friendly and sustainable production methods such as hydrogenation of nitrobenzene and direct oxidation of benzene to reduce emissions and minimize waste generation. Moreover, there's a rising emphasis on specialty aniline derivatives for high-value applications such as polyurethane production, agrochemicals, and pharmaceutical intermediates, leading to innovations in synthesis routes, catalyst systems, and purification techniques. Additionally, advancements in aniline storage, handling, and transportation safety measures are driving innovation and market expansion, enabling manufacturers to offer reliable and compliant solutions for diverse industrial needs in the global aniline market.

Aniline Market Competitive Landscape

The market report analyses the leading companies in the industry including BASF SE, Bondalti S.A., Covestro AG, Dow Inc, Gujarat Narmada Valley Fertilizers & Chemicals Ltd (GNFC), Huntsman International LLC, Jilin Connell Chemical Industry Co. Ltd, Shanghai Sinopec Mitsui Elastomers Company Ltd (SNEI), SP Chemicals Holdings Ltd, Sumitomo Chemical Company Ltd, Tosoh Corp, Wanhua Chemical Group Co. Ltd.

Aniline Market Dynamics

Aniline Market Trend: Increasing Demand for Polyurethane and Rubber Products

A prominent market trend for aniline is the increasing demand for polyurethane and rubber products across various industries. Aniline serves as a crucial raw material in the production of polyurethane, a versatile polymer used in applications such as foam insulation, coatings, adhesives, and elastomers. Additionally, aniline is a key component in the manufacture of rubber chemicals and synthetic rubber products. With the growing construction, automotive, and consumer goods sectors, there's a rising demand for polyurethane foams, coatings, and rubber products, driving market demand for aniline as a primary feedstock in the production of these materials.

Aniline Market Driver: Growth in Construction and Automotive Industries

A significant driver for the aniline market is the growth in construction and automotive industries worldwide. Aniline-based polyurethane products find extensive use in construction applications such as insulation, sealants, and coatings for buildings and infrastructure projects. Similarly, in the automotive sector, aniline-derived polyurethane foams are utilized in interior components such as seating, dashboards, and insulation, contributing to comfort, safety, and noise reduction in vehicles. As urbanization continues to drive construction activity and the automotive industry expands to meet consumer demand, there's a growing need for aniline-based polyurethane and rubber products, fueling market growth for aniline as a key chemical intermediate.

Aniline Market Opportunity: Development of Sustainable and Bio-Based Aniline Production Methods

An opportunity for the aniline market lies in the development of sustainable and bio-based production methods. With increasing focus on environmental sustainability and reducing carbon footprint, there's growing interest in developing alternative processes for aniline production that utilize renewable feedstocks and green chemistry principles. Bio-based aniline production methods, such as enzymatic synthesis or microbial fermentation, offer the potential to reduce reliance on fossil fuels and minimize environmental impact. Additionally, advancements in catalytic processes and carbon capture technologies present opportunities to improve the efficiency and environmental sustainability of traditional aniline production methods. By investing in research and development of sustainable and bio-based aniline production methods, manufacturers can meet consumer demand for eco-friendly products and contribute to the transition towards a more sustainable chemical industry.

Aniline Market Share Analysis: Methylene Diphenyl Diisocyanate (MDI) production segment generated the highest revenue in the industry

The largest segment in the Aniline Market is Methylene Diphenyl Diisocyanate (MDI) production, and this dominance is driven by Aniline is a crucial raw material used in the production of MDI, which is a primary component in the manufacturing of polyurethane foams and elastomers. MDI is widely used in various industries such as construction, automotive, furniture, and appliances for insulation, cushioning, and structural applications. The demand for MDI has been steadily increasing due to the growing construction and automotive sectors globally, which are major consumers of polyurethane products. Aniline's significance lies in its role as a precursor in the synthesis of MDI, as it is a key component in the production process. In addition, the versatility and performance characteristics of MDI, including its thermal insulation properties, durability, and lightweight nature, contribute to its widespread adoption across multiple industries. Further, the expansion of infrastructure projects, urbanization trends, and the increasing demand for energy-efficient materials drive the growth of MDI production and, consequently, the demand for aniline as a feedstock. Over the forecast period, the dominance of Methylene Diphenyl Diisocyanate production in the Aniline Market is driven by the critical role of aniline in the production of MDI, which is a vital component in the manufacturing of polyurethane-based products used in various applications.

Aniline Market Share Analysis: Automotive Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Aniline Market is the Automotive sector, and the rapid growth is driven by there is a rising demand for aniline in the automotive industry due to its essential role in the production of polyurethane materials used in automotive interiors, such as seat cushions, dashboard components, and insulation panels. Polyurethane foams and elastomers, which are derived from aniline-based Methylene Diphenyl Diisocyanate (MDI), offer advantages such as lightweight, durability, and excellent cushioning properties, making them ideal for automotive applications. Additionally, the increasing emphasis on vehicle comfort, safety, and interior aesthetics drives the demand for high-quality polyurethane materials in the automotive sector, further boosting the consumption of aniline. In addition, stringent regulations aimed at reducing vehicle emissions and improving fuel efficiency have led to the adoption of lightweight materials, including polyurethane foams, in automotive design and manufacturing. Aniline-based polyurethane materials contribute to the production of lighter vehicles, thereby helping automakers meet regulatory requirements and enhance Over the forecast period performance. Further, the growing trend towards electric and hybrid vehicles, which require lightweight materials to optimize battery efficiency and extend driving range, drives the demand for aniline-based polyurethane materials in the automotive industry. Over the forecast period, the rapid growth of the Automotive segment in the Aniline Market is driven by the increasing demand for polyurethane materials in vehicle manufacturing, driven by technological advancements, regulatory requirements, and consumer preferences for comfort and sustainability in automotive design.

Aniline Market Report Segmentation

By Application

Methylene Diphenyl Diisocyanate

Rubber-Processing Chemicals

Agricultural Chemicals

Dyes and Pigments

Specialty Fibers

Others

By End-User

Building and Construction

Rubber

Consumer Goods

Automotive

Packaging

Agriculture

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Aniline Companies Profiled in the Market Study

BASF SE

Bondalti S.A.

Covestro AG

Dow Inc

Gujarat Narmada Valley Fertilizers & Chemicals Ltd (GNFC)

Huntsman International LLC

Jilin Connell Chemical Industry Co. Ltd

Shanghai Sinopec Mitsui Elastomers Company Ltd (SNEI)

SP Chemicals Holdings Ltd

Sumitomo Chemical Company Ltd

Tosoh Corp

Wanhua Chemical Group Co. Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Aniline Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Aniline Market Size Outlook, $ Million, 2021 to 2030

3.2 Aniline Market Outlook by Type, $ Million, 2021 to 2030

3.3 Aniline Market Outlook by Product, $ Million, 2021 to 2030

3.4 Aniline Market Outlook by Application, $ Million, 2021 to 2030

3.5 Aniline Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Aniline Industry

4.2 Key Market Trends in Aniline Industry

4.3 Potential Opportunities in Aniline Industry

4.4 Key Challenges in Aniline Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Aniline Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Aniline Market Outlook by Segments

7.1 Aniline Market Outlook by Segments, $ Million, 2021- 2030

By Application

Methylene Diphenyl Diisocyanate

Rubber-Processing Chemicals

Agricultural Chemicals

Dyes and Pigments

Specialty Fibers

Others

By End-User

Building and Construction

Rubber

Consumer Goods

Automotive

Packaging

Agriculture

Others

8 North America Aniline Market Analysis and Outlook To 2030

8.1 Introduction to North America Aniline Markets in 2024

8.2 North America Aniline Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Aniline Market size Outlook by Segments, 2021-2030

By Application

Methylene Diphenyl Diisocyanate

Rubber-Processing Chemicals

Agricultural Chemicals

Dyes and Pigments

Specialty Fibers

Others

By End-User

Building and Construction

Rubber

Consumer Goods

Automotive

Packaging

Agriculture

Others

9 Europe Aniline Market Analysis and Outlook To 2030

9.1 Introduction to Europe Aniline Markets in 2024

9.2 Europe Aniline Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Aniline Market Size Outlook by Segments, 2021-2030

By Application

Methylene Diphenyl Diisocyanate

Rubber-Processing Chemicals

Agricultural Chemicals

Dyes and Pigments

Specialty Fibers

Others

By End-User

Building and Construction

Rubber

Consumer Goods

Automotive

Packaging

Agriculture

Others

10 Asia Pacific Aniline Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Aniline Markets in 2024

10.2 Asia Pacific Aniline Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Aniline Market size Outlook by Segments, 2021-2030

By Application

Methylene Diphenyl Diisocyanate

Rubber-Processing Chemicals

Agricultural Chemicals

Dyes and Pigments

Specialty Fibers

Others

By End-User

Building and Construction

Rubber

Consumer Goods

Automotive

Packaging

Agriculture

Others

11 South America Aniline Market Analysis and Outlook To 2030

11.1 Introduction to South America Aniline Markets in 2024

11.2 South America Aniline Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Aniline Market size Outlook by Segments, 2021-2030

By Application

Methylene Diphenyl Diisocyanate

Rubber-Processing Chemicals

Agricultural Chemicals

Dyes and Pigments

Specialty Fibers

Others

By End-User

Building and Construction

Rubber

Consumer Goods

Automotive

Packaging

Agriculture

Others

12 Middle East and Africa Aniline Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Aniline Markets in 2024

12.2 Middle East and Africa Aniline Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Aniline Market size Outlook by Segments, 2021-2030

By Application

Methylene Diphenyl Diisocyanate

Rubber-Processing Chemicals

Agricultural Chemicals

Dyes and Pigments

Specialty Fibers

Others

By End-User

Building and Construction

Rubber

Consumer Goods

Automotive

Packaging

Agriculture

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

BASF SE

Bondalti S.A.

Covestro AG

Dow Inc

Gujarat Narmada Valley Fertilizers & Chemicals Ltd (GNFC)

Huntsman International LLC

Jilin Connell Chemical Industry Co. Ltd

Shanghai Sinopec Mitsui Elastomers Company Ltd (SNEI)

SP Chemicals Holdings Ltd

Sumitomo Chemical Company Ltd

Tosoh Corp

Wanhua Chemical Group Co. Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Application

Methylene Diphenyl Diisocyanate

Rubber-Processing Chemicals

Agricultural Chemicals

Dyes and Pigments

Specialty Fibers

Others

By End-User

Building and Construction

Rubber

Consumer Goods

Automotive

Packaging

Agriculture

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)