Anti-Corrosion Coatings Market Size and Growth Driven by Infrastructure Protection and Marine Asset Longevity

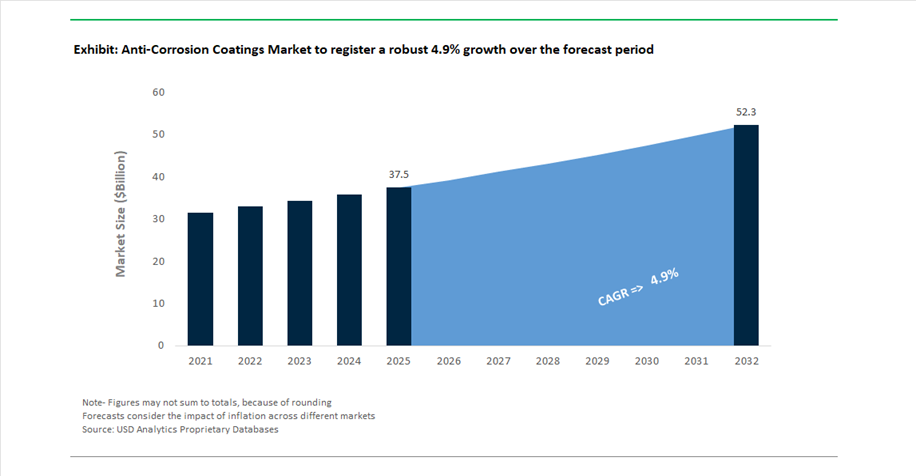

The Anti-Corrosion Coatings Market is a large-scale, mature yet steadily expanding segment, valued at USD 37.5 billion in 2025 and projected to reach USD 52.4 billion by 2032, growing at a CAGR of 4.9%. The market’s expansion is largely driven by the urgent need to mitigate corrosion-related losses, which cost global industries trillions annually due to asset degradation, operational downtime, and safety risks.

Anti-corrosion coatings serve as a critical protective barrier for metal substrates, particularly in industries such as oil & gas, marine, power generation, infrastructure, and transportation. These coatings, primarily based on epoxy, polyurethane, and zinc-rich systems, are engineered to resist chemical exposure, moisture ingress, saltwater corrosion, and extreme environmental conditions. As governments and private sector operators increasingly prioritize infrastructure resilience and lifecycle extension, demand for high-performance protective coatings is intensifying, especially in aging bridges, pipelines, offshore platforms, and water treatment facilities.

The market is also being shaped by the global transition toward sustainable and environmentally compliant coating technologies. Regulatory frameworks in Europe and North America are accelerating the shift toward low-VOC, water-based, and solvent-free formulations, without compromising durability and performance. Additionally, the emergence of smart coatings and predictive maintenance solutions is redefining corrosion management strategies, enabling early detection and intervention before structural damage occurs.

Growth is further supported by industrial expansion in emerging economies, particularly in Asia-Pacific and Southeast Asia, where large-scale infrastructure projects and manufacturing growth are driving demand for durable anti-corrosion solutions. The competitive landscape is characterized by technological innovation, strategic consolidation, and regional capacity expansion, positioning anti-corrosion coatings as a cornerstone of industrial asset protection strategies

Mega-Mergers, Smart Coating Technologies, and Capacity Expansion Reshaping Anti-Corrosion Coatings Market

The anti-corrosion coatings market is undergoing a structural evolution driven by strategic mergers, advanced material innovation, and global manufacturing expansion. Product innovation is increasingly focused on enhanced durability, environmental compliance, and intelligent functionality. In November 2025, Jotun introduced next-generation zinc-rich barrier coatings, offering superior bonding and resistance in salt-laden offshore and power plant environments. Building on this, Jotun’s January 2026 launch of smart coatings marks a technological breakthrough, incorporating real-time corrosion monitoring capabilities that allow infrastructure operators to detect early-stage degradation and optimize maintenance schedules.

Strategic initiatives from leading players are also accelerating market evolution. Hempel’s “Accelerate to Win” strategy (January 2026) emphasizes expansion in infrastructure and energy coatings, supported by innovations such as Hempafire Extreme, which integrates anti-corrosion performance with fire protection capabilities. Meanwhile, AkzoNobel’s December 2025 extension of its marine coatings partnership in China reflects increasing demand for sustainable anti-corrosive solutions in next-generation shipbuilding, particularly for eco-friendly vessels.

The industry is also witnessing a strategic shift toward portfolio optimization and high-margin segments. AkzoNobel’s divestment of its Indian decorative paints business (December 2025) underscores a focused pivot toward industrial performance coatings, including anti-corrosion technologies. Additionally, PPG’s investment in SIGMA COATINGS R&D (April 2025) highlights ongoing efforts to develop water-based and solvent-free epoxy systems, aligning with tightening environmental regulations in Europe.

Real-world applications continue to validate the importance of advanced coatings. Sherwin-Williams’ recognition for major infrastructure projects, including water treatment facilities utilizing epoxy and polysiloxane systems, demonstrates the role of anti-corrosion coatings in ensuring long-term structural integrity under aggressive chemical and atmospheric exposure.

Graphene-Enhanced Epoxy Primers Driving High-Performance Replacement of Zinc-Rich Systems

The anti-corrosion coatings industry is undergoing a significant material transition as graphene-enhanced epoxy primers begin to replace conventional zinc-rich epoxy (ZRE) systems. This shift is primarily driven by the operational limitations and environmental challenges associated with high zinc loading, which often exceeds 80% by weight in traditional coatings. Graphene introduces a highly efficient barrier mechanism through its “tortuous path” effect, significantly slowing down the diffusion of corrosive agents such as oxygen, moisture, and chlorides.

The performance gains from graphene integration are substantial even at minimal loading levels. Incorporating just 0.05% to 0.6% by weight of single-layer graphene into epoxy matrices has been shown to extend cathodic protection duration by over 50%, increasing corrosion resistance benchmarks from approximately 558 hours to over 850 hours in accelerated salt spray testing. Electrochemical impedance spectroscopy data from 2026 further validates this advancement, with graphene-zinc composite systems reducing corrosion current density from 2.88 × 10⁻⁶ A/cm² to 2.19 × 10⁻⁸ A/cm², representing a two-order magnitude improvement in corrosion inhibition efficiency.

Beyond performance, graphene-enhanced coatings offer clear advantages in weight and material efficiency. By reducing reliance on zinc dust, manufacturers can achieve equivalent C5-M marine-grade corrosion protection with coatings that are 15% to 20% lighter, a critical benefit for industries such as marine transportation and aerospace where weight optimization directly impacts operational efficiency. Additionally, graphene-infused primers demonstrate a 62% improvement in UV resistance and reduced yellowing compared to standard epoxy systems, ensuring long-term durability during exposure to harsh environmental conditions. These combined advantages position graphene-based anti-corrosion coatings as a next-generation solution for high-performance infrastructure and industrial applications.

Offshore Wind Corrosion Management Mandates Elevating Lifecycle Coating Standards

The rapid expansion of offshore wind energy infrastructure is intensifying the need for robust anti-corrosion strategies, driven by new regulatory mandates focused on asset integrity and lifecycle performance. Organizations such as the Energy Institute and the U.S. Bureau of Ocean Energy Management have introduced comprehensive Corrosion Management Plan (CMP) requirements, fundamentally changing how coatings are specified, applied, and monitored across offshore installations.

Corrosion-related degradation currently accounts for approximately 25% to 30% of total operations and maintenance costs in offshore wind farms, making it one of the most significant operational risks in the sector. In response, updated standards such as EI 3601 now require certified personnel responsible for corrosion management, ensuring that offshore assets meet a minimum design life of 25 years without the need for major recoating interventions. Additionally, regulatory frameworks such as the Renewable Energy Modernization Rule mandate detailed submission of Best Management Practices for cathodic protection systems and coating integrity monitoring, particularly for projects located on the Outer Continental Shelf.

The economic implications of non-compliance are substantial. Unplanned corrosion interventions can cost up to 100 times the initial coating application expense, reinforcing the need for high-durability coating systems. As a result, three-coat systems consisting of zinc primers, epoxy intermediates, and polyurethane topcoats have become the standard baseline for offshore wind applications in the absence of graphene-enhanced alternatives. This regulatory environment is accelerating demand for advanced anti-corrosion coatings that offer extended service life, reduced maintenance frequency, and compliance with stringent certification requirements, thereby creating a stable and high-value market segment within the broader coatings industry.

Specialized Coatings Enabling Efficiency and Durability in Green Hydrogen Electrolyzers

The transition toward green hydrogen production is creating a highly specialized opportunity for anti-corrosion coatings designed to operate in aggressive electrochemical environments. Proton Exchange Membrane (PEM) electrolyzers, a core technology in hydrogen generation, rely on metallic components such as titanium and stainless steel bipolar plates that are highly susceptible to corrosion and performance degradation over time.

Advanced conductive anti-corrosion coatings are playing a critical role in enhancing electrolyzer efficiency and longevity. These coatings can reduce voltage degradation rates to as low as 3 μV/h over 10,000 hours of operation, representing a 60% improvement compared to uncoated systems. Maintaining low interfacial contact resistance is essential for ensuring optimal current flow within the electrolyzer stack, and specialized coating formulations are engineered to prevent the formation of resistive oxide layers that can impair performance.

In addition to improving electrical efficiency, these coatings provide a protective barrier against hydrogen-induced degradation mechanisms such as embrittlement and hydriding. This is particularly important in high-pressure operating environments where structural integrity is critical. By extending component lifespan and reducing maintenance intervals, advanced anti-corrosion coatings are expected to lower the levelized cost of hydrogen production by 8% to 12% by 2028, making them a key enabler of economically viable green hydrogen systems.

Self-Healing Coatings Advancing Durability and Maintenance Efficiency in Military Applications

Self-healing anti-corrosion coatings are emerging as a transformative solution for military ground vehicles operating in highly corrosive and mechanically demanding environments. These coatings utilize advanced material systems, including microcapsule-based inhibitors and intrinsic polymer networks, to autonomously repair damage such as micro-cracks, scratches, and abrasion-induced defects.

Recent advancements in smart polymer chemistry have significantly improved healing efficiency and response time. Silicone-based coatings incorporating dynamic disulfide exchange mechanisms can achieve up to 94.6% healing efficiency within just 8 hours, enabling rapid restoration of protective functionality after damage occurs. Microcapsule-based systems further enhance corrosion resistance by releasing active inhibitors such as cerium ions or polyaniline upon rupture, forming a protective layer that can withstand salt spray exposure for more than 25 days even after coating damage.

From an operational standpoint, these coatings contribute to sustained asset readiness. Military validation tests indicate that self-healing coatings can recover up to 84% of their original mechanical toughness within 24 hours, ensuring continued protection in extreme environments such as coastal, desert, and high-humidity regions. Additionally, the adoption of self-repairing coatings is expected to reduce maintenance labor requirements by approximately 40%, allowing maintenance personnel to prioritize mission-critical mechanical systems rather than routine surface repairs.

Anti-Corrosion Coatings Market Share by Resin Type in 2025: Epoxy Coatings Dominate as the Backbone of Steel Protection Systems

Epoxy Resin Leadership Driven by Adhesion Strength, Chemical Resistance, and Multi-Functional Versatility

The anti-corrosion coatings market by resin type in 2025 is led by epoxy coatings, capturing 42.00% market share, reinforcing their position as the undisputed workhorse in corrosion protection technologies. Epoxy systems are uniquely capable of delivering exceptional adhesion to blast-cleaned steel, superior chemical resistance, and outstanding cathodic disbondment protection, making them indispensable in three-coat protective systems (zinc primer, epoxy mid-coat, polyurethane topcoat) used across critical infrastructure. This segment’s dominance is further strengthened by its broad technological versatility, including polyamide epoxies for general industrial coatings, amine epoxies for chemical immersion, novolac epoxies for high-temperature and acidic environments, and solvent-free epoxies for tank linings. In 2025, epoxy coatings represent the core of maintenance painting budgets, accounting for nearly 70% of surface preparation and primer application costs, as failure at this layer can result in steel replacement costs 5–10 times higher, emphasizing their critical role in asset integrity management.

Anti-Corrosion Coatings Market Share by End-Use Industry in 2025: Oil & Gas Sector Leads with High-Value Extreme Environment Applications

Oil & Gas Industry Drives Premium Demand Through Pipeline Coatings and High-Performance Protective Systems

The anti-corrosion coatings market by end-use industry in 2025 is dominated by the oil & gas sector, holding 25.50% market share, driven by the need for high-performance coatings capable of withstanding extreme operational environments. Unlike infrastructure coatings, oil & gas applications require resistance to high-pressure sour gas (H₂S), aggressive crude oil exposure, and thermal cycling, significantly increasing the cost per square meter for coatings such as offshore platform splash zone systems and internal pipeline flow coatings. The segment’s growth is anchored by midstream pipeline investments, where fusion bonded epoxy (FBE) coatings dominate as the primary solution for pipeline anti-corrosion and durability. Additionally, 2025 marks a strong shift toward thermal insulative coatings (TICs) and passive fire protection (PFP) epoxy intumescent coatings, driven by stringent process safety management (PSM) regulations. These advanced systems, applied alongside anti-corrosion primers, are expanding the value share of oil & gas coatings, making it the most lucrative segment in the global anti-corrosion coatings market.

Anti-Corrosion Coatings Market Competitive Landscape Driven by Advanced Protection Systems and Sustainable Technologies

The anti-corrosion coatings market is defined by high-performance epoxy coatings, zinc-rich primers, and powder coatings engineered for extreme environments. Leading players are advancing low-VOC formulations, digital application technologies, and corrosion protection systems across marine, energy, infrastructure, and automotive sectors.

AkzoNobel strengthens anti-corrosion leadership with laser-curing and sustainable powder coatings

AkzoNobel remains a major force in anti-corrosion coatings through its International® and Interpon® portfolios targeting marine coatings and industrial coatings applications. The company reported €10.16 billion in revenue in 2025 with an adjusted EBITDA margin of 14.2%, reflecting strong growth from protective coatings segments. In 2026, it entered the final phase of its merger with Axalta Coating Systems to strengthen global leadership in anti-corrosive powder coatings and liquid coatings. Sustainability progress includes nearly 50% reduction in Scope 1 and 2 emissions compared to 2018, alongside development of UV-reflective and corrosion-resistant coating technologies. Its partnership with IPG Photonics introduced laser-curing technology for powder coatings, reducing energy consumption in industrial application processes. Product innovation continues to focus on durability, efficiency, and environmentally advanced coatings.

PPG Industries advances electrocoat and graphene-enhanced anti-corrosion technologies

PPG Industries leads the anti-corrosion coatings market through advanced electrocoat (e-coat) systems and high-performance protective coatings. The company reported $15.9 billion in net sales in 2025, with growth driven by expansion in protective and marine coatings across APAC and North America. Its AMERLOCK® and SIGMASHIELD® product lines have gained strong traction in subsea pipeline rehabilitation, addressing over 45,000 km of aging infrastructure requiring ISO 21809 compliance. The company is introducing ECOAT 26 in 2026, focusing on automated and digital coating systems that reduce material waste by 12–15%. Investments exceeding $50 million in European manufacturing modernization support production of ultra-low VOC and chromate-free anti-corrosion coatings. Product development continues to integrate sustainability and high-performance corrosion protection technologies.

Jotun expands corrosion protection in energy and EV infrastructure with advanced coatings

Jotun A/S continues to lead in anti-corrosion coatings for marine, offshore wind, and energy infrastructure applications. The company reported revenues exceeding NOK 34 billion ($3.1 billion) in 2025, driven by strong demand from shipbuilding and renewable energy sectors. Its EV Battery Solutions include powder coatings providing dielectric insulation and C5-VH corrosion protection for battery housings in electric vehicles. Hull Skating Solutions contributed to avoiding 35.9 million tonnes of CO2 emissions in 2025 by preventing biofouling and corrosion in marine vessels. Participation in the EOLMED floating wind project includes supplying advanced 2K anti-corrosion coatings designed for harsh offshore environments. Product development continues to focus on high-performance coatings for extreme corrosion conditions.

Hempel sets benchmark in zinc-rich anti-corrosion primers with low-VOC formulations

Hempel A/S is advancing anti-corrosion coatings through high-performance zinc-rich primers and sustainability-driven strategies. The company reported €259 million in free cash flow in 2025 with an adjusted EBITDA margin of 18.2%, marking record financial performance. Its Avantguard 750 Pro primer offers corrosion protection exceeding 35 years while maintaining a low VOC content of 244 g/L, setting new industry standards. The Marine segment grew 9.8% organically to €750 million, supported by strong demand for advanced protective coatings such as Hempaguard NB. Sustainability initiatives include a 70% reduction in Scope 1 and 2 emissions compared to 2019, with a target of 90% reduction by 2026. Product innovation continues to focus on long-term durability and environmentally compliant coatings.

Sherwin-Williams enhances infrastructure coatings with fast-curing and global specification systems

Sherwin-Williams strengthens its position in anti-corrosion coatings through its Global Core product strategy targeting infrastructure and industrial applications. The company expanded its portfolio with Macropoxy® 2600 and Acrolon 7700 systems offering ISO 12944 CX-level corrosion protection with dry-to-handle times of 45 minutes. Its epoxy zinc phosphate coatings feature low-temperature curing capabilities, enabling application in sub-zero conditions without compromising adhesion or performance. The company plays a significant role in the $1.4 trillion U.S. infrastructure pipeline, supplying coatings for bridges, highways, and water management systems. Vertical integration in resin and pigment production ensures consistency in coating systems and color matching across global projects. Product development continues to align with performance reliability and application efficiency.

China Anti-Corrosion Coatings Market: Graphene Integration and Infrastructure-Driven Demand Surge

China’s anti-corrosion coatings market is witnessing rapid transformation, driven by technological advancements and large-scale infrastructure initiatives. The integration of graphene-enhanced epoxy primers is redefining coating performance by significantly improving salt-spray resistance while reducing coating thickness, making them ideal for offshore wind and marine applications. Simultaneously, the expansion of the “New Three” industries—electric vehicles, lithium-ion batteries, and solar—has increased the deployment of ultra-thin anti-corrosion coatings for battery casings, ensuring long-term durability and resistance to chemical degradation.

Massive infrastructure programs such as the Belt and Road Initiative are fueling demand for heavy-duty coatings across rail bridges, ports, and industrial corridors. Regulatory updates enforcing stricter VOC limits are accelerating the transition toward water-borne and powder-based anti-corrosion coatings. In addition, innovations such as self-healing polyurea coatings are improving maintenance efficiency in subsea pipelines, while increased adoption of CUI-mitigation coatings in petrochemical hubs is strengthening asset reliability in critical industrial environments.

United States Anti-Corrosion Coatings Market: Infrastructure Rehabilitation and Smart Coating Technologies

The United States anti-corrosion coatings market is expanding steadily, supported by infrastructure rehabilitation programs and continuous innovation in protective coating technologies. Government-backed investments in bridge repair and water infrastructure modernization are driving strong demand for zinc-rich primers and advanced corrosion-resistant coatings designed to extend asset lifespans in harsh environments.

Technological advancements are playing a pivotal role in market evolution. The development of cermet coatings applied through high-velocity processes is enhancing the durability of industrial equipment, particularly in oil and gas operations. At the same time, innovations such as smart sensing coatings are enabling real-time monitoring of coating integrity, improving maintenance efficiency and asset management. Stringent environmental regulations are also accelerating the shift toward safer, chrome-free formulations, reinforcing the market’s transition toward sustainable and high-performance anti-corrosion coating solutions.

India Anti-Corrosion Coatings Market: Petrochemical Expansion and Domestic Manufacturing Acceleration

India’s anti-corrosion coatings market is gaining strong momentum, driven by rapid industrialization and government-led initiatives promoting domestic manufacturing. Significant investments under national development programs are boosting the production of high-performance resins and coating materials, reducing reliance on imports and strengthening the local supply chain.

Infrastructure expansion projects, particularly in transportation and coastal development, are increasing the demand for advanced protective coatings such as fusion-bonded epoxy systems for reinforced steel structures. Innovations tailored to regional climatic conditions, including coatings capable of application in high-humidity environments, are addressing operational challenges. Additionally, the growth of chemical and fertilizer industries is driving demand for specialized coatings used in storage tanks and industrial equipment. Strategic collaborations in the defense sector are further supporting the development of advanced anti-corrosion and anti-fouling coating technologies.

Germany Anti-Corrosion Coatings Market: Bio-Based Resins and Hydrogen Infrastructure Protection

Germany’s anti-corrosion coatings market is characterized by its strong focus on sustainability, regulatory compliance, and advanced material innovation. The transition toward bio-based acrylic and epoxy resins is significantly reducing the carbon footprint of industrial coatings while maintaining high levels of durability and performance. Strict adherence to environmental regulations is also driving the adoption of safer formulations, eliminating hazardous substances from protective coating systems.

The country’s commitment to energy transition initiatives is creating substantial demand for anti-corrosion coatings in hydrogen infrastructure, including pipelines and electrolyzers. Technological advancements such as low-temperature curing powder coatings are improving energy efficiency in industrial processes. Additionally, investments in infrastructure renovation are driving the use of high-performance coatings for waterways and transportation systems. The implementation of digital tracking systems for coating lifecycle management is further enhancing transparency and sustainability across the value chain.

South Korea Anti-Corrosion Coatings Market: Shipbuilding Leadership and Advanced Antifouling Technologies

South Korea remains a global leader in the anti-corrosion coatings market, supported by its dominant shipbuilding industry and continuous technological innovation. The demand for advanced coatings is particularly strong in LNG carrier construction, where cryogenic-stable coatings are essential for maintaining structural integrity under extreme conditions.

Innovations in antifouling technologies, including bio-mimetic nano-coatings, are improving vessel efficiency by reducing drag and corrosion simultaneously. The integration of robotic application systems in shipyards is enhancing coating precision and operational efficiency. Regulatory frameworks promoting low-emission solutions are accelerating the adoption of solvent-free epoxy systems, while investments in advanced research facilities are supporting the development of next-generation silicone-based coatings. Growing offshore energy projects are also contributing to increased demand for durable protective coatings in subsea and marine environments.

Brazil Anti-Corrosion Coatings Market: Mining Operations and Offshore Energy Driving High-Performance Coatings

Brazil’s anti-corrosion coatings market is experiencing strong growth, driven by its mining and offshore oil and gas sectors. Heavy-duty industrial operations require highly durable coatings capable of withstanding extreme abrasion and corrosive environments, leading to widespread adoption of ceramic-epoxy liners in mining infrastructure.

Investments in manufacturing capacity and infrastructure development are further supporting market expansion. Technological advancements such as cold spray repair techniques are improving maintenance efficiency in offshore platforms, reducing downtime and operational costs. Regulatory updates are enforcing stricter standards for protective coatings in marine environments, driving demand for high-performance solutions. Additionally, the development of localized nanocoating technologies is enhancing innovation and reducing dependency on imported materials, strengthening the domestic coatings industry.

Japan Anti-Corrosion Coatings Market: Hydrogen Economy and Smart Infrastructure Innovations

Japan’s anti-corrosion coatings market is evolving rapidly, driven by advancements in material science and strong government support for sustainable infrastructure. The development of coatings capable of withstanding cryogenic temperatures is critical for hydrogen storage and transportation systems, positioning Japan at the forefront of next-generation energy technologies.

Technological innovations such as photocatalytic coatings are improving durability and reducing maintenance requirements in architectural applications. High-performance fluoropolymer coatings are extending the lifespan of critical infrastructure such as bridges and transportation systems. Additionally, the integration of smart sensors within coating systems is enabling real-time monitoring of structural health, enhancing maintenance efficiency. Regulatory shifts toward environmentally friendly formulations are further accelerating the adoption of advanced anti-corrosion coating solutions across industries.

Anti-Corrosion Coatings Market Report Scope

Anti-Corrosion Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$37.5 Billion

|

|

Market Size (2032)

|

$52.4 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Resin (Epoxy, Polyurethane, Acrylic, Alkyd, Zinc-Rich Coatings, Chlorinated Rubber, Others), By Technology (Solvent-borne, Water-borne, Powder Coatings, UV-Cured and Radiation Curable Systems), By End-Use Industry (Oil and Gas, Marine, Infrastructure, Power Generation, Industrial Manufacturing, Automotive and Transportation, Aerospace and Defense, Water and Wastewater Treatment), By Coating Layer (Primers, Intermediate Coats, Topcoats), By Corrosivity Category (Low to Medium Corrosivity, High to Very High Corrosivity, Extreme Marine), By Performance Function (Barrier Coatings, Galvanic Coatings, Inhibitive Coatings, Advanced Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, Jotun A/S, Hempel A/S, Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., BASF SE, RPM International Inc., Sika AG, Chugoku Marine Paints, Ltd., Asian Paints Limited, Tnemec Company, Inc., Wacker Chemie AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anti-Corrosion Coatings Market Segmentation

By Resin

- Epoxy

- Polyurethane

- Acrylic

- Alkyd

- Zinc-Rich Coatings

- Chlorinated Rubber

- Others

By Technology

- Solvent-borne

- Water-borne

- Powder Coatings

- UV-Cured and Radiation Curable Systems

By End-Use Industry

- Oil and Gas

- Marine

- Infrastructure

- Power Generation

- Industrial Manufacturing

- Automotive and Transportation

- Aerospace and Defense

- Water and Wastewater Treatment

By Coating Layer

- Primers

- Intermediate Coats

- Topcoats

By Corrosivity Category

- Low to Medium Corrosivity

- High to Very High Corrosivity

- Extreme Marine

By Performance Function

- Barrier Coatings

- Galvanic Coatings

- Inhibitive Coatings

- Advanced Coatings

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Anti corrosion Coatings Market

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Jotun A/S

- Hempel A/S

- Axalta Coating Systems Ltd.

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- BASF SE

- RPM International Inc

- Sika AG

- Chugoku Marine Paints, Ltd.

- Asian Paints Limited

- Tnemec Company, Inc.

- Wacker Chemie AG

*- List not Exhaustive

Table of Contents: Anti-Corrosion Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Anti-Corrosion Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Anti-Corrosion Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Growth Drivers: Infrastructure Protection and Asset Lifecycle Extension

2.4. Regulatory Trends and Shift Toward Sustainable Coatings

2.5. Industrial Expansion and Demand Across Marine and Energy Sectors

3. Innovations Reshaping the Anti-Corrosion Coatings Market

3.1. Trend: Mega-Mergers, Smart Coatings, and Capacity Expansion

3.2. Trend: Graphene-Enhanced Epoxy Primers Replacing Zinc-Rich Systems

3.3. Opportunity: Offshore Wind Corrosion Management and Lifecycle Coatings

3.4. Opportunity: Green Hydrogen Applications and Self-Healing Coatings

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Anti-Corrosion Coatings Market

5.1. By Resin

5.1.1. Epoxy

5.1.2. Polyurethane

5.1.3. Acrylic

5.1.4. Alkyd

5.1.5. Zinc-Rich Coatings

5.1.6. Chlorinated Rubber

5.1.7. Others

5.2. By Technology

5.2.1. Solvent-borne

5.2.2. Water-borne

5.2.3. Powder Coatings

5.2.4. UV-Cured and Radiation Curable Systems

5.3. By End-Use Industry

5.3.1. Oil and Gas

5.3.2. Marine

5.3.3. Infrastructure

5.3.4. Power Generation

5.3.5. Industrial Manufacturing

5.3.6. Automotive and Transportation

5.3.7. Aerospace and Defense

5.3.8. Water and Wastewater Treatment

5.4. By Coating Layer

5.4.1. Primers

5.4.2. Intermediate Coats

5.4.3. Topcoats

5.5. By Corrosivity Category

5.5.1. Low to Medium Corrosivity

5.5.2. High to Very High Corrosivity

5.5.3. Extreme Marine

5.6. By Performance Function

5.6.1. Barrier Coatings

5.6.2. Galvanic Coatings

5.6.3. Inhibitive Coatings

5.6.4. Advanced Coatings

6. Country Analysis and Outlook of Anti-Corrosion Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Anti-Corrosion Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Anti-Corrosion Coatings Market Size Outlook to 2032

7.1.1. By Resin

7.1.2. By Technology

7.1.3. By End-Use Industry

7.1.4. By Coating Layer

7.1.5. By Corrosivity Category

7.1.6. By Performance Function

7.2. Europe Anti-Corrosion Coatings Market Size Outlook to 2032

7.2.1. By Resin

7.2.2. By Technology

7.2.3. By End-Use Industry

7.2.4. By Coating Layer

7.2.5. By Corrosivity Category

7.2.6. By Performance Function

7.3. Asia Pacific Anti-Corrosion Coatings Market Size Outlook to 2032

7.3.1. By Resin

7.3.2. By Technology

7.3.3. By End-Use Industry

7.3.4. By Coating Layer

7.3.5. By Corrosivity Category

7.3.6. By Performance Function

7.4. South America Anti-Corrosion Coatings Market Size Outlook to 2032

7.4.1. By Resin

7.4.2. By Technology

7.4.3. By End-Use Industry

7.4.4. By Coating Layer

7.4.5. By Corrosivity Category

7.4.6. By Performance Function

7.5. Middle East and Africa Anti-Corrosion Coatings Market Size Outlook to 2032

7.5.1. By Resin

7.5.2. By Technology

7.5.3. By End-Use Industry

7.5.4. By Coating Layer

7.5.5. By Corrosivity Category

7.5.6. By Performance Function

8. Company Profiles: Leading Players in the Anti-Corrosion Coatings Market

8.1. PPG Industries, Inc.

8.2. Akzo Nobel N.V.

8.3. The Sherwin-Williams Company

8.4. Jotun A/S

8.5. Hempel A/S

8.6. Axalta Coating Systems Ltd.

8.7. Nippon Paint Holdings Co., Ltd.

8.8. Kansai Paint Co., Ltd.

8.9. BASF SE

8.10. RPM International Inc

8.11. Sika AG

8.12. Chugoku Marine Paints, Ltd.

8.13. Asian Paints Limited

8.14. Tnemec Company, Inc.

8.15. Wacker Chemie AG

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures