Market Overview: Anti Crease Agent Market to Reach $1.9 Billion by 2034 as Non-Formaldehyde Chemistry, Bio-Based Finishes, and Water-Efficient Processing Redefine Textile Performance

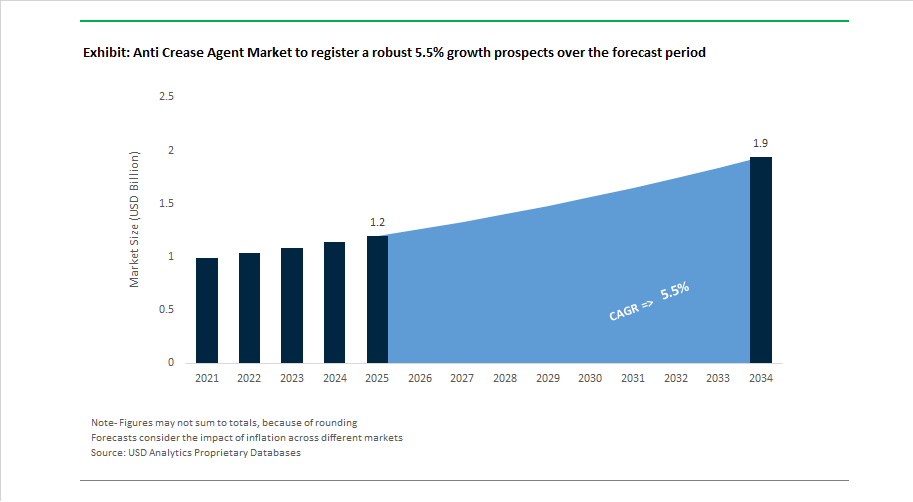

The global anti crease agent market is projected to grow from $1.2 billion in 2025 to $1.9 billion by 2034, registering a 5.5% CAGR driven by rising demand for wrinkle-resistant textiles, easy-care finishes, durable press treatments, and fabric stabilization technologies. Anti-crease agents are critical in apparel, home textiles, technical fabrics, and performance wear, where they reduce fiber deformation, enhance dimensional stability, and maintain garment aesthetics through multiple wash cycles. Market expansion is shaped by the transition away from formaldehyde-based resins, increasing adoption of bio-based lubricants, silicone crosslinkers, and non-toxic finishing agents, and the textile industry’s shift toward water-saving and zero-liquid-discharge processing. Regulatory alignment with REACH and global sustainability frameworks is accelerating reformulation toward low-emission and biodegradable chemistries.

Sustainability-focused innovation gained visibility in 2024 when Tanatex Chemicals received recognition for circular economy initiatives supporting anti-crease lubrication systems. Bio-inspired chemistry advanced in March 2025 as Rudolf Group launched fluorine-free finishing technologies improving structural fabric resilience. Environmental performance improvements emerged in mid-2025 when Nestor introduced a bio-based anti-crease agent with a lower carbon footprint. Research breakthroughs followed in August 2025 as NC State University demonstrated epoxidized cottonseed oil as a green wrinkle-resistance alternative. Regulatory-compliant finishing technologies were highlighted in October 2025 when Archroma presented non-formaldehyde easy-care resins and later launched SILIGEN D2W LIQ C silicone softener for durable smoothness.

Industry modernization accelerated in December 2025 as the CHT Group earned sustainability recognition and Indian firms Fineotex and Sarex advanced zero-water discharge auxiliaries for foam-based finishing. Water-efficiency innovation strengthened in 2025 with Centro Chino developing cationic formulations reducing wash water usage. Market consolidation occurred in February 2026 when Pulcra Chemicals acquired Devan, expanding its portfolio in wrinkle-reduction and functional textile finishes. Product innovation continued in January 2026 with Pulcra’s STABIFIX NBF fixing agent enhancing fabric stability in synthetic fibers. Leadership transitions at Huntsman Corporation during December 2025 aligned the company’s specialty amine chemistry with evolving textile auxiliary needs.

Trends and Opportunities Transforming the Anti Crease Agent Market

Regulatory Pressure Is Eliminating Formaldehyde-Based Chemistries From Market Access

The Anti Crease Agent market is undergoing a forced transition, where compliance rather than consumer preference is dictating reformulation strategies across textile finishing operations. The most visible disruption is the replacement of Dimethylol Dihydroxyethyleneurea (DMDHEU) and related formaldehyde-releasing chemistries, triggered by human carcinogenic classification. Under the EU Ecodesign for Sustainable Products Regulation (ESPR) finalized in mid-2025, these substances are now classified as Substances of Concern (SoCs) and must be digitally declared via Digital Product Passports. Textile processors serving EU import and export channels are therefore shifting toward BTCA (1,2,3,4-Butanetetracarboxylic Acid) cross-linkers, which deliver non-formaldehyde wrinkle recovery while maintaining market access under EU rules.

Post-regulatory performance has also become an EEAT metric. OEKO-TEX Standard 100 (effective April 1, 2025) tightened residual limits for Category I textile products (infants), accelerating adoption of citric acid and polycarboxylic acid blends, which now achieve WRA >210° without VOC emissions and without the historically punitive tear-strength loss. Peer-reviewed technical datasets (2025) confirm BTCA finishes retain 90.5% of original tear strength when combined with optimized catalysts such as sodium hydroxide, enabling mills to scale formaldehyde-free finishing without fabric integrity compromise.

Shift Toward Multi-Functional, Value-Rich Finishes in Travel, Sportswear and Performance Apparel

Brand portfolios are no longer seeking anti-crease effects alone. Sportswear, travel apparel, and athleisure categories are now sourcing “Smart Finish” chemistries that integrate wrinkle resistance with moisture-wicking, odor-resistance, and low-maintenance ironing elimination. Between 2024–2025, Archroma expanded ARKOFIX® formulations to pair anti-crease treatments with moisture-management systems such as HYDROPERM®, allowing garments to remain crisp and dry through multi-day use—a direct consumer value for airline travelers and commuters.

Technical synergies are advancing commercial differentiation. Nano-encapsulation platforms introduced in late-2024 allow anti-crease coatings to act as carrier matrices for silver-free antimicrobial actives, enabling dual-function odor control triggered by heat or friction. Mill data indicates that garments finished with these multifunctional blends reduce laundering frequency, contributing to 20% household water and energy reduction, aligning with ZDHC wastewater goals and brand-level sustainability scorecards. This creates pricing power for chemical manufacturers who provide measurable sustainability-indexed textile auxiliaries.

Durable Anti-Crease Systems Tailored for Recycled Polyester (rPET) and Circular Blends

As the textile sector moves toward 45% recycled polyester share by 2025 under the Textile Exchange Recycled Polyester Challenge, anti-crease chemistry is becoming a compliance enabler for circular textiles. rPET fibers exhibit surface inconsistency and reduced uniformity, making them prone to post-wash “bagging” and crease formation. Specialty polymeric anti-crease agents utilizing esterification bonding mechanisms are being engineered to create durable cross-links between cellulosic fibers and rPET, enabling premium drape consistency in rPET-cotton blends.

The commercial implication is scale: more than 130+ global brands committed to rPET transitions now require bluesign® APPROVED auxiliaries to meet Black Limits (BSBL) for restricted substances. Suppliers of anti-crease agents who can provide documentation for closed-loop, chemically recycled polyester compatibility will become the primary beneficiaries of procurement restructuring in 2025-2027.

High-Durability Finishes for Technical Workwear and Healthcare Sterilization Textiles

Technical workwear and clinical protective apparel are emerging as the highest-margin adoption zone for Anti Crease Agents. Healthcare textiles require finishes that survive 75+ autoclave sterilization cycles without degradation of barrier layers or professional appearance. Anionic heavy-duty anti-crease systems, such as Sarex Anticrease Conc, form a low-friction protective film that prevents chaffing and crease locking during wet-heat sterilization.

Workwear for cleanrooms and high-risk industrial facilities demands anti-crease finishes that retain integrity under acidic or alkaline exposure and withstand up to 180°C curing, ensuring that wrinkle resistance does not compromise ISO 20743 antimicrobial compatibility or protective coatings. As cleanroom expansions in semiconductor, battery, and biologics manufacturing add millions of square meters of workwear demand by 2026, suppliers positioned with dual-certified antimicrobial-compatible anti-crease agents can capture long-term supply contracts that command pricing premiums over commodity auxiliaries.

Anti Crease Agent Market Share and Segmentation Insights

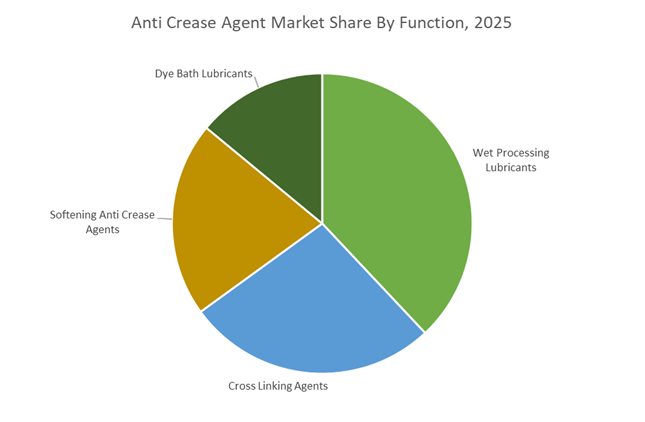

Market Share by Function: Wet Processing Lubricants Lead Volume While Formaldehyde-Free Crosslinkers Accelerate

Wet processing lubricants account for approximately 38% of the global anti crease agent market in 2025, making them the largest functional category. These preventive anti-crease chemicals are critical in bleaching, scouring, and jet dyeing operations, where they reduce fiber-to-fiber and fiber-to-metal friction, preventing rope marks, crack marks, and thermo-migration creasing in polyester and blended fabrics. Demand remains steady at 4 to 5% annually, aligned with synthetic fiber processing volumes. Cross linking agents rank second but represent the highest-value segment and the fastest-growing, as formaldehyde-free durable press resins replace conventional DMDHEU under OEKO-TEX and ZDHC compliance frameworks. Softening anti crease agents combine lubrication and hand-feel enhancement in knitwear and compact processing. Dye bath lubricants form the smallest but technically advanced niche, supporting high-temperature polyester dyeing and regenerated cellulosic fiber protection.

Market Share by End-Use Industry: Apparel Dominates as Technical Textiles Expand Rapidly

Apparel represents roughly 58% of anti crease agent consumption in 2025, encompassing woven shirts, denim, knitwear, and polyester activewear where wrinkle resistance and crease prevention are essential during wet processing and finishing. Production hubs across Bangladesh, Vietnam, India, and China drive volume, while sustainability mandates from global brands accelerate adoption of compliant, formaldehyde-free finishing chemistries. Home textiles rank second, serving bed linens, towels, curtains, and upholstery that require dimensional stability and durable press performance, particularly in hospitality and healthcare laundry cycles. Technical textiles are the fastest-growing segment, supported by automotive interior fabrics, flame-retardant protective clothing, geotextiles, and medical textiles requiring high-performance crosslinking and low-yellowing finishes. This segment is less price-sensitive and increasingly specification-driven, benefiting from automotive recovery and medical textile expansion.

Anti Crease Agent Market Competitive Landscape

The global anti crease agent market is being reshaped by sustainability mandates, formaldehyde-free finishing chemistries, and rising demand for durable easy-care textiles across apparel, home furnishings, automotive interiors, and technical fabrics. Leading suppliers are competing on silicone-based softeners, biodegradable lubricants, digital-print compatibility, and low-energy wet-processing systems. Capacity expansions in Asia, eco-certified auxiliaries (ZDHC, GOTS, Bluesign), and integrated “wet-process-to-finish” platforms are redefining mill efficiency. Market leadership increasingly depends on water and energy reduction, wrinkle-resistance durability over 50+ wash cycles, and multifunctional formulations that combine anti-crease performance with softness, color retention, and fiber protection.

Sustainable textile systems position Archroma as the global benchmark

Archroma dominates the premium anti crease agent segment following the integration of Huntsman Textile Effects, anchoring its leadership in Planet Conscious textile chemistry. Its AVITERA® SE and SILIGEN® portfolios, particularly SILIGEN® D2W (2025–2026), resolve the long-standing softness-versus-absorbency trade-off using advanced silicone technology. At Colombiatex 2026, Archroma showcased bundled anti-crease and High IQ® Lasting Color programs to extend garment life cycles. Through its Super-System approach, mills can cut water and energy use by up to 50%. The company’s strategic focus on formaldehyde-free crosslinking ensures wrinkle resistance even after 50+ industrial washes, supporting circular fashion and premium workwear.

Silicone-led auxiliaries drive CHT Group’s smart processing advantage

CHT Group specializes in silicone chemistry and intelligent textile auxiliaries designed to reduce mechanical stress during high-speed processing. Its BIAVIN series, including BIAVIN TCC and BIAVIN 109, delivers high glide properties that minimize abrasion marks and crease formation in wet operations. Recently scaled biodegradable, non-ionic lubricants meeting ZDHC MRSL Level 3 standards address sensitive cellulose and elastane blends. CHT’s solutions span automotive interiors, medical stockings, and luxury home textiles. Strategically, the company is transitioning toward a circular economy model by 2026, advancing Cradle-to-Cradle-aligned auxiliaries derived increasingly from renewable raw materials.

Functional finishing leadership defines Rudolf Group’s eco-performance positioning

Rudolf Group excels in functional finishing where performance meets ecological responsibility. In 2025, it launched phenol- and bisphenol-free fixing and anti-crease agents, removing hazardous precursors from dye-bath lubrication. Its RUCO-LUBE and RUCON series are widely used in denim and outdoor wear, preventing “crow’s feet” during garment dyeing through superior fiber-to-metal lubrication. Rudolf’s HypNO Technology and rPET-based polymers integrate anti-crease effects into denim bleaching with minimal water usage. The company is advancing bio-based moisture management, leveraging plant extracts and biological waste to maintain fabric breathability while delivering wrinkle resistance.

Digital-print optimization strengthens Tanatex Chemicals’s specialty coatings portfolio

Part of Transfar Group, Tanatex focuses on future-proof functional coatings and process optimization. Its TANALUBE® and PERSOFTAL® ranges, especially TANALUBE® FF, increase dyebath viscosity to reduce fiber friction and creasing. Tanatex brings deep expertise in Digital Pigment Printing via its Toolbox initiative, where anti-crease agents ensure fabric flatness for precision printing. Expansion of its Green Mission across Southeast Asia in 2025–2026 supports Bluesign-approved crease inhibitors for sportswear. Tanatex is a recognized specialist in man-made fibers, offering tailored solutions for polyester and nylon blends under high-temperature processing.

Processing excellence differentiates Pulcra Chemicals in high-speed finishing

Pulcra Chemicals targets processing excellence by developing anti-crease agents that also act as fiber-protective lubricants, safeguarding delicate cotton and silk during high-speed manufacturing. In 2025, Pulcra intensified its Smart Chemistry focus on wrinkle-free workwear and uniforms within the garment washing segment. The company’s strength lies in customization, providing site-specific formulations adapted to varying water hardness and machine conditions. Its portfolio of non-ionic and anionic lubricants is compatible with diverse dyes and finishing agents, preventing bath instability while ensuring consistent crease prevention across medium-to-large textile operations.

High-volume Asian supply anchors Sarex Chemicals’s global reach

Sarex Chemicals represents the value-driven backbone of the anti crease agent market in Asia, supplying REACH-compliant and GOTS-approved auxiliaries to global fast-fashion brands. With massive manufacturing scale in India, Sarex dominates garment washing and fabric finishing through easy-care resins that maintain a pressed appearance with minimal ironing. In late 2025, it expanded Sarakol and Lubril lines with concentrated grades to reduce shipping volumes and logistics emissions. Sarex operates extensive Technical Service Centers across Asia, enabling mills to optimize dosage by fiber type and machine configuration, reinforcing its leadership in cost-effective, high-throughput textile finishing.

China Anti Crease Agent Market: Circular Chemistry and Process Compression Drive Scale Adoption

China’s anti crease agent ecosystem is being reshaped by circular chemistry integration and national textile sustainability mandates. In January 2025, BASF inaugurated its first commercial loopamid® production facility at Caojing, Shanghai. While the plant is centered on nylon circularity, it also supplies integrated amine intermediates that are increasingly used in non-yellowing, next-generation anti-crease finishing agents. This Verbund-scale integration strengthens China’s ability to supply high-purity auxiliaries aligned with export market compliance.

Policy support is accelerating downstream adoption. Under the 2025–2030 Sustainable Textile Roadmap, formaldehyde-free cross-linking systems have been incentivized, resulting in a marked increase in citric-acid-based anti-wrinkle finishes across Jiangsu textile clusters. Export-oriented mills have also shifted toward AOS-based anti-crease lubricants to comply with updated Global Recycled Standard and European REACH requirements. Domestic innovators such as Dymatic Chemicals are pivoting toward water-based polyurethane anti-crease dispersions, while Guangdong mills are deploying single-bath scouring and dyeing systems that cut total processing time significantly. MIIT-backed funding in 2025 further supported nanotechnology-enabled anti-crease coatings that preserve breathability while improving durable press ratings.

India Anti Crease Agent Market: PLI-Driven Specialization and Water-Efficient Formulations

India’s anti crease agent market is evolving through targeted policy incentives and strong domestic innovation. The Production-Linked Incentive Scheme 2.0 for textiles, operationalized in 2025, explicitly prioritizes technical textiles, including high-performance permanent press finishes for defense, healthcare, and institutional apparel. This has encouraged suppliers to move beyond commodity lubricants toward engineered anti-crease auxiliaries with defined performance benchmarks.

Product innovation remains central. Fineotex Chemical Limited introduced bio-derived anti-crease agents in late 2024 designed to deliver soft hand feel and improved biodegradability for premium cotton exports. In parallel, Sarex Chemicals launched a dye-bath lubricant and anti-crease formulation capable of operating across extreme pH conditions, enabling more flexible wool and polyester blend processing. Capacity investments support this shift, with Resil Chemicals completing a dedicated expansion in 2025 for silicone emulsions that combine wrinkle resistance with moisture management. Regulatory pressure from stricter ZLD norms in Tamil Nadu has further increased demand for high-exhaustion anti-crease agents that reduce water and effluent loads.

Germany Anti Crease Agent Market: Precision Chemistry and Regulatory Benchmarking

Germany continues to define the premium end of the anti crease agent industry through precision chemistry and regulatory leadership. In 2025, Archroma received the ITMF Sustainability and Innovation Award for its Denim Halo process, which minimizes creasing and mechanical stress during laser denim finishing. This reflects a broader shift toward pre-treatment solutions that protect fabric integrity while supporting advanced finishing techniques.

German laboratories are also pushing durability boundaries. Patent-pending micro-x cross-linking systems demonstrated in late 2025 create stable silicone networks within cellulosic fibers, maintaining anti-crease performance through repeated industrial laundering. Pulcra Chemicals reported the launch of anti-crease agents that significantly enhance tear resistance, extending garment life in fast-fashion supply chains. Regulatory enforcement under the 2025 Supply Chain Act has accelerated the phase-out of traditional DMU resins in favor of low-formaldehyde DMDHEU systems. Complementing this, Tanatex Chemicals commercialized TANALUBE® FF, meeting BlueSign and GOTS 7.0 requirements and reinforcing Germany’s leadership in biodegradable textile auxiliaries.

United States Anti Crease Agent Market: Bio-Carbon Inputs and Modular Production Models

The United States anti crease agent market is characterized by bio-carbon innovation and flexible manufacturing models. New textile technology centers opened in 2024–2025, including facilities operated by the American Textile Company, are focusing on digitally enabled finishing systems that incorporate smart anti-crease additives for e-commerce-driven apparel production. These centers support rapid prototyping and shorter product cycles for brands targeting wrinkle-resistant casualwear.

Material innovation is advancing in parallel. Huntsman Corporation expanded its PHOBOTEX® portfolio in 2025 to include bio-based anti-crease components with significant renewable carbon content, aimed at outdoor and performance wear. The launch of Aegis® CR silicone emulsions further reduced reliance on high-heat ironing by delivering durable wrinkle resistance at lower energy use. Facing volatile demand, U.S. producers are increasingly adopting modular blending assets, enabling fast customization of anti-crease formulations for boutique and small-batch apparel brands.

Country-Level Strategic Positioning in the Anti-Crease Agent Industry

Anti-Crease Agent Market County Level Snapshot

|

Country

|

Core Strategic Focus

|

Industry Implication

|

|

China

|

Circular chemistry and single-bath processing

|

Scaled adoption of formaldehyde-free, multifunctional agents

|

|

India

|

PLI-driven innovation and water efficiency

|

Growth in bio-based, high-exhaustion anti-crease auxiliaries

|

|

Germany

|

Precision cross-linking and regulatory leadership

|

Benchmark for durable, low-formaldehyde performance

|

|

United States

|

Bio-carbon inputs and modular manufacturing

|

Flexible, energy-saving anti-crease solutions for premium apparel

|

Anti-Crease Agent Market Report Scope

Anti Crease Agent Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.2 Billion

|

|

Market Size (2034)

|

$1.9 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Type (Resin Based Anti Crease Agents, Non Resin Based Anti Crease Agents, Silicone Based Emulsions, Polyurethane Based Dispersions, Bio Polymer Based Agents), By Function (Dye Bath Lubricants, Cross Linking Agents, Wet Processing Lubricants, Softening Anti Crease Agents), By Fiber Type (Natural Fibers, Synthetic Fibers, Blended Fibers), By Application Method (Exhaust Method, Padding and Continuous Method, Spraying and Fogging), By End Use Industry (Apparel, Home Textiles, Technical Textiles)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huntsman International LLC, Archroma, BASF SE, Pulcra Chemicals, Tanatex Chemicals, Rudolf Group, Fineotex Chemical Limited, Sarex Chemicals, Dymatic Chemicals, Evonik Industries AG, Dow Inc, Transfar Chemicals Group, Resil Chemicals, Siam Pro Dyechem Group, Golden Technologia

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anti Crease Agent Market Segmentation

By Product Type

- Resin Based Anti Crease Agents

- Non Resin Based Anti Crease Agents

- Silicone Based Emulsions

- Polyurethane Based Dispersions

- Bio Polymer Based Agents

By Function

- Dye Bath Lubricants

- Cross Linking Agents

- Wet Processing Lubricants

- Softening Anti Crease Agents

By Fiber Type

- Natural Fibers

- Synthetic Fibers

- Blended Fibers

By Application Method

- Exhaust Method

- Padding and Continuous Method

- Spraying and Fogging

By End Use Industry

- Apparel

- Home Textiles

- Technical Textiles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Anti Crease Agent Industry

- Huntsman International LLC

- Archroma

- BASF SE

- Pulcra Chemicals

- Tanatex Chemicals

- Rudolf Group

- Fineotex Chemical Limited

- Sarex Chemicals

- Dymatic Chemicals

- Evonik Industries AG

- Dow Inc

- Transfar Chemicals Group

- Resil Chemicals

- Siam Pro Dyechem Group

- Golden Technologia

*- List not Exhaustive