Anti-Reflective Coatings Market Size and Growth Accelerated by Solar Efficiency and Optical Precision Demand

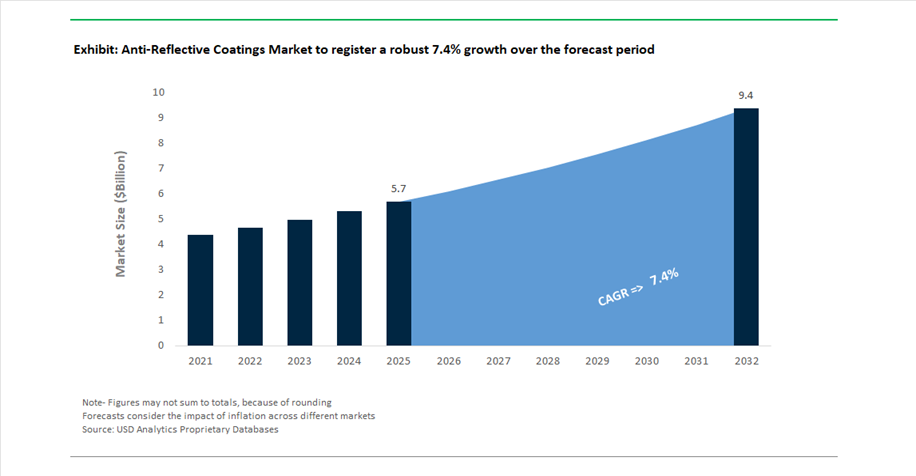

The Anti-Reflective Coatings (ARC) Market is projected to grow from USD 5.7 billion in 2025 to USD 9.4 billion by 2032, registering a strong CAGR of 7.4%. This growth is primarily driven by increasing demand for enhanced light transmission and reduced reflectance across high-value applications such as solar photovoltaic (PV) systems, eyewear, consumer electronics, and precision optics.

Anti-reflective coatings are engineered to minimize surface reflection and maximize light absorption, significantly improving the efficiency of optical systems. In the solar energy sector, ARC plays a critical role in boosting PV panel output, enabling higher energy conversion rates by reducing light loss. As global investments in renewable energy infrastructure accelerate, particularly in large-scale solar installations, demand for advanced ARC solutions is expanding rapidly. In parallel, the eyewear industry continues to adopt high-performance multi-layer coatings to enhance visual clarity, reduce glare, and improve user comfort, particularly in premium lenses and digital-use eyewear.

Technological advancements are centered on nanometer-scale thin-film deposition, multi-layer interference coatings, and hybrid material systems, allowing manufacturers to achieve near-zero reflectivity across a wide range of wavelengths. These innovations are particularly critical in high-resolution displays, camera lenses, and augmented reality (AR) devices, where even minor reflection losses can significantly impact performance. Additionally, the integration of hydrophobic, scratch-resistant, and smudge-resistant properties is transforming ARC into a multi-functional solution.

The market is also benefiting from the rapid expansion of automotive digital displays, wearable technologies, and aerospace optics, where high contrast and visibility under varying lighting conditions are essential. Competitive dynamics are defined by intensive R&D investment, strategic collaborations with OEMs, and scaling of advanced manufacturing capabilities, positioning anti-reflective coatings as a foundational technology across modern optical and energy systems

Multi-Layer Optical Innovation, Strategic Investments, and Cross-Industry Adoption Driving ARC Market Evolution

The anti-reflective coatings market is being reshaped by advanced optical engineering, strategic industry consolidation, and rapid expansion into high-growth application areas. A notable innovation was introduced in January 2025, when Corning launched Gorilla® Armor 2, the first anti-reflective glass ceramic for flagship smartphones. Debuting on the Samsung Galaxy S25 Ultra, this material reduces reflections by up to 75%, significantly improving outdoor display readability while maintaining high scratch resistance.

In the eyewear segment, innovation is accelerating through multi-layer coating technologies. HOYA Vision Care’s Hi-Vision Meiryo coating (January 2026) delivers 56% lower reflectance compared to previous solutions, enhancing optical clarity and durability for premium lenses. Similarly, HOYA’s MiYOSMART Smooth Touch Xtreme (STX) introduces hydrophobic and anti-reflective properties tailored for active users, particularly children requiring myopia control solutions. Complementing this, EssilorLuxottica’s SWITCH innovation initiative (announced October 2025) highlights the future of AI-driven coating optimization, enabling personalized visual performance through advanced layer engineering.

Precision optics and imaging technologies are also driving innovation. Nikon’s Meso Amorphous Coat (late 2025) represents a breakthrough in reducing ghosting and flare, utilizing mesoscale particle structures to control light from multiple angles. This advancement is particularly significant for high-end camera lenses and professional imaging systems, where optical precision is critical.

Automotive and electronics applications are emerging as key growth areas. Corning’s SurfaceIQ (December 2025) addresses visibility challenges in digital vehicle cockpits, ensuring high contrast and minimal distortion under dynamic lighting conditions. At the same time, SCHOTT’s expansion of optical waveguide production in Malaysia (September 2025) supports the scaling of AR smart glasses, where nanometer-scale ARC is essential for delivering clear, high-brightness images in compact wearable devices.

Transition Toward Sol-Gel and Liquid Coating Technologies Enabling Scalable Anti-Reflective Coatings Manufacturing

The anti-reflective coatings market is witnessing a decisive shift from traditional Physical Vapor Deposition (PVD) toward sol-gel and liquid coating technologies, driven by the need for high-throughput, cost-efficient manufacturing. Vacuum-based sputtering systems, while historically dominant in optical coatings, are increasingly constrained by scalability limitations and high CAPEX requirements. In contrast, sol-gel processing enables atmospheric-pressure deposition across large-area substrates and complex geometries, making it highly suitable for flexible electronics, consumer displays, and architectural glass applications. This transition is strengthening the adoption of advanced anti-reflective coatings in high-volume electronics manufacturing and industrial-scale glass processing.

From a performance standpoint, modern multi-layer sol-gel coatings have reached parity with premium vacuum-deposited coatings, achieving up to 99.8% light transmittance. This benchmark, validated by leading manufacturers such as AGC Inc. and Saint-Gobain, is accelerating commercialization across cost-sensitive applications such as smartphones, solar glass, and automotive displays. Additionally, chemical innovation led by BASF SE is enabling hybrid silica-fluoropolymer nanoparticle systems, delivering multifunctional surfaces that combine anti-reflective performance, photocatalytic self-cleaning, and superhydrophobicity. These integrated functionalities are difficult to achieve using conventional vacuum deposition, reinforcing the strategic importance of liquid-phase coating platforms in next-generation optical materials.

EU EPBD Regulations Driving Demand for High-Performance Anti-Reflective Architectural Glass

The implementation of the Energy Performance of Buildings Directive (EPBD) Recast (EU 2024/1275) is fundamentally reshaping demand dynamics within the architectural glass and anti-reflective coatings market. With a mandated 16% reduction in primary energy consumption for residential buildings by 2030, AR coatings are emerging as a critical enabler for improving visible light transmittance (VLT) and optimizing solar heat gain. This allows buildings to reduce dependency on artificial lighting and heating, directly aligning with energy efficiency and sustainability goals across the European construction sector.

The directive further introduces a “Zero-Emission Buildings” requirement by 2028 for all new public infrastructure, necessitating widespread adoption of high-performance insulating glass units (IGUs). Industry organizations such as Glass for Europe emphasize that anti-reflective coatings are essential to upgrade existing building stock, particularly the lowest-performing 16% segment, to meet compliance thresholds. With EU Member States required to transpose EPBD regulations into national law by May 2026, the market is poised for a surge in demand for AR-coated architectural glass, particularly within deep renovation projects and retrofit-driven energy efficiency upgrades.

Emerging Secondary Market for Anti-Reflective Coatings in Photovoltaic Module Repair and Lifecycle Extension

A significant growth opportunity in the anti-reflective coatings industry is emerging from the aging global photovoltaic (PV) infrastructure. As early-generation solar installations approach their 20–25 year lifecycle, degraded AR coatings are contributing to measurable efficiency losses. Studies highlighted by PV Magazine indicate that reflection losses from worn coatings can reach up to 4%, while re-application of advanced AR coatings can restore energy output by approximately 5.5% and reduce the Levelized Cost of Energy (LCOE) by 2.7%. This positions AR coating re-application as a high-impact, cost-effective intervention in solar asset management.

The scale of this opportunity is reinforced by data from the National Renewable Energy Laboratory (NREL), which reported over 235 GWdc of installed PV capacity in the U.S. by late 2025, with 80% deployed within the past seven years. This creates a predictable “maintenance wave” beginning around 2030, where spray-on sol-gel AR coatings will be critical for extending module lifespan. Furthermore, circular economy initiatives in solar energy are promoting repair over disposal, with AR coatings playing a dual role as both optical enhancers and protective sealants to prevent polymer degradation and mitigate trace metal leaching in aging modules.

Advanced Anti-Reflective Coatings for AR Waveguides Powering Spatial Computing and Enterprise Applications

The evolution of augmented reality (AR) technologies is unlocking a high-value application segment for anti-reflective coatings, particularly in waveguide optics used in spatial computing systems. At Meta Connect 2025, Meta Platforms, Inc. introduced its “Oryon” AR prototype featuring silicon carbide-based waveguides integrated with advanced AR coatings. These coatings are engineered to minimize light leakage, eliminate visual artifacts such as “eye glow” and the “rainbow effect,” and maintain display clarity under high ambient light conditions, addressing core limitations in next-generation AR devices.

Enterprise adoption is also accelerating, with companies like Microsoft Corporation and Magic Leap, Inc. focusing on high-transparency waveguides for applications such as surgical visualization and industrial remote assistance. These use cases demand ultra-low surface reflectance below 0.15% across the visible spectrum, combined with enhanced brightness and wide field-of-view (FOV). Additionally, the convergence of AI-enabled wearables and AR, exemplified by smart glasses platforms such as the Meta Ray-Ban series, is integrating adaptive lens technologies with AR coatings to ensure consistent visual performance across dynamic lighting conditions. This convergence is expected to significantly scale the consumer AR optics market by 2026, positioning anti-reflective coatings as a foundational technology in wearable computing ecosystems.

Dielectric Multi-Layer Coatings Capture 51% Share with Ultra-Low Reflectivity in Precision Optics Applications

Material Chemistry Analysis: Dielectric AR Coatings Lead with Broadband and V-Coat Dominance

Dielectric coatings hold a commanding 51.0% share of the anti-reflective (AR) coatings market in 2025, driven by their unmatched ability to achieve near-zero reflectivity (<0.1%) across targeted wavelength ranges. Built using alternating layers of SiO₂ (silicon dioxide) and TiO₂ or Ta₂O₅, these coatings are essential in precision optics, semiconductor lithography, laser systems, and high-performance camera lenses. The segment is bifurcated into Broadband AR (BBAR) coatings—typically 4–12 layer stacks optimized for the visible spectrum (400–700nm)—and V-coats, engineered for narrowband applications such as fiber optic communications (1550nm) and laser cutting (1064nm). In 2025, value creation is shifting toward ion-assisted deposition (IAD) and plasma-enhanced coating technologies, which enhance density, adhesion, and environmental stability. These advanced dielectric AR coatings are increasingly specified in aerospace HUDs, defense FLIR systems, and harsh-environment optics, reinforcing their leadership in the global AR coatings market.

Consumer Electronics Drives 31.5% of Anti-Reflective Coatings Market with Smartphone Display Demand

End-Use Industry Analysis: Smartphone and Foldable Display Boom Accelerates AR Coating Adoption

The consumer electronics segment dominates the anti-reflective coatings market with a 31.5% share in 2025, fueled primarily by the global shipment of approximately 1.4 billion smartphones annually, each requiring AR-coated display glass. Despite a low cost per unit, the sheer production scale makes this segment the largest revenue contributor. The market is undergoing a functional transformation toward multifunctional AR coating stacks, integrating anti-reflective (AR), anti-fingerprint (AFP), scratch-resistant hard coatings, and oleophobic layers in a single sputtered multilayer system. These coatings enhance outdoor readability, reduce power consumption, and improve durability, making them indispensable for premium devices. Additionally, the rise of foldable smartphones is creating a high-growth niche, as ultra-thin glass (UTG) and colorless polyimide (CPI) substrates require low-temperature PECVD or ALD-deposited AR coatings. This shift is driving innovation and premiumization within the consumer electronics AR coatings market, positioning it as a key growth engine.

Anti Reflective Coatings Market Competitive Landscape Driven by Optical Precision and Smart Integration

The anti reflective coatings market is shaped by advanced vacuum deposition technologies, multi-layer optical coatings, and high-transmission materials. Leading players are focusing on smart eyewear, semiconductor optics, automotive displays, and solar glass applications to enhance light transmission, reduce glare, and improve durability across industries.

EssilorLuxottica dominates eyewear AR coatings with Crizal innovation and smart integration

EssilorLuxottica leads the anti reflective coatings market in the ophthalmic segment, controlling the largest share of the eyewear AR market. Its Crizal® portfolio sets benchmarks for glare reduction, light transmission, and lens durability. The expansion of Crizal Sapphire™ HR introduces 360° multi-angular technology that minimizes reflections from all light directions, targeting digital device users. The company is advancing smart eyewear integration by embedding AR coatings into connected frames requiring high optical clarity. Its network of over 500 prescription laboratories enables rapid deployment of vacuum-deposited AR coatings with consistent quality across regions. Product development continues to focus on premium eyewear coatings and digital vision enhancement.

Carl Zeiss advances precision AR coatings with semiconductor and optical engineering leadership

Carl Zeiss AG is a leader in precision anti reflective coatings across vision care and semiconductor applications. The company reported €10.9 billion in revenue entering 2026, supported by strong demand in semiconductor manufacturing technologies. Its ZEISS DuraVision Plus portfolio, launched in 2026, integrates CleanGuard technology, enabling lenses to be cleaned up to three times faster than conventional coatings. The DuraVision Gold UV range achieves a Bayer ratio of 16.4, exceeding durability benchmarks for scratch resistance in industrial and consumer applications. Zeiss continues to invest in EUV lithography photomask blanks, maintaining global leadership in advanced optics critical to AI chip production. Product innovation emphasizes durability, optical precision, and high-performance AR coatings.

PPG Industries expands AR coatings in automotive displays and data center applications

PPG Industries strengthens its presence in anti reflective coatings through industrial coatings and integrated optical solutions. The company reported $15.9 billion in net sales in 2025, with 4% growth in its Industrial Coatings segment driven by AR and protective coatings demand. It introduced integrated AR coating solutions for data centers in 2026, enhancing signal transmission in optical sensors and fiber-optic connectors. A $50 million restructuring initiative supports production of low-VOC waterborne AR coatings for automotive glass and architectural applications. PPG continues to strengthen its share in the automotive display market by supplying AR/AG coating stacks for advanced digital cockpit systems. Product development continues to focus on performance optimization and environmental compliance.

Hoya strengthens AR coatings portfolio with blue light protection and antimicrobial technology

Hoya Corporation plays a key role in anti reflective coatings through advanced lens materials and healthcare-focused innovations. The Super HiVision Meiryo EX4 coating, launched in 2025, delivers 2.5x higher scratch resistance with enhanced contrast for night driving conditions. Its Hi-Vision LongLife BlueControl technology addresses blue light exposure by filtering high-energy visible light while maintaining 99% light transmission. The company expanded its antimicrobial AR coatings using silver-ion technology, achieving 99.9% bacterial inhibition on lens surfaces. Strategic expansion in Asia, which accounts for 44.7% of global AR demand growth, includes new manufacturing facilities in South Korea and India. Product development continues to align with digital eye protection and advanced optical performance.

AGC leads solar and architectural AR coatings with high-efficiency glass technologies

AGC Inc. is a global leader in anti reflective coatings for solar glass and architectural applications, focusing on energy efficiency and durability. Its coatings improve photovoltaic module efficiency by 6–12%, supporting growth in the solar energy sector. The company holds the second-largest global share in automotive cover glass, integrating AR coatings into heads-up display systems without compromising structural strength. Vertical integration enables production of alkali-free and aluminosilicate glass substrates, ensuring strong adhesion of AR layers and resistance to thermal stress. Sustainability initiatives include Eco-Etching processes introduced in 2025, reducing chemical waste in AR coating production by 20%. Product innovation continues to focus on high-transmission coatings and large-scale glass applications.

China Anti-Reflective Coatings Market: Solar PV Integration and Advanced Display Manufacturing Dominance

China’s anti-reflective coatings market is expanding rapidly, driven by strong vertical integration across solar photovoltaic (PV) manufacturing and display technologies. The widespread adoption of porous silica-based anti-reflective coatings on bifacial solar modules is enhancing energy efficiency, particularly in high-humidity floating solar installations. This advancement is positioning China as a global leader in high-performance solar glass coatings.

Technological innovation remains central to market growth, with the development of broadband anti-reflective coatings delivering ultra-low reflection across visible wavelengths for next-generation smartphone displays. Significant investments in large-scale display glass production are further strengthening supply capabilities for high-resolution screens. Government mandates promoting solvent-free and low-emission coating processes are accelerating the transition toward sustainable manufacturing. Additionally, the integration of multifunctional coatings with high light transmission and electromagnetic shielding properties is expanding applications across aerospace, electronics, and communication technologies.

United States Anti-Reflective Coatings Market: Aerospace Optics and AR/VR Technology Expansion

The United States anti-reflective coatings market is characterized by strong innovation in aerospace optics and immersive technology applications. Advanced coating solutions are being developed for infrared optical systems used in defense and thermal imaging, enhancing performance in critical aerospace and military applications.

The rapid growth of augmented and virtual reality technologies is also driving demand for high-performance anti-reflective coatings in optical components. Innovations such as nanostructured coatings designed to reduce glare and improve visual clarity are enabling enhanced user experiences in wearable devices. Investments in advanced coating facilities are supporting large-scale production of anti-reflective films, particularly for emerging sectors such as agrivoltaics. Additionally, regulatory initiatives promoting energy-efficient coating processes are encouraging the adoption of advanced deposition technologies, further strengthening the United States’ leadership in optical coatings innovation.

Germany Anti-Reflective Coatings Market: Automotive AR-HUD Growth and Sustainable Optical Coatings

Germany’s anti-reflective coatings market is driven by its leadership in automotive innovation and sustainable material development. The increasing integration of augmented reality head-up displays (AR-HUDs) in premium vehicles is generating substantial demand for high-performance anti-reflective coatings that enhance visual clarity and eliminate image distortion.

Sustainability remains a key focus, with manufacturers developing bio-based optical resins that reduce environmental impact while maintaining high optical performance. Investments in advanced deposition technologies are enabling the production of ultra-thin, high-precision coatings for complex optical components. Additionally, innovations such as self-cleaning coatings are improving durability and reducing maintenance requirements in outdoor applications. Strong collaboration between optical and semiconductor industries is further driving advancements in next-generation coating technologies, reinforcing Germany’s position as a global leader in optical materials.

India Anti-Reflective Coatings Market: Solar Mission Expansion and Electronics Manufacturing Growth

India’s anti-reflective coatings market is experiencing strong growth, driven by ambitious solar energy initiatives and rapid expansion in electronics manufacturing. Government-backed programs supporting rooftop solar installations are significantly increasing the demand for anti-reflective coated glass, which enhances energy conversion efficiency and system performance.

The establishment of new manufacturing facilities under production incentive schemes is strengthening domestic capabilities in coating technologies. Innovations such as dust-repellent coatings are addressing environmental challenges specific to the region, improving efficiency in solar installations. Additionally, the integration of anti-reflective coatings in transportation and public infrastructure is expanding their application scope. Regulatory standards mandating high transmission efficiency for solar glass are further driving adoption, positioning India as a key emerging market in the global anti-reflective coatings industry.

South Korea Anti-Reflective Coatings Market: OLED Advancements and Semiconductor Integration

South Korea’s anti-reflective coatings market is driven by its leadership in display technologies and semiconductor manufacturing. Innovations in OLED technology are enhancing brightness and reducing reflections, improving visual performance in next-generation consumer electronics.

Technological advancements in flexible coatings are enabling durability in foldable devices, supporting the growth of premium smartphone segments. The increasing application of anti-reflective coatings in imaging sensors is improving optical performance in high-resolution cameras. Investments in research and development are accelerating the adoption of advanced coating materials and processes, while government initiatives supporting semiconductor manufacturing are further strengthening the market. These developments position South Korea as a major hub for cutting-edge optical coating technologies.

Japan Anti-Reflective Coatings Market: Nanotechnology Innovation and Cryogenic Optical Applications

Japan’s anti-reflective coatings market is advancing through innovations in nanotechnology and specialized optical applications. The development of nano-etched coatings is enabling high-performance anti-reflective solutions with improved durability and cost efficiency, particularly for large-scale architectural and industrial uses.

The country’s focus on advanced infrastructure and energy systems is driving demand for coatings capable of operating in extreme conditions, including cryogenic environments associated with hydrogen transport. Hydrophobic and self-cleaning coatings are improving performance in marine and outdoor applications, reducing maintenance requirements. Additionally, investments in high-speed transportation projects and renewable energy initiatives are expanding the use of advanced anti-reflective coatings. Regulatory support for sustainable technologies is further accelerating the adoption of environmentally friendly coating solutions across industries.

Anti-Reflective Coatings Market Report Scope

Anti-Reflective Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.7 Billion

|

|

Market Size (2032)

|

$9.4 Billion

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Material Chemistry (Dielectric Coatings, Metal Oxide Coatings, Fluoropolymer-based Coatings, Nanostructured Coatings), By Deposition Technology (Vacuum Deposition, Sputtering, Chemical Vapor Deposition, Sol-Gel Process, Roll-to-Roll), By Layer Configuration (Single-Layer AR Coatings, Multi-Layer AR Coatings, Gradient-Index), By End-Use Industry (Eyewear and Ophthalmology, Consumer Electronics, Solar Energy, Automotive, Industrial and Precision Optics, Medical and Healthcare, Aerospace and Defense, Semiconductor Manufacturing), By Substrate Compatibility (Glass Substrates, Polymer Substrates, Crystalline Substrates), By Application Method (Batch Processing, In-Line Continuous Processing)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

EssilorLuxottica SA, Carl Zeiss AG, HOYA Corporation, PPG Industries, Inc., AGC Inc., Nippon Sheet Glass Co., Ltd., DuPont de Nemours, Inc., Honeywell International Inc., Applied Materials, Inc., Schott AG, Merck KGaA, Viavi Solutions Inc., Edmund Optics Inc., Janos Technology LLC, Rodensock GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anti-Reflective Coatings Market Segmentation

By Material Chemistry

- Dielectric Coatings

- Metal Oxide Coatings

- Fluoropolymer-based Coatings

- Nanostructured Coatings

By Deposition Technology

- Vacuum Deposition

- Sputtering

- Chemical Vapor Deposition

- Sol-Gel Process

- Roll-to-Roll

By Layer Configuration

- Single-Layer AR Coatings

- Multi-Layer AR Coatings

- Gradient-Index

By End-Use Industry

- Eyewear and Ophthalmology

- Consumer Electronics

- Solar Energy

- Automotive

- Industrial and Precision Optics

- Medical and Healthcare

- Aerospace and Defense

- Semiconductor Manufacturing

By Substrate Compatibility

- Glass Substrates

- Polymer Substrates

- Crystalline Substrates

By Application Method

- Batch Processing

- In-Line Continuous Processing

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Anti Reflective Coatings Market

- EssilorLuxottica SA

- Carl Zeiss AG

- HOYA Corporation

- PPG Industries, Inc.

- AGC Inc

- Nippon Sheet Glass Co., Ltd

- DuPont de Nemours, Inc.

- Honeywell International Inc.

- Applied Materials, Inc.

- Schott AG

- Merck KGaA

- Viavi Solutions Inc.

- Edmund Optics Inc.

- Janos Technology LLC

- Rodensock GmbH

*- List not Exhaustive

Table of Contents: Anti-Reflective Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Anti-Reflective Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Anti-Reflective Coatings (ARC) Market

2.2. Market Valuation and Growth Forecast (2025–2032)

2.3. Growth Drivers: Solar Efficiency and Optical Precision Demand

2.4. Multi-Industry Adoption: Solar, Eyewear, Electronics, and Automotive

2.5. Technological Evolution in Thin-Film and Nanostructured Coatings

3. Innovation Trends Reshaping the ARC Market

3.1. Trend: Multi-Layer Optical Engineering and Thin-Film Advancements

3.2. Trend: Integration of Hydrophobic, Scratch-Resistant, and Smudge-Resistant Features

3.3. Opportunity: Expansion in AR/VR, Wearables, and Automotive Displays

3.4. Opportunity: Solar PV Efficiency Enhancement through Advanced ARC

4. Competitive Landscape and Strategic Developments

4.1. Mergers, Partnerships, and Industry Consolidation

4.2. Product Innovation and R&D Focus

4.3. OEM Collaborations and Supply Chain Integration

4.4. Manufacturing Expansion and Capacity Scaling

5. Market Share and Segmentation Insights: Anti-Reflective Coatings Market

5.1. By Material Chemistry

5.1.1. Dielectric Coatings

5.1.2. Metal Oxide Coatings

5.1.3. Fluoropolymer-Based Coatings

5.1.4. Nanostructured Coatings

5.2. By Deposition Technology

5.2.1. Vacuum Deposition

5.2.2. Sputtering

5.2.3. Chemical Vapor Deposition

5.2.4. Sol-Gel Process

5.2.5. Roll-to-Roll Processing

5.3. By Layer Configuration

5.3.1. Single-Layer AR Coatings

5.3.2. Multi-Layer AR Coatings

5.3.3. Gradient-Index Coatings

5.4. By End-Use Industry

5.4.1. Eyewear and Ophthalmology

5.4.2. Consumer Electronics

5.4.3. Solar Energy

5.4.4. Automotive

5.4.5. Industrial and Precision Optics

5.4.6. Medical and Healthcare

5.4.7. Aerospace and Defense

5.4.8. Semiconductor Manufacturing

5.5. By Substrate Compatibility

5.5.1. Glass Substrates

5.5.2. Polymer Substrates

5.5.3. Crystalline Substrates

5.6. By Application Method

5.6.1. Batch Processing

5.6.2. In-Line Continuous Processing

6. Country Analysis and Outlook of Anti-Reflective Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. United Kingdom

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Anti-Reflective Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Anti-Reflective Coatings Market Size Outlook to 2032

7.1.1. By Material Chemistry

7.1.2. By Deposition Technology

7.1.3. By Layer Configuration

7.1.4. By End-Use Industry

7.1.5. By Substrate Compatibility

7.1.6. By Application Method

7.2. Europe Anti-Reflective Coatings Market Size Outlook to 2032

7.2.1. By Material Chemistry

7.2.2. By Deposition Technology

7.2.3. By Layer Configuration

7.2.4. By End-Use Industry

7.2.5. By Substrate Compatibility

7.2.6. By Application Method

7.3. Asia Pacific Anti-Reflective Coatings Market Size Outlook to 2032

7.3.1. By Material Chemistry

7.3.2. By Deposition Technology

7.3.3. By Layer Configuration

7.3.4. By End-Use Industry

7.3.5. By Substrate Compatibility

7.3.6. By Application Method

7.4. South America Anti-Reflective Coatings Market Size Outlook to 2032

7.4.1. By Material Chemistry

7.4.2. By Deposition Technology

7.4.3. By Layer Configuration

7.4.4. By End-Use Industry

7.4.5. By Substrate Compatibility

7.4.6. By Application Method

7.5. Middle East and Africa Anti-Reflective Coatings Market Size Outlook to 2032

7.5.1. By Material Chemistry

7.5.2. By Deposition Technology

7.5.3. By Layer Configuration

7.5.4. By End-Use Industry

7.5.5. By Substrate Compatibility

7.5.6. By Application Method

8. Company Profiles: Anti-Reflective Coatings Market

8.1. EssilorLuxottica SA

8.2. Carl Zeiss AG

8.3. HOYA Corporation

8.4. PPG Industries, Inc.

8.5. AGC Inc

8.6. Nippon Sheet Glass Co., Ltd

8.7. DuPont de Nemours, Inc.

8.8. Honeywell International Inc.

8.9. Applied Materials, Inc.

8.10. Schott AG

8.11. Merck KGaA

8.12. Viavi Solutions Inc.

8.13. Edmund Optics Inc.

8.14. Janos Technology LLC

8.15. Rodensock GmbH

9. Methodology

9.1. Research Scope

9.2. Market Research Methodology

9.3. Market Sizing and Forecasting Approach

9.4. Data Collection and Validation

9.5. Assumptions and Limitations

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures