Antifouling Coatings Market Size and Growth Driven by Marine Fuel Efficiency and Decarbonization Goals

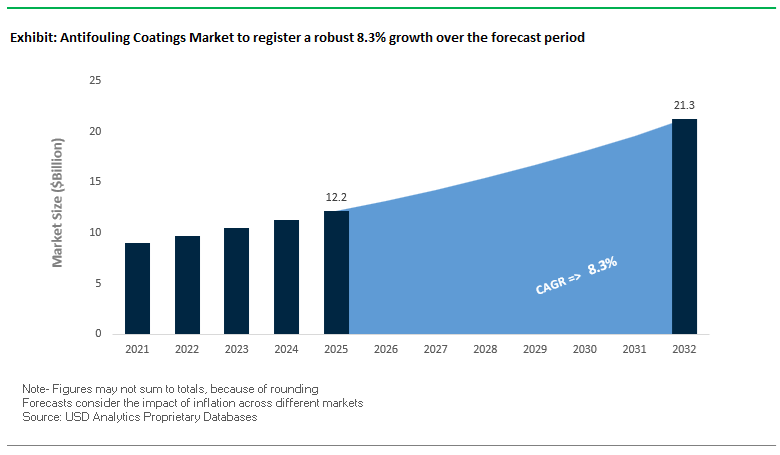

The Antifouling Coatings Market is projected to expand from USD 12.2 billion in 2025 to USD 21.32 billion by 2032, registering a strong CAGR of 8.3%. The rapid growth is predominantly driven by the global maritime industry's increasing focus on fuel efficiency, emission reduction, and vessel performance optimization. Antifouling coatings are essential for preventing the accumulation of marine organisms such as algae and barnacles on ship hulls, which significantly increases drag and fuel consumption.

These coatings play a critical role in improving hydrodynamic efficiency, enabling vessels to reduce fuel usage and comply with stringent environmental regulations such as IMO decarbonization targets and Carbon Intensity Indicator (CII) standards. Even minor reductions in hull friction can result in substantial operational cost savings for commercial fleets, making antifouling coatings a high-value investment. The market is also benefiting from rising global trade volumes and fleet expansion, particularly in Asia-Pacific shipping corridors, where demand for high-performance marine coatings is accelerating.

Technological advancements are shifting the industry toward biocide-free, low-friction, and environmentally sustainable coating systems. Innovations such as silicone-based foul-release coatings, silyl methacrylate polymers, and copper-free formulations are gaining traction as regulatory pressure intensifies on traditional toxic biocides. Additionally, integration of smart coatings and predictive maintenance technologies is enabling ship operators to optimize dry-docking schedules and enhance long-term asset performance.

The competitive landscape is defined by intensive R&D investment, strategic partnerships, and a strong focus on sustainability-driven innovation, positioning antifouling coatings as a cornerstone technology in the maritime sector’s transition toward energy-efficient and low-emission operations

Biocide-Free Innovation, Strategic Partnerships, and Performance Optimization Transforming Market Dynamics

The antifouling coatings market is undergoing a major transformation driven by next-generation product innovation, strategic consolidation, and sustainability-focused initiatives. A key development occurred in November 2025, when AkzoNobel and Axalta announced a mega-merger, creating a global coatings leader with enhanced capabilities in marine coatings and advanced resin technologies. The combined entity is expected to accelerate the development of biocide-free antifouling systems, aligning with tightening environmental regulations.

Product innovation remains central to market evolution. In August 2025, Chugoku Marine Paints (CMP) launched SEAFLO NEO SL ZX, a next-generation coating utilizing silyl methacrylate technology to achieve ultra-low friction and improved vessel efficiency. Similarly, Nippon Paint’s FASTAR technology (March 2026) focuses on minimizing biofouling through advanced surface chemistry, significantly reducing drag and fuel consumption. PPG’s NEXEON 810 (May 2024) introduces a copper-free antifouling solution with photodegradable biocides, offering up to 20% power savings when combined with advanced foul-release systems.

Strategic partnerships and large-scale deployments are reinforcing market adoption. In December 2025, AkzoNobel extended its partnership with Winning Shipping, supplying advanced coatings such as Intersleek® 1100SR, a biocide-free fouling control system, and Intercept® 8500 LPP for drydocking projects. Additionally, AkzoNobel’s July 2025 involvement in protecting the world’s first sail-assisted Aframax tanker highlights the integration of advanced coatings with alternative propulsion technologies, supporting maritime decarbonization efforts.

Corporate strategies are increasingly aligned with sustainability and emissions reduction. Hempel’s “Accelerate to Win” strategy (January 2026) emphasizes investment in its Hempaguard range, which has already contributed to reducing 35.9 million tonnes of CO2 emissions. Similarly, Jotun reported in February 2026 that its coatings helped avoid 11.8 million tonnes of CO2 emissions, translating into $2 billion in fuel savings for customers, validated through independent verification models.

Market expansion is further supported by strong demand across marine and energy sectors. Sherwin-Williams reported robust growth in its Protective & Marine segment (January 2026), driven by increasing adoption of high-performance coatings despite broader market softness. Additionally, CMP’s expansion of its tank coating portfolio (May 2025) reflects the growing need for integrated protection systems that address both external hull fouling and internal chemical exposure.

IMO Cybutryne Ban Forcing Global Reformulation and Accelerating Dry-Docking Cycles

The antifouling coatings industry is undergoing a regulatory-driven overhaul following the enforcement of the Cybutryne (Irgarol 1051) ban under the International Convention on the Control of Harmful Anti-Fouling Systems on Ships. As of 2026, this prohibition has transitioned from policy to operational enforcement, requiring all vessels constructed prior to 2023 to either remove existing Cybutryne-based coatings or apply an approved sealer layer during their first mandatory survey after January 1, 2026. This mandate affects approximately 70% of legacy antifouling formulations, creating a large-scale reformulation wave across the global maritime fleet.

The implications extend beyond compliance into operational economics. Shipowners are increasingly adopting Cybutryne-free Self-Polishing Copolymer systems that deliver measurable fuel efficiency gains. Modern high-performance coatings can reduce hull friction sufficiently to generate fuel savings in the range of 8% to 15%, aligning directly with decarbonization targets and emissions reduction strategies under IMO frameworks. At the same time, regulatory enforcement is tightening port-state controls. Vessels unable to produce valid International Anti-Fouling System Certificates confirming compliance risk detention in major global ports, creating a strong incentive for immediate retrofitting.

Hydrogel Fouling-Release Coatings Replacing Biocidal Systems in Sensitive Marine Environments

The antifouling coatings market is entering a new technological phase with the rapid adoption of hydrogel-based fouling-release coatings, often described as the third generation of antifouling solutions. These advanced systems are displacing traditional copper- and biocide-based coatings, particularly in ecologically sensitive regions such as Marine Protected Areas and “No-Anchor” zones where chemical leaching is heavily restricted.

Hydrogel-silicone hybrid coatings significantly reduce reliance on toxic biocides, utilizing less than 5% of the active chemical load found in conventional copper-based paints while maintaining effective fouling resistance. Unlike earlier fouling-release coatings that required vessel speeds to facilitate organism detachment, next-generation hydrogel systems provide static protection for up to 30 days, making them suitable for vessels with irregular sailing schedules or extended port stays.

Surface smoothness is a key performance differentiator. Hydrogel coatings achieve ultra-low surface roughness levels below 75 microns, compared to more than 120 microns for traditional coatings. This smoother surface reduces hydrodynamic drag and contributes directly to improved Carbon Intensity Indicator performance. In long-term field applications, hydrogel coatings deployed in environmentally sensitive waters such as the Baltic and Mediterranean seas have demonstrated complete prevention of hard fouling over service intervals of up to 60 months without releasing heavy metals into surrounding ecosystems.

Offshore Renewable Energy Infrastructure Creating High-Value Demand for Static Fouling Protection

The rapid expansion of offshore renewable energy assets, including wind and wave energy installations, is creating a new and highly specialized demand segment for antifouling coatings. Unlike mobile vessels, these stationary structures are exposed to continuous biofouling pressure, leading to significant operational and structural challenges.

Biofouling accumulation on offshore wind foundations can contribute to as much as 10% of the Levelized Cost of Electricity due to increased hydrodynamic drag and structural fatigue. Additionally, the mass loading effect of macrofouling organisms such as mussels and barnacles can add substantial weight to substructures, potentially compromising structural integrity and accelerating material degradation. These challenges are driving demand for advanced coatings capable of maintaining low surface energy and preventing organism attachment over extended periods.

From an economic perspective, the implementation of high-durability antifouling coatings combined with autonomous cleaning technologies can reduce maintenance costs by more than $18,000 per megawatt annually. Extending the clean operational window of offshore structures to over 10 years allows operators to reduce reliance on costly remotely operated vehicle-based cleaning operations by up to 50%, improving overall project economics and bankability.

Desalination Infrastructure Driving Demand for High-Performance Intake Pipeline Coatings

The global expansion of desalination capacity is creating a parallel demand for antifouling coatings designed to protect intake pipelines from biological growth. Biofouling within these systems presents a significant operational risk, increasing surface roughness and reducing hydraulic efficiency.

In practical terms, biofouling can increase pumping energy requirements by 15% to 25% due to head loss caused by increased friction within the pipeline. Severe fouling conditions can lead to the formation of thick biological layers, in some cases reaching up to 19 centimeters, which significantly reduces internal pipe diameter and disrupts water flow capacity. These conditions can lead to pump cavitation, mechanical failure, and reduced reliability of intake systems.

The application of advanced antifouling coatings during pipeline construction is proving to be a critical mitigation strategy. Non-leaching coating systems are enabling operators to control biofouling without relying on continuous chemical dosing, such as chlorine treatment, which is increasingly restricted under environmental discharge regulations. By reducing chemical usage and improving operational stability, these coatings support compliance with evolving environmental standards while enhancing system efficiency.

Self-Polishing Copolymer (SPC) Coatings Lead Antifouling Market with 44% Share Driven by Fuel Efficiency and Regulatory Compliance

Chemistry Analysis: SPC Technology Dominates with Controlled Polishing and Biocide Optimization

Self-Polishing Copolymers (SPC) account for a leading 44.0% share of the global antifouling coatings market in 2025, establishing themselves as the industry benchmark for deep-sea vessel protection and long-term hull performance. Built on silyl acrylate and copper acrylate polymer chemistries, SPC coatings deliver a controlled hydrolysis-driven polishing mechanism, ensuring continuous exposure of fresh biocidal layers over a 60-month dry-docking cycle. This results in consistently smooth hull surfaces, reducing drag and enabling 6%–12% fuel savings, a critical factor under IMO Carbon Intensity Indicator (CII) and EU ETS regulations. A major 2025 trend is the shift toward copper acrylate SPC formulations, which act as both polishing controllers and secondary antifouling agents, reducing reliance on booster biocides by up to 30%. This evolution enhances environmental compliance while maintaining superior antifouling efficacy, reinforcing SPC’s leadership in the marine coatings market.

Commercial Shipping Sector Dominates Antifouling Coatings Market with 58% Share Amid Global Fleet Expansion

End-Use Industry Analysis: Vessel Scale and Slow Steaming Trends Drive Coating Demand

Commercial shipping commands a dominant 58.0% share of the antifouling coatings market in 2025, driven by the विशाल scale of the global fleet, comprising over 60,000 vessels exceeding 500 gross tonnage, including container ships, bulk carriers, and oil tankers. Each vessel requires full hull recoating approximately every five years, with Ultra Large Container Vessels (ULCVs) consuming up to 40,000–60,000 liters of antifouling paint per dry-docking cycle. A key growth driver is the industry-wide adoption of slow steaming (12–16 knots), which increases the risk of biofouling from barnacles and marine organisms, thereby necessitating high-performance SPC coatings over traditional alternatives. Additionally, 2025 marks a shift toward integrated hull maintenance strategies, where coatings are paired with ROV-based underwater cleaning systems. Shipowners increasingly demand durable foul-release SPC hybrid coatings capable of withstanding periodic cleaning while maintaining optimal hull smoothness and fuel efficiency compliance, reinforcing the segment’s dominance in the global antifouling coatings market.

Antifouling Coatings Market Competitive Landscape Driven by Sustainable Marine Technologies and Fuel Efficiency Optimization

The antifouling coatings market is defined by biocide-free coatings, fouling release systems, and advanced hydrolysis technologies. Leading companies are focusing on fuel efficiency, emission reduction, and long-life marine coatings to support regulatory compliance and performance optimization across global shipping and offshore sectors.

AkzoNobel leads antifouling coatings with biocide-free slime release and long-life protection systems

AkzoNobel holds 18% of the antifouling coatings market, driven by its International® portfolio and leadership in sustainable marine coatings. The company secured a major supply agreement with Winning Shipping in December 2025, targeting large-scale drydocking demand in the APAC region. Its Intersleek® 1100SR coating remains a benchmark biocide-free fouling release solution, reducing hull resistance and supporting fuel efficiency targets. The Intercept® 8500 LPP system provides up to 90 months of protection for deep-sea vessels through advanced linear polishing technology. AkzoNobel also contributed to coating the world’s first sail-assisted Aframax tanker, supporting maritime decarbonization initiatives. Product innovation focuses on long-duration protection and environmentally compliant coatings.

Jotun strengthens antifouling coatings leadership with hull performance systems and robotic cleaning solutions

Jotun A/S continues to expand its antifouling coatings portfolio with strong financial performance and advanced marine technologies. The company reported operating revenues exceeding NOK 34 billion in 2025, with significant growth across marine coatings segments. Its Jotun Hull Performance framework standardizes performance metrics for antifouling coatings, enhancing fuel efficiency and operational predictability. Hull Skating Solutions integrates robotic cleaning technology to maintain clean hull conditions and reduce CO2 emissions, validated by DNV for environmental impact. Expansion into offshore wind through the EOLMED project highlights its role in renewable energy coatings. Product development emphasizes performance monitoring, emission reduction, and lifecycle optimization.

PPG Industries advances antifouling coatings with electrostatic application and copper-free solutions

PPG Industries is a key player in antifouling coatings, focusing on application efficiency and sustainable marine solutions. Its Sigmaglide® 2390 fouling release coating delivers up to 35% greenhouse gas reduction and 20% power savings, addressing CII and EEXI regulatory requirements. The launch of NEXEON™ 810 introduced a copper-free antifouling coating using photodegradable biocides to minimize environmental impact. PPG has adapted electrostatic coating technology from aerospace to shipbuilding, achieving high transfer efficiency and reduced VOC emissions. The company is supporting major fleets with data-driven hull performance solutions aimed at achieving net-zero targets. Product innovation focuses on efficiency, sustainability, and advanced application technologies.

Hempel expands antifouling coatings with silicone hull systems and APAC growth strategy

Hempel A/S is strengthening its position in antifouling coatings through innovation and geographic expansion. The company achieved an 18% adjusted EBITDA margin in 2025, with its Marine segment recording 9.8% organic growth. Its Hempaguard® NB coating is the first silicone-based hull coating designed specifically for newbuild vessels, improving efficiency from initial deployment. Expansion in APAC includes a new office in Pune and full-capacity operations in China to support shipbuilding demand. Strategic collaboration with CVC Funds is enabling further investments and acquisitions in marine and offshore sectors. Product development focuses on high-performance coatings and lifecycle efficiency.

Chugoku Marine Paints advances silyl-based antifouling coatings with strong Asian shipbuilding presence

Chugoku Marine Paints (CMP) is a specialized leader in antifouling coatings, particularly through its expertise in silyl-based technologies. The company is expanding its footprint in China through new production investments to align with the region’s dominant shipbuilding capacity. Its SEAFLO NEO and SEA PREMIER series provide high-performance antifouling solutions using controlled hydrolysis to maintain smooth hull surfaces. CMP’s SEA GRANDPRIX 950 L coating has been applied to over 10,000 vessels, demonstrating strong performance in long-term marine protection. Participation in SEA JAPAN 2026 highlights its focus on global regulatory trends and eco-friendly coatings. Product development centers on durability, polishing control, and compliance with evolving environmental standards.

South Korea Antifouling Coatings Market: Shipbuilding Dominance and Green Maritime Transition Driving Advanced Coatings

South Korea remains the global leader in the antifouling coatings market, driven by its unmatched dominance in shipbuilding and high-performance marine coatings. The country’s “Big Three” shipbuilders—HD Hyundai, Samsung Heavy Industries, and Hanwha Ocean—have standardized the use of premium self-polishing copolymer (SPC) antifouling coatings across all new high-specification vessels, ensuring optimal hull performance and long-term durability. This standardization is reinforcing South Korea’s position as the benchmark for high-performance antifouling technologies in ultra-large container ships and LNG carriers.

Technological innovation and sustainability initiatives are accelerating market growth. Advanced solutions such as integrated robotic hull cleaning systems and graphene-reinforced antifouling primers are enhancing coating performance and lifecycle efficiency. Government-backed programs promoting green maritime technologies are incentivizing the adoption of low-friction coatings that significantly improve fuel efficiency. Regulatory leadership in banning harmful biocides and expanding climate-controlled coating infrastructure is further strengthening South Korea’s leadership in next-generation antifouling coatings.

China Antifouling Coatings Market: Eco-Friendly Marine Coatings and Offshore Energy Expansion Fueling Demand

China’s antifouling coatings market is the largest globally in terms of volume, driven by rapid industrialization and extensive maritime activity. Government mandates promoting environmentally friendly coatings are accelerating the transition toward biocide-free and low-leaching antifouling systems, particularly for vessels operating in sensitive marine environments. The widespread adoption of advanced antifouling films in high-speed ferries and coastal transport systems is improving operational efficiency and sustainability.

The expansion of offshore wind energy projects is a major growth driver, with antifouling coatings being widely used to protect structural components from marine biofouling. Technological advancements such as photocatalytic coatings and biomimetic surface designs are enhancing performance while reducing environmental impact. Investments in manufacturing capacity and research facilities are further strengthening China’s leadership in the global antifouling coatings market.

Norway Antifouling Coatings Market: Autonomous Shipping and Biocide-Free Coatings Driving Innovation

Norway’s antifouling coatings market is characterized by its focus on sustainability and advanced maritime technologies. The country is a global pioneer in autonomous shipping, driving demand for high-performance antifouling coatings that reduce maintenance requirements and improve operational efficiency. The widespread adoption of biocide-free silicone-based coatings is positioning Norway as a leader in environmentally sustainable marine coatings.

Technological advancements are enabling the development of innovative solutions such as hydrogel-based coatings that prevent organism adhesion and ultrasonic hull protection systems that complement coating performance. Government initiatives promoting green shipping and strict regulatory standards are further accelerating the adoption of advanced antifouling coatings. Additionally, innovations in aquaculture and offshore industries are expanding the application scope of these coatings, reinforcing Norway’s leadership in sustainable maritime technologies.

Japan Antifouling Coatings Market: Low-Friction Membrane Technologies and Advanced Marine Applications

Japan’s antifouling coatings market is driven by its expertise in precision chemical engineering and advanced material innovation. The development of low-friction membrane technologies is significantly improving vessel efficiency by reducing drag and fuel consumption. These innovations are particularly important in high-performance shipping and energy applications.

The integration of self-healing polymer technologies and hydrogel-based coatings is enhancing durability and extending service life in harsh marine environments. Investments in shipyard automation and advanced coating application systems are improving efficiency and consistency. Additionally, the growing use of antifouling coatings in renewable energy infrastructure, such as tidal turbines, is expanding market opportunities. These developments position Japan as a leader in advanced antifouling coating technologies.

United States Antifouling Coatings Market: Naval Modernization and Biotech Coating Innovations

The United States antifouling coatings market is driven by strong demand from naval and defense sectors, along with advancements in biotechnology-based coating solutions. The transition toward high-performance foul-release coatings is improving durability and extending maintenance cycles for military vessels, reducing operational costs and downtime.

Technological innovation is focused on developing environmentally friendly and highly efficient coating systems. Enzyme-based coatings that prevent marine organism attachment are gaining traction, offering a sustainable alternative to traditional antifouling solutions. Infrastructure investments in offshore oil platforms and inland waterways are further driving demand for specialized coatings. Regulatory frameworks standardizing discharge requirements are also shaping market dynamics, reinforcing the adoption of compliant and high-performance antifouling coatings.

Singapore Antifouling Coatings Market: Digital Monitoring and High-Efficiency Maintenance Solutions

Singapore’s antifouling coatings market is evolving through the integration of digital technologies and its position as a global maritime hub. The adoption of IoT-enabled coating systems is enabling real-time monitoring of hull performance, improving maintenance efficiency and reducing operational costs for shipping companies.

The country’s advanced port infrastructure is supporting the rapid application of next-generation antifouling coatings, particularly for floating production systems and high-value vessels. Innovations such as electrically active coatings and fast-curing systems are enhancing performance and reducing downtime. Strategic investments in research and development are further strengthening Singapore’s role as a key center for advanced marine coating technologies.

Germany Antifouling Coatings Market: Biomimetic Surfaces and Sustainable Coating Innovations

Germany’s antifouling coatings market is defined by its focus on sustainable materials and advanced surface engineering. The development of biomimetic coatings inspired by natural structures is enabling high-performance solutions that reduce environmental impact while maintaining effectiveness.

Regulatory leadership is driving the transition toward safer coating formulations, eliminating harmful substances and promoting eco-friendly alternatives. Innovations in smart materials and responsive coatings are improving efficiency by optimizing biocide release based on environmental conditions. Additionally, investments in testing facilities and renewable energy applications are expanding the scope of antifouling coatings, positioning Germany as a leader in sustainable marine technologies.

India Antifouling Coatings Market: Indigenous Defense Coatings and Shipyard Expansion Driving Growth

India’s antifouling coatings market is gaining momentum, supported by government initiatives promoting domestic manufacturing and maritime infrastructure development. The development of indigenous antifouling coatings for defense applications is strengthening national capabilities and reducing reliance on imports.

Large-scale infrastructure projects are expanding shipyard capacity, increasing demand for high-performance antifouling coatings in commercial and naval vessels. Innovations in coating formulations tailored to tropical climates are improving application efficiency and durability. Additionally, modernization programs in the fishing industry are driving the replacement of traditional coatings with eco-friendly alternatives. Strategic partnerships with global companies are further enhancing technology transfer and market growth, positioning India as an emerging player in the global antifouling coatings market.

Antifouling Coatings Market Report Scope

Antifouling Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.2 Billion

|

|

Market Size (2032)

|

$21.3 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Chemistry (Self-Polishing Copolymers, Controlled Depletion Polymers, Hybrid and Nano-Hybrid Formulations, Copper-Based Systems, Biocide-Free, Multi-Functional Coatings), By Technology (Conventional, Foul Release, Surface-Active Material, Sol-Gel Processing, Electroluminescence), By Application Area (Hull Coatings, Internal Seawater Systems, Tank and Ballast Coatings, Propellers and Niche Areas, Underwater Infrastructure), By End-Use Industry (Commercial Shipping, Offshore Oil and Gas, Marine Energy, Naval and Defense, Recreational and Leisure Boating, Aquaculture and Fisheries), By User Segment (OEM, Maintenance and Repair), By Service Duration (Short-term, Mid-term, Long-term)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Akzo Nobel N.V., Jotun A/S, Hempel A/S, PPG Industries, Inc., Chugoku Marine Paints, Ltd., The Sherwin-Williams Company, Nippon Paint Marine Coatings Co., Ltd., Kansai Paint Co., Ltd., KCC Corporation, BASF SE, Axalta Coating Systems Ltd., Boero YachtCoatings, Pettit Marine Paint, New Nautical Coatings, Inc., Advanced Polymer Coatings

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Antifouling Coatings Market Segmentation

By Chemistry

- Self-Polishing Copolymers

- Controlled Depletion Polymers

- Hybrid and Nano-Hybrid Formulations

- Copper-Based Systems

- Biocide-Free

- Multi-Functional Coatings

By Technology

- Conventional

- Foul Release

- Surface-Active Material

- Sol-Gel Processing

- Electroluminescence

By Application Area

- Hull Coatings

- Internal Seawater Systems

- Tank and Ballast Coatings

- Propellers and Niche Areas

- Underwater Infrastructure

By End-Use Industry

- Commercial Shipping

- Offshore Oil and Gas

- Marine Energy

- Naval and Defense

- Recreational and Leisure Boating

- Aquaculture and Fisheries

By User Segment

- OEM

- Maintenance and Repair

By Service Duration

- Short-term

- Mid-term

- Long-term

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Antifouling Coatings Market

- Akzo Nobel N.V.

- Jotun A/S

- Hempel A/S

- PPG Industries, Inc.

- Chugoku Marine Paints, Ltd.

- The Sherwin-Williams Company

- Nippon Paint Marine Coatings Co., Ltd.

- Kansai Paint Co., Ltd.

- KCC Corporation

- BASF SE

- Axalta Coating Systems Ltd.

- Boero YachtCoatings

- Pettit Marine Paint

- New Nautical Coatings, Inc.

- Advanced Polymer Coatings

*- List not Exhaustive

Table of Contents: Antifouling Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Antifouling Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Antifouling Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Role of Antifouling Coatings in Fuel Efficiency and Emission Reduction

2.4. Impact of IMO Regulations and Decarbonization Targets

2.5. Growth in Global Shipping, Offshore Energy, and Marine Infrastructure

3. Innovations Reshaping the Antifouling Coatings Market

3.1. Trend: Biocide-Free and Silicone-Based Foul-Release Technologies

3.2. Trend: Hydrogel-Based and Low-Friction Coating Systems

3.3. Opportunity: Offshore Renewable Energy and Static Fouling Protection

3.4. Opportunity: Advanced Coatings for Desalination and Marine Infrastructure

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Antifouling Coatings Market

5.1. By Chemistry

5.1.1. Self-Polishing Copolymers

5.1.2. Controlled Depletion Polymers

5.1.3. Hybrid and Nano-Hybrid Formulations

5.1.4. Copper-Based Systems

5.1.5. Biocide-Free

5.1.6. Multi-Functional Coatings

5.2. By Technology

5.2.1. Conventional

5.2.2. Foul Release

5.2.3. Surface-Active Material

5.2.4. Sol-Gel Processing

5.2.5. Electroluminescence

5.3. By Application Area

5.3.1. Hull Coatings

5.3.2. Internal Seawater Systems

5.3.3. Tank and Ballast Coatings

5.3.4. Propellers and Niche Areas

5.3.5. Underwater Infrastructure

5.4. By End-Use Industry

5.4.1. Commercial Shipping

5.4.2. Offshore Oil and Gas

5.4.3. Marine Energy

5.4.4. Naval and Defense

5.4.5. Recreational and Leisure Boating

5.4.6. Aquaculture and Fisheries

5.5. By User Segment

5.5.1. OEM

5.5.2. Maintenance and Repair

5.6. By Service Duration

5.6.1. Short-term

5.6.2. Mid-term

5.6.3. Long-term

6. Country Analysis and Outlook of Antifouling Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Antifouling Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Antifouling Coatings Market Size Outlook to 2032

7.1.1. By Chemistry

7.1.2. By Technology

7.1.3. By Application Area

7.1.4. By End-Use Industry

7.1.5. By User Segment

7.1.6. By Service Duration

7.2. Europe Antifouling Coatings Market Size Outlook to 2032

7.2.1. By Chemistry

7.2.2. By Technology

7.2.3. By Application Area

7.2.4. By End-Use Industry

7.2.5. By User Segment

7.2.6. By Service Duration

7.3. Asia Pacific Antifouling Coatings Market Size Outlook to 2032

7.3.1. By Chemistry

7.3.2. By Technology

7.3.3. By Application Area

7.3.4. By End-Use Industry

7.3.5. By User Segment

7.3.6. By Service Duration

7.4. South America Antifouling Coatings Market Size Outlook to 2032

7.4.1. By Chemistry

7.4.2. By Technology

7.4.3. By Application Area

7.4.4. By End-Use Industry

7.4.5. By User Segment

7.4.6. By Service Duration

7.5. Middle East and Africa Antifouling Coatings Market Size Outlook to 2032

7.5.1. By Chemistry

7.5.2. By Technology

7.5.3. By Application Area

7.5.4. By End-Use Industry

7.5.5. By User Segment

7.5.6. By Service Duration

8. Company Profiles: Leading Players in the Antifouling Coatings Market

8.1. Akzo Nobel N.V.

8.2. Jotun A/S

8.3. Hempel A/S

8.4. PPG Industries, Inc.

8.5. Chugoku Marine Paints, Ltd.

8.6. The Sherwin-Williams Company

8.7. Nippon Paint Marine Coatings Co., Ltd.

8.8. Kansai Paint Co., Ltd.

8.9. KCC Corporation

8.10. BASF SE

8.11. Axalta Coating Systems Ltd.

8.12. Boero YachtCoatings

8.13. Pettit Marine Paint

8.14. New Nautical Coatings, Inc.

8.15. Advanced Polymer Coatings

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures