Antifouling Paints and Coatings Market Size and Growth Driven by Marine Efficiency and Regulatory Transition

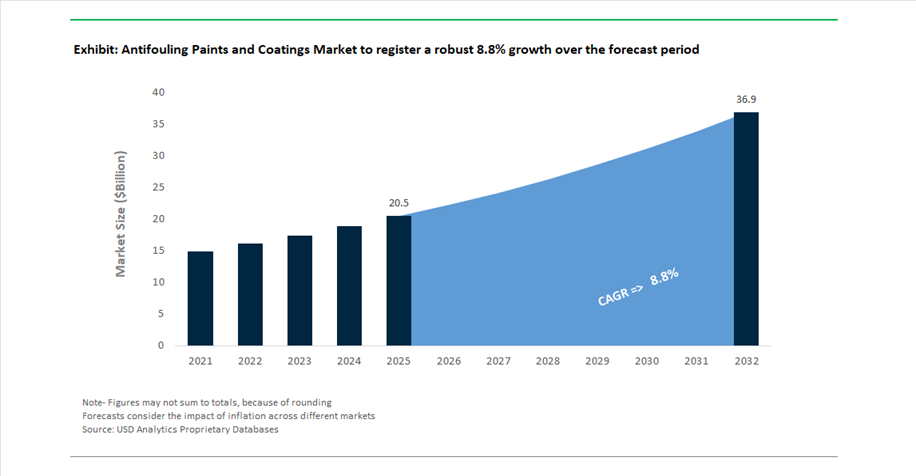

The Antifouling Paints and Coatings Market is projected to grow from USD 20.5 billion in 2025 to USD 37.0 billion by 2032, registering a strong CAGR of 8.8%. This robust expansion is driven by the increasing need for high-performance marine protection systems that enhance vessel efficiency, reduce operational costs, and comply with tightening environmental regulations. As global shipping volumes rise and fleet sizes expand, antifouling paints have become essential in maintaining optimal hull performance and long-term asset durability.

Antifouling paints and coatings are specifically designed to prevent the accumulation of marine organisms such as algae, barnacles, and biofilms on submerged surfaces. This biofouling significantly increases hydrodynamic drag, leading to higher fuel consumption and emissions. By maintaining smooth hull surfaces, these coatings enable fuel savings, improved speed performance, and compliance with international environmental standards, including IMO decarbonization targets and Carbon Intensity Indicator (CII) benchmarks. The market is also witnessing strong demand from offshore structures, subsea equipment, and marine infrastructure, where long-term corrosion and fouling resistance are critical.

A major trend shaping the market is the shift toward copper-free and biocide-free coating technologies, driven by stricter environmental regulations and sustainability goals. Manufacturers are investing in foul-release coatings, hydrophilic film technologies, and low-friction polymer systems that minimize environmental impact while maintaining high performance. Additionally, integration of digital monitoring tools and predictive maintenance systems is enhancing coating lifecycle management, enabling ship operators to optimize maintenance schedules and reduce downtime.

Biocide-Free Innovation, Digital Analytics, and Strategic Partnerships Driving Market Transformation

The antifouling paints and coatings market is evolving rapidly through advanced material innovation, digital integration, and industry consolidation. Product innovation remains a central growth driver. In August 2025, Chugoku Marine Paints (CMP) launched SEAFLO NEO SL ZX, a premium antifouling coating utilizing silyl methacrylate technology to achieve ultra-low friction and improved vessel efficiency. Similarly, Nippon Paint’s FASTAR technology (March 2026) introduces a hydrophilic film mechanism that significantly reduces biofouling and fuel consumption, particularly for large commercial vessels. These advancements reflect the industry’s focus on energy efficiency and emission reduction.

Strategic partnerships and large-scale deployments are reinforcing market adoption. AkzoNobel’s December 2025 partnership with Winning Shipping focuses on supplying Intersleek® 1100SR, a biocide-free fouling control system featuring patented slime-release technology. Additionally, CMP’s participation in RightShip’s Zero Harm Innovation Program (January 2026) highlights the industry’s commitment to promoting sustainable marine coatings and reducing environmental impact.

Digital transformation is emerging as a key differentiator. In March 2026, PPG launched InsightsNav, a real-time analytics platform designed to optimize coating performance and maintenance across global fleets. This tool enables shipowners to enhance operational efficiency, compliance, and lifecycle management of antifouling systems, reflecting the growing importance of data-driven decision-making in marine operations.

Corporate strategies are increasingly aligned with sustainability and performance optimization. Hempel’s “Accelerate to Win” strategy (January 2026) emphasizes investment in its Hempaguard NB system, contributing to 35.9 million tonnes of avoided CO2 emissions. Similarly, Jotun reported in February 2026 that its coatings helped avoid 11.8 million tonnes of CO2 emissions, demonstrating the measurable environmental and economic benefits of advanced antifouling technologies.

Market growth is further supported by strong demand across marine segments. Sherwin-Williams reported record sales in 2025, driven by robust demand for protective and marine coatings, while AkzoNobel’s March 2026 contract to supply coatings for new ferries highlights the increasing adoption of integrated coating systems that combine antifouling performance with safety features such as anti-slip surfaces.

Port State Control Enforcement Elevating Biofouling Compliance and Operational Risk Management

The antifouling paints and coatings industry is entering a compliance-intensive phase as the IMO Biofouling Guidelines (Resolution MEPC.378(80)) transition from voluntary adoption to active enforcement by Port State Control authorities. In 2026, major maritime jurisdictions such as the United States, Australia, and New Zealand have intensified inspection protocols, placing significant emphasis on hull cleanliness, antifouling system integrity, and the accuracy of Biofouling Management Plans. This shift reflects growing global concern over the transfer of invasive aquatic species and its ecological and economic consequences.

Inspection intensity has increased notably, with the U.S. Coast Guard conducting more than 8,700 Port State Control examinations in 2024, many of which included detailed verification of underwater hull conditions and certification compliance. Environmental deficiencies related to ineffective antifouling coatings and incomplete documentation are becoming key contributors to vessel detention. While overall detention rates may be declining, the technical rigor of inspections is rising, focusing on coating performance and lifecycle management.

The financial implications for non-compliance are significant. Detention-related downtime can cost shipowners between $20,000 and $50,000 per day depending on vessel type and port location, creating a strong incentive for proactive compliance. Furthermore, with over 95 countries now ratifying the AFS Convention, there is near-global enforcement of tin-free and cybutryne-free coating standards, effectively restricting non-compliant vessels from accessing approximately 90% of international trade routes.

Silicone Fouling-Release Coatings Achieving Mainstream Adoption Through Performance and Regulatory Alignment

Silicone-based fouling-release coatings are transitioning from niche applications to mainstream adoption across commercial shipping fleets. Historically limited by cost and application complexity, these coatings are now gaining widespread acceptance due to their compatibility with regulatory requirements and operational performance benefits. One of the most significant developments is the granting of Class Society Type Approval for in-water cleaning, allowing vessels to maintain hull performance through robotic grooming without damaging the coating or releasing harmful substances.

The performance advantages of silicone fouling-release coatings are substantial. Their ultra-smooth surfaces, typically achieving roughness levels below 75 microns, significantly reduce hydrodynamic drag. This contributes directly to improved Carbon Intensity Indicator scores, with studies indicating that a clean hull can reduce fuel consumption and associated greenhouse gas emissions by up to 15%. This efficiency gain is particularly important as shipowners align with decarbonization targets and fuel cost optimization strategies.

Durability improvements are also enhancing the value proposition of silicone coatings. Modern formulations are now designed for extended service intervals of up to 90 months, representing a 50% increase over traditional self-polishing copolymer systems that typically require dry-docking every 60 months. Regulatory pressures on copper leaching, particularly in regions such as the European Union and California, are further accelerating the shift toward non-biocidal silicone systems, as these coatings eliminate concerns related to heavy metal discharge.

Extended Dry-Docking Coatings for VLECs Unlocking Operational Efficiency Gains

The expansion of global ethane transportation is driving demand for Very Large Ethane Carriers, creating a specialized opportunity for extended dry-docking coating systems. These vessels operate under tight scheduling constraints and represent high-value assets, making extended operational uptime a critical economic objective. Coating technologies that enable dry-docking intervals of 7.5 to 10 years are becoming increasingly attractive for fleet operators.

Extending dry-docking intervals from five to seven and a half years can generate cost savings of approximately $1.5 million per vessel per cycle, driven by reduced shipyard fees and minimized operational downtime. Achieving this requires advanced coating systems that combine durability with consistent antifouling performance over extended periods. Fluoropolymer-enhanced and hydrogel-modified silicone coatings are emerging as leading solutions, capable of maintaining fouling resistance for more than 90 months even under static or slow-steaming conditions typical of LNG and ethane transport routes.

In addition to antifouling performance, corrosion protection is becoming a critical design consideration. Premium VLEC coating specifications now incorporate integrated systems combining high-performance primers with fouling-release topcoats to address localized corrosion risks, particularly in areas exposed to mechanical abrasion such as the waterline. This integrated approach ensures both structural integrity and hydrodynamic efficiency over extended service intervals.

Advanced Copper-Acrylate SPC Coatings Enhancing Naval Performance and Stealth Capabilities

While commercial shipping increasingly adopts silicone-based solutions, the naval sector continues to rely on self-polishing copolymer coatings due to their predictable performance characteristics and ability to provide effective protection during extended idle periods. The latest innovation in this segment is the development of tin-free copper-acrylate SPC coatings, which offer enhanced performance while meeting stringent environmental regulations.

Naval vessels often remain stationary for up to 70% of their operational lifecycle, making idle-time fouling prevention a critical requirement. Advanced copper-acrylate SPC coatings are engineered to provide static protection for up to 30 days, preventing the accumulation of hard fouling organisms that can affect vessel performance and acoustic signatures. This is particularly important in defense applications where stealth and operational readiness are paramount.

From a performance perspective, acrylate-based SPC coatings deliver a controlled and linear polishing rate, maintaining a smooth hull surface throughout the service lifecycle. This contributes to improved hydrodynamic efficiency, enabling speed increases of 3% to 5% while reducing wake turbulence. These characteristics provide a tactical advantage in naval operations, particularly in high-sensitivity environments.

Environmental compliance is also a key focus. Modern naval-grade SPC coatings utilize non-persistent biocides and advanced binder technologies designed to meet evolving environmental standards set by defense agencies in the United States and Europe. This ensures long-term regulatory compliance without compromising operational performance.

Self-Polishing Copolymers (SPC) Lead Antifouling Paints Market with 41.5% Share Driven by Long-Term Hull Efficiency

Product Chemistry Analysis: SPC Coatings Dominate with Predictable Polishing and Carbon Compliance Benefits

Self-Polishing Copolymers (SPC) hold a leading 41.5% share of the antifouling paints and coatings market in 2025, driven by their ability to deliver consistent, long-term antifouling performance over a 60-month dry-docking cycle. These coatings, based on silyl acrylate and copper acrylate chemistries, undergo controlled hydrolysis in seawater, enabling a continuous “self-polishing” effect that maintains a smooth hull surface throughout the vessel lifecycle. This directly translates into fuel efficiency gains and reduced carbon emissions, aligning with IMO Carbon Intensity Indicator (CII) and EU ETS compliance requirements. A fouled hull can increase fuel consumption by 15%–30%, making SPC coatings a critical investment for shipowners seeking operational savings. The market is witnessing a strong shift toward copper acrylate SPC formulations, which reduce reliance on booster biocides by 20–30%, improving both cost-efficiency and environmental performance while maintaining antifouling efficacy.

Maintenance & Repair (MRO) Segment Dominates with 68.4% Share Driven by Global Fleet Recoating Demand

User Segment Analysis: Installed Vessel Base and Dry-Docking Cycles Fuel MRO Growth

The Maintenance and Repair (MRO) segment accounts for 68.4% of the antifouling paints market in 2025, making it the largest consumer due to the vast installed base of over 60,000 ocean-going vessels requiring periodic recoating every 2.5 to 5 years. Unlike OEM newbuild demand, which is limited to approximately 1,200–1,500 ships annually, MRO demand remains stable and recession-resistant, as vessels must comply with classification society inspection and certification requirements. This segment also consumes higher paint volumes per vessel due to surface reconditioning, stripe coatings, and touch-up applications, increasing material usage by 10–15% compared to new builds. Decision-making in MRO is increasingly driven by fleet managers and technical superintendents, who prioritize hull performance analytics and fuel savings ROI. This has accelerated the adoption of premium SPC and foul-release coatings, reinforcing MRO’s dominance in the global antifouling coatings market.

Antifouling Paints and Coatings Market Competitive Landscape Driven by Decarbonization and Advanced Marine Technologies

The antifouling paints and coatings market is driven by biocide-free coatings, silyl-based technologies, and fouling release systems. Leading players are focusing on fuel efficiency, emission reduction, and long-life marine coatings to support IMO regulations, CII and EEXI compliance, and performance optimization across global shipping and offshore sectors.

AkzoNobel strengthens antifouling coatings leadership through merger-driven innovation and slime release technology

AkzoNobel remains a dominant force in antifouling paints and coatings, supported by its International® portfolio and strategic consolidation initiatives. The proposed merger with Axalta Coating Systems, targeted for completion in 2026, is expected to generate $600 million in cost synergies and expand R&D capabilities for low-VOC antifouling coatings. The company reported 15.1% profitability in Q3 2025, supported by a 10% improvement in production efficiency through operational optimization. Its Intersleek® 1100SR coating continues to lead in biocide-free slime release technology, reducing hull resistance and improving fuel efficiency. Sustainability performance includes a 47% reduction in Scope 1 and 2 emissions compared to 2018, nearing long-term decarbonization targets. Product development focuses on environmentally compliant, high-performance marine coatings.

Jotun expands antifouling coatings capabilities with hull performance systems and offshore energy focus

Jotun A/S continues to strengthen its position in antifouling coatings through strong financial performance and global expansion. The company reported record revenues of NOK 34.3 billion in 2025, driven by growth in offshore energy and emerging markets. Expansion into Africa and the Middle East, supported by new production facilities, enhances its global supply capabilities. Its Hull Skating Solutions technology integrates robotic cleaning to prevent biofouling and has been verified to reduce CO2 emissions by 35.9 million tonnes annually. Strategic focus on floating wind projects in 2026 reflects increasing demand for specialized coatings in renewable energy infrastructure. Product innovation centers on performance optimization and emission reduction.

Hempel drives antifouling coatings growth with silicone hull systems and strong marine segment performance

Hempel A/S is advancing in antifouling paints and coatings through its Accelerate to Win strategy and strong marine coatings portfolio. The company reported €2.165 billion in revenue in 2025 with an 18.2% EBITDA margin, reflecting record financial performance. Its Marine segment reached €750 million in revenue, supported by high demand in drydock and newbuilding markets. The Hempaguard® range, including Hempaguard NB, provides silicone-based antifouling coatings optimized for hydrodynamic efficiency from initial vessel deployment. These coatings support compliance with CII and EEXI regulations by reducing fuel consumption and emissions. Product development focuses on high-efficiency, low-emission marine coatings.

PPG Industries enhances antifouling coatings with electrostatic application and copper-free solutions

PPG Industries is transforming antifouling coatings through advanced application technologies and sustainable product innovation. Its Sigmaglide® 2390 coating delivers up to 20% power savings and maintains performance during idle periods of up to 150 days. The adoption of electrostatic coating technology in shipyards has reduced overspray by 40%, improving application efficiency and lowering VOC emissions. The NEXEON™ 810 coating introduces copper-free antifouling technology with photodegradable biocides for reduced environmental impact. The company reduced carbon emissions by 15% in 2025, with sustainably advantaged coatings accounting for 43% of total sales. Product development emphasizes efficiency, sustainability, and advanced marine coatings technologies.

Chugoku Marine Paints advances silyl antifouling coatings with data-driven performance integration

Chugoku Marine Paints (CMP) remains a leader in antifouling coatings through its expertise in silyl-based technologies and strong presence in Asian shipbuilding markets. The company expanded its manufacturing footprint in China in 2026 to align with the region’s dominant share of global shipbuilding capacity. Its SEAFLO NEO SL ZX coating delivers ultra-low friction performance with reduced speed loss over extended service intervals, supporting ISO 19030 standards. CMP’s participation in the RightShip Zero Harm Innovation program aligns its R&D with global safety and ESG requirements. Its CMP-MAP digital platform integrates hull performance data with coating analytics, enabling real-time operational optimization. Product innovation focuses on durability, efficiency, and data-driven coating performance.

South Korea Antifouling Paints and Coatings Market: AI-Driven Formulation and Hydrogel Systems Advancing Maritime Efficiency

South Korea continues to dominate the antifouling paints and coatings market through its leadership in shipbuilding and next-generation coating technologies. The integration of AI-driven formulation systems such as K-Smart is revolutionizing product development by drastically reducing R&D cycles for customized antifouling coatings. This technological edge is enabling rapid innovation in ultra-low friction coatings, supporting enhanced vessel performance and reduced operational costs.

The country’s shipbuilding giants have standardized hydrogel-based foul-release coatings across LNG and methanol-fueled vessels, ensuring compliance with global carbon intensity targets. Innovations such as nano-type antifouling paints and integrated hull monitoring systems are improving fuel efficiency and enabling real-time performance tracking. Government incentives promoting VOC-free coatings and infrastructure investments in specialized marine coating centers are further strengthening South Korea’s position as a global leader in advanced antifouling paints and coatings.

China Antifouling Paints and Coatings Market: Graphene Reinforcement and Eco-Friendly Marine Coatings Scaling Rapidly

China’s antifouling paints and coatings market is characterized by high-volume production and rapid adoption of environmentally sustainable technologies. Government mandates under the “Healthy Ocean” initiative are accelerating the transition toward silicone-based, biocide-free antifouling coatings, particularly for vessels operating in sensitive marine ecosystems.

Technological advancements are reshaping the market, with the commercialization of graphene-reinforced antifouling primers offering superior durability and corrosion resistance. The expansion of offshore wind energy infrastructure is further driving demand for long-life antifouling coatings on marine structures. Additionally, innovations such as biomimetic coatings inspired by shark-skin textures are improving hydrodynamic performance and reducing acoustic signatures in naval applications. Continuous investments in R&D and manufacturing capacity are reinforcing China’s leadership in advanced antifouling coating technologies.

Japan Antifouling Paints and Coatings Market: Low-Friction Membrane Technology and Self-Healing Coatings Driving Innovation

Japan remains a global innovator in antifouling paints and coatings, focusing on precision chemical engineering and performance optimization. The development of advanced low-friction membrane technologies is significantly reducing vessel drag, improving fuel efficiency, and extending maintenance cycles.

Innovations such as self-healing coatings are enhancing durability by automatically repairing surface damage, preventing localized fouling. The integration of antifouling coatings in autonomous vessel systems and advanced sensor technologies is expanding application scope. Regulatory initiatives promoting environmentally safe coatings and incentives for low-leaching systems are further driving adoption. Additionally, advancements in robotic hull cleaning technologies are improving maintenance efficiency, positioning Japan as a leader in high-performance antifouling solutions.

United States Antifouling Paints and Coatings Market: Naval Modernization and Bio-Based Coating Technologies Driving Growth

The United States antifouling paints and coatings market is driven by strong demand from naval and offshore sectors, supported by advancements in coating technologies and regulatory compliance. The modernization of naval fleets is accelerating the adoption of multifunctional antifouling coatings that extend maintenance intervals and enhance operational efficiency.

Technological innovation is focused on developing environmentally friendly coating systems, including enzyme-based solutions that prevent marine organism attachment without harmful chemicals. Investments in offshore energy infrastructure are further driving demand for specialized antifouling coatings. Regulatory frameworks are promoting safer alternatives to traditional copper-based coatings, encouraging the adoption of advanced biocide-free systems. These developments position the United States as a key player in high-performance antifouling coatings.

Norway Antifouling Paints and Coatings Market: Autonomous Shipping and Sustainable Marine Coating Leadership

Norway’s antifouling paints and coatings market is defined by its leadership in sustainable maritime technologies and autonomous shipping systems. The widespread adoption of silicone-hydrogel coatings is improving fuel efficiency and reducing environmental impact, particularly in protected marine environments.

Technological advancements are enabling the integration of intelligent coating systems that monitor performance and signal maintenance requirements. Innovations such as ultrasonic antifouling technologies are complementing coating systems, enhancing effectiveness. Government initiatives supporting green shipping corridors and strict sustainability standards are accelerating the adoption of advanced antifouling coatings. Additionally, developments in aquaculture applications are expanding market opportunities, reinforcing Norway’s position as a global leader in eco-friendly marine coatings.

Singapore Antifouling Paints and Coatings Market: Digital Monitoring and High-Efficiency Marine Maintenance Solutions

Singapore’s antifouling paints and coatings market is evolving through digital innovation and its strategic role as a global maritime hub. The integration of IoT-enabled monitoring systems is enabling real-time tracking of coating performance, improving maintenance efficiency and operational decision-making.

Regulatory advancements are shaping the market, with strict controls on chemical composition and requirements for coating durability under high-pressure cleaning conditions. The expansion of port infrastructure and research facilities is supporting the development of advanced antifouling coatings tailored for tropical marine environments. Additionally, the linkage of coating performance with carbon credit systems is encouraging the adoption of high-efficiency coatings that reduce fuel consumption and emissions, positioning Singapore as a leader in smart marine coating solutions.

Germany Antifouling Paints and Coatings Market: Biomimetic Surfaces and Low-VOC Coatings Driving Sustainability

Germany’s antifouling paints and coatings market is characterized by its focus on sustainability and advanced material science. The development of biomimetic coatings inspired by natural structures is enabling high-performance solutions that reduce environmental impact while maintaining effectiveness.

Regulatory leadership in Europe is driving the transition toward low-VOC and biocide-free coating systems. Innovations such as self-replenishing surfaces and hybrid coating technologies are improving durability and performance in marine environments. Additionally, investments in renewable energy infrastructure are expanding the use of antifouling coatings in offshore applications. These developments reinforce Germany’s leadership in sustainable and high-performance antifouling coating technologies.

India Antifouling Paints and Coatings Market: Maritime Infrastructure Expansion and Indigenous Coating Development

India’s antifouling paints and coatings market is gaining momentum, supported by strong government initiatives and expanding maritime infrastructure. The development of indigenous antifouling coatings for defense applications is enhancing domestic capabilities and reducing reliance on imports.

Infrastructure projects under national development programs are increasing demand for antifouling coatings across ports, shipyards, and marine structures. Innovations tailored to tropical climates are improving coating performance in high-temperature environments. Additionally, modernization programs in the fishing industry are driving the adoption of eco-friendly antifouling coatings. Strategic investments and partnerships are further strengthening the market, positioning India as an emerging player in the global antifouling coatings industry.

Antifouling Paints and Coatings Market Report Scope

Antifouling Paints and Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$20.5 Billion

|

|

Market Size (2032)

|

$37 Billion

|

|

Market Growth Rate

|

8.8%

|

|

Segments

|

By Product Chemistry (Self-Polishing Copolymers, Copper-Based Systems, Hybrid and Nano-Hybrid Formulations, Controlled Depletion Polymers, Biocide-Free, Advanced Coatings), By Technology (Conventional, Non-Biocidal Foul Release, Surface-Active Material, Sol-Gel Processed Coatings, Hard Antifouling, Eroding Antifouling), By End-Use Industry (Commercial Shipping, Offshore Energy, Naval and Defense, Recreational and Leisure Boating, Aquaculture, Inland Waterway Transport), By Application Area (Hull Coatings, Underwater Infrastructure, Propellers and Niche Areas, Tank and Ballast Coatings), By User Segment (OEM, Maintenance and Repair), By Service Duration (Short-term, Standard, Extended Service)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Akzo Nobel N.V., Jotun A/S, Hempel A/S, PPG Industries, Inc., Chugoku Marine Paints, Ltd., The Sherwin-Williams Company, Nippon Paint Marine Coatings Co., Ltd., Kansai Paint Co., Ltd., BASF SE, RPM International Inc., Axalta Coating Systems Ltd., KCC Corporation, Boero YachtCoatings, New Nautical Coatings, Inc., Sika AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Antifouling Paints and Coatings Market Segmentation

By Product Chemistry

- Self-Polishing Copolymers

- Copper-Based Systems

- Hybrid and Nano-Hybrid Formulations

- Controlled Depletion Polymers

- Biocide-Free

- Advanced Coatings

By Technology

- Conventional

- Non-Biocidal Foul Release

- Surface-Active Material

- Sol-Gel Processed Coatings

- Hard Antifouling

- Eroding Antifouling

By End-Use Industry

- Commercial Shipping

- Offshore Energy

- Naval and Defense

- Recreational and Leisure Boating

- Aquaculture

- Inland Waterway Transport

By Application Area

- Hull Coatings

- Underwater Infrastructure

- Propellers and Niche Areas

- Tank and Ballast Coatings

By User Segment

- OEM

- Maintenance and Repair

By Service Duration

- Short-term

- Standard

- Extended Service

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Antifouling Paints and Coatings Market

- Akzo Nobel N.V.

- Jotun A/S

- Hempel A/S

- PPG Industries, Inc.

- Chugoku Marine Paints, Ltd.

- The Sherwin-Williams Company

- Nippon Paint Marine Coatings Co., Ltd.

- Kansai Paint Co., Ltd.

- BASF SE

- RPM International Inc

- Axalta Coating Systems Ltd.

- KCC Corporation

- Boero YachtCoatings

- New Nautical Coatings, Inc.

- Sika AG

*- List not Exhaustive

Table of Contents: Antifouling Paints and Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Antifouling Paints and Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Antifouling Paints and Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Role of Antifouling Coatings in Fuel Efficiency and Emission Reduction

2.4. Impact of IMO Biofouling Guidelines and Environmental Regulations

2.5. Growth in Global Shipping, Offshore Energy, and Marine Infrastructure

3. Innovations Reshaping the Antifouling Paints and Coatings Market

3.1. Trend: Silicone-Based and Biocide-Free Fouling-Release Technologies

3.2. Trend: Digital Analytics and Smart Coating Performance Monitoring

3.3. Opportunity: Extended Dry-Docking Coatings for VLECs and LNG Vessels

3.4. Opportunity: Advanced SPC and Copper-Acrylate Technologies for Naval Applications

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Antifouling Paints and Coatings Market

5.1. By Product Chemistry

5.1.1. Self-Polishing Copolymers

5.1.2. Copper-Based Systems

5.1.3. Hybrid and Nano-Hybrid Formulations

5.1.4. Controlled Depletion Polymers

5.1.5. Biocide-Free

5.1.6. Advanced Coatings

5.2. By Technology

5.2.1. Conventional

5.2.2. Non-Biocidal Foul Release

5.2.3. Surface-Active Material

5.2.4. Sol-Gel Processed Coatings

5.2.5. Hard Antifouling

5.2.6. Eroding Antifouling

5.3. By End-Use Industry

5.3.1. Commercial Shipping

5.3.2. Offshore Energy

5.3.3. Naval and Defense

5.3.4. Recreational and Leisure Boating

5.3.5. Aquaculture

5.3.6. Inland Waterway Transport

5.4. By Application Area

5.4.1. Hull Coatings

5.4.2. Underwater Infrastructure

5.4.3. Propellers and Niche Areas

5.4.4. Tank and Ballast Coatings

5.5. By User Segment

5.5.1. OEM

5.5.2. Maintenance and Repair

5.6. By Service Duration

5.6.1. Short-term

5.6.2. Standard

5.6.3. Extended Service

6. Country Analysis and Outlook of Antifouling Paints and Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Antifouling Paints and Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Antifouling Paints and Coatings Market Size Outlook to 2032

7.1.1. By Product Chemistry

7.1.2. By Technology

7.1.3. By End-Use Industry

7.1.4. By Application Area

7.1.5. By User Segment

7.1.6. By Service Duration

7.2. Europe Antifouling Paints and Coatings Market Size Outlook to 2032

7.2.1. By Product Chemistry

7.2.2. By Technology

7.2.3. By End-Use Industry

7.2.4. By Application Area

7.2.5. By User Segment

7.2.6. By Service Duration

7.3. Asia Pacific Antifouling Paints and Coatings Market Size Outlook to 2032

7.3.1. By Product Chemistry

7.3.2. By Technology

7.3.3. By End-Use Industry

7.3.4. By Application Area

7.3.5. By User Segment

7.3.6. By Service Duration

7.4. South America Antifouling Paints and Coatings Market Size Outlook to 2032

7.4.1. By Product Chemistry

7.4.2. By Technology

7.4.3. By End-Use Industry

7.4.4. By Application Area

7.4.5. By User Segment

7.4.6. By Service Duration

7.5. Middle East and Africa Antifouling Paints and Coatings Market Size Outlook to 2032

7.5.1. By Product Chemistry

7.5.2. By Technology

7.5.3. By End-Use Industry

7.5.4. By Application Area

7.5.5. By User Segment

7.5.6. By Service Duration

8. Company Profiles: Leading Players in the Antifouling Paints and Coatings Market

8.1. Akzo Nobel N.V.

8.2. Jotun A/S

8.3. Hempel A/S

8.4. PPG Industries, Inc.

8.5. Chugoku Marine Paints, Ltd.

8.6. The Sherwin-Williams Company

8.7. Nippon Paint Marine Coatings Co., Ltd.

8.8. Kansai Paint Co., Ltd.

8.9. BASF SE

8.10. RPM International Inc

8.11. Axalta Coating Systems Ltd.

8.12. KCC Corporation

8.13. Boero YachtCoatings

8.14. New Nautical Coatings, Inc.

8.15. Sika AG

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures