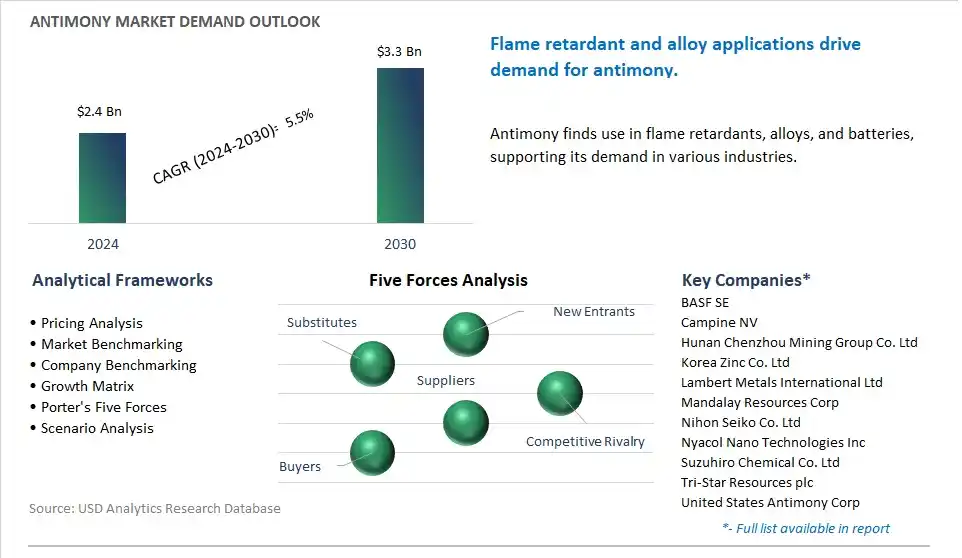

The global Antimony Market is poised to register a 5.5% CAGR from $2.4 Billion in 2024 to $3.3 Billion in 2030.

The global Antimony Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Trioxides, Alloys, Others), By Application (Flame Retardant, Plastic Additives, Lead Acid Batteries, Glass & Ceramics, Others), By End-User (Chemical, Automotive, Electrical & Electronics, Others).

An Introduction to Global Antimony Market in 2024

The antimony market is experiencing steady growth driven by increasing demand in flame retardants, lead-acid batteries, and semiconductor industries. Key trends shaping the future of the industry include the growing adoption of antimony compounds such as antimony trioxide and antimony pentoxide as synergists and halogen-free flame retardants in plastics, textiles, and construction materials to enhance fire safety and meet regulatory requirements. Moreover, there's a rising emphasis on antimony recycling and sustainable sourcing practices, leading to innovations in recovery technologies and closed-loop recycling systems to reduce environmental impact and ensure a stable supply chain. Additionally, advancements in antimony refining, alloying, and purification methods are driving innovation and market competitiveness, enabling antimony producers to offer high-quality and cost-effective solutions for diverse industrial applications in the global antimony market.

Antimony Market Competitive Landscape

The market report analyses the leading companies in the industry including BASF SE, Campine NV, Hunan Chenzhou Mining Group Co. Ltd, Korea Zinc Co. Ltd, Lambert Metals International Ltd, Mandalay Resources Corp, Nihon Seiko Co. Ltd, Nyacol Nano Technologies Inc, Suzuhiro Chemical Co. Ltd, Tri-Star Resources plc, United States Antimony Corp, Yiyang Huachang Antimony Industry Co. Ltd, Yunnan Muli Antimony Industry Co. Ltd.

Antimony Market Dynamics

Antimony Market Trend: Increasing Demand for Flame Retardants and Antimony Trioxide

A prominent market trend for antimony is the increasing demand for flame retardants and antimony trioxide in various industries including plastics, textiles, electronics, and construction. Antimony compounds, particularly antimony trioxide, serve as effective flame retardants by inhibiting the ignition and spread of fires in materials such as plastics, textiles, and building materials. With stringent regulations and safety standards mandating the use of flame retardants to improve fire safety in consumer products and construction materials, there's a growing demand for antimony-based flame retardants to meet regulatory requirements and enhance fire resistance in end-use applications. The trend towards greater adoption of flame retardant solutions drives market demand for antimony as a key component in flame retardant formulations.

Antimony Market Driver: Growth in Electronics and Electrical Industries

A significant driver for the antimony market is the growth in electronics and electrical industries, particularly in emerging markets and developing economies. Antimony finds extensive use in the production of lead-acid batteries, which are essential components in automotive vehicles, uninterruptible power supply (UPS) systems, and renewable energy storage solutions. Additionally, antimony-based alloys are utilized in the manufacturing of soldering materials, semiconductors, and electronic components such as diodes and infrared detectors. With the proliferation of electronic devices, telecommunications infrastructure, and renewable energy technologies worldwide, there's a corresponding increase in demand for antimony as a critical raw material for electronics and electrical applications, driving market growth for antimony-based products.

Antimony Market Opportunity: Development of Antimony Substitutes and Alternative Applications

An opportunity for the antimony market lies in the development of antimony substitutes and alternative applications in response to environmental and regulatory concerns. While antimony-based products offer effective flame retardant properties and performance benefits, there's increasing scrutiny and restrictions on the use of antimony compounds due to environmental and health concerns. Manufacturers have the opportunity to innovate and develop alternative flame retardant formulations using non-halogenated compounds, phosphorus-based additives, or intumescent coatings that offer comparable fire protection properties while minimizing environmental impact and health risks. Additionally, there's potential to explore alternative applications for antimony in industries such as metallurgy, catalysts, and glass production, leveraging its unique properties such as hardness, corrosion resistance, and catalytic activity. By investing in research and development of antimony substitutes and alternative applications, manufacturers can address market demand for safer and more sustainable flame retardant solutions, and diversify their product portfolio for broader market opportunities.

Antimony Market Share Analysis: Trioxides segment generated the highest revenue in the industry

The largest segment in the Antimony Market is Trioxides, and this dominance is driven by Antimony trioxide (Sb2O3) is the most common and widely produced form of antimony, accounting for a significant portion of global antimony consumption. Antimony trioxide is primarily used as a flame retardant synergist in plastics, rubber, textiles, and other materials to enhance their fire resistance properties. Its ability to inhibit the spread of flames and suppress smoke generation makes it indispensable in industries where fire safety is paramount, such as construction, electronics, automotive, and aerospace. Additionally, antimony trioxide finds applications in the production of polyethylene terephthalate (PET) bottles for beverages, as a catalyst in the production of polyester fibers and resins, and as a pigment in paints, ceramics, and glass. In addition, the growing demand for flame retardant materials in response to stringent fire safety regulations and increasing awareness of the importance of fire protection further drives the consumption of antimony trioxide. Further, its relatively low cost, high effectiveness as a flame retardant, and compatibility with a wide range of materials contribute to its widespread use and dominance in the Antimony Market. Over the forecast period, the dominance of Trioxides in the Antimony Market is driven by its essential role as a flame retardant additive and its versatility in various industrial applications where fire safety is critical.

Antimony Market Share Analysis: Flame Retardant Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Antimony Market is Flame Retardant, and this growth is driven by Flame retardants, including antimony compounds such as antimony trioxide (Sb2O3), are essential additives used to enhance the fire resistance properties of various materials, including plastics, textiles, rubber, and electronics. With increasing concerns about fire safety and stringent regulations governing building codes and product standards, there is a growing demand for flame retardant materials across industries such as construction, automotive, electronics, and textiles. Antimony compounds act as effective synergists in flame retardant formulations, where they inhibit the ignition and spread of flames and reduce smoke emissions during combustion. Additionally, antimony-based flame retardants offer advantages such as high efficiency, versatility, and compatibility with a wide range of polymers and materials. In addition, the growing adoption of flame retardant materials in emerging economies, where rapid urbanization and infrastructure development drive the demand for fire-resistant building materials and consumer products, further fuels the growth of the Flame Retardant segment in the Antimony Market. Further, advancements in flame retardant technologies, including the development of eco-friendly and halogen-free formulations, contribute to the expanding application scope of antimony-based flame retardants. Over the forecast period, the rapid growth of the Flame Retardant segment in the Antimony Market is driven by the increasing demand for fire safety solutions, regulatory requirements, technological advancements, and the versatility of antimony compounds as effective flame retardant additives in various industrial applications.

Antimony Market Share Analysis: Electrical & Electronics Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Antimony Market is Electrical & Electronics, and this growth is driven by Antimony finds extensive use in the electrical and electronics industry due to its unique properties and diverse applications. One of the primary applications of antimony in this sector is as an alloying agent in lead-acid batteries, which are essential components in various electronic devices, automotive vehicles, and industrial equipment. Lead-acid batteries require antimony to enhance their mechanical strength, resistance to corrosion, and Over the forecast period performance, especially in deep-cycle and high-demand applications such as electric vehicles and uninterruptible power supply (UPS) systems. Additionally, antimony compounds, particularly antimony trioxide (Sb2O3), serve as crucial additives in flame retardant formulations used in electrical and electronic products to meet safety standards and regulatory requirements. Further, the increasing demand for consumer electronics, telecommunications equipment, and renewable energy technologies such as solar panels and wind turbines drives the consumption of antimony in the Electrical & Electronics segment. In addition, advancements in electronic device miniaturization, energy storage technologies, and semiconductor manufacturing processes further contribute to the growing demand for antimony-based materials and compounds in the electrical and electronics industry. Over the forecast period, the rapid growth of the Electrical & Electronics segment in the Antimony Market is driven by the expanding applications of antimony in lead-acid batteries, flame retardants, and electronic components, coupled with the evolving trends in consumer electronics, automotive electrification, and renewable energy adoption.

Antimony Market Report Segmentation

By Product

Trioxides

Alloys

Others

By Application

Flame Retardant

Plastic Additives

Lead Acid Batteries

Glass & Ceramics

Others

By End-User

Chemical

Automotive

Electrical & Electronics

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Antimony Companies Profiled in the Market Study

BASF SE

Campine NV

Hunan Chenzhou Mining Group Co. Ltd

Korea Zinc Co. Ltd

Lambert Metals International Ltd

Mandalay Resources Corp

Nihon Seiko Co. Ltd

Nyacol Nano Technologies Inc

Suzuhiro Chemical Co. Ltd

Tri-Star Resources plc

United States Antimony Corp

Yiyang Huachang Antimony Industry Co. Ltd

Yunnan Muli Antimony Industry Co. Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Antimony Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Antimony Market Size Outlook, $ Million, 2021 to 2030

3.2 Antimony Market Outlook by Type, $ Million, 2021 to 2030

3.3 Antimony Market Outlook by Product, $ Million, 2021 to 2030

3.4 Antimony Market Outlook by Application, $ Million, 2021 to 2030

3.5 Antimony Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Antimony Industry

4.2 Key Market Trends in Antimony Industry

4.3 Potential Opportunities in Antimony Industry

4.4 Key Challenges in Antimony Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Antimony Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Antimony Market Outlook by Segments

7.1 Antimony Market Outlook by Segments, $ Million, 2021- 2030

By Product

Trioxides

Alloys

Others

By Application

Flame Retardant

Plastic Additives

Lead Acid Batteries

Glass & Ceramics

Others

By End-User

Chemical

Automotive

Electrical & Electronics

Others

8 North America Antimony Market Analysis and Outlook To 2030

8.1 Introduction to North America Antimony Markets in 2024

8.2 North America Antimony Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Antimony Market size Outlook by Segments, 2021-2030

By Product

Trioxides

Alloys

Others

By Application

Flame Retardant

Plastic Additives

Lead Acid Batteries

Glass & Ceramics

Others

By End-User

Chemical

Automotive

Electrical & Electronics

Others

9 Europe Antimony Market Analysis and Outlook To 2030

9.1 Introduction to Europe Antimony Markets in 2024

9.2 Europe Antimony Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Antimony Market Size Outlook by Segments, 2021-2030

By Product

Trioxides

Alloys

Others

By Application

Flame Retardant

Plastic Additives

Lead Acid Batteries

Glass & Ceramics

Others

By End-User

Chemical

Automotive

Electrical & Electronics

Others

10 Asia Pacific Antimony Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Antimony Markets in 2024

10.2 Asia Pacific Antimony Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Antimony Market size Outlook by Segments, 2021-2030

By Product

Trioxides

Alloys

Others

By Application

Flame Retardant

Plastic Additives

Lead Acid Batteries

Glass & Ceramics

Others

By End-User

Chemical

Automotive

Electrical & Electronics

Others

11 South America Antimony Market Analysis and Outlook To 2030

11.1 Introduction to South America Antimony Markets in 2024

11.2 South America Antimony Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Antimony Market size Outlook by Segments, 2021-2030

By Product

Trioxides

Alloys

Others

By Application

Flame Retardant

Plastic Additives

Lead Acid Batteries

Glass & Ceramics

Others

By End-User

Chemical

Automotive

Electrical & Electronics

Others

12 Middle East and Africa Antimony Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Antimony Markets in 2024

12.2 Middle East and Africa Antimony Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Antimony Market size Outlook by Segments, 2021-2030

By Product

Trioxides

Alloys

Others

By Application

Flame Retardant

Plastic Additives

Lead Acid Batteries

Glass & Ceramics

Others

By End-User

Chemical

Automotive

Electrical & Electronics

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

BASF SE

Campine NV

Hunan Chenzhou Mining Group Co. Ltd

Korea Zinc Co. Ltd

Lambert Metals International Ltd

Mandalay Resources Corp

Nihon Seiko Co. Ltd

Nyacol Nano Technologies Inc

Suzuhiro Chemical Co. Ltd

Tri-Star Resources plc

United States Antimony Corp

Yiyang Huachang Antimony Industry Co. Ltd

Yunnan Muli Antimony Industry Co. Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Trioxides

Alloys

Others

By Application

Flame Retardant

Plastic Additives

Lead Acid Batteries

Glass & Ceramics

Others

By End-User

Chemical

Automotive

Electrical & Electronics

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)