Antiviral Coatings Market Size and Growth Driven by Public Health Priorities and Advanced Surface Protection Technologies

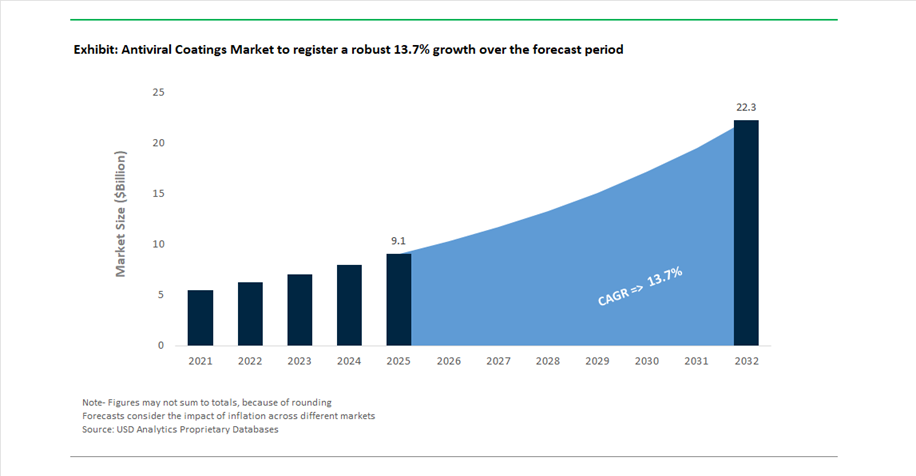

The Antiviral Coatings Market is projected to grow from USD 9.1 billion in 2025 to USD 22.35 billion by 2032, registering a robust CAGR of 13.7%. This accelerated growth reflects the increasing global emphasis on infection prevention, public health safety, and hygienic infrastructure, particularly across healthcare facilities, public transportation systems, commercial buildings, and consumer electronics.

Antiviral coatings are engineered to neutralize or deactivate viruses upon contact, utilizing advanced technologies such as nanoparticle-based agents, photocatalytic materials, and bioactive compounds. These coatings are becoming essential in environments where high-touch surfaces and airborne contamination risks are prevalent, including hospitals, airports, schools, and mass transit networks. The post-pandemic landscape has significantly elevated the importance of continuous, passive protection mechanisms, driving adoption beyond traditional healthcare applications into residential and commercial sectors.

Technological advancements are centered on nanotechnology-enabled coatings with long-lasting efficacy, capable of maintaining antiviral activity under continuous use and repeated cleaning cycles. Additionally, the integration of low-VOC, waterborne, and sustainable resin systems is aligning the market with tightening environmental regulations. The growing role of smart coatings and AI-driven material discovery is further accelerating innovation, enabling the development of coatings that are both highly effective and environmentally compliant.

The market is also benefiting from increasing demand for multi-functional coatings, combining antiviral properties with antibacterial, anti-fungal, and easy-to-clean characteristics, ensuring comprehensive surface protection. Competitive dynamics are defined by intensive R&D investment, strategic collaborations, and expansion into high-value applications, positioning antiviral coatings as a critical component of modern hygiene and safety ecosystems

AI-Driven R&D, Regulatory Standardization, and Strategic Expansion Accelerating Market Evolution

The antiviral coatings market is undergoing rapid transformation driven by advanced research initiatives, strategic consolidation, and regulatory alignment. Innovation is increasingly focused on AI-driven material discovery and next-generation coating chemistries. In February 2026, Nippon Paint, in collaboration with the University of Tokyo, launched Phase II of its R&D initiative, leveraging generative AI to develop environmentally friendly antiviral coatings with continuous efficacy against evolving viral strains. This builds on the success of its PROTECTON® antiviral coatings, which are already deployed across high-traffic environments.

Product development is also aligning with regulatory and environmental requirements. PPG’s HI-GARD® Non-Methanol coating reflects the shift toward solvent-free and compliant formulations, serving as a base for integrating antiviral and optical functionalities in applications such as ophthalmic lenses. Similarly, Arkema’s March 2026 expansion of bio-based acrylic monomer production supports the development of low-carbon antiviral coatings, enabling manufacturers to meet sustainability targets without compromising performance.

Capacity expansion and regional strategies are strengthening market penetration. Sherwin-Williams’ March 2026 facility expansion in Kentucky is aimed at increasing production of specialized functional coatings, including antiviral systems for consumer electronics and appliances. Additionally, AkzoNobel’s decision to retain its International Research Center in India reinforces its focus on global development of high-performance antimicrobial and antiviral coatings.

Standardization and validation are emerging as critical factors in market maturity. In June 2025, the European Committee for Standardization (CEN) launched a workshop to establish standardized testing protocols for antimicrobial and antiviral coatings, providing a unified framework for evaluating efficacy under real-world conditions. This initiative enhances market credibility and regulatory acceptance, facilitating broader adoption across industries.

Corporate strategies are increasingly aligned with premiumization and application expertise. Axalta’s record earnings in February 2026 highlight the growing demand for high-functionality coatings, while PPG’s $10 million investment in applicator training (March 2026) underscores the importance of precision application in maintaining antiviral effectiveness. Additionally, Kansai Paint’s strategic focus on high-functionality coatings (April 2025) includes the deployment of Shikkui antiviral coatings, leveraging natural lime-based chemistry for viral inactivation.

EPA Residual Efficacy Protocols Raising the Bar for Long-Lasting Antiviral Coatings

The antiviral coatings industry is undergoing a critical regulatory shift as the U.S. Environmental Protection Agency enforces updated residual efficacy testing protocols under MLB SOP MB-40 and MB-41. These revisions represent a decisive move toward real-world validation of long-lasting antiviral claims, eliminating reliance on generalized antimicrobial data and requiring product-specific virucidal verification. This shift has significantly reduced the number of market participants able to substantiate durability claims for antiviral coatings.

Under the updated framework, coatings must pass mandatory virucidal efficacy testing that simulates real-world conditions through alternating wet and dry abrasion cycles. This ensures that coatings maintain antiviral performance despite mechanical wear and repeated cleaning. The regulatory emphasis on durability is further reinforced by stricter residual claim limitations. As of 2026, any antiviral coating claiming efficacy beyond one week requires direct EPA consultation, replacing earlier guidance that allowed up to four weeks without formal review. This change is constraining marketing claims and forcing manufacturers to recalibrate product positioning strategies.

Consistency requirements have also been tightened. Manufacturers must now demonstrate efficacy across two independent production lots, ensuring reproducibility against target viruses such as SARS-CoV-2 and Norovirus. This reflects a broader shift toward precision validation and quality assurance in antiviral coatings. Additionally, all products undergoing testing after October 7, 2023 must comply with these updated protocols, triggering a widespread revalidation cycle across existing product portfolios.

These regulatory developments are elevating technical entry barriers and driving investment in advanced formulation science, durability testing, and compliance infrastructure, positioning validated long-lasting antiviral coatings as a premium segment within the broader antimicrobial coatings market.

EU BPR Classification of Copper(I) Oxide Accelerating Transition to Alternative Virucidal Technologies

The European antiviral coatings market is experiencing increased regulatory pressure following the classification of Copper(I) Oxide as a Candidate for Substitution under the Biocidal Products Regulation. This designation introduces a mandatory comparative assessment requirement, forcing manufacturers to demonstrate that no safer or more effective alternatives exist before obtaining or renewing product approvals.

This regulatory classification is significantly impacting product development strategies. Approximately 30% of antiviral coating R&D budgets in Europe are now being redirected toward alternative technologies, including bio-based organic virucides and photocatalytic titanium dioxide systems. These alternatives are being developed to mitigate the risk of future restrictions or bans on copper-based actives, which have historically been widely used due to their strong virucidal performance.

Administrative complexity is also increasing. Renewal applications for copper-based products must be submitted at least 550 days prior to authorization expiry, requiring long-term regulatory planning. Furthermore, the mandatory adoption of the IUCLID submission format from July 1, 2026 is increasing the documentation burden for manufacturers, necessitating more structured and data-intensive regulatory filings.

This evolving regulatory landscape is accelerating the transition toward non-metallic and hybrid antiviral technologies, creating opportunities for innovation in photocatalytic and bio-based coating systems that can deliver high efficacy while meeting stringent safety and environmental criteria.

Long-Term Care Facilities Driving Demand for Continuous Antiviral Surface Protection

The heightened vulnerability of long-term care facilities to viral outbreaks is creating a strong demand for passive antiviral coatings that provide continuous surface protection. High-touch surfaces such as bed rails, handrails, and nurse call systems represent critical transmission vectors, making them priority targets for antiviral surface treatments.

Advanced antiviral coatings are demonstrating strong efficacy even in the presence of organic contaminants, a key requirement in healthcare environments where bio-burden levels are high. Copper-based and hybrid antiviral systems have shown the ability to maintain virucidal performance under these conditions, providing reliable protection between scheduled cleaning cycles. Clinical evaluations indicate that residual antiviral coatings can achieve sustained 3-log reductions in viral load within two hours, effectively bridging the hygiene gap between manual disinfection events.

From an economic perspective, the adoption of antiviral coatings in long-term care facilities offers measurable return on investment. By reducing surface-mediated transmission of respiratory viruses, facilities can potentially lower outbreak-related healthcare costs and staffing disruptions by 15% to 20%. This is particularly relevant in aging populations where infection control is directly linked to patient outcomes and operational efficiency.

Public Transit Surface Engineering Creating New Opportunities for Durable Antiviral Coatings

Public transportation systems are increasingly adopting antiviral coatings as part of broader efforts to restore passenger confidence and enhance hygiene standards. High-contact surfaces such as grab handles, seating areas, and stanchions are key application areas where durable antiviral coatings can provide continuous protection in high-density environments.

Operational efficiency is a major driver in this segment. The application of long-lasting antiviral coatings reduces the need for frequent deep-cleaning interventions, allowing transit operators to maintain vehicles in service for up to 10% longer per operational cycle. This translates into improved fleet utilization and reduced maintenance costs. To meet these operational demands, coatings must demonstrate high durability under continuous mechanical stress. Industry specifications now require coatings to maintain antiviral efficacy for 12 to 24 months while withstanding abrasion from thousands of daily passenger interactions.

Innovation is also emerging in smart coating technologies. Photocatalytic coatings based on titanium dioxide are gaining traction, leveraging ambient light to activate antiviral properties without relying on chemical leaching. These systems offer a sustainable and low-maintenance solution for transit environments where continuous exposure to light can be harnessed for passive disinfection.

Sol-Gel Technology Leads Antiviral Coatings Market with 41% Share Driven by Photocatalytic Efficiency and Surface Versatility

Coating Technology Analysis: TiO₂-Based Sol-Gel Coatings Dominate with Transparent, Self-Activating Antiviral Properties

Sol-Gel technology captures a leading 41.0% share of the antiviral coatings market in 2025, driven by its unmatched application versatility, optical transparency, and long-lasting antiviral performance. This technology utilizes metal alkoxides such as titanium dioxide (TiO₂) and silicon dioxide (SiO₂) to form a nanoporous, glass-like coating that can be applied at room temperature on heat-sensitive substrates, including plastics, textiles, and painted surfaces. The key innovation lies in photocatalytic antiviral action, where TiO₂ nanoparticles generate reactive oxygen species (ROS) under visible or UV-A light, effectively neutralizing viruses like SARS-CoV-2, Influenza, and Norovirus within 15–60 minutes. Unlike traditional disinfectants, this creates a self-regenerating antiviral surface. Additionally, Sol-Gel coatings maintain high optical clarity, making them ideal for touchscreens, glass partitions, and consumer electronics, positioning them as the dominant solution in the global antiviral coatings market.

Medical & Healthcare Sector Leads with 32% Share Driven by Continuous Viral Protection and Infection Control Standards

End-Use Industry Analysis: High-Touch Surface Protection and Regulatory Compliance Fuel Market Growth

The medical and healthcare segment holds a 32.0% share of the antiviral coatings market in 2025, driven by the urgent need to prevent hospital-acquired viral infections (HAVI) and reduce operational disruptions. Viral outbreaks in healthcare facilities can result in $200,000–$500,000 per incident due to ward closures and deep-cleaning costs, making antiviral coatings a critical investment. These coatings are widely applied on high-touch surfaces such as bed rails, nurse call buttons, overbed tables, privacy curtains, and waiting room furniture, ensuring continuous viral suppression. A major industry shift is toward “terminal cleaning plus continuous protection”, where antiviral coatings act as a 24/7 passive defense layer, reducing viral load between cleaning cycles. Furthermore, increasing scrutiny from The Joint Commission and CMS is pushing hospitals to adopt EPA-registered antiviral coatings as part of compliance and liability mitigation strategies. This regulatory and operational pressure solidifies healthcare as the largest segment in the global antiviral coatings market.

Antiviral Coatings Market Competitive Landscape Driven by Nanotechnology and Smart Surface Protection

The antiviral coatings market is driven by silver-ion coatings, metal-oxide nanocoatings, and low-VOC formulations. Leading players are integrating antiviral functionality into architectural coatings, medical devices, consumer electronics, and public infrastructure to enhance hygiene, durability, and regulatory compliance across high-touch environments.

AkzoNobel advances antiviral coatings with nanoparticle technology and durable powder systems

AkzoNobel leads the antiviral coatings market through its Interpon® and Dulux portfolios, integrating antiviral protection into architectural and industrial coatings. The company is progressing toward its Axalta merger in 2026, aimed at strengthening R&D capabilities in low-VOC antiviral powder coatings. It achieved a 47% reduction in Scope 1 and 2 emissions in 2025 while advancing eco-friendly antiviral biocide systems aligned with regulatory standards. Its coatings utilize silver-ion and metal-oxide nanoparticle technologies to deliver transparent, long-lasting antiviral protection without altering surface aesthetics. The Interpon AM range now features Active Surface Defense capable of maintaining efficacy after more than 10,000 scrub cycles in healthcare environments. Product development focuses on durability, sustainability, and high-performance antiviral coatings.

PPG Industries expands antiviral coatings with integrated solutions for transportation and electronics

PPG Industries strengthens its position in antiviral coatings through large-scale industrial integration and diversified applications. The company showcased antiviral coating solutions under its MASTER'S MARK™ and TIKKURILA™ brands, targeting residential and commercial interior applications. Its copper-based and silver-ion coatings are widely used in public transportation systems, supported by strong supply chain integration across North America and Asia. The Color Now 2026 initiative includes antiviral clearcoats for consumer electronics with added anti-fingerprint and anti-smudge properties. PPG is expanding digital manufacturing capabilities to ensure consistent coating thickness, which is critical for antiviral performance. Product innovation focuses on multifunctional coatings and large-scale deployment.

Nippon Paint accelerates antiviral coatings growth with AI-driven innovation and APAC expansion

Nippon Paint Holdings is a key growth player in antiviral coatings, driven by strategic acquisitions and advanced R&D initiatives. The acquisition of AOC in 2025 expanded its presence in Europe and North America while strengthening its technical capabilities. Its VirusGuard coatings are proven to be 99.9% effective against viruses including SARS-CoV-2 and H1N1, using proprietary inactivation technology that maintains indoor air quality. The company is targeting revenue growth through expansion of antiviral smart building materials across APAC markets. AI-driven product development initiatives focus on near-zero VOC antiviral coatings for healthcare applications. Product development emphasizes sustainability, scalability, and advanced coating technologies.

Sherwin-Williams enhances antiviral coatings with smart surface technologies and healthcare applications

Sherwin-Williams leverages its extensive distribution network to lead antiviral coatings in healthcare and institutional markets. The company expanded production capacity in Kentucky in 2026 to support growing demand for antimicrobial and antiviral coatings. Its coatings are widely used in medical devices and healthcare environments, designed to withstand UV-C sterilization and chemical disinfectants without losing efficacy. Integration of smart coating technologies enables real-time monitoring of surface hygiene, advancing the concept of connected surfaces. The company is also developing bio-based resin systems to support sustainable construction and LEED-certified projects. Product innovation focuses on durability, monitoring capabilities, and regulatory compliance.

Hydromer delivers specialized antiviral coatings with integrated application systems for medical devices

Hydromer Inc. is a niche leader in antiviral coatings for medical and industrial applications, focusing on integrated coating solutions. The company expanded into automated coating equipment in 2026, combining antiviral chemistry with high-speed application systems to improve manufacturing efficiency. Its hydrophilic coatings, enhanced with antiviral agents, are widely used in medical devices such as catheters, stents, and surgical instruments. The new automated coating systems improve coating consistency by 30%, ensuring compliance with global regulatory standards. Hydromer’s integrated approach reduces time-to-market for manufacturers by providing both materials and application technologies. Product development focuses on precision coating, medical-grade performance, and process optimization.

United States Antiviral Coatings Market: EPA Enforcement and Medical-Grade Innovations Reshaping Industry Standards

The United States antiviral coatings market remains the global benchmark, driven by stringent EPA enforcement and rapid advancements in medical-grade coating technologies. Increased regulatory scrutiny under FIFRA has led to over $10.6 million in penalties for non-compliant antiviral claims, forcing a market shift toward verified, long-lasting antiviral coatings with proven efficacy. This regulatory tightening is accelerating consolidation and strengthening the adoption of high-performance polymer-based antiviral solutions across healthcare and infrastructure sectors.

Innovation is a key growth driver, particularly with FDA-approved antiviral coatings for surgical robotics using non-eluting technologies to prevent cross-contamination in automated operating environments. Infrastructure investments under the Bipartisan Infrastructure Law are expanding the use of antiviral coatings in HVAC systems and airport facilities. Public transit modernization projects, including nano-copper antiviral coatings in major metro systems, are improving hygiene in high-density environments. Additionally, advancements in photo-active antiviral coatings that neutralize viruses under LED lighting are redefining performance standards, while PRIA 5 is streamlining regulatory approvals for next-generation antiviral coatings.

China Antiviral Coatings Market: Smart City Deployment and Graphene-Based Coating Innovations Driving Scale

China dominates the antiviral coatings market in terms of production scale and infrastructure deployment, supported by strong government initiatives and technological advancements. The integration of antiviral coatings in smart city infrastructure, including public kiosks, ATMs, and high-speed rail systems, is being mandated under the “Healthy China 2030” initiative, significantly expanding application scope.

Technological innovation is centered around advanced materials such as graphene-silver hybrid coatings, which are widely used in consumer electronics to prevent pathogen transmission on touchscreens. Massive investments in infection-proof logistics hubs are driving the adoption of antiviral coatings in cold-chain packaging and port infrastructure. Regulatory modernization is also accelerating innovation, with streamlined pathways for clinical trials of antiviral materials. Additionally, advancements in manufacturing techniques such as magnetron sputtering are improving coating quality and consistency for large-scale applications, reinforcing China’s leadership in high-volume antiviral coating production.

Germany Antiviral Coatings Market: Sustainable Chemistry and Automotive Integration Driving High-Performance Coatings

Germany’s antiviral coatings market is defined by its leadership in sustainable chemistry and precision engineering. The development of VOC-free, plant-based antiviral coatings using chitosan-derived materials is aligning with strict EU environmental standards, particularly in public infrastructure applications.

The automotive sector is a major driver, with leading manufacturers integrating photocatalytic antiviral coatings into vehicle interiors to enhance hygiene through ambient light activation. Government initiatives under the Medical Technology Strategy are prioritizing antiviral coatings as a critical component of national biosecurity. Large-scale hospital modernization projects are also boosting demand, with copper-based coatings being applied to high-contact surfaces. Additionally, regulatory frameworks such as VDI standards are setting global benchmarks for antiviral coating durability in ventilation systems, reinforcing Germany’s position as a leader in sustainable and high-performance coating technologies.

Japan Antiviral Coatings Market: Smart Responsive Materials and Nanotechnology Advancements Driving Innovation

Japan’s antiviral coatings market is advancing through cutting-edge nanotechnology and smart material innovations. The development of femtosecond laser-textured antiviral surfaces is enabling physical disruption of viral structures without relying on chemical agents, representing a major breakthrough in sustainable antiviral technologies.

Public infrastructure applications are expanding rapidly, with photocatalytic antiviral coatings deployed across high-speed rail systems, ensuring consistent hygiene in mass transit environments. Innovations in responsive polymers that release antiviral agents only when pathogens are detected are enhancing efficiency and reducing chemical usage. Additionally, Japan’s focus on aging population solutions is driving demand for durable antiviral coatings in healthcare facilities. The integration of antiviral coatings in semiconductor cleanrooms further highlights the market’s diversification, positioning Japan as a leader in advanced antiviral coating technologies.

India Antiviral Coatings Market: Infrastructure Expansion and Domestic Manufacturing Driving Rapid Growth

India is emerging as one of the fastest-growing markets for antiviral coatings, supported by strong government initiatives and expanding healthcare infrastructure. The Production Linked Incentive (PLI) scheme is fostering domestic manufacturing of antiviral chemicals, creating a robust ecosystem for coating innovation.

The adoption of antiviral coatings is expanding across public infrastructure and transportation sectors. High-speed rail projects such as Vande Bharat trains are incorporating silver-ion infused antiviral coatings to enhance passenger safety. Regulatory reforms in food packaging are driving demand for antiviral coatings in polymer films, while pharmaceutical manufacturing hubs are mandating antiviral wall coatings for compliance with global standards. Additionally, government initiatives under Swachh Bharat 2.0 are promoting self-sanitizing surfaces in public sanitation facilities. The rise of startups developing cost-effective antiviral coating technologies is further accelerating market growth, positioning India as a key emerging player.

United Kingdom Antiviral Coatings Market: Graphene Innovation and Biosecurity-Driven Regulatory Evolution

The United Kingdom antiviral coatings market is evolving through strong innovation in graphene-based materials and post-Brexit regulatory flexibility. The deployment of graphene-enhanced antiviral coatings in NHS infrastructure is improving both durability and pathogen resistance, particularly in modular healthcare facilities.

Regulatory divergence under the UK REACH framework is enabling faster testing and adoption of novel antiviral technologies, including metasurface coatings. Applications are expanding into defense and aviation sectors, with antiviral coatings being used in next-generation cockpit systems. Additionally, investments in research and development are supporting advancements in antiviral coatings for educational institutions and public infrastructure. The integration of antiviral coatings in EV charging networks further highlights the market’s diversification, positioning the UK as a leader in advanced antiviral coating technologies.

Singapore Antiviral Coatings Market: Smart Infrastructure and Maritime Applications Driving Advanced Coating Adoption

Singapore’s antiviral coatings market is emerging as a global innovation hub, driven by its focus on smart infrastructure and maritime safety. The deployment of antiviral smart glass coatings in commercial buildings is enhancing both energy efficiency and hygiene standards in urban environments.

Maritime applications are a key growth area, with mandatory antiviral coatings being applied to vessels to prevent cross-border pathogen transmission. The country’s regulatory sandbox for coating technologies is encouraging innovation in cleaning systems and coating durability. Additionally, large-scale infrastructure projects such as Changi Airport Terminal 5 are integrating antiviral coatings into high-density public interfaces. Strategic partnerships with global manufacturers are further strengthening Singapore’s position as a leader in advanced antiviral coating solutions.

Israel Antiviral Coatings Market: Deep-Tech Innovation and Military-Grade Coating Solutions Driving Growth

Israel’s antiviral coatings market stands out for its strong focus on deep-tech innovation and defense applications. The development of self-healing antiviral coatings is enabling long-lasting protection even under extreme wear conditions, making them ideal for industrial and military environments.

The country’s defense sector is a major driver, with high demand for antiviral-coated systems used in aviation and emergency response equipment. Innovations in biomimetic coatings that eliminate viruses through physical mechanisms are redefining performance standards. Additionally, advancements in medical robotics and agricultural technologies are expanding the application scope of antiviral coatings. Strong venture capital investments in next-generation coating technologies are further accelerating innovation, positioning Israel as a global leader in advanced antiviral coating solutions.

Antiviral Coatings Market Report Scope

Antiviral Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.1 Billion

|

|

Market Size (2032)

|

$22.4 Billion

|

|

Market Growth Rate

|

13.7%

|

|

Segments

|

By Material (Metallic Nanoparticles, Antiviral Polymers, Functional Nanomaterials, Liquid-Repellent Surfaces), By Coating Technology (Sol-Gel Process, Chemical Vapor Deposition, Physical Vapor Deposition, Atomic Layer Deposition, Self-Assembled Monolayers, Micro-encapsulation), By Form (Liquid Coatings, Powder Coatings, Aerosol and Spray-on, Films and Laminates), By Substrate Compatibility (Metal, Plastics and Polymers, Glass and Ceramics, Textiles and Non-wovens, Porous Surfaces), By End-Use Industry (Medical and Healthcare, Building and Construction, Transportation and Automotive, Consumer Electronics, Packaging, Protective Clothing, Sports and Leisure)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, Nippon Paint Holdings Co., Ltd., Axalta Coating Systems Ltd., BASF SE, Kansai Paint Co., Ltd., Hempel A/S, Jotun A/S, Bio-Gate AG, Nano-Care Deutschland AG, Microban International, Ltd., BioCote Limited, Nanovere Technologies, LLC, Arkema S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Antiviral Coatings Market Segmentation

By Material

- Metallic Nanoparticles

- Silver

- Copper

- Zinc

- Titanium Dioxide

- Antiviral Polymers

- Quaternary Ammonium Compounds

- N-Halamines

- Chitosan and Bio-derived Polymers

- Functional Nanomaterials

- Graphene and Carbon Nanotubes

- Mesoporous Silica

- Liquid-Repellent Surfaces

By Coating Technology

- Sol-Gel Process

- Chemical Vapor Deposition

- Physical Vapor Deposition

- Atomic Layer Deposition

- Self-Assembled Monolayers

- Micro-encapsulation

By Form

- Liquid Coatings

- Powder Coatings

- Aerosol and Spray-on

- Films and Laminates

By Substrate Compatibility

- Metal

- Plastics and Polymers

- Glass and Ceramics

- Textiles and Non-wovens

- Porous Surfaces

By End-Use Industry

- Medical and Healthcare

- Building and Construction

- Transportation and Automotive

- Consumer Electronics

- Packaging

- Protective Clothing

- Sports and Leisure

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Antiviral Coatings Market

- PPG Industries, Inc

- Akzo Nobel N.V

- The Sherwin-Williams Company

- Nippon Paint Holdings Co., Ltd.

- Axalta Coating Systems Ltd.

- BASF SE

- Kansai Paint Co., Ltd.

- Hempel A/S

- Jotun A/S

- Bio-Gate AG

- Nano-Care Deutschland AG

- Microban International, Ltd.

- BioCote Limited

- Nanovere Technologies, LLC

- Arkema S.A.

*- List not Exhaustive

Table of Contents: Antiviral Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Antiviral Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Antiviral Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Role of Antiviral Coatings in Public Health and Hygienic Infrastructure

2.4. Regulatory Landscape: EPA Protocols and EU BPR Compliance

2.5. Demand Across Healthcare, Public Transit, Consumer Electronics, and Smart Infrastructure

3. Innovations Reshaping the Antiviral Coatings Market

3.1. Trend: AI-Driven Material Discovery and Nanotechnology-Enabled Coatings

3.2. Trend: Photocatalytic and Sol-Gel-Based Self-Activating Antiviral Systems

3.3. Opportunity: Long-Term Care Facilities and Continuous Surface Protection

3.4. Opportunity: Public Transportation Surface Engineering and Smart Coatings

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Antiviral Coatings Market

5.1. By Material

5.1.1. Metallic Nanoparticles

5.1.1.1. Silver

5.1.1.2. Copper

5.1.1.3. Zinc

5.1.1.4. Titanium Dioxide

5.1.2. Antiviral Polymers

5.1.2.1. Quaternary Ammonium Compounds

5.1.2.2. N-Halamines

5.1.2.3. Chitosan and Bio-derived Polymers

5.1.3. Functional Nanomaterials

5.1.3.1. Graphene and Carbon Nanotubes

5.1.3.2. Mesoporous Silica

5.1.3.3. Liquid-Repellent Surfaces

5.2. By Coating Technology

5.2.1. Sol-Gel Process

5.2.2. Chemical Vapor Deposition

5.2.3. Physical Vapor Deposition

5.2.4. Atomic Layer Deposition

5.2.5. Self-Assembled Monolayers

5.2.6. Micro-encapsulation

5.3. By Form

5.3.1. Liquid Coatings

5.3.2. Powder Coatings

5.3.3. Aerosol and Spray-on

5.3.4. Films and Laminates

5.4. By Substrate Compatibility

5.4.1. Metal

5.4.2. Plastics and Polymers

5.4.3. Glass and Ceramics

5.4.4. Textiles and Non-wovens

5.4.5. Porous Surfaces

5.5. By End-Use Industry

5.5.1. Medical and Healthcare

5.5.2. Building and Construction

5.5.3. Transportation and Automotive

5.5.4. Consumer Electronics

5.5.5. Packaging

5.5.6. Protective Clothing

5.5.7. Sports and Leisure

6. Country Analysis and Outlook of Antiviral Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Antiviral Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Antiviral Coatings Market Size Outlook to 2032

7.1.1. By Material

7.1.2. By Coating Technology

7.1.3. By Form

7.1.4. By Substrate Compatibility

7.1.5. By End-Use Industry

7.2. Europe Antiviral Coatings Market Size Outlook to 2032

7.2.1. By Material

7.2.2. By Coating Technology

7.2.3. By Form

7.2.4. By Substrate Compatibility

7.2.5. By End-Use Industry

7.3. Asia Pacific Antiviral Coatings Market Size Outlook to 2032

7.3.1. By Material

7.3.2. By Coating Technology

7.3.3. By Form

7.3.4. By Substrate Compatibility

7.3.5. By End-Use Industry

7.4. South America Antiviral Coatings Market Size Outlook to 2032

7.4.1. By Material

7.4.2. By Coating Technology

7.4.3. By Form

7.4.4. By Substrate Compatibility

7.4.5. By End-Use Industry

7.5. Middle East and Africa Antiviral Coatings Market Size Outlook to 2032

7.5.1. By Material

7.5.2. By Coating Technology

7.5.3. By Form

7.5.4. By Substrate Compatibility

7.5.5. By End-Use Industry

8. Company Profiles: Leading Players in the Antiviral Coatings Market

8.1. PPG Industries, Inc.

8.2. Akzo Nobel N.V.

8.3. The Sherwin-Williams Company

8.4. Nippon Paint Holdings Co., Ltd.

8.5. Axalta Coating Systems Ltd.

8.6. BASF SE

8.7. Kansai Paint Co., Ltd.

8.8. Hempel A/S

8.9. Jotun A/S

8.10. Bio-Gate AG

8.11. Nano-Care Deutschland AG

8.12. Microban International, Ltd.

8.13. BioCote Limited

8.14. Nanovere Technologies, LLC

8.15. Arkema S.A.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures