Market Overview: Semiconductor-Grade Chemistry and Aerospace “Dry Wash” Technologies Accelerate Aqueous Based Metal Cleaners Market Expansion

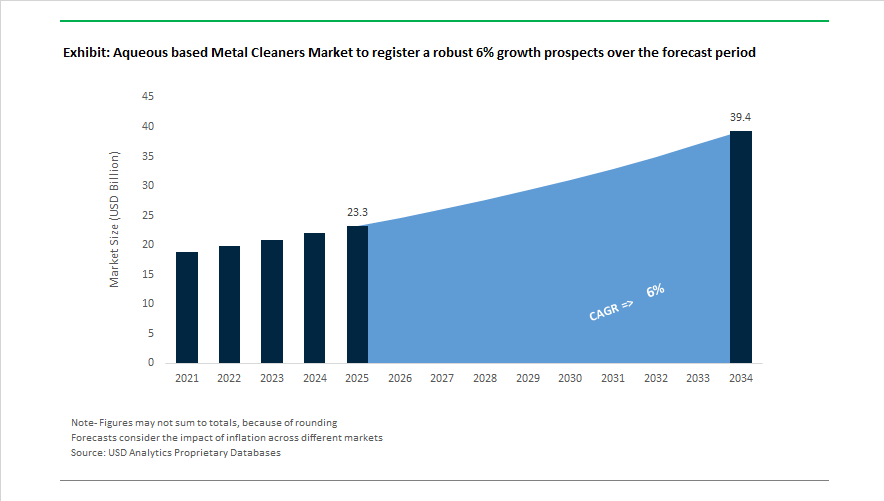

The aqueous based metal cleaners market is valued at $23.3 billion in 2025 and is projected to reach $39.4 billion by 2034, advancing at a 6% CAGR. Growth is anchored in rising adoption of water-based industrial cleaners, low-VOC degreasers, aqueous precision cleaning chemicals, semiconductor wafer cleaning solutions, aircraft exterior cleaners, and eco-friendly metal surface treatment fluids. A critical technology milestone occurred in September 2023–2024 when Dow commercialized DOWSIL CC-8000, a biodegradable aqueous formulation for removing uncured silicone residues in electronics and automotive assembly. This marked a structural shift away from solvent-heavy degreasers toward safer, water-compatible chemistries suited for high-precision metal parts. The industrial ecosystem consolidated in January 2024 when MacDermid Enthone Industrial Solutions acquired the cleaning chemical business of All Star Chemical, strengthening its portfolio of aqueous cleaners used in automotive and aerospace finishing operations.

Manufacturing sustainability and process efficiency became dominant themes during 2024–2025. In September 2024, Zeller+Gmelin introduced Zubora TTS PF, a mineral-oil-free, water-miscible cooling lubricant that integrates metalworking performance with aqueous environmental compliance. In May 2024, Quick Sheen launched an eco-friendly aqueous metal polish targeting marine and commercial transport maintenance. By May 2025, Chemetall converted its Langelsheim production site to 100% renewable electricity, reinforcing decarbonization across corrosion protection and cleaning chemistries. At Lubricant Expo Europe in August 2025, Petrofer advanced its ENVO line of sustainable aqueous cleaners designed to lower chemical consumption in die casting and heat treatment operations, improving total cost of ownership.

Advanced aerospace, semiconductor, and packaging requirements intensified the technology transition in September–October 2025. Henkel launched Bonderite C-AK DW 805 AERO in October 2025, a ready-to-use aqueous dry-wash aircraft cleaner that eliminates rinse water, cuts wastewater treatment costs, and reduces aircraft downtime. In the same month, Henkel introduced Darex COV phthalate-free metal packaging sealants using aqueous-compatible chemistry for food-contact applications. BASF announced construction of an electronic-grade ammonium hydroxide plant in Ludwigshafen in October 2025, supporting semiconductor wafer cleaning expansion in Europe. Chemetall and Azelis extended their Southeast Asia distribution alliance in September 2025, followed by Chemetall receiving its tenth consecutive Airbus SQIP Award and opening an application laboratory in Vietnam in late 2025, strengthening regional aerospace and automotive surface treatment support.

Trends and Opportunities Transforming the Aqueous Based Metal Cleaners Market

Market Trend: Regulatory Phase-Out of NPEs and Phosphonate Chelators Reshaping Formulation Strategies

Across North America and the European Union, environmental mandates are no longer just targeting volatile organic compounds. They now focus on the chemical composition of the surfactants and chelating agents themselves, creating a structural reformulation cycle in the aqueous-based metal cleaners market.

Under EU REACH Annex XVII (2025), Nonylphenol Ethoxylates (NPEs) are capped at 0.1% by weight, forcing manufacturers to migrate toward glucamide and alcohol ethoxylate surfactants. Similarly, state-level regulation in California is accelerating the elimination of phosphonate and EDTA-based chelators in industrial effluent systems. These changes are driving adoption of MGDA and GLDA, which provide equivalent degreasing performance in hard water while minimizing contribution to eutrophication and wastewater chemical load.

Meanwhile, enforcement of TSCA Risk Management rules in the U.S. has initiated “substitution-by-design,” where companies proactively re-engineer formulations ahead of 2026 compliance deadlines. Industry data from the American Cleaning Institute shows that over 30% of industrial metal cleaners have already been reformulated to meet these restrictions. These regulatory pressures are rewiring raw materials sourcing, raising the competitive advantage of suppliers with green-chemistry surfactant portfolios and chelator IP.

Market Trend: Shift Toward "Clean + Protect" Aqueous Systems With Built-In Corrosion Inhibitors

Manufacturers across automotive, aerospace and machinery assembly are moving toward single-step aqueous cleaners that can both remove contaminants and deposit a controlled passivating layer to delay corrosion.

In November 2025, Henkel's BONDERITE® C-NE evolution showcased a leap in this category, achieving up to 90 days of indoor corrosion protection on steel, cast iron and non-ferrous metals. By forming ultra-thin conductive film layers that do not interfere with precision gauging, these new-age cleaners eliminate the need for downstream oiling, drying or dip-tank cycles.

Production-line data published in 2025 indicates that integrated "clean-and-protect" systems reduce chemical disposal by 15–20% and lower energy usage, particularly in multi-stage washing halls. With organic, carboxylate-based inhibitors now representing 72% of the corrosion-inhibiting additives market, OEMs using aluminum and magnesium lightweight frames are adopting these chemistries as a default fixture in their supply contracts.

Market Opportunity: Ultra-Clean Aqueous Formulations for EV Battery Gigafactory Contamination Control

The fastest-scaling opportunity is tied to the lithium-ion battery manufacturing ecosystem, where cleanliness failure can cause safety defects and catastrophic cell rejection.

Busbar welding lines and aluminum battery-cooling plates now mandate aqueous-cleaned, residue-free metal surfaces to ensure adhesion of thermal interface materials (TIMs). In June 2025, BASF’s Schwarzheide Black Mass plant formalized a new industrial specification where aqueous cleaning is preferred over solvent-based degreasers for thermal management metal components.

Battery OEM audits in 2025 show that surface preparation must meet ISO 16232 particulate cleanliness metrics, a threshold that legacy cleaners cannot meet. This has created a premium niche for low-conductivity aqueous formulations, which prevent ionic residue-induced micro-shorts. Quaker Houghton’s 2025 acquisition of Dipsol Chemicals explicitly targets this fast-growing segment for EV electrification surface-prep solutions.

As gigafactory capacity expands in Europe, China and the U.S., supply contracts increasingly specify “aqueous purity-certified suppliers,” positioning the segment as a mission-critical and recurring revenue stream for chemical producers.

Market Opportunity: Precision-Grade Cleaners for Spot-Free Drying in Medical, Aerospace and Optics

Beyond industrial workshops, high-value precision sectors demand aqueous cleaners engineered for flawless end-surface condition.

In hospitals, ultrasonic-compatible aqueous cleaners reduce manual scrubbing times by 35% when paired with deionized-water rinse and vacuum drying workflows. These cleaners are also used on orthopedic implants where spot-free finishes are mandatory for regulatory approval and surface biocompatibility.

New 2025-era sheeting-surfactant chemistry enables rinse water surface tension to drop below 30 mN/m, creating rapid runoff and preventing water-mark formation. This is particularly relevant in aerospace, where mineral spotting on high-tolerance engine hardware affects aerodynamic performance and thermal expansion.

The move toward semiconductor-grade cleaning quality is also spilling into the metal finishing market. BASF’s October 2025 launch of an Electronic-Grade Ammonium Hydroxide plant in Germany signals a future where semiconductor-style purity cascades into mainstream automotive and energy metals, raising the compliance bar for all suppliers.

Aqueous Based Metal Cleaners Market Share and Segmentation Insights

Technology-Led Market Share Dynamics: Spray Cleaning Leads While Ultrasonic Accelerates Fastest

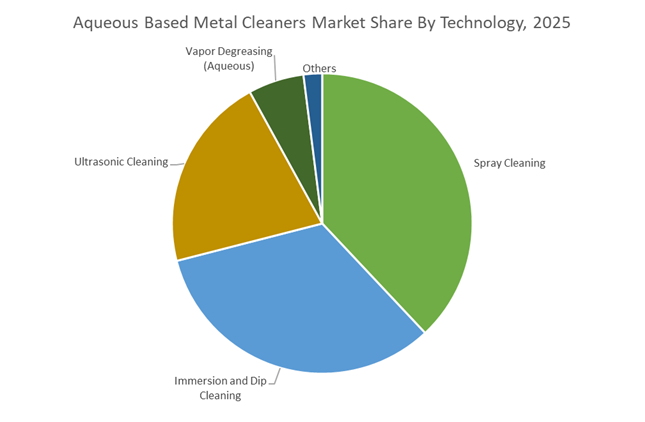

In 2025, spray cleaning commands 38% of the global aqueous based metal cleaners market, making it the dominant technology due to its high throughput, seamless integration with automated production lines, and superior performance on large surface areas. Conveyorized spray washers using alkaline water-based cleaners with surfactants are now standard across automotive powertrain and general manufacturing, with EV motor housings and battery trays emerging as key growth drivers. Immersion and dip cleaning ranks second, favored for complex geometries and high-volume small components such as fasteners and bearings, though bath life management and disposal costs constrain margins. Ultrasonic cleaning is the fastest-growing segment, driven by micron-level cleanliness requirements in medical devices, semiconductors, aerospace hydraulics, and optics, supported by ISO 16232 and VDA 19 standards. Aqueous vapor degreasing remains niche. Regulatory pressure on VOCs and HAPs continues accelerating solvent-to-aqueous conversion, particularly across Asia-Pacific.

End-Use Industry Market Share: Manufacturing Dominates as Electronics and Healthcare Drive Premium Growth

By end-use, general manufacturing holds the largest 2025 market share at 34%, supported by sustained demand from metal fabrication, heavy equipment, and industrial machinery, where alkaline aqueous cleaners with corrosion inhibitors dominate cost-sensitive workflows. Automotive ranks second, spanning engine and drivetrain cleaning, EV motor housings, inverter casings, battery trays, and aftermarket reconditioning, with closed-loop water recycling systems increasingly adopted to meet zero-liquid discharge mandates. Electronics and semiconductors represent the fastest-growing vertical, requiring ultra-pure aqueous chemistries for PCB assemblies and wafer processing with ionic contamination below 1 µg/cm², driven by miniaturization and 5G components. Aerospace and defense remains a high-margin segment governed by AMS and OEM specifications, while healthcare provides recession-resistant demand for enzymatic and pH-neutral cleaners. Regionally, Asia-Pacific accounts for ~45% of global consumption, with North America leading precision cleaning.

Aqueous Based Metal Cleaners Market Competitive Landscape

The aqueous based metal cleaners market is rapidly evolving as manufacturers transition from solvent-based degreasers to low-temperature aqueous cleaning systems, bio-based surfactants, phosphate-free builders, and ultra-high-purity formulations. Competitive differentiation now centers on nanotechnology-enabled surface wetting, low-concentration efficiency, residue-free corrosion protection, and circular bath-life extension. Market leaders are investing heavily in AI-driven formulation optimization, green chelates, mass-balance bio-based chemistry, and integrated wastewater management, driven by growing demand from EV battery manufacturing, aerospace pretreatment, semiconductor fabrication, and medical devices. Strategic priorities include energy-efficient ambient cleaning, hard-water tolerant chemistries, and fully recyclable aqueous systems, positioning aqueous metal cleaners as a core pillar of sustainable industrial processing.

Nanotechnology-driven circular metal cleaning innovation by Henkel AG & Co. KGaA

Henkel leads the aqueous metal cleaners market through its Bonderite® portfolio, delivering alkaline and neutral cleaners for high-precision automotive and aerospace pretreatment. In early 2026, Henkel introduced nanotechnology-based aqueous cleaners that achieve superior contaminant removal at ambient temperatures, cutting energy consumption by up to 30%. A February 2026 collaboration with Sekab integrates bio-based ethyl acetate and ethanol-derived surfactants into Henkel’s industrial cleaning platforms. Under its “Regenerative Planet” framework, Henkel is advancing 100% circular cleaning systems, emphasizing oil-splitting formulations that extend bath life and reduce waste, strengthening its position in sustainable metal surface preparation.

Process-integrated aqueous cleaning systems from Quaker Houghton

Quaker Houghton approaches aqueous metal cleaning as a critical manufacturing node through its Fluidcare™ chemical management platform, providing onsite monitoring to ensure zero-defect downstream coating and plating. In late 2025, the company expanded its Advanced Solutions segment, targeting customized aqueous cleaning for EV battery trays and aerospace composites. Its cleaners deliver residue-free corrosion protection, leaving an invisible protective film during inter-process storage without secondary rinsing. For 2026, Quaker Houghton is prioritizing low-concentration efficiency, enabling high cleaning power with reduced chemical usage, lowering logistics costs while supporting sustainable industrial operations.

Mass-balance surfactant chemistry and digital optimization by BASF SE

BASF strengthens the aqueous based metal cleaners market through high-purity surfactants and builders that power next-generation cleaning formulations, especially for electronics and semiconductor manufacturing. During 2025–2026, BASF scaled low-temperature aqueous pretreatment agents capable of removing heavy greases at just 35°C. The company announced a Global Digital Hub in Hyderabad in Q1 2026, leveraging AI analytics to optimize cleaner performance for APAC manufacturers. Strategically, BASF is transitioning toward mass-balance bio-based surfactants, enabling drop-in sustainability while maintaining identical molecular performance to fossil-derived cleaning systems.

Surfactant and chelation expertise powering aqueous descaling by Stepan Company

Stepan operates as a surfactant powerhouse for aqueous metal cleaning, integrating high-performance sequestrants and inhibitors following its PerformanX Specialty Chemicals acquisition. The company dominates neutral and acidic aqueous chemistries used for rust removal and descaling in heavy industrial and construction equipment applications. In late 2025, Stepan expanded its Specialty Products segment into healthcare and medical device cleaning, where low-residue aqueous systems are essential. Its core strength lies in advanced chelating technology, allowing cleaners to remain effective in hard-water environments without scale buildup on processing equipment.

Ultra-high-purity aqueous systems and circular water management from Evonik Industries AG

Evonik delivers precision functionality to aqueous metal cleaners through smart materials and advanced additives. In 2025, the company launched Next-Generation Solutions for wafer cleaning and complex electronic geometries requiring zero metallic contamination. Under its SYNEQT strategy, Evonik is refining its portfolio toward high-margin aqueous system solutions for water treatment and ultra-pure metal cleaning. The company uniquely integrates cleaning chemistries with PAA/H2O2 wastewater disinfection, enabling customers to manage the full water lifecycle. Evonik’s “Beyond Chemistry” vision targets circular, biodegradable aqueous systems as a major growth driver.

Bio-based chelates and phosphate-free innovation led by Nouryon

Nouryon is redefining aqueous metal cleaning through bio-based performance chemistry. In February 2026, it launched FinnFix® PB MAX, a 100% biodegradable cellulose polymer that prevents soil redeposition in aqueous systems. The company is a global leader in green chelates such as GLDA, replacing EDTA while delivering superior oxide removal with ready biodegradability. Nouryon has allocated over 75% of its R&D pipeline to Eco-Premium Solutions, targeting phosphorus-free builders. A new biodegradable chelates facility opened in the Netherlands in 2025 further strengthens Nouryon’s leadership in sustainable aqueous metal cleaners.

Germany Aqueous Based Metal Cleaners Market: Semiconductor-Grade Purity and Circular Manufacturing Compliance

Germany is setting the benchmark for zero-emission and high-purity aqueous metal cleaning. In January 2025, Chemetall, a BASF brand, confirmed that its Langelsheim production site operates on 100% renewable electricity, cutting indirect CO₂ emissions by roughly 620 tonnes annually. This milestone reinforces Germany’s leadership in decarbonized specialty chemical manufacturing.

Semiconductor supply chains are a decisive growth lever. In October 2025, BASF began construction of an electronic-grade ammonium hydroxide plant in Ludwigshafen, addressing Europe’s rising demand for ultra-pure aqueous wafer cleaning and etching solutions. Parallel innovation is occurring at the equipment level. Henkel unveiled Smartwash™ Technology at CES 2025, an AI-driven dosing concept whose algorithmic logic is now being adapted for industrial metal pretreatment to minimize chemical overuse. German OEMs are also adopting low-temperature aqueous immersion with next-generation ultrasonic transducers, reducing energy consumption by 18% versus hot-spray systems. Regulatory reinforcement comes from upcoming Packaging Act updates, which require compatibility with closed-loop wastewater recycling, firmly embedding aqueous cleaners into Germany’s circular manufacturing model.

United States Aqueous Based Metal Cleaners Market: Solvent Prohibitions and Aerospace-Grade Aqueous Transition

The United States market is undergoing a structural pivot driven by regulation and federal funding. On January 1, 2025, the U.S. Environmental Protection Agency finalized its perchloroethylene rule under TSCA, effectively triggering a nationwide migration away from chlorinated solvents toward aqueous-based metal cleaners. This regulatory shift is reinforced by the EPA SNAP program, which in early 2025 approved new aqueous and semi-aqueous blends as acceptable substitutes for ozone-depleting cleaning agents in precision manufacturing.

Federal industrial policy is amplifying adoption. The U.S. Department of Energy announced USD 355 million in late 2025 to support domestic mineral processing, including advanced aqueous leaching and cleaning chemistries for battery-grade metals. At the corporate level, Quaker Houghton reported that digital fluid platforms now extend aqueous bath life by an average of 25% across North American operations. Aerospace compliance is another catalyst, as FAA and NASA updates in 2025 prioritize pH-neutral aqueous cleaners for aluminum and titanium alloys to mitigate hydrogen embrittlement risks. Expanded surfactant availability following Stepan Company’s 2025 integration further strengthens regional supply resilience.

China Aqueous Based Metal Cleaners Market: Environmental Codification and Ultra-Pure Manufacturing Hubs

China’s aqueous metal cleaners industry is being reshaped by systemic environmental reform and high-tech manufacturing requirements. The draft Ecological and Environmental Code released in April 2025 consolidates fragmented regulations into a unified framework, mandating full disclosure of hazardous properties for all industrial cleaning agents. This has accelerated the shift toward biodegradable, low-toxicity aqueous formulations compatible with municipal wastewater infrastructure.

Under updated 14th Five-Year Plan targets, China aims for a 95% sewage treatment rate at county level by the end of 2025, directly favoring aqueous cleaners that do not foul treatment membranes. Industrial adoption is evident in steel and electronics. Baosteel launched a near-zero-carbon steel line in 2025, using advanced aqueous surface treatments to prepare hydrogen-smelted steel for automotive applications. Meanwhile, the Suzhou and Wuxi semiconductor corridors transitioned to ultra-pure aqueous cleaning standards to support localized production of 7 nm and below nodes, embedding aqueous chemistries into China’s advanced manufacturing backbone.

India Aqueous Based Metal Cleaners Market: Policy-Driven Localization and ZLD-Compatible Cleaning Systems

India’s growth trajectory is anchored in policy-led manufacturing expansion and water stewardship. In November 2025, the Ministry of Steel launched the third round of the PLI scheme for specialty steel, incentivizing coated steels and superalloys that require high-performance aqueous pretreatment lines. Complementing this, R&D grants under Atmanirbhar Bharat are supporting the development of indigenous corrosion inhibitors tailored for aqueous systems, reducing import dependence in electronics manufacturing.

Regulatory clarity is accelerating adoption in sensitive sectors. The Food Safety and Standards Authority of India introduced 2025 guidelines favoring GRAS-certified aqueous surfactants for metal cleaners used in food-processing machinery. On the infrastructure side, new automotive clusters in Tamil Nadu and Gujarat mandate zero-liquid-discharge systems for metal cleaning installations, structurally embedding aqueous solutions into India’s industrial expansion.

Japan Aqueous Based Metal Cleaners Market: PFAS-Free Enforcement and Battery Circularity

Japan’s aqueous metal cleaners industry is shaped by chemical safety enforcement and battery recycling leadership. Following the 2024 PFAS Action Plan, 2025 saw rapid adoption of PFAS-free aqueous alternatives across semiconductor and precision instrument manufacturing. These formulations are increasingly specified in supplier audits, reflecting Japan’s zero-tolerance stance on persistent fluorinated substances.

Circularity in energy storage is a defining trend. Sumitomo Metal Mining scaled its LiPure technology in 2025, using specialized aqueous cleaners to enable up to 90% water reuse during lithium recovery from battery leachate streams. Updated JIS standards for industrial surface cleaners further reinforce quality differentiation, with Eco-Mark-certified aqueous products commanding a 25 to 30% premium in the domestic B2B market.

Strategic Positioning of the Aqueous-Based Metal Cleaners Industry by Country

Aqueous based Metal Cleaners Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Strategic Impact on Aqueous Metal Cleaners

|

|

Germany

|

Semiconductor purity and circular economy law

|

Ultra-pure, low-energy, closed-loop cleaning systems

|

|

United States

|

TSCA solvent bans and federal funding

|

Rapid substitution of solvents in aerospace and batteries

|

|

China

|

Environmental codification and tech self-sufficiency

|

Biodegradable cleaners and ultra-pure fab standards

|

|

India

|

PLI schemes and ZLD mandates

|

Localized formulations and water-efficient systems

|

|

Japan

|

PFAS enforcement and battery recycling

|

High-margin PFAS-free and circular aqueous chemistries

|

Aqueous based Metal Cleaners Market Report Scope

Aqueous based Metal Cleaners Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$23.3 Billion

|

|

Market Size (2034)

|

$39.4 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Chemistry Type (Alkaline Cleaners, Acidic Cleaners, Neutral Cleaners, Semi Aqueous Cleaners), By Technology (Ultrasonic Cleaning, Spray Cleaning, Immersion and Dip Cleaning, Vapor Degreasing), By Metal Type (Ferrous Metals, Non Ferrous Metals, Noble Metals), By End Use Industry (Automotive, Aerospace and Defense, Healthcare, Electronics and Semiconductors, General Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG and Co KGaA, BASF SE, Dow Inc, Ecolab Inc, Quaker Houghton, Evonik Industries AG, Stepan Company, DuPont de Nemours Inc, Eastman Chemical Company, Nouryon, 3M Company, Solvay SA, Zestron Corporation, Kyzen Corporation, Sumitomo Chemical Co Ltd

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aqueous Based Metal Cleaners Market Segmentation

By Chemistry Type

- Alkaline Cleaners

- Acidic Cleaners

- Neutral Cleaners

- Semi Aqueous Cleaners

By Technology

- Ultrasonic Cleaning

- Spray Cleaning

- Immersion and Dip Cleaning

- Vapor Degreasing

By Metal Type

- Ferrous Metals

- Non Ferrous Metals

- Noble Metals

By End Use Industry

- Automotive

- Aerospace and Defense

- Healthcare

- Electronics and Semiconductors

- General Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Aqueous Based Metal Cleaners Industry

- Henkel AG and Co KGaA

- BASF SE

- Dow Inc

- Ecolab Inc

- Quaker Houghton

- Evonik Industries AG

- Stepan Company

- DuPont de Nemours Inc

- Eastman Chemical Company

- Nouryon

- 3M Company

- Solvay SA

- Zestron Corporation

- Kyzen Corporation

- Sumitomo Chemical Co Ltd

*- List not Exhaustive