Architectural Paint Oxide Market Size and Growth Driven by UV-Stable Pigments and Sustainable Construction Materials

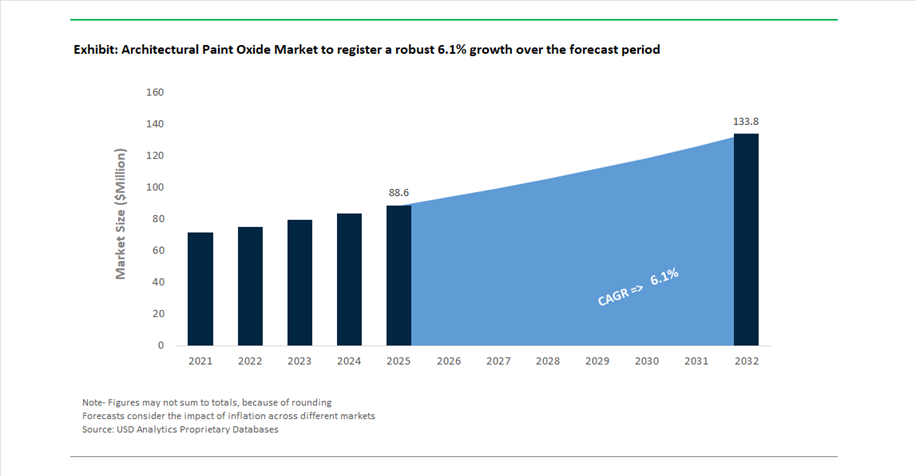

The Architectural Paint Oxide Market is projected to grow from USD 88.6 million in 2025 to USD 134.1 million by 2032, registering a CAGR of 6.1%. This steady growth is driven by the continued reliance on inorganic oxide pigments—particularly iron oxides and titanium dioxide (TiO₂)—for delivering long-lasting color stability, UV resistance, and durability in architectural coatings and construction materials.

Iron oxide pigments remain the industry benchmark for exterior-grade coloration, widely used in decorative paints, concrete colorants, roofing materials, and façade coatings. Their inherent resistance to UV degradation, chemical exposure, and weathering ensures consistent color performance even in harsh outdoor environments, making them indispensable in regions with extreme climatic conditions. Additionally, titanium dioxide plays a critical role in enhancing opacity, brightness, and reflectivity, supporting the development of cool roof coatings and energy-efficient building materials.

The market is also benefiting from the growing shift toward sustainable and environmentally compliant construction solutions. Manufacturers are increasingly focusing on low-carbon pigment production, bio-based binder compatibility, and eco-efficient processing technologies, aligning with global ESG targets and green building certifications. Furthermore, the integration of functional oxide technologies, such as photocatalytic pigments for air purification and self-cleaning surfaces, is expanding the application scope of architectural paint oxides beyond traditional coloration.

Demand is further supported by urbanization, infrastructure development, and renovation activities, particularly in emerging markets where cost-effective and durable pigment solutions are critical. Competitive dynamics are shaped by raw material cost fluctuations, supply chain optimization, and continuous innovation in pigment chemistry, positioning oxide-based pigments as a foundational component of high-performance architectural coatings

Sustainability-Driven Pigment Innovation, Strategic Consolidation, and Cost Pressures Reshaping Market Dynamics

The architectural paint oxide market is evolving through sustainability-led innovation, strategic restructuring, and supply chain realignment, reflecting both growth opportunities and cost pressures within the pigment industry. A major development occurred in March 2026, when LANXESS announced a global price increase of up to 20% for inorganic pigments, including iron oxide and chromium oxide products. This move highlights the impact of rising energy costs, logistics challenges, and raw material volatility, which are reshaping pricing strategies and margin structures across the value chain.

Sustainability is emerging as a key competitive differentiator. In February 2025, LANXESS launched its “Scopeblue” range of iron oxide pigments, produced using renewable energy and eco-efficient raw materials, significantly reducing carbon emissions. Similarly, Sherwin-Williams’ expansion into bio-based oxide binders (late 2025) reflects the growing demand for eco-premium architectural coatings, where natural pigments are combined with sustainable resin systems to deliver both performance and environmental compliance.

Strategic consolidation and portfolio expansion are strengthening market positioning. Cathay Industries’ integration of Venator’s pigment business has significantly enhanced its capabilities in high-purity synthetic iron oxides, enabling broader offerings for premium decorative paints. At the same time, Venator’s post-restructuring focus on titanium dioxide (late 2024) underscores the importance of high-opacity and UV-resistant oxides in key architectural markets across Europe and North America.

Product innovation is also advancing pigment performance and application versatility. LANXESS’ launch of next-generation iron oxide red pigments (July 2025) introduces improved color consistency, dispersion, and mid-range tonal performance, catering to architectural and construction applications. In parallel, Nippon Paint’s photocatalytic innovation platform (July 2024) is leveraging advanced oxide materials such as TiO₂ to develop coatings with air-purifying and self-cleaning capabilities, expanding functional applications beyond aesthetics.

Capacity expansion and operational optimization are further shaping the competitive landscape. Huntsman’s January 2026 asset realignment strategy, including plant closures and production consolidation, reflects efforts to stabilize margins and improve operational efficiency in response to volatile input costs.

Additionally, KRONOS Worldwide’s strategic pivot toward high-purity TiO₂ (mid-2025) highlights the increasing demand for advanced oxide pigments in applications such as cool roof coatings and heat-reflective surfaces, aligning with global energy efficiency trends.

Regulatory Scrutiny on Synthetic Amorphous Silica Driving Safer Material Positioning

The architectural paint oxide industry is navigating a nuanced regulatory landscape surrounding Synthetic Amorphous Silica (SAS), a widely used matting agent and rheology modifier. As of early 2026, SAS has not been classified as a Substance of Very High Concern under EU REACH, allowing continued use in architectural coatings. However, regulatory attention has intensified around particle size distribution and nano-material labeling, introducing a precautionary shift in formulation strategies.

Manufacturers are proactively adapting to anticipated regulatory tightening. Approximately 65% of European pigment suppliers have transitioned toward non-nano SAS grades to avoid potential labeling obligations and consumer scrutiny. This shift reflects a broader industry move toward transparency and risk mitigation, particularly in consumer-facing paint products where regulatory and reputational risks are closely linked.

In parallel, voluntary substitution trends are gaining momentum. Around 15% to 20% of premium architectural coating producers are replacing SAS with bio-based alternatives such as diatomaceous earth and rice husk-derived silica to align with eco-label certifications and sustainability benchmarks. This transition is further supported by the European Chemicals Agency’s “safe and sustainable by design” initiative, which has driven a 40% increase in advanced toxicological data submissions related to silica-based materials.

While SAS remains a functional cornerstone in coating formulations, the increasing regulatory scrutiny and sustainability expectations are reshaping material selection strategies, encouraging the development of safer, transparent, and environmentally aligned alternatives.

Synthetic Iron Oxides from Industrial Waste Streams Transforming Pigment Supply Chains

The architectural coatings industry is undergoing a structural shift in pigment sourcing, moving away from mined iron oxides toward synthetic alternatives derived from steel industry byproducts such as spent pickling liquor. This circular production model is gaining traction due to its superior performance characteristics and strong environmental credentials.

Synthetic iron oxides produced through processes such as the Laux method or pickling liquor recovery consistently achieve purity levels exceeding 95% Fe₂O₃, significantly outperforming natural ochre-based pigments, which typically range between 80% and 85%. This higher purity translates into improved color strength and consistency, with synthetic pigments demonstrating a color variance (ΔE) below 0.5. This level of uniformity enables paint manufacturers to reduce pigment loading by 10% to 15% while maintaining consistent visual output across production batches.

The environmental benefits of this transition are substantial. Producing one ton of synthetic iron oxide from recovered pickling liquor prevents the disposal of approximately 2,500 liters of acidic industrial waste, contributing to waste valorization and improved ESG performance. Additionally, this circular approach reduces the global warming potential of pigment production by approximately 25% compared to traditional mining and processing methods.

This shift toward recovered and synthetic pigment sources is not only enhancing product performance but also aligning the industry with sustainability mandates and circular economy principles, positioning synthetic iron oxides as a preferred material in modern architectural coatings.

NIR-Reflective Iron Oxide Pigments Enabling High-Efficiency Cool Roof Systems

The increasing adoption of cool roof technologies, driven by LEED v5 and urban heat island mitigation policies, is creating significant demand for near-infrared (NIR) reflecting iron oxide pigments. These advanced pigments enable dark-colored coatings to achieve high solar reflectance, overcoming the traditional trade-off between aesthetics and thermal performance.

Conventional dark iron oxide pigments typically exhibit total solar reflectance values of 5% to 8%, leading to high heat absorption. In contrast, NIR-optimized pigments can achieve reflectance levels between 60% and 75% while maintaining the same visible color profile. This capability allows architects and designers to use darker shades without compromising energy efficiency or regulatory compliance.

The performance benefits are measurable. Cool roof coatings incorporating NIR-reflective pigments can reduce roof surface temperatures by up to 15°C, resulting in a 10% to 15% reduction in building cooling energy demand. Additionally, by minimizing thermal stress on the coating system, these pigments extend the lifespan of the binder by up to 30%, delaying degradation and reducing long-term maintenance requirements.

Regulatory drivers are reinforcing this trend. More than 30 major cities worldwide now mandate minimum Solar Reflectance Index values for commercial roofing applications, making NIR-reflective pigments an essential component in compliant coating formulations. This convergence of regulatory requirements, energy efficiency goals, and aesthetic flexibility is positioning NIR iron oxide pigments as a high-growth segment within the architectural coatings market.

Ultrafine Transparent Iron Oxides Advancing Wood Protection and Aesthetic Coatings

The demand for natural aesthetic finishes in architectural design is driving the adoption of ultrafine transparent iron oxide pigments in wood coatings. These pigments, characterized by particle sizes below 0.1 micrometers, offer a unique combination of UV protection and visual transparency, making them ideal for applications where preserving the natural appearance of wood is critical.

Transparent iron oxides provide exceptional UV shielding, blocking up to 99% of ultraviolet radiation while allowing visible light to pass through. This prevents the degradation and “silvering” of wood surfaces, extending the lifespan of architectural timber by up to five years compared to coatings based on organic dyes. This performance is particularly valuable in exterior applications where prolonged UV exposure can significantly impact material integrity and appearance.

Efficiency in formulation is another advantage. Due to their high tinting strength, transparent iron oxides achieve desired color intensity at 30% to 40% lower loading levels than conventional opaque pigments. This reduces the overall pigment content in the formulation, preserving coating viscosity and enhancing breathability—key factors in high-performance wood protection systems.

Durability testing further underscores their value. In accelerated weathering conditions, coatings formulated with transparent iron oxides show negligible color fading even after extended UV exposure, significantly outperforming organic pigment systems. Additionally, their compatibility with waterborne resin systems supports the industry’s transition toward low-VOC coatings, reducing the need for solvent-based dispersants.

Architectural Paint Oxide Market Share and Segmentation Insights

Market Share by Oxide Type: Titanium Dioxide (TiO₂) Commands 68% Share Driven by Opacity and High Loading Rates

Titanium Dioxide (TiO₂) overwhelmingly dominates the architectural paint oxide market with a 68% market share in 2025, reflecting its irreplaceable role as the primary white pigment in both interior and exterior coatings. Its superior refractive index delivers unmatched opacity (hiding power) and brightness, making it the foundational component in architectural formulations where coverage efficiency and visual uniformity are critical performance parameters. More than half of global TiO₂ consumption is attributed to paints and coatings, underscoring its centrality in the broader coatings value chain. From a formulation standpoint, TiO₂ functions as a volume driver due to its high loading levels, typically comprising 15 to 25% of total paint solids in latex and alkyd systems. This high inclusion rate, combined with its essential functional properties, ensures that TiO₂ maintains a structurally dominant position in the architectural oxide market. While iron oxides, zinc oxide, mixed metal oxides, and chromium oxide green serve specialized roles in pigmentation, corrosion resistance, and color stability, none approach the scale or functional indispensability of TiO₂ in architectural coatings.

Market Share by End-Use Application: Exterior Coatings Lead with 45% Share Supported by High Exposure and Repaint Cycles

Exterior coatings represent the largest end-use application segment in the architectural paint oxide market, capturing 45% of total demand in 2025. This segment’s leadership is driven by the stringent performance requirements associated with outdoor exposure, including UV resistance, weatherability, color retention, and chalk resistance over extended service lifecycles. As a result, exterior formulations require higher pigment loading, particularly of TiO₂ for opacity and brightness, and iron oxides for durable color pigmentation and UV stability. Additionally, the volume consumption of oxides in exterior applications is significantly amplified by the larger surface area of building exteriors, infrastructure assets, and industrial structures compared to interior spaces. Frequent repaint cycles, typically ranging from 5 to 10 years depending on climatic conditions and substrate type, further accelerate oxide demand in this segment. Growth is also reinforced by ongoing investments in residential housing, commercial construction, and infrastructure refurbishment globally, positioning exterior coatings as the primary consumption engine for architectural paint oxides.

Architectural Paint Oxide Market Competitive Landscape Driven by High-Performance Pigments and Sustainable Color Technologies

The architectural paint oxide market is driven by synthetic iron oxide pigments, high-chroma colorants, and pre-dispersed pigment systems. Leading players are focusing on low-VOC compatibility, UV stability, and sustainable pigment production to enhance color performance, durability, and regulatory compliance in architectural coatings and construction applications.

LANXESS leads architectural paint oxides with high-performance Bayferrox pigments and sustainable production

LANXESS dominates the architectural paint oxide market through its Bayferrox® portfolio of synthetic iron oxide pigments. The company introduced Bayferrox 130 in 2026, featuring enhanced dispersibility in low-VOC coatings and compliance with ISO 16128 sustainability standards. A 25,000 metric ton capacity expansion at its Brazil facility supports rising demand in Latin America’s architectural coatings sector. Its pigments are widely used in exterior coatings due to superior lightfastness and thermal stability. Investment in zero-liquid-discharge technologies aligns production with EU Green Deal requirements. Product development focuses on high-durability pigments and environmentally compliant manufacturing.

Cathay Industries expands high-chroma iron oxide pigments with VOC-free formulation advantages

Cathay Industries is strengthening its position in architectural paint oxides through high-chroma pigment innovation and global capacity expansion. The company commissioned a 25,000 metric ton production line in China in 2025, increasing global output by 12%. Its CATHAYCOAT Red RA11A pigment enables vibrant color performance in VOC-free coatings while reducing grinding time and processing costs. Advanced high-chroma technology allows manufacturers to achieve organic-like color intensity with inorganic durability. A major supply agreement for the NEOM project highlights its growing role in large-scale infrastructure coatings. Product development focuses on cost efficiency and color performance.

BASF integrates iron oxide pigments with advanced coating systems and nano-enhanced technologies

BASF leverages its chemical integration capabilities to provide advanced iron oxide pigment solutions for architectural coatings. The Sicopal product line includes pre-dispersed pigments optimized for water-based coatings, enabling improved color development with lower pigment loading. Increased R&D investment in 2025 supports development of nano-enhanced pigments with UV protection and self-cleaning properties. BASF’s integrated approach combines pigments, resins, and additives into complete coating systems for improved formulation efficiency. Sustainably advantaged products account for over 40% of its coatings segment sales. Product development focuses on performance optimization and sustainability.

Venator strengthens architectural oxide pigments with solar reflective and high-opacity technologies

Venator Materials focuses on high-opacity pigment systems, combining titanium dioxide with iron oxide pigments for architectural coatings. Its portfolio supports solar reflective coatings that meet cool roof standards, particularly in Asia-Pacific and Middle Eastern markets. The company has implemented energy recovery and waste acid recycling systems to improve production efficiency and reduce environmental impact. Micronized iron oxides provide consistent particle size, improving finish quality in high-gloss architectural coatings. Its integrated pigment offerings support a significant share of the high-performance pigment market. Product development focuses on energy efficiency and optical performance.

Heubach Group expands global pigment portfolio with micronized oxides and APAC-focused growth

Heubach Group is a major player in architectural paint oxides following its acquisition of Clariant’s pigments business. The company operates a globally diversified supply network with strong focus on high-growth APAC markets. Its micronized and transparent iron oxides are widely used in wood coatings and decorative finishes, providing UV protection while maintaining natural aesthetics. Expansion of production capacity in India supports rising demand from the construction sector, which is growing at 8–10% annually. The shift toward synthetic pigments reflects demand for consistency and purity in architectural coatings. Product development focuses on high-performance pigments and regional market expansion.

China Architectural Paint Oxide Market: Regulatory Overhaul and Photocatalytic Pigment Innovation Driving Global Leadership

China continues to dominate the architectural paint oxide market as the world’s largest production hub for synthetic iron oxide pigments, now undergoing a significant regulatory transformation to enhance environmental purity. The implementation of GB 30981.1-2025 standards (effective June 2026) is tightening restrictions on heavy metals and aromatic compounds, forcing manufacturers to upgrade legacy production systems and adopt cleaner pigment technologies. This regulatory shift is accelerating innovation in eco-friendly architectural oxide pigments and reinforcing China’s global leadership.

Technological advancements are further strengthening market growth. The expansion of chloride-process titanium dioxide (TiO₂) capacity to 1.5 million tons by LB Group is enabling the production of premium-grade pigments with superior dispersion and durability. Demand is also surging from urban renewal initiatives, particularly the “Old Community Renovation” programs, which are driving adoption of self-cleaning photocatalytic oxides. Breakthroughs in nano-titania pigments capable of neutralizing NOx emissions are transforming architectural coatings in smog-prone cities. Additionally, innovations such as infrared-reflective oxide pigments for high-speed rail infrastructure and sustainability incentives for closed-loop manufacturing systems are positioning China at the forefront of advanced architectural pigment technologies.

United States Architectural Paint Oxide Market: PFAS-Free Coating Transition and High-Durability Pigment Demand

The United States architectural paint oxide market is evolving rapidly, driven by regulatory mandates and innovation in high-performance coatings. Following EPA directives, the industry has transitioned toward PFAS-free architectural coatings, significantly influencing the selection of surface-treated oxide pigments and additives. This shift is creating strong demand for sustainable and non-toxic oxide formulations, particularly in residential and commercial applications.

Innovation remains a key differentiator in the U.S. market. The introduction of microbicidal oxide-based coatings, such as advanced variants of antimicrobial paints, is enhancing indoor hygiene for high-touch surfaces. The adoption of cool-roof oxide pigments with Solar Reflectance Index (SRI >110) is expanding across the Sun Belt, improving energy efficiency in urban infrastructure. Investments by companies such as Venator and Chemours are stabilizing domestic TiO₂ supply chains, ensuring resilience amid global price volatility. Additionally, increasing use of anti-mildew zinc oxide additives in coastal coatings and federal support for AI-driven color-matching technologies are strengthening the U.S. position in high-performance architectural oxide markets.

India Architectural Paint Oxide Market: Capacity Expansion and Infrastructure Boom Driving High-Performance Pigment Demand

India is emerging as one of the fastest-growing markets in the architectural paint oxide industry, supported by massive infrastructure investments and rapid capacity expansion. The launch of Birla Opus with 1.3 billion liters of capacity has significantly increased demand for high-tinting-strength iron oxide pigments, reshaping the domestic supply landscape.

Government initiatives such as the City Economic Regions (CER) program are creating a strong pipeline for weather-resistant oxide coatings across Tier-2 and Tier-3 cities. Infrastructure projects, including freight corridors and maritime developments, are driving mandatory adoption of anti-corrosive oxide pigments for long-term durability. Regulatory updates under FSSAI are also increasing demand for low-migration pigments in food and pharmaceutical facility coatings. Additionally, advancements such as water-dispersible oxide pastes are improving ease of application for small-scale contractors, while backward integration by major players is strengthening domestic production capabilities. These factors position India as a high-growth hub for architectural paint oxides.

Germany Architectural Paint Oxide Market: Carbon-Negative Pigments and Green Chemistry Leadership

Germany sets the global benchmark in sustainable architectural paint oxide technologies, driven by strict environmental regulations and advanced material innovation. The development of carbon-sequestering mineral paints infused with recycled oxides is aligning with Net-Zero construction targets, enabling coatings that actively absorb CO₂ during curing.

The market is also characterized by strong adoption of water-borne oxide technologies, supported by the Decopaint Directive, which has pushed these solutions to dominate the architectural coatings sector. Demand for UV-stable iron oxide pigments is increasing in prefabricated housing and metal cladding applications, driven by Germany’s focus on energy-efficient construction. Additionally, compliance with VDI 6022 standards is driving the use of antimicrobial oxide additives in HVAC systems. Government incentives under renovation programs are further boosting demand for high-reflectivity oxide coatings, reinforcing Germany’s leadership in eco-friendly and high-performance architectural pigments.

Saudi Arabia Architectural Paint Oxide Market: Extreme Climate Coatings and Mega-Project Demand Driving Growth

Saudi Arabia is emerging as a critical market for architectural paint oxides, driven by Vision 2030 and large-scale infrastructure projects. Mega-developments such as NEOM and The Line are generating strong demand for high-SRI titanium dioxide pigments, designed to withstand extreme desert temperatures exceeding 50°C.

The market is also shaped by regulatory and technological advancements. New fire safety mandates are driving the use of intumescent oxide additives in commercial buildings, while infrastructure projects such as the Riyadh Metro are increasing demand for anti-carbonation oxide coatings. Innovations such as temperature-responsive color-changing pigments are being integrated into smart city developments, enhancing building performance monitoring. Additionally, the shift toward solvent-free powder-based oxide coatings is supporting sustainability goals, positioning Saudi Arabia as a key hub for advanced architectural coatings in extreme environments.

Japan Architectural Paint Oxide Market: Nanotechnology Precision and Antiviral Pigment Innovation

Japan’s architectural paint oxide market is defined by its leadership in nanoscale pigment technology and advanced functional coatings. The integration of AI-driven formulation platforms, developed through collaborations between industry and academia, is optimizing oxide dispersion for next-generation zero-emission coatings.

Technological innovation is expanding applications across multiple sectors. Japan leads in visible-light-activated antiviral oxide pigments, widely used in public infrastructure and healthcare facilities. The development of high-elongation oxide coatings is improving seismic resilience by maintaining color integrity during structural movement. Additionally, innovations such as ultra-matte oxide finishes and super-hydrophilic self-cleaning coatings are enhancing both aesthetics and maintenance efficiency. Advanced logistics solutions, including vacuum-sealed dispersions, are further improving pigment stability, reinforcing Japan’s leadership in precision architectural oxide technologies.

Brazil Architectural Paint Oxide Market: Mineral Resource Advantage and Bio-Based Pigment Innovation Driving Regional Growth

Brazil is leveraging its abundant natural resources to establish a strong position in the architectural paint oxide market. The country’s dominance in iron ore production is enabling cost-effective manufacturing of high-quality iron oxide pigments, giving domestic producers a competitive advantage across South America.

Infrastructure and social housing programs are key growth drivers, generating strong demand for affordable, high-coverage oxide pigments. Regulatory changes under Mercosur are accelerating the shift toward water-borne oxide stabilizers, supporting sustainability initiatives. The agricultural sector is also contributing to demand, particularly for zinc-rich protective oxides used in storage and processing facilities. Additionally, innovations such as sugarcane-derived bio-based pigment carriers and partnerships with mining companies to refine tailing oxides into high-purity pigments are strengthening Brazil’s role as a leader in sustainable and cost-efficient architectural pigment solutions.

Architectural Paint Oxide Market Report Scope

Architectural Paint Oxide Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$88.6 Million

|

|

Market Size (2032)

|

$134.1 Million

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Oxide (Titanium Dioxide (TiO2), Iron Oxide, Chromium Oxide Green, Zinc Oxide (ZnO), Mixed Metal Oxides), By Source (Synthetic Oxides, Natural Oxides), By Product Form (Dry Powder, Granular, Liquid Dispersions), By Technology Compatibility (Water-borne Compatible, Solvent-borne Compatible, Powder Coating Grade), By End-Use Application (Exterior Coatings, Interior Coatings, Wood Stains and Preservatives, Decorative Concrete and Floor Coatings), By Performance Grade (Standard Grade, High-Opacity, Heat-Stable, Nanoscale Oxides)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

LANXESS AG, BASF SE, Venator Materials PLC, Cathay Industries, Heubach Group, Lomon Billions Group, Tronox Holdings plc, The Chemours Company, Ferro Corporation, Hunan Three-Ring Pigments Co., Ltd., Yipin Pigments, Kronos Worldwide, Inc., Applied Minerals Inc., Titanos Group, Precheza a.s.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Architectural Paint Oxide Market Segmentation

By Oxide

- Titanium Dioxide (TiO2)

- Iron Oxide

- Chromium Oxide Green

- Zinc Oxide (ZnO)

- Mixed Metal Oxides

By Source

- Synthetic Oxides

- Natural Oxides

By Product Form

- Dry Powder

- Granular

- Liquid Dispersions

By Technology Compatibility

- Water-borne Compatible

- Solvent-borne Compatible

- Powder Coating Grade

By End-Use Application

- Exterior Coatings

- Interior Coatings

- Wood Stains and Preservatives

- Decorative Concrete and Floor Coatings

By Performance Grade

- Standard Grade

- High-Opacity

- Heat-Stable

- Nanoscale Oxides

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Architectural Paint Oxide Market

- LANXESS AG

- BASF SE

- Venator Materials PLC

- Cathay Industries

- Heubach Group

- Lomon Billions Group

- Tronox Holdings plc

- The Chemours Company

- Ferro Corporation

- Hunan Three-Ring Pigments Co., Ltd.

- Yipin Pigments

- Kronos Worldwide, Inc.

- Applied Minerals Inc.

- Titanos Group

- Precheza a.s.

*- List not Exhaustive

Table of Contents: Architectural Paint Oxide Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Architectural Paint Oxide Market Landscape & Outlook (2025–2032)

2.1. Introduction to Architectural Paint Oxide Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Market Drivers: UV Stability, Durability, and Color Performance in Construction Materials

2.4. Raw Material Dynamics: Energy Costs, Supply Chain Volatility, and Pigment Pricing Trends

2.5. Sustainability Transition: Low-Carbon Pigments, Circular Economy, and Green Building Compliance

3. Innovations Reshaping the Architectural Paint Oxide Market

3.1. Trend: Synthetic Iron Oxides from Industrial Waste and Circular Pigment Production

3.2. Trend: NIR-Reflective and Photocatalytic Oxide Pigments for Energy Efficiency

3.3. Opportunity: Ultrafine Transparent Iron Oxides for Wood Protection and Aesthetic Coatings

3.4. Opportunity: Bio-Based and Non-Nano Silica Alternatives for Safer Formulations

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Pigment Chemistry Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Capacity Optimization

5. Market Share and Segmentation Insights: Architectural Paint Oxide Market

5.1. By Oxide

5.1.1. Titanium Dioxide (TiO₂)

5.1.2. Iron Oxide

5.1.3. Chromium Oxide Green

5.1.4. Zinc Oxide (ZnO)

5.1.5. Mixed Metal Oxides

5.2. By Source

5.2.1. Synthetic Oxides

5.2.2. Natural Oxides

5.3. By Product Form

5.3.1. Dry Powder

5.3.2. Granular

5.3.3. Liquid Dispersions

5.4. By Technology Compatibility

5.4.1. Water-borne Compatible

5.4.2. Solvent-borne Compatible

5.4.3. Powder Coating Grade

5.5. By End-Use Application

5.5.1. Exterior Coatings

5.5.2. Interior Coatings

5.5.3. Wood Stains and Preservatives

5.5.4. Decorative Concrete and Floor Coatings

5.6. By Performance Grade

5.6.1. Standard Grade

5.6.2. High-Opacity

5.6.3. Heat-Stable

5.6.4. Nanoscale Oxides

6. Country Analysis and Outlook of Architectural Paint Oxide Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Architectural Paint Oxide Market Size Outlook by Region (2025–2032)

7.1. North America Architectural Paint Oxide Market Size Outlook to 2032

7.1.1. By Oxide

7.1.2. By Source

7.1.3. By Product Form

7.1.4. By Technology Compatibility

7.1.5. By End-Use Application

7.1.6. By Performance Grade

7.2. Europe Architectural Paint Oxide Market Size Outlook to 2032

7.2.1. By Oxide

7.2.2. By Source

7.2.3. By Product Form

7.2.4. By Technology Compatibility

7.2.5. By End-Use Application

7.2.6. By Performance Grade

7.3. Asia Pacific Architectural Paint Oxide Market Size Outlook to 2032

7.3.1. By Oxide

7.3.2. By Source

7.3.3. By Product Form

7.3.4. By Technology Compatibility

7.3.5. By End-Use Application

7.3.6. By Performance Grade

7.4. South America Architectural Paint Oxide Market Size Outlook to 2032

7.4.1. By Oxide

7.4.2. By Source

7.4.3. By Product Form

7.4.4. By Technology Compatibility

7.4.5. By End-Use Application

7.4.6. By Performance Grade

7.5. Middle East and Africa Architectural Paint Oxide Market Size Outlook to 2032

7.5.1. By Oxide

7.5.2. By Source

7.5.3. By Product Form

7.5.4. By Technology Compatibility

7.5.5. By End-Use Application

7.5.6. By Performance Grade

8. Company Profiles: Leading Players in the Architectural Paint Oxide Market

8.1. LANXESS AG

8.2. BASF SE

8.3. Venator Materials PLC

8.4. Cathay Industries

8.5. Heubach Group

8.6. Lomon Billions Group

8.7. Tronox Holdings plc

8.8. The Chemours Company

8.9. Ferro Corporation

8.10. Hunan Three-Ring Pigments Co., Ltd.

8.11. Yipin Pigments

8.12. Kronos Worldwide, Inc.

8.13. Applied Minerals Inc.

8.14. Titanos Group

8.15. Precheza a.s.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures