Australia Water Treatment Chemicals Market: Value Analysis, Growth Trends, and Forecast to 2034

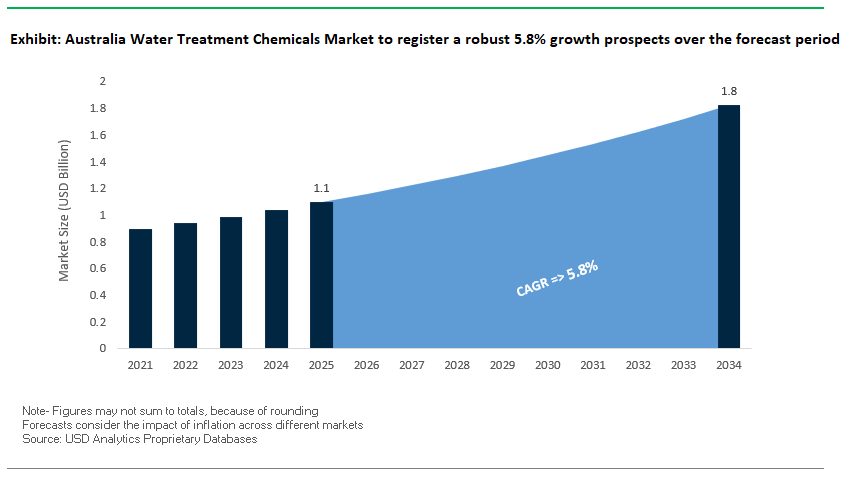

Australia Water Treatment Chemicals Market Size is estimated at $1.1 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 5.8% to reach $1.8 Billion by 2034.

Australia’s water treatment chemicals market is evolving rapidly, shaped by climate-induced hydrological variability, regulatory modernization, and growing adoption of sustainable and smart water technologies. The sector spans diverse end-uses including municipal drinking water, industrial and mining effluents, seawater desalination, and recycled water reuse each demanding specialized chemical approaches tailored to Australia’s distinct environmental and policy contexts. Increasing drought risk, salinity issues, and emerging contaminants like PFAS are driving both innovation and regulatory scrutiny, especially in sectors where water recycling, nutrient recovery, and advanced purification are becoming essential to long-term resource resilience.

- Drinking Water Treatment- Municipal water utilities across Australia rely heavily on coagulants and flocculants to meet stringent health-based performance targets set under the Australian Drinking Water Guidelines (ADWG, 2023). Aluminum-based coagulants especially polyaluminum chloride (PACl) remain standard, typically dosed at 5–25 mg/L to reduce turbidity and remove organic matter. Filtration systems aim to maintain turbidity below 0.2 NTU post-treatment, particularly to protect against chlorine-resistant pathogens like Cryptosporidium and Giardia. Variability in raw water quality due to extreme weather events, including bushfires and floods, necessitates adaptive chemical dosing and rapid-response treatment strategies. Optimizing chemical use in such events is increasingly supported by online turbidity and organics monitoring tools.

- Mining and Industrial Wastewater Management- Australia’s mining-intensive states Western Australia, Queensland, and New South Wales present complex water treatment challenges, especially in acid mine drainage (AMD) management. Common practices include pH adjustment using lime or caustic soda to precipitate heavy metals such as iron, aluminum, and manganese. Sludge generation in these processes is substantial, requiring effective dewatering, stabilization, and disposal strategies compliant with state EPA guidelines. High total dissolved solids (TDS) in mine water also call for antiscalants, dispersants, and proprietary complexing agents to manage scale formation in closed-loop systems and water reuse circuits. Regulatory agencies like the Department of Climate Change, Energy, the Environment and Water (DCCEEW) enforce water reuse targets and discharge controls in high-risk catchments.

- Wastewater Reuse and Nutrient Recovery- Australia is a global leader in municipal wastewater reuse, especially in arid and peri-urban zones. Utilities such as SA Water and Melbourne Water are piloting advanced nutrient recovery systems. Phosphorus recovery via struvite (magnesium ammonium phosphate) crystallization is gaining traction in sludge handling operations, contributing to fertilizer production. However, adoption remains limited by cost challenges compared to conventional phosphate fertilizers. For nitrogen removal, advanced biological processes including partial nitritation-anammox (PNA) are operational in selected treatment plants, delivering energy savings and greenhouse gas reductions. Class A+ recycled water used for irrigation and industrial cooling is typically treated using microfiltration, reverse osmosis, and UV/H₂O₂ advanced oxidation processes (AOPs) to meet strict thresholds for total organic carbon (<0.5 mg/L) and microbial safety, under frameworks such as the Water Supply (Safety and Reliability) Act 2008 (Qld).

- PFAS Remediation and Emerging Contaminants- PFAS remediation remains a priority, particularly at defense, aviation, and industrial sites. National guidance is set by the PFAS National Environmental Management Plan (NEMP), developed by the Heads of EPAs (HEPA). Technologies in use include granular activated carbon (GAC), strong-base anion exchange resins, and advanced sorbents like ion-imprinted polymers. While some pilot systems use regenerable resins with solvent-based elution, most large-scale applications are currently designed for single-use media due to safety and handling concerns. State-based regulatory frameworks are converging toward uniform criteria for PFOS, PFOA, and PFHxS in discharged waters and biosolids, affecting chemical selection and system design in remediation projects.

- Green Chemistry in Public Infrastructure- Australia’s commitment to sustainable procurement is influencing chemical selection in water treatment projects. Natural coagulants derived from renewable sources such as tannin-based formulations developed in collaboration with CRC CARE are under evaluation for use in decentralized and eco-sensitive treatment systems. These biodegradable alternatives to alum and PACl have shown promise in regional applications where low-salinity raw water and low sludge volumes are prioritized. However, scalability and cost remain key constraints. Government procurement frameworks, including the Australian Government Sustainable Procurement Guidelines, are encouraging lifecycle-based selection of green chemicals for public water assets.

- Smart Dosing and Digital Optimization- With rising chemical costs and growing water reuse mandates, utilities and industries in Australia are investing in intelligent dosing systems. These platforms integrate real-time monitoring of turbidity, pH, residual disinfectants, and organics (e.g., UV254 or TOC) with AI-based control algorithms to minimize chemical consumption while maintaining compliance. Such systems are particularly valuable in variable-source applications, including desalination pre-treatment and stormwater harvesting, where source quality can change rapidly. Companies like Hydroflow and DMI Australia are providing modular systems with telemetry for remote and centralized facilities, supporting data-driven chemical management and reducing sludge volumes and operational costs.

Market Trend: Mining Expansion and ESG Pressures Transform Industrial Water Chemistry in Australia

Australia’s water treatment chemicals market is being reshaped by the convergence of mining sector growth, tightening environmental regulation, and rising ESG expectations. As the world’s top producer of lithium and a major exporter of iron ore, copper, and critical minerals, Australia’s mining industry accounts for the largest share of industrial water chemical usage particularly in water-intensive regions like Western Australia and Queensland. The treatment challenges are intensifying due to declining ore grades and higher impurity loads, such as elevated silica concentrations in Pilbara iron ore, which demand more advanced scale inhibitors and anti-fouling strategies.

Regulatory frameworks are evolving accordingly. The Western Australia Department of Water and Environmental Regulation (DWER) has revised environmental discharge licenses for total dissolved solids (TDS), with stricter site-specific salinity thresholds now enforced in key catchments. These changes have elevated compliance costs, and violations can result in substantial penalties and reputational damage. Additionally, reforms to the Modern Slavery Act 2018 proposed in 2023 and under stakeholder review highlight chemical supply chain risks, particularly around hazardous substances such as cyanide and PFAS, and are prompting broader audits of chemical sourcing and stewardship.

Major mining operators, including BHP and Rio Tinto, are responding by trialing lower-toxicity alternatives and process-integrated solutions to reduce chemical load. For instance, studies by the Commonwealth Scientific and Industrial Research Organisation (CSIRO) have explored electrochemical treatments and membrane-compatible antiscalants for metal recovery circuits, contributing to chemical savings and water recycling improvements. The shift is further reinforced by capital markets: according to the Australasian Centre for Corporate Responsibility (ACCR), water-related shareholder resolutions and investor queries are rising across ASX-listed miners, positioning responsible water management as a key ESG differentiator. Collectively, these forces are elevating water treatment chemistry from an operational necessity to a strategic function directly tied to social license, decarbonization targets, and access to global investment.

Market Opportunity: Seawater Desalination Chemicals Surge with National Infrastructure Push

Australia’s growing vulnerability to drought and water scarcity is driving significant investment in seawater desalination, creating a strong growth opportunity for reverse osmosis (RO)-compatible treatment chemicals. With more than A$12 billion in new and planned desalination infrastructure covering municipal supply, hydrogen production, and industrial operations the market for SWRO-specific antiscalants, membrane cleaners, pH conditioners, and biofouling controls is projected to expand rapidly. Australia’s conditions are uniquely challenging: variable feedwater characteristics across coastal intakes require chemical programs to be highly site-specific. For example, desalination plants in South Australia and Victoria contend with seasonal spikes in natural organic matter and algae, while Northern Queensland systems may face higher boron or silica loads.

Public utilities and industrial operators are increasingly specifying PFAS-free and low-byproduct formulations in alignment with updated drinking water regulations. For instance, Western Australia’s 2024 Drinking Water Quality Guideline revisions align with national standards by setting stricter limits for residual contaminants in treated water, influencing procurement of compatible chemical formulations. Desalination’s role in supporting the energy transition is also expanding. Projects like the Hydrogen Jobs Plan in South Australia and the Western Green Energy Hub incorporate large-scale desalination to supply ultra-pure process water for electrolysis, intensifying demand for RO-compatible chemistries that minimize membrane fouling and preserve system performance.

Chemical suppliers are adapting to these trends with multi-functional products and digital integration. Modular antiscalant blends with enhanced silica and sulfate tolerance are now standard, and condition-specific oxidant neutralizers are used to protect polyamide membranes. Companies such as Veolia, SUEZ, and Kurita have introduced AI-assisted platforms that optimize chemical dosing through predictive analytics. For example, the Victorian Desalination Plant leverages sensor-based monitoring systems to fine-tune chemical inputs, reducing operational costs and extending membrane lifespan. In parallel, there is growing interest in locally adapted solutions. Several collaborative efforts with Indigenous communities and research centers (e.g., through CRC CARE and regional partnerships) are exploring the potential of bio-derived antifouling agents and sustainable coagulants tailored for Australia’s ecosystems.

This convergence of national water security planning, clean energy policy, and innovation in sustainable chemistries positions Australia not only as a key domestic market for desalination chemicals but also as a center of expertise for export-oriented solutions particularly as countries across the Indo-Pacific region invest in similar infrastructure for resilience and decarbonization.

Competitive Landscape: Australia Water Treatment Chemicals Market

The competitive landscape of Australia’s water treatment chemicals market is influenced by a mix of global companies, local innovators, and established regional players, each using different strategies for industrial, municipal, and remote applications. This market is shaped not just by pricing, but also by the inclusion of valuable services, logistical capabilities, and sustainability standards. As demand becomes more specific and environmental, social, and governance (ESG) requirements increase, vendors are adjusting their strategies through technology, bio-based innovations, and mergers and acquisitions to maintain or grow their market share.

Deep Client Integration and Value-Added Services as Differentiators

One significant strategy in the Australian market is the incorporation of technical services into customer operations. Some multinational companies have moved beyond just selling products. They now place on-site engineers and water treatment experts directly at client facilities, from city utilities to remote mining sites. This approach creates long-term partnerships and changes the buyer-supplier dynamic to focus on solutions. Real-time chemical control systems, particularly those showing clear returns on investment in water or energy savings, are key for justifying higher prices. However, this comprehensive approach faces challenges in cost-sensitive areas where local companies provide simpler, adequate solutions at a lower total cost.

Local Manufacturing and Distribution Infrastructure: A Critical Competitive Moat

Local manufacturing capabilities provide a strategic edge, especially for coagulants and flocculants in large-volume municipal applications. Companies with factories in Queensland and Victoria enjoy better supply chain resilience, faster response times during peak demands, and reduced shipping costs factors that are increasingly important in public tenders. It is also crucial to maintain consistent chemical quality and meet Australian regulatory standards. Distribution networks, including remote blending and storage facilities in mining regions, further set market leaders apart from those relying on outside logistics providers. This is particularly important in remote areas rich in resources, like Western Australia and the Northern Territory.

Specialization, Customization, and Agility as Competitive Levers

While large suppliers dominate high-volume contracts and integrated services, specialized companies are finding their place by concentrating on specific problem-solving chemical solutions and being agile. These firms excel where rigid corporate practices or standardized products fail, such as in reducing legionella risk in commercial HVAC systems, treating wastewater in food processing, or using solar desalination for off-grid communities. Their success often comes from quick development, hands-on technical support, and direct engagement with clients, avoiding traditional distribution methods. In fragmented regional markets that lack adequate service, these agile competitors often respond better and adapt more easily than larger firms.

Battlegrounds: Mining, Municipal, and Regulatory Challenges

The mining sector is the most competitive area, with long-term contracts driving intense rivalry. Here, reliability and remote technical support are essential, especially for risky process water treatment. While price is a critical consideration during bidding, trust in performance and consistent service often favors established companies with a proven track record. In the municipal sector, councils are closely monitoring sludge volumes and moving away from traditional metal-based coagulants. This shift creates opportunities for bio-based alternatives and low-residue formulations, intensifying competition among global innovators, large manufacturers, and agile problem-solvers.

Regulatory and Sustainability Pressures Accelerate Market Segmentation

Australia’s regulatory landscape, especially regarding biocide approvals, PFAS phase-outs, and chemical transport regulations, presents considerable challenges for smaller firms, benefiting those with global regulatory knowledge and strong research and development capabilities. Sustainability demands are even rising, though unevenly. Companies mindful of ESG factors and some government agencies are starting to allocate budgets for low-carbon chemicals and biodegradable additives. Firms that can prove their environmental performance, backed by life cycle assessments, carbon management certifications, or circular chemistry claims, are increasingly winning contracts for future-focused projects.

Converging Models: Solutions vs. Commodity Supply

The market is splitting into two strategic models. One segment consists of solution-driven providers offering bundled services that include dosing equipment, real-time monitoring, and predictive maintenance alongside chemical supply. The other segment features modular, chemical-only suppliers who prioritize speed, customization, and price flexibility. Both approaches have potential for success, but traditional chemical-only suppliers are feeling pressure to adjust their offerings or focus more on specialized niches where full-service arrangements are not practical.

Australia Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

By Type of Chemical: Coagulants Lead, Membrane Cleaners Show Strongest Growth

In 2025, coagulants and flocculants are projected to hold the largest share of the Australian water treatment chemicals market at approximately 28.7%, owing to their critical role in turbidity removal and solids separation across both municipal water systems and the country’s extensive mining wastewater operations. PolyDADMAC, alum, and ferric chloride are among the most widely used coagulants in Australia's centralized water treatment infrastructure, particularly in regions with variable raw water quality.

Membrane cleaning chemicals are forecast to exhibit the fastest growth at a CAGR of 7.1%, driven by rapid expansions in reverse osmosis (RO) desalination facilities and rising reuse of brackish and wastewater across drought-prone territories like Western Australia and New South Wales. Biocides and disinfectants, are gaining momentum due to increasingly stringent regulations on Legionella control and biofilm prevention in commercial cooling towers and hospitals. Meanwhile, oxygen scavengers and defoamers support niche industrial systems, and a small share of the market includes specialized chemical blends for niche applications in mining remediation and high-purity water loops.

By Application: Municipal Dominates, Water Reuse Grows Fastest

Municipal water treatment accounts for the largest share at 39.2% of the market in 2025, driven by population growth, regulatory upgrades, and the need for replacing aging distribution and treatment infrastructure. State-level water reform policies, including Australia's National Water Initiative, continue to push for improved chemical dosing efficiency and sludge management at water and sewage utilities. The industrial sector is a major consumer of corrosion inhibitors, scale control agents, and biocides, particularly in mining operations (Queensland, WA), thermal power stations, and food & beverage processing plants. Water-intensive industries are increasingly investing in chemical treatment programs to reduce operational downtime and environmental discharge penalties.

Notably, water reuse and recycling is the fastest-growing segment, projected to expand at a CAGR of 6.8%. As Australia seeks to strengthen its climate resilience, facilities across cities like Perth and Adelaide are investing in advanced treatment technologies for greywater, stormwater, and treated effluent reuse. This surge has boosted demand for membrane anti-scalants, cleaning chemicals, and disinfection agents. Desalination, with an estimated 10% market share, is another high-growth area, particularly as cities like Sydney and Melbourne scale up RO-based plants to ensure potable water availability amid declining reservoir levels. Commercial water treatment, including schools, hotels, and healthcare facilities, accounts for the remaining 12%, with growing emphasis on Legionella prevention and HVAC water loop management.

.png)

Australia Water Treatment Chemicals Report Scope

Australia Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2034)

|

$1.8 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, pH Adjusters and Softeners, Oxygen Scavengers, Defoamers and Antifoaming Agents, Membrane Cleaning Chemicals, Others), By Application (Municipal Water Treatment, Industrial Water Treatment, Commercial Water Treatment, Water Desalination, Water Reuse and Recycling), By Form of Chemical (Liquid, Powder/Solid), By Distribution Channel (Direct Sales, Distributors/Channel Partners, Online Sales

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Kurita Water Industries Ltd. (Japan), Solenis LLC (U.S.), BASF SE (Germany), Kemira Oyj (Finland), Ion Exchange (India) Ltd. (India), Veolia Water Technologies (France), IXOM (Australia), MAK Water (Australia), BioChem Water (Australia), Filchem Australia (Australia), SWA Water Australia (Australia), Buckman (U.S.), Accepta Ltd. (UK),

|

Australia Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Corrosion and Scale Inhibitors

- Biocides and Disinfectants

- pH Adjusters and Softeners

- Oxygen Scavengers

- Defoamers and Antifoaming Agents

- Membrane Cleaning Chemicals

- Others

By Application

- Municipal Water Treatment

- Drinking Water Treatment

- Municipal Wastewater Treatment

- Industrial Water Treatment

- Power Generation

- Mining and Metallurgy

- Oil and Gas

- Food and Beverage

- Chemical and Petrochemical

- Pulp and Paper

- Pharmaceutical

- Electronics and Semiconductors

- Other Manufacturing Industries

- Commercial Water Treatment

- Water Desalination

- Water Reuse and Recycling

By Form of Chemical

By Distribution Channel

- Direct Sales

- Distributors/Channel Partners

- Online Sales

Top Companies in Australia Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Kurita Water Industries Ltd. (Japan)

- Solenis LLC (U.S.)

- BASF SE (Germany)

- Kemira Oyj (Finland)

- Ion Exchange (India) Ltd. (India)

- Veolia Water Technologies (France)

- IXOM (Australia)

- MAK Water (Australia)

- BioChem Water (Australia)

- Filchem Australia (Australia)

- SWA Water Australia (Australia)

- Buckman (U.S.)

- Accepta Ltd. (UK)

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the dynamic evolution of the Australia Water Treatment Chemicals Market, delivering detailed analysis reviews and highlighting emerging opportunities across municipal, industrial, and desalination segments. It covers breakthroughs in green chemistry, PFAS remediation strategies, and AI-driven dosing optimization, ensuring readers gain a competitive edge in a sustainability-driven market. This report is an essential resource for decision-makers, consultants, and investors seeking actionable intelligence on regulatory shifts, advanced chemical formulations, and ESG-aligned procurement strategies.

Scope Includes:

- Segmentation By Type of Chemical: Coagulants & Flocculants, Corrosion & Scale Inhibitors, Biocides & Disinfectants, pH Adjusters & Softeners, Oxygen Scavengers, Defoamers & Antifoaming Agents, Membrane Cleaning Chemicals, Others

- Segmentation By Application: Municipal Water Treatment (Drinking Water, Wastewater), Industrial Water Treatment (Power, Mining, Oil & Gas, Food & Beverage, Chemical & Petrochemical, Pulp & Paper, Pharmaceutical, Electronics), Commercial Water, Water Desalination, Water Reuse & Recycling

- Segmentation By Form of Chemical: Liquid, Powder/Solid

- Segmentation By Distribution Channel: Direct Sales, Distributors/Channel Partners, Online Sales

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Companies: Ecolab Inc., Kurita Water Industries, Solenis, BASF SE, Kemira Oyj, Ion Exchange, Veolia Water Technologies, IXOM, MAK Water, BioChem Water, Filchem Australia, SWA Water Australia, Buckman, Accepta Ltd.

Methodology

The study applies a bottom-up market modeling approach, integrating primary interviews with utility operators, industrial plant managers, and chemical suppliers across Australia. Secondary research includes regulatory frameworks (ADWG, PFAS NEMP), desalination project databases, and procurement policies. Data triangulation combines chemical dosage norms, treatment capacity expansions, and historical pricing trends to validate forecasts. Forecast models incorporate macro drivers like climate-driven water security initiatives, circular economy strategies, and adoption of digital dosing platforms to ensure accurate, future-ready insights.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements