Automotive Coatings Market Size and Growth Driven by EV Expansion and Advanced Surface Technologies

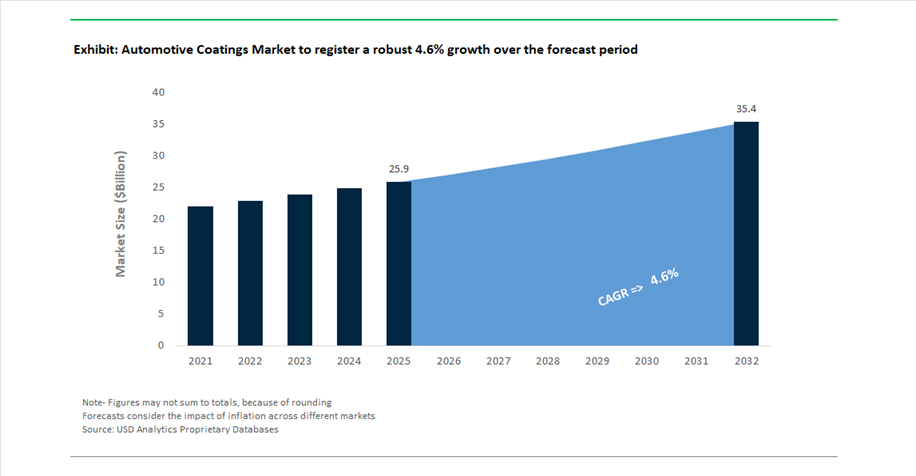

The Automotive Coatings Market is projected to grow from USD 25.9 billion in 2025 to USD 35.5 billion by 2032, registering a CAGR of 4.6%. This growth is driven by the evolution of vehicle design, increasing electric vehicle (EV) adoption, and rising demand for high-performance, durable, and aesthetically advanced coatings across OEM and refinish segments.

Automotive coatings are critical for providing corrosion protection, UV resistance, scratch durability, and visual appeal, while also supporting vehicle lightweighting and energy efficiency goals. With the rapid rise of EVs, coatings are being specifically engineered for battery housings, lightweight composites, and advanced substrates, requiring enhanced thermal stability and electrical insulation properties. At the same time, OEMs are increasingly focusing on premium finishes, color innovation, and surface functionality, driving demand for coatings that combine aesthetic sophistication with functional performance.

Technological advancements are reshaping the market, particularly through the development of smart coatings with self-healing capabilities, anti-scratch performance, and radar transparency for autonomous driving systems. Additionally, the shift toward low-VOC, waterborne, and sustainable coating technologies is accelerating, driven by stringent environmental regulations and the automotive industry’s commitment to reducing carbon emissions. The refinish segment is also evolving, with increasing demand for fast-curing, high-efficiency coatings that reduce repair cycle times and improve productivity in body shops.

The market is further supported by global automotive production recovery, expansion of mobility solutions, and increasing customization trends, particularly in emerging economies. Competitive dynamics are characterized by intensive R&D investment, digitalization of application processes, and strategic consolidation, positioning automotive coatings as a key enabler of next-generation mobility and vehicle performance

Digitalization, Strategic M&A, and Next-Generation Coating Technologies Transforming Market Dynamics

The automotive coatings market is undergoing a structural transformation driven by technological innovation, digital integration, and large-scale industry consolidation. Product innovation is heavily focused on efficiency and performance optimization. In March 2026, PPG introduced a fast-drying clearcoat within its DELTRON® portfolio, significantly reducing refinish cycle times while maintaining high gloss and durability. Complementing this, PPG’s MIX’N’SHAKE™ automated stirring technology (October 2025) enhances color precision and material consistency, supporting the broader digitalization of body shop operations and reducing waste.

Aesthetic and functional advancements are converging in next-generation coatings. BASF’s “Driving the Proxy” collection (October 2025) highlights the integration of functional layers such as radar transparency into visually advanced coatings, supporting the development of autonomous and connected vehicles. Similarly, AkzoNobel’s partnership extension with McLaren Racing (January 2026) focuses on ultra-lightweight, high-performance coatings, leveraging insights from Formula 1 to enhance commercial automotive refinish products.

Sustainability and decarbonization are becoming central to innovation strategies. AkzoNobel’s hydrogen-powered spray booth (November 2024) represents a breakthrough in reducing emissions from energy-intensive curing processes, offering a scalable model for net-zero body shop operations. Meanwhile, Sherwin-Williams’ acquisition and integration of Suvinil (February 2026) is expanding its production footprint for automotive coatings in Latin America, supporting regional growth and supply chain resilience.

Strategic expansion and workforce development are also shaping the market. Nippon Paint’s plan to deploy 5,000 Application Service Partners (February 2026) is aimed at improving application efficiency and reducing lead times, particularly for custom coatings. Additionally, Kansai Nerolac’s amalgamation with Nerofix (February 2026) strengthens its ability to deliver integrated coating and adhesive solutions for automotive manufacturing.

Financial performance and premiumization strategies further highlight market direction. Axalta’s record EBITDA in 2026 underscores strong demand for high-value coatings, particularly in mobility applications.

Phthalate Phase-Out Driving Safer and Sustainable Automotive Primer Formulations

The automotive coatings industry is undergoing a major regulatory-driven transformation as restrictions on phthalates—particularly Bis(2-ethylhexyl) phthalate (DEHP)—are enforced under EU REACH Annex XVII (Entry 51). As of 2026, coatings must maintain DEHP concentrations below 0.1% by weight, effectively eliminating its use in legacy primer systems and forcing a shift toward safer plasticizer alternatives.

This transition has reached near-complete adoption within Europe, with approximately 95% of automotive coatings produced in the European Economic Area now compliant with phthalate-free requirements. The impact extends beyond regulatory compliance into workplace safety improvements. Industry audits indicate a 40% reduction in hazardous emissions within automotive paint shops, reflecting a significant improvement in operator exposure conditions and environmental footprint.

Formulation innovation is central to this transition. Bio-based succinate plasticizers are increasingly replacing DEHP, delivering equivalent flexibility and adhesion while reducing carbon footprint by approximately 25%. These alternatives also align with broader sustainability goals, supporting the automotive industry’s shift toward greener manufacturing practices.

Importantly, the influence of EU regulation is extending globally. Approximately 80% of Tier 1 automotive suppliers have standardized phthalate-free coatings across North American and Asian operations to maintain supply chain consistency and regulatory alignment. This “globalization of compliance” is accelerating the universal adoption of safer coating chemistries, positioning phthalate-free formulations as the new industry standard.

2-Wet Monocoat Systems Revolutionizing Paint Shop Efficiency and Energy Consumption

Automotive OEMs, particularly in the commercial vehicle segment, are aggressively optimizing paint shop operations by transitioning from traditional 3-wet coating processes to advanced 2-wet monocoat systems. This shift is driven by the need to reduce energy consumption, as paint operations can account for up to 70% of total energy use in vehicle assembly plants.

The 2-wet monocoat process combines primer and basecoat layers into a single application step, followed by an ambient “no-heat” flash stage. This eliminates one curing oven and reduces the number of application stages from three to two. As a result, manufacturers are achieving energy savings of approximately 20% to 30% per vehicle, representing a substantial operational efficiency gain.

Facility design is also benefiting from this transition. By reducing process complexity, manufacturers can decrease paint line footprint by up to 15%, enabling more compact and modular plant layouts. This is particularly valuable for new production facilities designed with flexibility and scalability in mind.

Performance improvements have accompanied these process innovations. Modern monocoat systems based on hyper-branched acrylic polymers now achieve up to 90% gloss retention after four years, a dramatic improvement over earlier single-stage systems that exhibited minimal durability. Additionally, the reduction in coating layers contributes to a 12% decrease in VOC emissions per vehicle, supporting compliance with increasingly stringent environmental regulations.

This shift toward process consolidation is redefining automotive coating operations, delivering a combination of energy efficiency, environmental benefits, and improved coating performance.

Low-Bake Coatings Enabling Safe Processing of Lightweight EV Materials

The rapid growth of electric vehicles and the increasing use of lightweight materials such as aluminum alloys and carbon fiber composites are creating a strong demand for low-bake coating technologies. Traditional curing processes, which typically require temperatures around 140°C, pose risks to sensitive EV components, including battery systems and thin-gauge structural materials.

Low-bake polyurethane coatings are emerging as a critical solution, enabling curing at temperatures as low as 80°C. This lower thermal threshold provides a significant safety margin, particularly for battery-integrated vehicle architectures where excessive heat can trigger thermal management issues. In addition to safety benefits, these coatings offer substantial energy savings, reducing thermal energy consumption by 45% to 50%—the single largest carbon reduction opportunity within automotive paint operations.

Productivity gains are also notable. Modern low-bake coatings achieve rapid curing times, with “click-to-dry” performance in under 20 minutes at 80°C, increasing refinish and production throughput by approximately 35%. Despite the lower curing temperature, these coatings deliver high-end performance, including superior distinctness of image and enhanced scratch resistance, ensuring that EV surfaces maintain premium aesthetic quality throughout their lifecycle.

Radar-Transparent Coatings Supporting Advanced Driver Assistance Systems (ADAS) Integration

The advancement of autonomous driving technologies is creating a specialized demand for radar-transparent coatings that enable seamless integration of Advanced Driver Assistance Systems. Conventional metallic coatings can interfere with millimeter-wave radar signals, particularly in the 77–79 GHz range, leading to signal attenuation and reduced sensor accuracy.

To address this challenge, coating manufacturers are developing non-metallic pigment systems and dielectric resin formulations that allow radar signals to pass through with minimal interference. Advanced radar-transparent coatings achieve transmission losses below 1.5 dB, ensuring reliable sensor performance across the vehicle’s exterior.

The impact on vehicle functionality is significant. Next-generation radar systems, including 4D millimeter-wave architectures introduced in 2026, demonstrate up to 30% improvement in angular resolution when paired with sensor-compatible coatings. This enhances the accuracy of object detection and positioning, contributing to safer autonomous driving capabilities.

From a design perspective, these coatings enable greater aesthetic flexibility. Automotive designers can conceal sensors behind body-colored panels without compromising performance, resolving a long-standing conflict between design requirements and functional constraints. Validation testing conducted under real-world conditions confirms that radar-transparent coatings do not interfere with critical safety systems such as Automatic Emergency Braking, even in adverse weather scenarios.

Basecoat Segment Leads Automotive Coatings Market with 34% Share Driven by High-Value Pigment Technologies

Coating Layer Analysis: Waterborne Basecoat Systems Dominate with Advanced Color Effects and Process Integration

The basecoat segment holds a leading 34.0% share of the automotive coatings market in 2025, driven by its role as the primary carrier of color, aesthetics, and premium visual effects in vehicle finishing. Unlike other coating layers, basecoats contain a high concentration of expensive pigments such as aluminum flakes, mica, Xirallic pigments, and high-performance organic colorants, making them 2x–5x more costly per liter than primers or electrocoats. Automotive OEMs now offer 60–100 color variants per model, significantly increasing formulation complexity and boosting the value share of basecoats. A key industry shift is the dominance of waterborne basecoat technology, accounting for over 80% of global OEM usage, driven by stringent VOC regulations (EPA, REACH, China GB standards). Additionally, the rise of 3-wet compact paint processes—where primer functions are integrated into the basecoat—further amplifies its market share, reinforcing its position as the most critical layer in the automotive coatings value chain.

Passenger Cars Dominate Automotive Coatings Market with 63% Share Driven by Production Volume and Premiumization Trends

Vehicle Type Analysis: SUV Growth and EV Transition Accelerate Coatings Demand

Passenger cars account for a dominant 63.0% share of the automotive coatings market in 2025, driven by global production volumes of approximately 65–70 million units annually and a significantly larger painted surface area per vehicle (8–10 square meters) compared to other vehicle types. The segment is further strengthened by the ongoing shift toward SUVs and crossovers (CUVs), which now represent nearly 50% of global passenger car sales and require 15–25% more coating material per unit. Premiumization trends are also accelerating demand for advanced coating systems, including tri-coat and quad-coat finishes as well as matte clearcoats, which command 30–50% higher prices than standard coatings. Additionally, the transition to electric vehicle (EV) manufacturing is reshaping coating technologies, with increased adoption of low-bake and UV-curable coatings for lightweight materials like aluminum and composites. These innovations, combined with high production scale, solidify passenger cars as the primary driver of growth in the global automotive coatings market.

Automotive Coatings Market Competitive Landscape Driven by EV Innovation and High-Performance Coating Technologies

The automotive coatings market is shaped by OEM coatings, refinish coatings, electrocoat systems, and advanced clearcoats. Leading players are focusing on EV coatings, radar-compatible coatings, low-temperature curing technologies, and digital color systems to enhance durability, aesthetics, and sustainability across global automotive production.

PPG Industries leads automotive coatings with radar-compatible innovation and digital refinish systems

PPG Industries remains a dominant player in automotive coatings, supported by its strong OEM coatings and refinish coatings portfolio. The company reported $15.9 billion in net sales in 2025, driven by growth across automotive and industrial segments. Its MOONWALK automated mixing system, with over 3,000 installations, enhances precision and reduces material waste in refinish applications. PPG is advancing radar-compatible coatings that enable seamless sensor performance for Level 3 autonomous vehicles. The launch of “Secret Safari” under its 2026 color strategy highlights its leadership in automotive color trends and design innovation. Expansion of its North Carolina facility strengthens development of advanced primers and clearcoats for next-generation vehicles.

BASF strengthens automotive coatings with e-coat leadership and low-energy curing technologies

BASF is advancing automotive coatings through its strategic “Winning Ways” transformation and focus on high-performance coating systems. The transition of its coatings division into a standalone business in 2025 enhances agility in addressing EV and autonomous vehicle demands. BASF leads the cathodic electrocoat segment, critical for corrosion protection in EV battery structures and complex vehicle architectures. Its collaboration with Sirrus introduces methylene malonate-based coatings that reduce curing temperatures and energy consumption. The company is also promoting biomass balance solutions to replace fossil-based raw materials in clearcoat production. Product development focuses on sustainability, efficiency, and advanced coating technologies.

AkzoNobel accelerates automotive coatings growth with merger-driven scale and circular innovation

AkzoNobel is strengthening its position in automotive coatings through its merger with Axalta, targeting €600 million in synergies across R&D and supply chain operations. The company achieved a 14.2% adjusted EBITDA margin in 2026 through operational efficiency and focus on premium coating brands. Its “Rhythm of Blues” color collection reflects evolving automotive interior design trends and color customization demand. The development of removable coatings technology supports vehicle recycling and refurbishment, aligning with circular economy regulations. AkzoNobel continues to expand its presence in high-performance coatings and sustainable automotive solutions. Product innovation focuses on durability, aesthetics, and recyclability.

Axalta drives automotive coatings innovation with AI-powered manufacturing and EV safety solutions

Axalta Coating Systems is recognized for advanced automotive coatings innovation, supported by record financial performance and strong R&D investment. The company reported a 22% adjusted EBITDA margin in 2025, enabling continued development of next-generation coatings. Its Alesta e-PRO FG Black coating provides fire resistance for EV battery protection, addressing thermal safety requirements. The TintMaster AI platform improves color accuracy and reduces waste by 29%, enhancing manufacturing efficiency. EcoNextJet digital coating technology enables large-scale vehicle customization without increasing production downtime. Product development focuses on UV-curable clearcoats, EV safety coatings, and digital manufacturing solutions.

Kansai Paint strengthens APAC automotive coatings leadership with full-stack OEM solutions

Kansai Paint holds a leading position in automotive coatings across Asia-Pacific, particularly in India and Japan. The company reported revenues of ₹7,500 crore in FY2024, maintaining its leadership in key regional markets. Its full-stack coating solutions include pretreatment chemicals, electro-deposition primers, and high-solid topcoats for OEM applications. Strategic price adjustments in 2026 support margin improvement amid raw material volatility. Kansai is shifting its business mix toward industrial coatings, targeting over 50% contribution from OEM and industrial segments. Product development focuses on integrated coating systems and long-term automotive partnerships.

South Korea Automotive Coatings Market: Self-Healing Clearcoats and High-Voltage EV Coatings Driving Next-Gen Innovation

South Korea stands as a global leader in the automotive coatings market, particularly in functional polymer engineering and EV-focused coating technologies. The implementation of hydrogen-bonded elastomeric self-healing clearcoats, now standardized in Hyundai’s 2026 premium EV lineup, is redefining durability by enabling coatings to autonomously repair micro-scratches at room temperature. This advancement significantly enhances vehicle aesthetics and lifecycle performance in high-end automotive segments.

The country is also advancing rapidly in EV-specific coating technologies. KCC Corporation’s specialized facility in Ulsan is producing high-heat-resistant epoxy coatings for EV motor housings and power electronics, while innovations such as dielectric powder coatings with breakdown voltages above 30 kV/mm are critical for 800V battery architectures. The introduction of thermal-indicator paints that change color to detect battery hotspots is improving safety and maintenance efficiency. Regulatory enforcement under the “Clean Paint Act” is driving VOC reduction, while AI-integrated paint application systems are optimizing efficiency by reducing paint waste across Hyundai and Kia production lines.

China Automotive Coatings Market: Waterborne Coating Dominance and EV Manufacturing Expansion Accelerating Growth

China leads the global automotive coatings market in volume, supported by its massive EV production base and aggressive sustainability targets under Carbon Neutrality 2060. Government mandates such as the “Green Auto-Manufacturing” initiative are requiring all new automotive paint lines to adopt waterborne basecoats or powder clearcoats by 2027, accelerating the transition toward eco-friendly coatings.

Technological innovation is driving competitive differentiation. BASF’s automated OEM coatings facility in Shanghai is advancing 3-wet coating processes, improving efficiency and reducing emissions. Innovations such as photocatalytic air-purifying coatings for EV interiors are enhancing cabin air quality by neutralizing VOCs. The deployment of radar-transparent coatings for autonomous vehicles ensures compatibility with ADAS systems, while biomass-balanced coatings are reducing carbon footprints. Additionally, the expansion of ultra-low-VOC cathodic electrocoats with enhanced corrosion resistance is strengthening China’s leadership in sustainable automotive coating technologies.

United States Automotive Coatings Market: PFAS-Free Transition and Aerodynamic Coatings Enhancing EV Performance

The United States automotive coatings market is evolving through strong regulatory oversight and innovation in high-performance coatings. The implementation of NESHAP Phase II regulations is capping emissions, accelerating the shift toward low-VOC and PFAS-free coating technologies across OEM and refinish segments.

Innovation is centered on EV performance and safety. The introduction of thermal management coatings for battery fire protection is improving passenger safety, while the adoption of laminar-flow coatings—borrowed from aerospace—is reducing drag and enhancing vehicle efficiency. Investments such as Axalta’s Sustainable Mobility Center are driving development of low-cure coatings that reduce energy consumption in manufacturing. Additionally, the refinish market is benefiting from advanced digital tools, including spectrophotometers paired with waterborne paints, ensuring precise color matching for complex finishes.

Germany Automotive Coatings Market: Luxury Finishing Standards and Low-Temperature Cure Technologies Leading Innovation

Germany remains the global benchmark for premium automotive coatings, particularly in luxury vehicle segments. The development of UV-curable clearcoats capable of achieving high hardness within seconds is revolutionizing manufacturing efficiency, reducing paint shop processing time significantly.

The market is also driven by sustainability and performance innovation. BASF’s biomass-balanced coating facility is advancing eco-friendly production, while partnerships between Covestro and Nippon Paint are driving development of polyurethane coatings with enhanced stone-chip resistance. High-performance clearcoats with 2H–3H hardness are becoming standard in luxury brands, offering superior scratch resistance. Regulatory compliance with the Industrial Emissions Directive is pushing adoption of closed-loop VOC systems, while antimicrobial coatings are gaining traction in shared mobility applications, reinforcing Germany’s leadership in advanced automotive coatings.

India Automotive Coatings Market: PLI-Driven Manufacturing Expansion and Infrastructure Synergy Fueling Demand

India is emerging as a high-growth market in the automotive coatings industry, driven by strong government support and rapid industrial expansion. The Production Linked Incentive (PLI) scheme is enabling domestic production of high-purity pigments and advanced coating materials, strengthening the local supply chain.

Market dynamics are further shaped by infrastructure and mobility trends. The expansion of Vande Bharat trains and electric bus manufacturing is driving demand for anti-graffiti polyurethane coatings, while automotive applications are seeing increased adoption of anti-corrosive underbody coatings designed for high-humidity and coastal environments. Capacity expansions by major players and consolidation activities are enhancing competitiveness. Additionally, rising demand for UV-stable coatings in two-wheelers is addressing challenges posed by extreme tropical conditions, positioning India as a key growth hub.

Japan Automotive Coatings Market: Radar-Transparent Finishes and Sensor-Friendly Coatings Driving Autonomous Mobility

Japan is at the forefront of innovation in the automotive coatings market, particularly in sensor-compatible coatings for autonomous vehicles. The development of signal-transparent metallic coatings allows radar waves to pass through vehicle surfaces without interference, ensuring optimal performance of ADAS systems.

Technological advancements are also enhancing functionality and durability. The introduction of self-cleaning hydrophilic coatings for automotive sensors is improving visibility and safety, while high-durability polyester coatings are extending product lifecycles in commercial vehicles. Japan’s focus on supply chain security for critical pigments and adoption of concentrated coating systems is improving efficiency and sustainability. Additionally, the expansion of antimicrobial coatings in public transportation highlights the growing importance of multifunctional automotive coatings in urban mobility systems.

Brazil Automotive Coatings Market: Bio-Based Resin Innovation and Tropical Climate Coatings Driving Growth

Brazil is strengthening its position in the automotive coatings market through innovation in bio-based materials and climate-adaptive coatings. The commercialization of soybean and castor oil-derived resins is reducing reliance on petrochemical feedstocks, aligning with sustainability goals.

The market is also driven by strong demand in the refinish and commercial vehicle segments. High-solids clearcoats are gaining popularity in refurbishment applications, delivering OEM-quality finishes. Regulatory initiatives such as the “Green Seal” are promoting eco-friendly coatings by reducing hazardous pigments. Additionally, the adoption of infrared-reflective coatings is improving thermal comfort in vehicles, particularly in tropical climates. Strategic expansions and consolidation activities are further strengthening Brazil’s role as a key regional hub for automotive coatings.

United Kingdom Automotive Coatings Market: Graphene-Based Coatings and Smart Repair Technologies Driving Innovation

The United Kingdom automotive coatings market is evolving through advanced material innovation and regulatory flexibility. The use of graphene-enhanced coatings is significantly improving corrosion resistance and conductivity, particularly in EV applications.

The market is also characterized by strong growth in luxury and bespoke coatings, with manufacturers offering custom “Paint-to-Sample” finishes using nanoparticle-dispersed pigments. Investments in sustainable manufacturing, including fully renewable-energy-powered coating facilities, are strengthening the UK’s position as a sustainability hub. Additionally, advancements in self-healing polymers and anti-icing coatings for autonomous systems are expanding application scope. The integration of anti-static coatings in EV infrastructure further highlights the market’s diversification, positioning the UK as a leader in next-generation automotive coating technologies.

Automotive Coatings Market Report Scope

Automotive Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.9 Billion

|

|

Market Size (2032)

|

$35.5 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Coating Layer (Electrocoat (E-Coat), Primer Surfacer, Basecoat, Clearcoat), By Resin Chemistry (Polyurethane (PU), Epoxy, Acrylic, Polyester, Vinyl and Alkyd), By Technology (Water-borne, Solvent-borne, Powder Coatings, UV-Cured and Radiation Curable), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Two-Wheelers and Three-Wheelers), By Sales Channel (OEM (Original Equipment Manufacturer), Automotive Refinish, Automotive Parts and Components), By Substrate Compatibility (Metal, Plastic and Composites, Glass)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., BASF SE, Axalta Coating Systems Ltd., The Sherwin-Williams Company, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., KCC Corporation, Sika AG, Jotun A/S, Mankiewicz Gebr. & Co., Berger Paints India Limited, Asian Paints PPG Pvt. Ltd., Beckers Group, Hempel A/S

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Automotive Coatings Market Segmentation

By Coating Layer

- Electrocoat (E-Coat)

- Primer Surfacer

- Basecoat

- Clearcoat

By Resin Chemistry

- Polyurethane (PU)

- Epoxy

- Acrylic

- Polyester

- Vinyl and Alkyd

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- UV-Cured and Radiation Curable

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Two-Wheelers and Three-Wheelers

By Sales Channel

- OEM (Original Equipment Manufacturer)

- Automotive Refinish

- Automotive Parts and Components

By Substrate Compatibility

- Metal

- Plastic and Composites

- Glass

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Automotive Coatings Market

- PPG Industries, Inc.

- Akzo Nobel N.V.

- BASF SE

- Axalta Coating Systems Ltd.

- The Sherwin-Williams Company

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- KCC Corporation

- Sika AG

- Jotun A/S

- Mankiewicz Gebr. & Co.

- Berger Paints India Limited

- Asian Paints PPG Pvt. Ltd.

- Beckers Group

- Hempel A/S

*- List not Exhaustive

Table of Contents: Automotive Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Automotive Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Automotive Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Market Drivers: EV Expansion, Lightweight Materials, and Advanced Surface Performance

2.4. Technology Shift: Smart Coatings, Self-Healing Systems, and Radar Transparency

2.5. Sustainability Transition: Low-VOC, Waterborne, and Carbon Reduction Initiatives

3. Innovations Reshaping the Automotive Coatings Market

3.1. Trend: Digitalization and Automated Paint Systems Enhancing Efficiency and Precision

3.2. Trend: Low-Bake, 2-Wet Monocoat, and Radar-Transparent Coating Technologies

3.3. Opportunity: EV-Specific Coatings for Battery Protection and Lightweight Substrates

3.4. Opportunity: Sustainable Formulations and Phthalate-Free Coating Systems

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Automotive Coatings Market

5.1. By Coating Layer

5.1.1. Electrocoat (E-Coat)

5.1.2. Primer Surfacer

5.1.3. Basecoat

5.1.4. Clearcoat

5.2. By Resin Chemistry

5.2.1. Polyurethane (PU)

5.2.2. Epoxy

5.2.3. Acrylic

5.2.4. Polyester

5.2.5. Vinyl and Alkyd

5.3. By Technology

5.3.1. Water-borne

5.3.2. Solvent-borne

5.3.3. Powder Coatings

5.3.4. UV-Cured and Radiation Curable

5.4. By Vehicle Type

5.4.1. Passenger Cars

5.4.2. Light Commercial Vehicles (LCVs)

5.4.3. Heavy Commercial Vehicles (HCVs)

5.4.4. Two-Wheelers and Three-Wheelers

5.5. By Sales Channel

5.5.1. OEM (Original Equipment Manufacturer)

5.5.2. Automotive Refinish

5.5.3. Automotive Parts and Components

5.6. By Substrate Compatibility

5.6.1. Metal

5.6.2. Plastic and Composites

5.6.3. Glass

6. Country Analysis and Outlook of Automotive Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Automotive Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Automotive Coatings Market Size Outlook to 2032

7.1.1. By Coating Layer

7.1.2. By Resin Chemistry

7.1.3. By Technology

7.1.4. By Vehicle Type

7.1.5. By Sales Channel

7.1.6. By Substrate Compatibility

7.2. Europe Automotive Coatings Market Size Outlook to 2032

7.2.1. By Coating Layer

7.2.2. By Resin Chemistry

7.2.3. By Technology

7.2.4. By Vehicle Type

7.2.5. By Sales Channel

7.2.6. By Substrate Compatibility

7.3. Asia Pacific Automotive Coatings Market Size Outlook to 2032

7.3.1. By Coating Layer

7.3.2. By Resin Chemistry

7.3.3. By Technology

7.3.4. By Vehicle Type

7.3.5. By Sales Channel

7.3.6. By Substrate Compatibility

7.4. South America Automotive Coatings Market Size Outlook to 2032

7.4.1. By Coating Layer

7.4.2. By Resin Chemistry

7.4.3. By Technology

7.4.4. By Vehicle Type

7.4.5. By Sales Channel

7.4.6. By Substrate Compatibility

7.5. Middle East and Africa Automotive Coatings Market Size Outlook to 2032

7.5.1. By Coating Layer

7.5.2. By Resin Chemistry

7.5.3. By Technology

7.5.4. By Vehicle Type

7.5.5. By Sales Channel

7.5.6. By Substrate Compatibility

8. Company Profiles: Leading Players in the Automotive Coatings Market

8.1. PPG Industries, Inc.

8.2. Akzo Nobel N.V.

8.3. BASF SE

8.4. Axalta Coating Systems Ltd.

8.5. The Sherwin-Williams Company

8.6. Nippon Paint Holdings Co., Ltd.

8.7. Kansai Paint Co., Ltd.

8.8. KCC Corporation

8.9. Sika AG

8.10. Jotun A/S

8.11. Mankiewicz Gebr. & Co.

8.12. Berger Paints India Limited

8.13. Asian Paints PPG Pvt. Ltd.

8.14. Beckers Group

8.15. Hempel A/S

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures