Automotive Conformal Coatings Market Size and Growth Driven by Vehicle Electrification and PCB Protection Needs

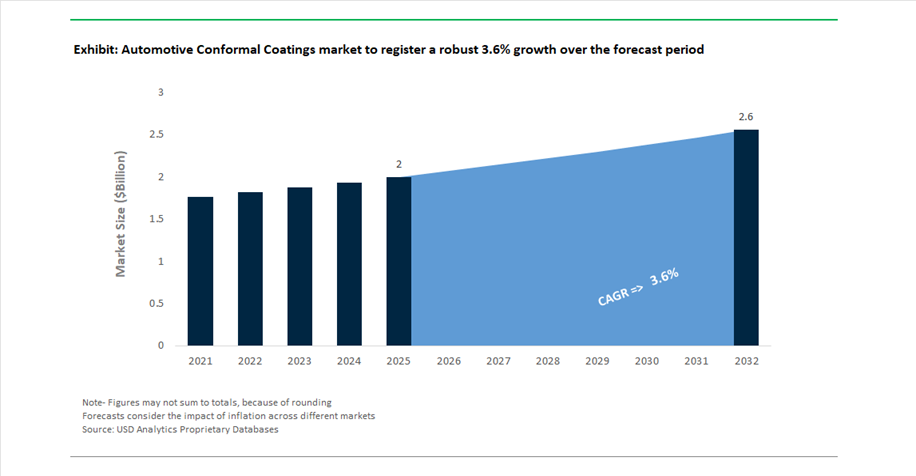

The Automotive Conformal Coatings Market is projected to grow from USD 2 billion in 2025 to USD 2.6 billion by 2032, registering a CAGR of 3.6%. This steady growth reflects the increasing role of vehicles as electronics-intensive platforms, where conformal coatings are essential for protecting printed circuit boards (PCBs) and electronic assemblies from environmental and operational stress.

Modern vehicles, particularly electric and autonomous platforms, integrate a high density of advanced electronics such as ADAS modules, infotainment systems, power electronics, sensors, and battery management systems. Conformal coatings provide a thin, protective layer that shields these components from moisture, dust, thermal cycling, vibration, and chemical exposure, ensuring long-term reliability and performance. As vehicles evolve into “computers on wheels,” the demand for high-performance coatings that can maintain electrical insulation and mechanical stability under extreme conditions is intensifying.

The market is also being shaped by the rapid expansion of electric vehicles (EVs) and autonomous driving technologies, which require coatings capable of supporting high-voltage systems, miniaturized electronics, and complex sensor architectures. Additionally, regulatory and safety requirements are pushing manufacturers toward coatings that meet stringent flammability, durability, and environmental standards, including low-VOC and solvent-free formulations.

Technological advancements are focused on UV-curable coatings, silicone-based materials, and nano-engineered formulations, which offer faster curing times, improved adhesion, and enhanced resistance to harsh automotive environments. Competitive dynamics are defined by innovation in specialty chemicals, strategic investments in semiconductor-related materials, and increasing collaboration with automotive OEMs, positioning conformal coatings as a critical enabler of next-generation mobility systems

UV-Curing Innovation, Semiconductor Expansion, and Supply Chain Pressures Transforming Market Dynamics

The automotive conformal coatings market is undergoing significant transformation driven by advanced material innovation, semiconductor ecosystem expansion, and cost pressures across the supply chain. A key development occurred in February 2026, when Henkel launched Loctite Stycast UV 7998, a solvent-free, UL 94 V-0 rated conformal coating designed to reduce CO₂ emissions by up to 40% compared to traditional systems. This innovation highlights the industry’s shift toward sustainable, high-performance coatings for automotive electronics.

Product innovation is strongly centered on UV/LED light-curable technologies. In March 2026, Dymax showcased advanced conformal coatings at APEX EXPO, engineered to withstand extreme automotive conditions, including high temperatures, vibration, and outgassing challenges in under-the-hood environments. Complementing this, Dymax’s NASA-standard low-outgassing adhesive (October 2025) is being adapted for automotive sensors and LiDAR systems, ensuring optical clarity and long-term reliability in precision components.

Strategic investments in semiconductor and material supply chains are reinforcing market growth. Shin-Etsu’s ¥83 billion investment in a new semiconductor materials facility (announced July 2025, operational 2026) is aimed at supporting the growing demand for automotive chips and advanced electronics, which directly drives the need for conformal coatings. Additionally, the expansion of its U.S. production capacity ensures stable supply of high-purity materials used in coating formulations.

Corporate strategies are increasingly focused on efficiency, digitalization, and high-specification solutions. Dow’s Transform to Outperform initiative leverages AI and automation to enhance productivity in specialty chemical lines, including silicone-based coatings for EV power electronics and ADAS systems. Similarly, H.B. Fuller’s global price adjustment (March 2026) reflects ongoing raw material constraints in petrochemical supply chains, underscoring cost pressures across the industry.

Capacity expansion and regional growth initiatives are further strengthening market capabilities. Dymax Europe’s facility expansion in Germany (April 2026) enhances production and R&D capacity for light-curing conformal coatings, supporting European automotive OEMs transitioning toward electrified and autonomous platforms. Meanwhile, Henkel’s UL 94 V-0 certification for its new coating series (February 2026) reinforces compliance with stringent safety standards, particularly for high-voltage EV battery systems.

Financial performance and market positioning also reflect strong demand for specialized solutions. H.B. Fuller’s $3.5 billion revenue in FY2025 highlights its expansion into highly specified automotive electronics coatings, driven by increasing complexity and miniaturization of components.

ISO 26262 ASIL-D Requirements Driving Ultra-Reliable Coating Systems for Automotive Electronics

The automotive conformal coatings industry is undergoing a structural shift as ISO 26262 functional safety standards redefine performance expectations for Electronic Control Units (ECUs). Systems classified under ASIL-D—the highest safety integrity level—require coatings that deliver near-zero failure rates in mission-critical applications such as braking, steering, and advanced driver assistance systems. These stringent requirements are elevating conformal coatings from a protective layer to a core functional safety component.

To meet ASIL-D benchmarks, coatings must demonstrate a 99.9% reliability rate in preventing moisture-induced failures such as dendrite growth and electrochemical migration over a 15-year operational lifespan. This long-term reliability requirement is driving the adoption of advanced material systems, including Parylene coatings and thin-film urethanes, particularly for high-density Domain Control Units used in autonomous driving platforms. The increasing complexity of these systems has contributed to a 25% rise in demand for high-performance coatings capable of protecting micro-pitch electronic architectures.

Manufacturing processes are also evolving to support compliance. Approximately 40% of Tier-1 suppliers have integrated automated optical inspection systems with UV-fluorescent tracers into their coating lines, ensuring full coverage and traceability. Additionally, coatings certified under IPC-CC-830C are now being cross-validated against ISO 16750-4 environmental stress tests, including thermal cycling and salt spray exposure, to ensure operational stability under extreme conditions.

This convergence of safety standards, material innovation, and process validation is redefining conformal coating requirements, positioning high-reliability coating systems as essential enablers of next-generation automotive electronics.

100% Solids UV-Cure Systems Transforming High-Volume Automotive Electronics Production

The transition toward 100% solids UV-cure conformal coatings is fundamentally transforming production efficiency and environmental compliance in automotive electronics manufacturing. Traditional solvent-based coatings are being phased out due to VOC emissions and longer curing times, making UV-cure systems the preferred solution for high-throughput assembly lines.

UV-cure coatings offer a dramatic improvement in process efficiency, reducing curing times by up to 90% compared to thermal curing methods. This enables automated selective coating systems to achieve production rates of up to 300 printed circuit boards per hour, significantly enhancing manufacturing throughput. The elimination of solvents also ensures compliance with stringent environmental regulations in Europe and North America, removing the need for costly emissions control systems such as thermal oxidizers.

Energy efficiency is another critical advantage. The adoption of UV-LED curing technology reduces energy consumption by up to 70% compared to conventional mercury arc systems, supporting automotive OEMs in achieving carbon neutrality targets. Additionally, advancements in dual-cure formulations—combining UV and moisture curing mechanisms—have resolved historical limitations related to shadowed areas under complex components. Modern systems now achieve complete curing coverage, even in densely populated electronic assemblies.

This shift toward UV-cure technology represents a convergence of sustainability, productivity, and performance, positioning it as the dominant coating process for next-generation automotive electronics manufacturing.

High-Temperature Silicone Coatings Supporting Next-Generation EV Power Electronics

The evolution of electric vehicle architectures, particularly the adoption of 800V systems and silicon carbide power modules, is creating a specialized demand for high-temperature conformal coatings. These systems operate under extreme thermal conditions, requiring coatings that can maintain electrical insulation and structural integrity at temperatures exceeding 200°C.

Advanced silicone-based conformal coatings are emerging as the preferred solution in this segment. These materials maintain dielectric strength above 1500 V/mil even after prolonged exposure to high temperatures, ensuring reliable insulation for high-voltage components such as traction inverters. In addition to thermal stability, silicone coatings offer excellent flexibility, providing vibration damping and thermal shock resistance. This is particularly important in EV drivetrains, where high torque and rapid load changes generate significant mechanical stress.

The use of silicone coatings also supports increased power density in electronic assemblies. By enabling tighter component spacing without compromising insulation, these coatings allow for up to a 15% reduction in printed circuit board footprint, contributing to more compact and efficient power electronics designs.

Low-Viscosity Conformal Coatings Enabling Precision Protection in LiDAR Systems

The rapid deployment of LiDAR technology in autonomous vehicles is creating new requirements for conformal coatings capable of protecting highly sensitive optical and electronic components. Unlike traditional electronic assemblies, LiDAR systems involve complex optical stacks and precision sensors that require coatings with exceptional penetration and optical compatibility.

Next-generation low-viscosity conformal coatings, with viscosities as low as 20 to 50 centipoise, are being developed to achieve deep penetration into densely packed assemblies, including Ball Grid Array sensors and optical emitters. This ensures complete coverage and protection in areas that are inaccessible to conventional coating methods.

Optical integrity is a critical performance parameter in this segment. Advanced formulations are engineered to exhibit zero outgassing, preventing the formation of haze on lenses and mirrors that could degrade signal-to-noise ratios by up to 30%. This is essential for maintaining the accuracy and reliability of LiDAR systems, which rely on precise optical measurements for object detection and navigation.

Miniaturization trends are further driving adoption. As LiDAR units become smaller and more integrated into vehicle structures, low-viscosity coatings enable masking-free application through high-precision selective jetting techniques. This reduces processing costs by approximately 20% while ensuring consistent coating performance across complex geometries.

UV-Cured Conformal Coatings Lead Automotive Electronics Market with 38.5% Share Driven by High-Speed Manufacturing Efficiency

Coating Technology Analysis: UV-Cured Systems Dominate with Instant Cure and Dual-Cure Reliability

UV-cured conformal coatings hold a leading 38.5% share of the automotive conformal coatings market in 2025, driven by their ability to deliver ultra-fast curing (2–5 seconds), making them indispensable for high-volume automotive electronics manufacturing. Unlike traditional moisture-cure or heat-cure coatings, UV systems enable inline, automated coating processes, eliminating work-in-progress bottlenecks and improving production efficiency. These coatings are 100% solids and solvent-free, ensuring zero VOC emissions and 70–80% lower energy consumption, aligning with OEM sustainability targets. A major innovation is dual-cure technology, where exposed areas cure instantly under UV light while shadowed regions cure via ambient moisture, ensuring complete coverage on complex PCB assemblies. Additionally, UV-cured coatings provide exceptional chemical resistance against battery electrolytes, brake fluids, and harsh automotive environments, making them critical for EV battery systems and power electronics protection.

Passenger Vehicles Dominate Automotive Conformal Coatings Market with 68% Share Driven by ECU Proliferation and EV Growth

Vehicle Type Analysis: Rising Electronics Content and EV Architectures Accelerate Coating Demand

Passenger vehicles account for a dominant 68.0% share of the automotive conformal coatings market in 2025, fueled by the rapid increase in electronic control units (ECUs) and sensors per vehicle, now reaching 100–150 ECUs and 50–70 sensors in modern cars. The shift toward zonal electronic architectures is further increasing the complexity and size of PCBs, requiring high-reliability conformal coatings capable of withstanding extreme thermal cycling (-40°C to +125°C) and harsh environmental exposure. The rise of battery electric vehicles (BEVs)—representing 18–20% of global production—is significantly amplifying demand, as EVs require advanced coatings for battery management systems (BMS), inverters, and high-voltage electronics, often operating in corrosive and high-temperature conditions. These applications demand thicker, chemically resistant coatings such as UV-cured urethanes and parylene-based systems. Combined with increasing electronic integration and safety requirements, passenger vehicles remain the primary growth driver in the global automotive conformal coatings market.

Automotive Conformal Coatings Market Competitive Landscape Driven by EV Electronics Protection and Advanced Coating Technologies

The automotive conformal coatings market is driven by rapid electrification, ADAS integration, and increasing PCB density in vehicles. Key players focus on UV-curable coatings, silicone conformal coatings, nano-coatings, and low-VOC formulations to enhance thermal stability, moisture resistance, and reliability in automotive electronics.

Henkel leads automotive conformal coatings with UV-curable innovation and sustainable formulations

Henkel dominates the automotive conformal coatings market through its Loctite and Technomelt portfolios, targeting high-reliability automotive electronics protection. The company is prioritizing UV-curable conformal coatings that reduce curing time from hours to seconds, improving manufacturing efficiency and lowering carbon emissions. Its dual-cure UV/moisture coatings deliver 30% improved protection in shadow areas, ensuring full insulation of complex automotive PCB assemblies. Expansion of technical centers in Shanghai and South Korea supports real-time simulation for EV platform development. Henkel’s leadership in low-VOC and solvent-free coatings aligns with stringent EU CSRD and China VOC regulations. Product innovation focuses on sustainability, high-performance insulation, and advanced curing technologies.

Dow strengthens silicone conformal coatings leadership for high-temperature automotive electronics

Dow leads the silicone conformal coatings segment, which is witnessing strong demand due to rising thermal loads in EV power electronics. The segment is driven by applications in power conversion modules and ADAS systems. Its DOWSIL portfolio includes high-viscosity coatings for dam-and-fill applications, preventing material migration in compact sensor housings. The DOWSIL CC-8030 coating offers dual UV-moisture curing with high flexibility and moisture resistance. Dow’s integrated solutions combine conformal coatings with thermal management materials such as gap fillers. Product development focuses on high-temperature stability, flexibility, and system-level integration.

H.B. Fuller expands automotive conformal coatings with customized solutions for EV and miniaturized electronics

H.B. Fuller is gaining traction in automotive conformal coatings through its Engineering Adhesives segment, supported by $3.5 billion in 2025 revenue. The company launched advanced acrylic and urethane coatings in 2026 designed for high-density interconnect (HDI) boards and miniaturized automotive electronics. Its solutions address corrosion risks in EV batteries, including protection against electrolyte leakage. H.B. Fuller’s strength lies in customized formulations tailored for fuel-cell systems, hydrogen sensors, and specialized automotive components. A global technical service initiative supports EV battery manufacturers with application-specific coatings. Product strategy focuses on customization, reliability, and next-generation automotive electronics protection.

Dymax accelerates conformal coatings adoption with light-curable systems and smart inspection technologies

Dymax is a key innovator in light-curable conformal coatings, enabling ultra-fast processing for high-speed automotive production lines. Its See-Cure technology provides instant visual confirmation of coating coverage, improving quality assurance in automated manufacturing environments. Expansion of its Shenzhen facility in 2026 supports rising demand in the Asian EV market. Dymax offers parylene-alternative coatings that deliver comparable protection with lower cost and faster throughput. Its turnkey systems integrate coating materials with UV-curing equipment, reducing time to market by 15%. Product development focuses on process efficiency, inspection capability, and cost-effective protection solutions.

Shin-Etsu advances nano-enabled conformal coatings with high-purity silicone technologies

Shin-Etsu is a leading supplier of high-performance conformal coatings in Asia, particularly in Japan and South Korea automotive markets. The company developed high-dielectric silicone coatings capable of maintaining insulation at temperatures up to +200°C, targeting next-generation SiC power electronics. Its vertical integration ensures superior raw material purity, enhancing reliability for sensitive automotive microelectronics. Shin-Etsu is advancing nano-coating technologies with ultra-thin moisture barriers as low as 5 microns for compact PCBs. The company supports major OEMs such as Toyota and Hyundai in autonomous vehicle development. Product innovation focuses on high-temperature performance, miniaturization, and advanced electronic protection.

China Automotive Conformal Coatings Market: Dual-Cure UV Technologies and 800V EV Architecture Driving High-Volume Leadership

China continues to dominate the automotive conformal coatings market, emerging as the global epicenter for high-volume production and next-generation EV electronics protection. Under the “Made in China 2025 – Automotive Phase” mandate, the industry has undergone a massive transformation, with a 45% shift toward UV-curable and waterborne conformal coatings across PCB assembly lines. This transition is accelerating sustainability while meeting the rapid production cycles of the world’s largest EV manufacturing ecosystem.

Technological advancements are centered around high-voltage EV architectures and sensor integration. The widespread adoption of high-dielectric silicone conformal coatings is enabling safe operation of 800V battery management systems by preventing electrical arcing. Additionally, innovations in optically clear, low-outgassing coatings are supporting LiDAR and camera modules by preventing fogging during thermal cycling. China is also investing heavily in selective coating robotics for zonal controllers, replacing traditional ECUs and enhancing reliability in autonomous systems. Regulatory enforcement under GB/T 30981-2026 standards is driving VOC reduction, while R&D into ultra-high-temperature epoxy coatings for silicon carbide (SiC) power modules is strengthening China’s leadership in high-performance automotive electronics coatings.

United States Automotive Conformal Coatings Market: PFAS-Free Innovation and Aerospace-Grade Reliability Driving Advanced Applications

The United States automotive conformal coatings market is evolving through stringent regulatory frameworks and high-performance innovation, particularly in autonomous vehicles and defense-grade electronics. Following the 2025 EPA directive, over 90% of automotive conformal coating portfolios have transitioned to PFAS-free and TPO-free UV-curable formulations, significantly improving environmental compliance and safety.

The market is also leveraging aerospace and defense technologies for automotive applications. The deployment of Parylene-C vapor deposition coatings is ensuring long-term durability of autonomous trucking sensors, offering resistance to vibration, salt spray, and extreme environments. Additionally, the integration of anti-tamper epoxy coatings for V2X modules is enhancing cybersecurity by preventing physical hardware interference. Innovation is further supported by advanced R&D infrastructure, including precision coating systems for nano-coating development. Federal initiatives promoting bio-derived conformal resins with high dielectric strength are reinforcing the U.S. position as a leader in sustainable, high-performance conformal coatings.

Germany Automotive Conformal Coatings Market: Zero-Defect Manufacturing and Low-Temperature Cure Technologies Driving Precision Engineering

Germany sets the global benchmark for automotive conformal coatings through its focus on zero-defect manufacturing, sustainability, and precision engineering. The introduction of hybrid UV coatings that cure below 100°C is enabling the protection of heat-sensitive components in advanced digital cockpit systems used by premium automotive brands.

The market is also characterized by high durability and quality assurance. The adoption of ultra-flexible urethane-acrylate coatings capable of withstanding over 1,000 thermal shock cycles ensures reliability in harsh operating conditions. Regulatory compliance under EU frameworks, including the Digital Product Passport, is driving transparency and recyclability in coating formulations. Additionally, innovations such as fluorescent tracer integration for automated optical inspection (AOI) are improving quality control in high-speed manufacturing environments. Germany’s leadership in antimicrobial coatings for HVAC electronics further strengthens its position in advanced automotive conformal coating technologies.

Japan Automotive Conformal Coatings Market: Nanoscale Precision and Stress-Relief Coatings Driving High-End Electronics Protection

Japan remains a global leader in automotive conformal coatings, driven by nanoscale precision and advanced material engineering. The launch of high-performance nano-coatings with exceptional elongation properties is reducing mechanical stress on fine-pitch components, ensuring reliability in miniaturized automotive electronics.

The country is also advancing hybrid coating technologies tailored for EV power modules. The development of silicone-epoxy hybrid coatings combines moisture resistance with thermal flexibility, making them ideal for IGBT modules and high-performance electronic systems. Japan’s focus on low-dielectric coatings for 5G and V2X communication systems is supporting the next generation of connected and autonomous vehicles. Additionally, the adoption of solvent-free, moisture-cure silicones is improving sustainability by eliminating energy-intensive curing processes, reinforcing Japan’s leadership in precision automotive coatings.

South Korea Automotive Conformal Coatings Market: OLED-Integrated Protection and Self-Healing Coatings Driving Innovation

South Korea is a dominant force in the automotive conformal coatings market, particularly in advanced display integration and battery system protection. The development of ultra-thin conformal coatings for curved OLED automotive displays is enabling high-performance protection without compromising optical clarity or touch sensitivity.

Innovation is also focused on EV battery systems and durability enhancement. Strategic investments in high-solid conformal coatings are supporting large-scale battery production clusters, while the integration of self-healing polymer technologies is improving resistance to micro-cracks caused by vibration. The adoption of AI-driven coating formulation platforms is accelerating product development for extreme climate conditions. Regulatory leadership under K-REACH is eliminating hazardous substances, while advanced application technologies such as plasma-enhanced chemical vapor deposition (PECVD) are enabling precision coating of complex sensor geometries.

India Automotive Conformal Coatings Market: PLI-Driven Localization and EV Electronics Expansion Fueling Growth

India is emerging as one of the fastest-growing markets for automotive conformal coatings, supported by strong government incentives and expanding domestic EV manufacturing. The Production Linked Incentive (PLI) scheme has triggered significant investments in local production of high-grade acrylic and silicone coatings, strengthening the supply chain for automotive electronics.

Market growth is driven by diverse applications across EVs, railways, and public infrastructure. The standardization of anti-corrosive conformal coatings for EV bus controllers and railway signaling systems is enhancing durability in high-humidity and coastal environments. Rapid adoption of cost-effective acrylic coatings in electric two-wheelers is addressing challenges such as dust and monsoon exposure. Additionally, the expansion of localized manufacturing facilities and development of semi-automated coating systems are enabling SMEs to participate in the automotive electronics ecosystem, positioning India as a key growth hub.

Thailand Automotive Conformal Coatings Market: EV Sub-Assembly Hub and UV-LED Coating Technologies Driving Regional Growth

Thailand is strengthening its position as a regional hub in the automotive conformal coatings market, supported by government incentives and expansion of EV manufacturing facilities. Tax incentives under EV Package 3.5 have driven a significant increase in conformal coating line installations across the Eastern Economic Corridor.

Technological advancements are enhancing production efficiency and performance. The adoption of UV-LED curing systems is replacing legacy mercury-based technologies, improving sustainability and energy efficiency. Additionally, the demand for sulfur-resistant coatings is growing in heavy-duty vehicle and agricultural applications. Innovations such as dual-stage moisture-cure coatings are ensuring protection in complex PCB geometries, while investments in testing and certification facilities are aligning the market with international safety standards.

Taiwan Automotive Conformal Coatings Market: Semiconductor-Grade Precision and High-Density Interconnect Protection Leading Innovation

Taiwan remains a global leader in automotive conformal coatings, particularly in semiconductor-level precision and high-density electronics protection. The development of hybrid encapsulation-conformal coatings for chip-on-board applications is combining mechanical strength with comprehensive coverage, ensuring reliability in automotive power electronics.

The market is also driven by advanced R&D collaborations and cutting-edge technologies. Partnerships between semiconductor manufacturers and coating formulators are ensuring compatibility with next-generation substrates, while fluoropolymer-based coatings are supporting edge-computing modules in autonomous vehicles. The integration of cleanroom-compliant coating processes is enhancing quality for critical automotive electronics, while innovations in transparent conductive coatings are expanding applications in smart windshields. These advancements position Taiwan as a leader in high-precision automotive conformal coating technologies.

Automotive Conformal Coatings Market Report Scope

Automotive Conformal Coatings market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2 Billion

|

|

Market Size (2032)

|

$2.6 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Material Chemistry (Acrylic Resins (AR), Silicone Resins (SR), Polyurethane, Epoxy Resins (ER), Parylene (XY), Specialty Hybrid and Nano-coatings), By Coating Technology (UV-Cured (Ultraviolet), Heat-Cure, Solvent-borne, Moisture-Cured, Vapor Deposition), By Application Method (Selective Robotic Spraying, Automated Dipping, Manual and Automated Brushing, Aerosol and Needle Dispensing), By Automotive Component (ECUs and Control Modules, EV Battery Management Systems (BMS), ADAS and Sensor Suites, Infotainment and Connectivity, Interior Electronics, Power Electronics), By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Autonomous Shuttles and Delivery Bots)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Dow Inc., Chase Corporation, H.B. Fuller Company, Shin-Etsu Chemical Co., Ltd., 3M Company, Electrolube, Dymax Corporation, ELANTAS Electrical Insulation, Illinois Tool Works Inc., MG Chemicals, Kisco Ltd., Nordson Corporation, Huitian New Materials, Peters Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Automotive Conformal Coatings Market Segmentation

By Material Chemistry

- Acrylic Resins (AR)

- Silicone Resins (SR)

- Polyurethane

- Epoxy Resins (ER)

- Parylene (XY)

- Specialty Hybrid and Nano-coatings

By Coating Technology

- UV-Cured (Ultraviolet)

- Heat-Cure

- Solvent-borne

- Moisture-Cured

- Vapor Deposition

By Application Method

- Selective Robotic Spraying

- Automated Dipping

- Manual and Automated Brushing

- Aerosol and Needle Dispensing

By Automotive Component

- ECUs and Control Modules

- EV Battery Management Systems (BMS)

- ADAS and Sensor Suites

- Infotainment and Connectivity

- Interior Electronics

- Power Electronics

By Vehicle Type

- Passenger Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Autonomous Shuttles and Delivery Bots

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Automotive Conformal Coatings Market

- Henkel AG & Co. KGaA

- Dow Inc.

- Chase Corporation

- H.B. Fuller Company

- Shin-Etsu Chemical Co., Ltd.

- 3M Company

- Electrolube

- Dymax Corporation

- ELANTAS Electrical Insulation

- Illinois Tool Works Inc.

- MG Chemicals

- Kisco Ltd.

- Nordson Corporation

- Huitian New Materials

- Peters Group

*- List not Exhaustive

Table of Contents: Automotive Conformal Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Automotive Conformal Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Automotive Conformal Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Market Drivers: Vehicle Electrification and PCB Protection Requirements

2.4. Technology Evolution: UV-Curable, Silicone-Based, and Nano-Coatings

2.5. Regulatory and Safety Landscape: Functional Safety Standards and Low-VOC Transition

3. Innovations Reshaping the Automotive Conformal Coatings Market

3.1. Trend: UV-Cure and Dual-Cure Technologies Enabling High-Speed Manufacturing

3.2. Trend: High-Temperature Silicone and Nano-Coatings for EV Power Electronics

3.3. Opportunity: Advanced Coatings for LiDAR, ADAS, and Autonomous Systems

3.4. Opportunity: Semiconductor Ecosystem Expansion and High-Reliability Coating Demand

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Automotive Conformal Coatings Market

5.1. By Material Chemistry

5.1.1. Acrylic Resins (AR)

5.1.2. Silicone Resins (SR)

5.1.3. Polyurethane

5.1.4. Epoxy Resins (ER)

5.1.5. Parylene (XY)

5.1.6. Specialty Hybrid and Nano-Coatings

5.2. By Coating Technology

5.2.1. UV-Cured (Ultraviolet)

5.2.2. Heat-Cure

5.2.3. Solvent-borne

5.2.4. Moisture-Cured

5.2.5. Vapor Deposition

5.3. By Application Method

5.3.1. Selective Robotic Spraying

5.3.2. Automated Dipping

5.3.3. Manual and Automated Brushing

5.3.4. Aerosol and Needle Dispensing

5.4. By Automotive Component

5.4.1. ECUs and Control Modules

5.4.2. EV Battery Management Systems (BMS)

5.4.3. ADAS and Sensor Suites

5.4.4. Infotainment and Connectivity

5.4.5. Interior Electronics

5.4.6. Power Electronics

5.5. By Vehicle Type

5.5.1. Passenger Vehicles

5.5.2. Light Commercial Vehicles (LCVs)

5.5.3. Heavy Commercial Vehicles (HCVs)

5.5.4. Autonomous Shuttles and Delivery Bots

6. Country Analysis and Outlook of Automotive Conformal Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Automotive Conformal Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Automotive Conformal Coatings Market Size Outlook to 2032

7.1.1. By Material Chemistry

7.1.2. By Coating Technology

7.1.3. By Application Method

7.1.4. By Automotive Component

7.1.5. By Vehicle Type

7.2. Europe Automotive Conformal Coatings Market Size Outlook to 2032

7.2.1. By Material Chemistry

7.2.2. By Coating Technology

7.2.3. By Application Method

7.2.4. By Automotive Component

7.2.5. By Vehicle Type

7.3. Asia Pacific Automotive Conformal Coatings Market Size Outlook to 2032

7.3.1. By Material Chemistry

7.3.2. By Coating Technology

7.3.3. By Application Method

7.3.4. By Automotive Component

7.3.5. By Vehicle Type

7.4. South America Automotive Conformal Coatings Market Size Outlook to 2032

7.4.1. By Material Chemistry

7.4.2. By Coating Technology

7.4.3. By Application Method

7.4.4. By Automotive Component

7.4.5. By Vehicle Type

7.5. Middle East and Africa Automotive Conformal Coatings Market Size Outlook to 2032

7.5.1. By Material Chemistry

7.5.2. By Coating Technology

7.5.3. By Application Method

7.5.4. By Automotive Component

7.5.5. By Vehicle Type

8. Company Profiles: Leading Players in the Automotive Conformal Coatings Market

8.1. Henkel AG & Co. KGaA

8.2. Dow Inc.

8.3. Chase Corporation

8.4. H.B. Fuller Company

8.5. Shin-Etsu Chemical Co., Ltd.

8.6. 3M Company

8.7. Electrolube

8.8. Dymax Corporation

8.9. ELANTAS Electrical Insulation

8.10. Illinois Tool Works Inc.

8.11. MG Chemicals

8.12. Kisco Ltd.

8.13. Nordson Corporation

8.14. Huitian New Materials

8.15. Peters Group

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures