Market Overview: Benzene Toluene Xylene Market Growth Path Anchored in Integrated Aromatics and Derivative Relocation (2025–2034)

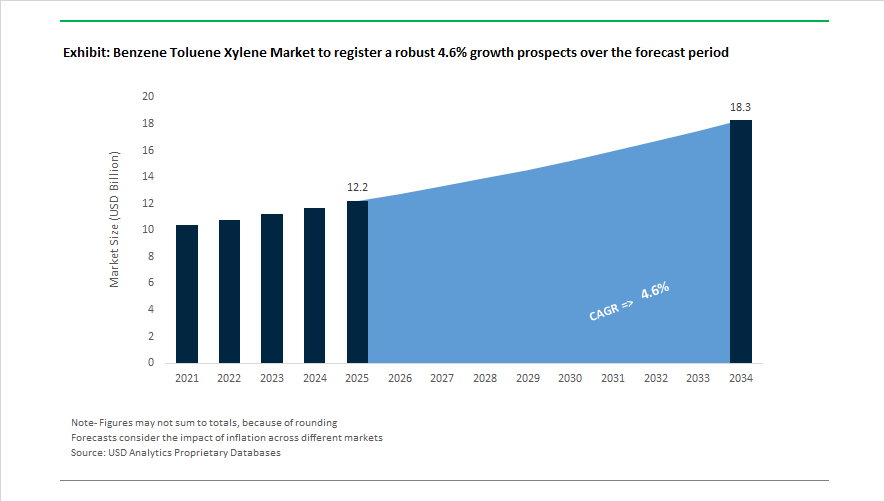

The benzene toluene xylene market is projected to expand from USD 12.2 billion in 2025 to USD 18.3 billion by 2034, reflecting a CAGR of 4.6% driven by paraxylene, mixed xylene, and benzene derivative demand across polyester fibers, PET packaging, synthetic resins, fuel blending components, and aroma chemicals. BTX aromatics remain foundational petrochemical intermediates linking refinery reformate streams with high-value downstream chains such as PTA, PET, styrene, phenol, engineering plastics, and specialty fragrance ingredients. Structural shifts began intensifying in 2024 when Indorama Ventures shut PTA and PET assets in Rotterdam, signaling economic pressure on European aromatics manufacturing. In October 2024, Givaudan and Privi Speciality Chemicals started operations at their Mahad plant in India, using toluene and benzene derivatives for complex fragrance molecules, reinforcing India’s role in value-added BTX downstream processing. During 2025, Rongsheng Petrochemical commissioned the next phase of its mega integrated refinery-petrochemical complex, optimizing paraxylene and ethylene co-production and lowering energy intensity in aromatics extraction.

Derivative production is relocating toward energy-advantaged regions and integrated hubs. In January 2026, Germany’s MAK Group agreed with OQ to transfer repurposed PTA and PET equipment to Sohar Port under a $550 million project backed by long-term paraxylene supply, formalizing a major shift of xylene derivative capacity from Europe to the Middle East. Feedstock security developments are supporting this transition. BP Trinidad and Tobago confirmed new upstream gas deliveries beginning April 2026 to stabilize thermal energy and feedstock supply for Caribbean petrochemical production. Chinese expansions continue to influence supply balances. Sinopec Zhongyuan Petrochemical plans to add 600,000 mt per year of high-purity aromatics capacity in 2026, while Zhenhua Petrochemical is preparing to commission a 660,000 mt per year MTBE unit in 2026, intensifying competition between aromatics streams and oxygenates for gasoline blending economics. In March 2024 through 2026, BASF advanced a citral production investment at its Zhanjiang Verbund site, relying on benzene-derived intermediates to serve expanding Asia-Pacific flavors and fragrance demand.

Regulation, financial instruments, and downstream consolidation are reshaping market dynamics. In June 2025, China launched benzene futures and options on the Dalian Commodity Exchange, providing localized hedging tools for aromatics price volatility management. In July 2025, the U.S. FDA established a strict 2 ppm benzene contamination limit for pharmaceuticals, driving adoption of ultra-high-purity benzene grades and improved solvent recovery technologies. Specialty chemical innovation continues. Solvay introduced Eugenol Synth during 2024 to 2025, supplying high-purity synthetic eugenol derived from aromatic feedstocks for fragrance applications. Downstream consolidation is also visible. In January 2026, private equity firm Clayton, Dubilier & Rice completed acquisition of Sealed Air, a major consumer of xylene-derived polyester materials, signaling tighter supply chain integration across BTX derivative demand centers.

Trends and Opportunities Reshaping the Benzene Toluene Xylene Market

Market Trend: Geopolitical Sanctions Reshaping Global BTX Price Equilibrium

The Benzene Toluene Xylene Market is experiencing a structural recalibration driven by sanctions, supply-chain vulnerability, and refinery contraction. The enforcement of the EU’s 14th–19th sanctions packages throughout 2025 has altered benzene trade flows, shifting Europe from a traditionally high-cost sourcing basin to the world’s lowest-priced region. In the Amsterdam–Rotterdam–Antwerp hub, benzene spot prices averaged approximately USD 660 per metric ton in September 2025, about USD 50 lower than equivalent U.S. and Northeast Asian benchmarks. This decline stems from a 6% year-over-year contraction in European refinery output paired with weakened demand for styrene and cyclohexane derivatives.

Real-world logistics constraints are magnifying this regional imbalance. Freight rates rose by nearly 20% during 2025 due to persistent Red Sea transit reroutes and drought-driven Panama Canal restrictions. These maritime bottlenecks effectively shut the transatlantic arbitrage window, leaving European suppliers at disadvantageous margins and absorbing losses ranging between USD 5 and USD 15 per ton on traditional exports to the U.S. Gulf Coast. This geopolitical and logistical convergence signals that BTX pricing will remain regionally fragmented rather than converging toward pre-2023 global averages.

Market Trend: Maximizing Para-Xylene Yield through Selective Conversion Technologies

Strategic de-bottlenecking and refinery optimization are now central to improving BTX margin pools. Integrated aromatics producers are deploying technologies such as Toluene Disproportionation (TDP), Selective TDP (STDP), and advanced xylene isomerization to convert lower-value toluene and mixed xylenes into Para-Xylene (PX), the high-demand feedstock essential for polyester and PET production.

China is setting the global benchmark for scale. As of May 2025, national PX capacity rose to approximately 47 million tonnes per year, anchored by mega-refining complexes that utilize catalyst systems with shorter reaction cycles and higher PX selectivity. These scale advantages allow Chinese producers to sustain competitive margins even during periods of volatile naphtha feedstock costs. Upgrades in Japan and South Korea underscore the shift toward digitally assisted aromatics operations; in 2025, AI-driven monitoring improved oxidation efficiency by up to 12% and reduced emissions by 18 percent, aligning with regional mandates targeting refinery decarbonization.

Market Opportunity: Toluene Positioned as a Critical Aromatic Component for Sustainable Aviation Fuel

Toluene offers a high-value growth path in the Sustainable Aviation Fuel landscape. As countries move toward volume-mandated SAF blending, refiners must boost aromatic content to satisfy ASTM D7566, which requires minimum aromatic levels for elastomer swell and fuel systems integrity.

Because HEFA-SPK (Hydroprocessed Esters and Fatty Acids) fuels contain less than 0.5% aromatics, toluene is emerging as the preferred additive to achieve the required 8% aromatic threshold. The UK has legislated a 10% SAF mandate by 2030, and India initiated a 1% SAF blending requirement in 2025, positioning toluene as a supply-critical molecule in early-stage aviation decarbonization. A June 2025 performance study further validated its importance by demonstrating that alkylbenzenes deliver an average o-ring swell of 4.8% v/v, preventing fuel leakage in legacy aircraft fleets. This technical necessity makes toluene a bridging molecule that enables airlines and refiners to comply with sustainability rules while transitioning toward 100% synthetic kerosene solutions.

Market Opportunity: Ortho-Xylene Gains Traction as a Growth Engine for High-Performance Plasticizers

Ortho-Xylene is experiencing a profitability rebound driven by its downstream link to Phthalic Anhydride (PA), now used in emerging non-phthalate and bio-based plasticizer grades for automotive and construction. In 2025, Ortho-Xylene profits averaged 296 RMB per ton, peaking at 1,190 RMB per ton in Q2. This resurgence reflects a favorable "scissors gap" where raw material pricing declined sharply while export-oriented PA demand remained resilient, particularly in India’s infrastructure market.

EV lightweighting requirements are enhancing long-term demand stability. Flexible PVC compounds used in cable insulation and interior trims increasingly depend on PA-based high-performance plasticizers as automakers seek better weight-to-durability ratios. Regulatory scrutiny under the U.S. EPA’s 2025 TSCA evaluations is expected to accelerate a migration from legacy DINP and DIDP toward improved performance plasticizers, securing Ortho-Xylene’s relevance in future automotive polymer formulations.

Benzene, Toluene, Xylene (BTX) Market Share and Segmentation Insights

Market Share by Application: Chemical Intermediates Anchor BTX Value Chains Across Polymers and Fibers

Chemical intermediates account for 41% of BTX consumption in 2025, positioning this segment as the structural backbone of the global Benzene, Toluene, Xylene market. Benzene is primarily converted into ethylbenzene for styrene, cumene for phenol, and cyclohexane for nylon, underpinning demand from polystyrene, polycarbonate, and engineering plastics. Toluene feeds TDI production for polyurethanes, while xylene is upgraded into paraxylene for polyester and orthoxylene for phthalic anhydride. Gasoline blending represents a significant secondary outlet, particularly for toluene and mixed xylenes due to their high octane ratings, although volumes remain highly price-sensitive versus petrochemical margins. Polymers and synthetic fibers form another major demand pillar, led by polyester from PX and nylon from benzene derivatives. Solvents and diluents remain stable, while paints, coatings, and adhesives face gradual substitution pressure from VOC regulations.

Market Share By Application, 2025.png)

Market Share by End Use Industry: Packaging and Mobility Applications Sustain Volume-Led Growth

Packaging leads BTX end-use consumption with a 32% share in 2025, driven by polyester in PET bottles, trays, and films, alongside polystyrene used in food service containers and protective packaging. Continued e-commerce expansion supports both rigid and flexible packaging demand. Automotive and transportation remains a critical downstream sector, consuming BTX derivatives in nylon engine components, ABS interior trims, styrene-butadiene rubber for tires, and fuel system materials, with EV adoption reshaping material mixes while preserving aggregate volumes. Construction and infrastructure utilize BTX in EPS and XPS insulation, PVC plasticizers derived from orthoxylene, sealants, and flooring, closely tracking non-residential building activity. Consumer electronics relies on ABS and polycarbonate for housings and enclosures, balancing miniaturization with higher performance polymers. Pharmaceuticals and agrochemicals represent lower-volume but premium segments, requiring high-purity BTX isomers for APIs and crop protection intermediates.

China Benzene Toluene Xylene Market: Capacity Discipline, Self-Sufficiency, and Digitalized Aromatics

China’s Benzene Toluene Xylene industry is being reshaped by a coordinated policy framework that prioritizes stabilization, self-sufficiency, and higher-value downstream integration. In late September 2025, the Ministry of Industry and Information Technology and six other ministries released a joint Work Plan targeting an average annual growth of 5% in petrochemical added value through 2026. This plan places aromatics at the center of industrial upgrading, linking BTX output to advanced materials and strategic manufacturing priorities.

Supply-side integration has progressed rapidly. By late 2025, China’s integrated complexes reached 11.8 million tonnes per year of combined benzene and paraxylene capacity, explicitly designed to reduce reliance on Northeast Asian imports and stabilize domestic styrenics and polyester chains. The government has further committed RMB 800 billion in new material investments by 2026, channeling BTX streams into high-purity electronic chemicals and high-end polyolefins. To manage a projected ethylene surplus of 11.5 million tonnes in 2025, authorities are strictly regulating new paraxylene capacity while steering aromatics toward high-end applications supporting the low-altitude economy and humanoid robotics. Complementing these measures, the national AI plus petrochemicals initiative launched in late 2025 is accelerating digital upgrades across aromatics plants, optimizing catalytic reforming efficiency while cutting energy intensity and carbon emissions.

Competitive Landscape Analysis of the Benzene Toluene Xylene Market

The Benzene Toluene Xylene market is entering a structurally transformative phase, driven by refinery reconfiguration, on-purpose aromatics production, and deep downstream integration into PTA, PET, polyurethanes, and engineering plastics. Market leaders are shifting from gasoline-oriented reforming toward chemicals-only configurations that maximize BTX yields and margin capture. Competitive differentiation now hinges on catalytic reforming efficiency, toluene methylation technologies, crude-to-chemicals integration, and circular aromatics platforms. Sustainability, carbon capture integration, and mass-balance certified feedstocks are becoming critical procurement criteria for automotive, electronics, packaging, and specialty chemicals sectors across North America, Asia-Pacific, Europe, and the Middle East.

Sinopec Group accelerates aromatic self-sufficiency through chemicals-only refining

Sinopec Group remains the global volume leader in the Benzene Toluene Xylene market, prioritizing China’s aromatic self-sufficiency strategy. In 2026, Sinopec Zhongyuan Petrochemical is set to add 600,000 mt per year of MTBE and aromatics-related capacity to reduce domestic supply gaps. The company is expanding its Zhanjiang and Gulei integrated complexes as primary Asia-Pacific hubs for high-purity benzene and xylene. Strategically, Sinopec is converting select refineries into chemicals-only configurations, reducing gasoline output to maximize BTX yields for PTA and PET production. Next-generation catalytic reforming units underpin its 2026 roadmap to reduce aromatic import dependence.

Reliance Industries dominates merchant benzene exports and paraxylene integration

Reliance Industries operates the world’s largest single-location aromatic complex in Jamnagar, positioning itself as a premier merchant exporter of benzene globally. With combined benzene capacity of 1.4 MMTPA across Jamnagar, Hazira, and Vadodara, Reliance supplies key markets in the US, Europe, and the Middle East. The company ranks among the top global paraxylene producers and maintains 525 KTA of ortho-xylene capacity, supporting polyester fiber and fiberglass demand. In 2026, Reliance is showcasing RCAT-HTL technology that converts organic waste into renewable crude, enabling circular benzene production. Aromatics integration with its Green Energy Giga Complex strengthens wind and EV materials development.

ExxonMobil advances high-purity BTX with net-zero integrated hubs

ExxonMobil commands a leading position in high-purity benzene, toluene, and xylene production, focusing on high-value derivatives and carbon-efficient operations. Following full integration of Pioneer Natural Resources by 2026, ExxonMobil optimizes low-cost Permian feedstocks for BTX output at Baytown and Beaumont complexes. The company is executing a High-Value Solutions pivot, diverting benzene volumes into proprietary Proxxima thermoset resins that outperform traditional epoxies. ExxonMobil supplies premium toluene and xylenes for low-VOC automotive paints and specialty adhesives. Its 2026 strategy integrates carbon capture and storage at aromatics hubs to produce low-carbon benzene aligned with sustainable supply chains.

SABIC maximizes crude-to-aromatics value through methylation and circular platforms

SABIC, backed by Saudi Aramco feedstock strength, leads in crude-to-aromatics technology, bridging energy and materials value chains. Its portfolio includes SABIC Benzene, styrene monomer, and pygas, central to engineering plastics and polycarbonate production. In 2026, SABIC is deepening downstream integration by co-locating aromatic assets with PTA and PET facilities, capturing full value from benzene and xylene streams. The company is deploying advanced toluene methylation technology to convert lower-value toluene into paraxylene, maximizing profitability per carbon unit. Through its TRUCIRCLE initiative, SABIC is scaling chemical recycling to generate certified circular benzene from mixed plastic waste.

BASF transforms BTX into specialty chemicals through digital Verbund optimization

BASF leverages its Verbund integration model to convert BTX streams into thousands of high-value derivatives, reinforcing its specialty chemicals leadership. By 2026, its Zhanjiang Verbund site is emerging as a benchmark for smart aromatics-to-specialties production. In February 2026, BASF implemented a 200 dollar per metric ton TDI price increase across Asia-Pacific and MEAF, reflecting its strategy to capture higher polyurethane chain value. The company introduced near-zero SVOC dispersion technology for ultra-clean interior coatings. BASF’s new Digital Hub in Hyderabad utilizes AI to optimize global aromatics production flows, enhancing energy efficiency and real-time margin responsiveness.

Shell prioritizes selective BTX growth and bio-based integration

Shell is repositioning its Benzene Toluene Xylene portfolio toward selective growth, focusing on electronics, personal care, and medical-grade plastics. The company manufactures high-purity benzene, toluene, and mixed xylenes, with emphasis on polycarbonate and specialty resin applications in 2026. Following European refinery rationalization, Shell now concentrates BTX production at fully integrated chemical hubs aligned with polymer demand. Its global digital product-tracking systems provide detailed stewardship documentation for aromatic precursors. Strategically, Shell is expanding mass-balanced benzene volumes derived from bio-based feedstocks, enabling customers to claim renewable content in consumer goods and automotive components.

India Benzene Toluene Xylene Market: Mega-Projects, Policy Liberalization, and Feedstock Security

India’s BTX industry is entering an investment-led expansion phase underpinned by mega-project execution and regulatory recalibration. In January 2025, Adani Petrochemicals partnered with Indorama Resources to launch Valor Petrochemicals Ltd., initiating a USD 4.2 billion project in Gujarat with Phase I completion targeted for 2026. This complex is designed to strengthen India’s domestic aromatics base and reduce import exposure across benzene and xylene derivatives.

Infrastructure depth is expanding through oil-to-chemical integration. In April 2025, Haldia Petrochemicals Limited announced a USD 10 billion OTC project in Tamil Nadu, targeting 3.5 million metric tonnes per year of ethylene and propylene with significant aromatics yield by 2028–2029. Regulatory flexibility has improved market fluidity. In December 2025, the Department of Chemicals and Petrochemicals rescinded Quality Control Orders for six chemicals including paraxylene and toluene, easing domestic trade and manufacturing constraints. Policy reforms under the updated Oilfields Amendment Bill and HELP have expanded exploration acreage to 1 million square kilometers, improving long-term feedstock security for benzene production. These measures supported petrochemicals Gross Value Added of INR 2.12 lakh crore in FY 2024–2025, aided by investments in bio-refineries and hydrogen integration.

South Korea Benzene Toluene Xylene Market: Capacity Rationalization and Export Repositioning

South Korea’s BTX industry is navigating a deliberate contraction to restore competitiveness amid global oversupply. In November 2025, major producers including Lotte Chemical and HD Hyundai Chemical submitted restructuring plans to the government to cut naphtha-cracking capacity by up to 25 percent, equivalent to 2.7–3.7 million tonnes per year. This rationalization is intended to protect margins and redirect resources toward higher-value aromatics and R&D.

Macroeconomic impacts are acknowledged. The Bank of Korea projected a short-term production loss of KRW 6.7 trillion in 2026 due to restructuring, while emphasizing longer-term gains in technology competitiveness. Export orientation is shifting accordingly. The Korea Chamber of Commerce and Industry forecasts a 6.1% decline in petrochemical exports in 2026 as firms pivot away from commodity BTX toward specialty aromatic derivatives. Downstream resilience remains a stabilizer. South Korea’s automotive sector, a major consumer of benzene-based ABS and polyurethane, is projected to increase output by 1.2% in 2026 to 4.13 million units, partially offsetting chemical sector headwinds.

United States Benzene Toluene Xylene Market: Margin Pressure, Trade Frictions, and Feedstock Optimization

The United States BTX industry is contending with subdued operating rates and evolving trade dynamics while optimizing internal aromatics loops. North American ethylbenzene styrene monomer operating rates are forecast to remain between 48 and 60% in early 2026 due to weak export demand to Europe and elevated feedstock costs. At the same time, gasoline blending economics have turned favorable for aromatics. In late 2025, toluene and mixed xylenes saw increased demand as high-octane blendstocks to compensate for low-octane light naphtha in the U.S. gasoline export pool.

Process economics remain challenging for conversion units. Operating rates for selective toluene disproportionation are expected to stay low in 2026 as benzene price strength reflects tight supply rather than robust downstream demand, compressing margins. Trade policy has compounded pressures. Ongoing U.S. tariffs have increased costs for benzene traders, reducing imports from Europe and Asia and forcing domestic producers to maximize internal integration across reforming and aromatics extraction. This environment is reinforcing the United States’ role as a flexible supplier rather than a volume exporter of BTX commodities.

Saudi Arabia Benzene Toluene Xylene Market: International Pivot and Circular Aromatics Scaling

Saudi Arabia’s BTX strategy is shifting outward through international partnerships and selective domestic upgrades. In late 2025, Saudi Aramco announced a pivot toward international refining and chemical investments, prioritizing projects in China and South Korea while placing three domestic chemical projects on hold. This reflects a capital allocation strategy focused on proximity to demand growth and integrated downstream value.

Selective upgrades continue at home. In November 2025, Aramco and Sinopec signed a Venture Framework Agreement to expand the Yasref refinery in Yanbu with a new petrochemical complex aimed at enhancing BTX output. Sustainability is emerging as a differentiator. SABIC reported a 45% increase in net adjusted income in Q3 2025 and is scaling circularity-certified LNP ELCRES resins that use aromatics derived from chemical recycling, aligning BTX production with circular economy objectives.

Country-Level Strategic Snapshot: Benzene Toluene Xylene Industry

Benzene Toluene Xylene (BTX) Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Developments

|

|

China

|

Capacity discipline and value upgrading

|

5% growth plan, 11.8 mtpa BTX capacity, RMB 800 bn new materials, AI-driven plant optimization

|

|

India

|

Mega-project execution and feedstock security

|

Valor Petrochemicals, OTC investments, QCO withdrawal, exploration expansion

|

|

South Korea

|

Rationalization and specialty pivot

|

Naphtha capacity cuts, short-term output loss, export repositioning

|

|

United States

|

Margin management and internal optimization

|

Low SM rates, gasoline blending demand, tariff-driven import decline

|

|

Saudi Arabia

|

International expansion and circularity

|

Overseas investment pivot, Yasref upgrade, circular aromatics scaling

|

Benzene Toluene Xylene (BTX) Market Report Scope

Benzene Toluene Xylene Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.2 Billion

|

|

Market Size (2034)

|

$18.3 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product Type (Benzene, Toluene, Xylene), By Production Process (Catalytic Reforming, Steam Cracking, Toluene Disproportionation, Coal to Aromatics, Bio Based Pathways), By Application (Chemical Intermediates, Solvents and Diluents, Gasoline Blending, Polymers and Synthetic Fibers, Paints Coatings and Adhesives), By End Use Industry (Automotive and Transportation, Construction and Infrastructure, Packaging, Consumer Electronics, Pharmaceuticals and Agrochemicals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

China Petroleum and Chemical Corporation, Saudi Aramco, Exxon Mobil Corporation, BASF, Reliance Industries, PetroChina, LG Chem, Lotte Chemical, Chevron Phillips Chemical, Shell, TotalEnergies, LyondellBasell Industries, Mitsubishi Chemical Group, Enchem, Adani Petrochemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Benzene Toluene Xylene Market Segmentation

By Product Type

By Production Process

- Catalytic Reforming

- Steam Cracking

- Toluene Disproportionation

- Coal to Aromatics

- Bio Based Pathways

By Application

- Chemical Intermediates

- Solvents and Diluents

- Gasoline Blending

- Polymers and Synthetic Fibers

- Paints Coatings and Adhesives

By End Use Industry

- Automotive and Transportation

- Construction and Infrastructure

- Packaging

- Consumer Electronics

- Pharmaceuticals and Agrochemicals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Benzene Toluene Xylene Industry

- China Petroleum and Chemical Corporation

- Saudi Aramco

- Exxon Mobil Corporation

- BASF

- Reliance Industries

- PetroChina

- LG Chem

- Lotte Chemical

- Chevron Phillips Chemical

- Shell

- TotalEnergies

- LyondellBasell Industries

- Mitsubishi Chemical Group

- Enchem

- Adani Petrochemicals

*- List not Exhaustive