Market Overview: Bitumen Emulsifiers Market Growth Driven by Sustainable Asphalt Additives, Distribution Expansion, and Cold-Mix Technologies (2025–2034)

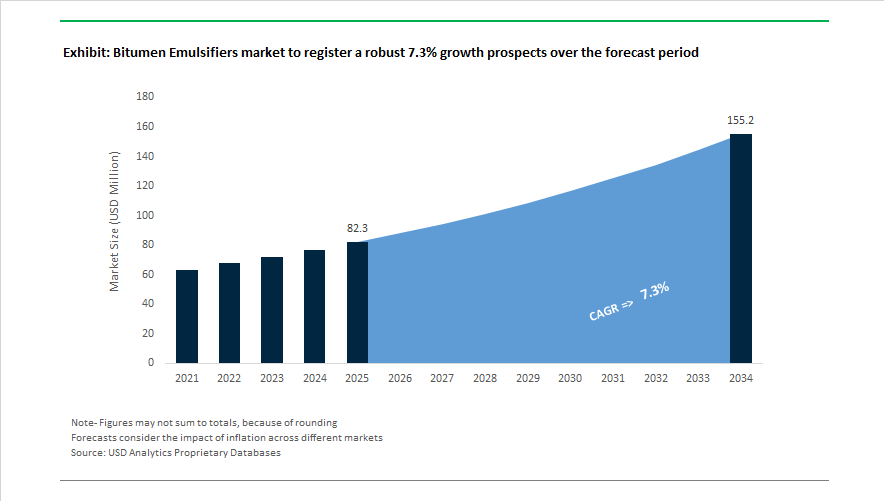

The bitumen emulsifiers market is projected to expand from USD 82.3 Million in 2025 to USD 155.2 Million by 2034, registering a CAGR of 7.3% supported by the global shift toward energy-efficient road construction, cold-mix asphalt technologies, and bio-based infrastructure materials. Market transformation began accelerating in February 2024 when Shrieve introduced the PROGILINE ECO-T range of organic asphalt additives for Europe, targeting carbon footprint reduction through bio-based emulsification. In April 2024, BASF launched EcoBind sustainable asphalt additives alongside new production investments to meet demand for low-energy emulsified bitumen paving systems. Distribution access widened in July 2024 when Nouryon partnered with Brenntag to enhance U.S. availability of bitumen emulsifiers and anti-stripping agents, reinforcing durability improvements in North American pavements.

Innovation in warm mix and application methods expanded through late 2024 and 2025. In December 2024, Sripath Technologies introduced PHALANX, a warm mix additive designed to reduce paving temperatures for polymer-modified bitumen, cutting emissions while preserving structural performance. IndianOil strengthened logistical efficiency in late 2024 by launching DURAPACK packaging that simplifies bitumen handling and emulsification at small-scale project sites. Market demand growth was highlighted in September 2025 when the Road Emulsion Association reported that encapsulation protection using bitumen emulsion covered one in four surface-dressed UK roads, reflecting increased adoption of high-performance emulsifiers. In July 2025, Gujarat Alkalies and Chemicals Limited began dispatching chlorotoluene-derived precursors essential for producing cationic emulsifiers, strengthening raw material supply for water-based asphalt technologies.

Strategic portfolio focus and industry alignment are shaping competitive direction. In November 2025, Evonik advanced its corporate restructuring under the Evonik Tailor Made program, affecting specialty monomer supply chains that feed emulsifier production. In January 2026, Ingevity completed the divestiture of its crude tall oil refinery and Industrial Specialties line, concentrating on its Road Technologies segment where bitumen emulsifiers represent a core growth area. The same month, Ingevity was recognized among America’s Most Responsible Companies, underscoring ESG alignment in cold-mix recycling technologies. Standardization efforts are also influencing product design. In January 2026, Eurobitume’s biomaterials terminology framework gained adoption across national road authorities, defining requirements for bio-based binders and emulsifiers. Collaboration expanded in September 2025 when PEAB Asfalt joined Eurobitume, promoting trials of polymer-modified emulsions engineered for climate resilience.

Trends and Opportunities Transforming the Bitumen Emulsifiers Market

Market Trend: Polymer-Modified Bitumen Emulsion (PME) Systems Become Central to Climate-Resilient Infrastructure

The Bitumen Emulsifiers Market is experiencing structural demand growth as road authorities adopt polymer-modified bitumen (PME) to withstand extreme temperature fluctuations, rutting, cracking, and heavy-axle loads. High-performance infrastructure targets have pushed elastomer-enhanced emulsions (SBS and crumb rubber) into mainstream specifications. In March 2025, Grampet Logistics in Romania launched a 480,000-ton-per-year polymerized bitumen facility operating four continuous production lines, signaling Europe’s shift toward industrial-scale PME manufacturing.

For emulsifier suppliers, the technical bottleneck lies not in polymer dispersion but in maintaining emulsion stability under long-haul transport and multiple climate zones. PME-40 grades accounted for over 47% of polymer-modified bitumen volumes in 2024 and require precision-engineered emulsifiers capable of preventing phase separation and “breaking” during storage. This is particularly critical in APAC, where PME road-laying demand is projected to reach 11.5 million tons in 2025, often transported across rural distances with limited temperature control and high moisture exposure.

Market Trend: Shift Toward Multifunctional Emulsifiers Integrating Set-Control and Anti-Stripping Performance

As contractors seek to simplify logistics and reduce on-site chemical handling, bitumen emulsifiers are evolving from single-purpose surfactants to multifunctional molecules. These integrated systems provide adhesion promotion, aggregate compatibility, set-time control, and water stripping resistance in a single package. Nouryon’s Redicote® and Wetfix® systems and Kao’s ASFIER solutions are shaping industry benchmarks by eliminating the need for post-addition chemical dosing at project sites.

A structural competency shift is occurring upstream, demonstrated by Kao Chemicals’ 2025 commissioning of a tertiary amine production facility in Texas designed to meet demand for precision-controlled QS (Quick-Setting) and SS (Slow-Setting) emulsifier formulations. These intermediates offer formulation engineers the ability to tune cohesion development and accelerate traffic reopening, aligning directly with urban demand for minimum downtime and rapid-return roadway projects. The market increasingly sees emulsifier performance as a productivity and cost-efficiency lever—not merely a chemical ingredient.

Market Opportunity: Cold Recycling and Full-Depth Reclamation Create Circularity and CAPEX Avoidance

The strongest monetizable opportunity in the Bitumen Emulsifiers Market lies in circular pavement technologies. CIR (Cold In-Place Recycling) and FDR (Full-Depth Reclamation) systems are becoming regulatory priorities, supported by GHG-reduction mandates and road-budget optimization programs. These techniques rely heavily on slow-setting emulsifiers to uniformly coat RAP (Reclaimed Asphalt Pavement) at ambient temperatures—making emulsifier selection a decisive factor between project failure and structural equivalence.

Kraton’s April 2025 Cirkular + Series (C5000) exemplifies where surfactant engineering meets climate policy. The solution enables contractors to lift RAP usage rates while minimizing binder drain-off. Academic findings published in the Journal of Transportation Engineering (September 2024) show that 10 cm cold-recycled layers can match the performance of 6 cm traditional HMA—only achievable when emulsifiers improve aggregate wetting, moisture resistance, and fatigue properties. Market expansion is therefore being framed not merely as volume growth, but also as a mechanism to defer CAPEX-heavy resurfacing cycles across North America, EU, and India.

Market Opportunity: High-Viscosity Emulsions Enable Porous Asphalt for Noise and Water Management

A growing infrastructure niche, “Quiet Roads,” is catalyzing demand for porous asphalt—open-graded, sound-absorbing pavements that reduce traffic noise and support rainwater infiltration. This segment requires high-viscosity emulsifiers engineered to bind aggregates without draining out of 18–24% void systems. Data from ICBE 2025 confirms that dual-layer porous asphalt can reduce roadway noise by up to 8 dB, enabling compliance with EU and urban environmental noise standards.

As governments in India (Roads 2047), Europe, and Japan adopt criteria linking road investments to climate resilience and liveability metrics, porous surfacing—combined with Micro-surfacing and PFC technologies—creates a durable growth runway for specialty emulsifiers. Suppliers positioned with binder-drainage-resistant, polymer-compatible surfactants stand to secure multi-year procurement pipelines as city planners transition from capacity-maximization to environmental performance design.

Bitumen Emulsifiers Market Share and Segmentation Insights

Market Share by Type: Cationic Emulsifiers Lead Through Superior Aggregate Adhesion

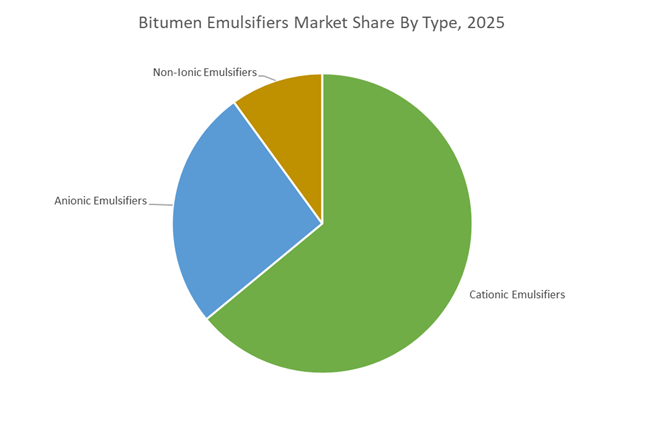

Cationic emulsifiers command 64% of the Bitumen Emulsifiers Market in 2025, owing to their ability to impart a positive charge to bitumen droplets, ensuring strong adhesion to negatively charged siliceous aggregates such as granite and quartzite. This enhances stripping resistance and accelerates setting times, making cationic slow-setting and rapid-setting grades standard in modern road construction. Fatty amines, imidazolines, and quaternary ammonium compounds dominate this chemistry class. Anionic emulsifiers hold the second-largest share, effective with positively charged limestone and calcareous aggregates, offering cost advantages and suitability for soil stabilization. Non-ionic emulsifiers represent the smallest segment, primarily functioning as co-emulsifiers to improve storage stability, viscosity control, and low-temperature performance. Growing adoption of polymer-modified bitumen emulsions is gradually expanding demand for advanced non-ionic systems.

Market Share by End Use Industry: Road Infrastructure Anchors Demand with Polymer-Modified Growth in Airports

Road construction and maintenance account for 72% of bitumen emulsifier consumption in 2025, supported by chip seals, slurry seals, micro-surfacing, fog seals, and cold mix asphalt applications. Preventive maintenance strategies and cold paving technologies, which reduce energy consumption and emissions, are accelerating adoption, reinforced by infrastructure spending in developing economies and rehabilitation programs in mature markets. Building and construction applications include damp-proofing, roofing membranes, and bridge deck waterproofing, with cationic emulsions preferred for vertical adhesion. Industrial flooring is a niche but expanding segment utilizing emulsions in heavy-duty screeds and anti-static surfaces for logistics facilities. Airport infrastructure remains specialized, requiring polymer-modified emulsions capable of withstanding high shear loads, jet fuel exposure, and extreme temperature cycles, with expansion projects in Asia-Pacific and the Middle East sustaining growth.

Competitive Landscape Analysis of the Bitumen Emulsifiers Market

The global bitumen emulsifiers market in 2026 is shaped by climate-resilient infrastructure mandates, warm-mix asphalt adoption, and decarbonization of road construction chemicals. Competitive dynamics center on cationic surfactant chemistry, cold in-place recycling technology, polymer-modified bitumen emulsions, and bio-based feedstocks. Infrastructure stimulus spending across North America, Europe, and Asia-Pacific is accelerating demand for high-performance asphalt emulsifiers optimized for microsurfacing, chip seals, and heavy-haul pavements. Leading suppliers are integrating digital formulation services, aggregate compatibility testing, and low-VOC systems to meet evolving ESG standards and federal transportation requirements.

Nouryon leads global asphalt emulsifier chemistry through Redicote innovation

Nouryon dominates asphalt chemicals with its Redicote platform, setting industry standards in cationic emulsifier performance. In 2026, Redicote E-7000 serves as a hybrid emulsifier compatible with both anionic and cationic systems, delivering stable, easy-to-handle emulsions. The patented Redicote C-320E, scaled in early 2026, supports night paving and cool-weather microsurfacing by accelerating cohesion development. Nouryon prioritizes climate-resilient infrastructure through emulsifiers designed for cold in-place recycling, enabling full pavement reuse on-site. Its global technical centers provide binder-aggregate compatibility testing, optimizing dosage for region-specific aggregates such as granite and limestone.

Ingevity expands bio-based warm-mix and cold-mix paving technologies

Ingevity leads with lignin-based chemistry derived from crude tall oil, supporting sustainable asphalt emulsifiers and Evotherm warm-mix technology. Following its 2025 Strategic Portfolio Update, the company prioritized its Pavement Technologies division to capitalize on US infrastructure spending initiatives. The EnvaMul series launched in 2026 enhances stability in high-float emulsions used for heavy-duty patching and cold-mix repairs. Operating from 24 global locations, Ingevity recently expanded Asia-Pacific technical teams to support green paving standards. Its bio-based adhesion systems outperform petroleum surfactants in durability, reinforcing leadership in sustainable road construction chemicals.

Arkema drives low-carbon micro-surfacing and smart emulsion solutions

Arkema positions itself as a specialty materials leader with ArrMuls and Polyram emulsifiers optimized for rapid-setting micro-surfacing applications. Under its Ambition 2028 strategy, Arkema transitioned its bitumen portfolio toward bio-sourced and low-carbon formulations. Through Stabiram technology, the company addresses storage stability challenges in polymer-modified bitumen emulsions. Its 2026 R&D focuses on low-VOC emulsifiers that eliminate solvent-based cutback bitumen, aligning with global environmental regulations. Arkema collaborates directly with emulsion plants to implement smart manufacturing workflows, enhancing urban road maintenance performance and decarbonized infrastructure systems.

Kao Corporation optimizes vegetable-based asphalt emulsifiers for rapid traffic return

Kao Chemicals leads the Asia-Pacific asphalt emulsifier market with fatty amine-derived surfactants under the ASFIER series. ASFIER N480L delivers broad aggregate compatibility, ensuring consistent mixing across diverse mineral sources. Newly introduced ASFIER 113 and 121 provide ultra-fast breaking times, allowing tack coats and chip seals to reopen to traffic within minutes. Kao’s vegetable-based feedstock capability supports the growing bio-bitumen trend in Europe and Japan. In 2026, the company emphasizes optimized emulsion viscosity and disintegration control, customizing surfactant chemistry to regional cement and filler compositions.

BASF integrates polymer-modified emulsions with digital formulation services

BASF leverages its Verbund integration to internally produce amine and ethylene precursors for emulsifiers, ensuring cost stability during petrochemical volatility. In Q1 2026, BASF opened a Global Digital Hub in Hyderabad to provide AI-driven bitumen emulsion formulation optimization. Its near-zero SVOC dispersion technology improves occupational safety during tunnel waterproofing applications. BASF leads in polymer-modified emulsions, supplying cross-linking additives for airport runways and heavy-haul logistics lanes. Digitalized recipe optimization enhances consistency and performance across global construction chemical markets.

Evonik Industries enhances asphalt durability with specialty effect additives

Evonik focuses on high-value effect additives and polybutadiene modifiers that improve asphalt elasticity and low-temperature crack resistance. In 2026, capacity expansion for POLYVEST ST-E 60 supports polymer-modified bitumen applications. The company streamlined North American distribution, appointing regional partners for faster asphalt additive support. Evonik’s Custom Solutions segment co-develops smart pavement coatings and sound-dampening additives for urban infrastructure. Meeting financial guidance in 2025 and introducing a dynamic dividend policy in 2026 has enabled reinvestment into next-generation bio-based surfactants for sustainable construction and coatings markets.

India Bitumen Emulsifiers Market: Net-Zero Road Policy and Rapid-Repair Economics Drive Emulsifier Uptake

India has emerged as one of the most policy-driven markets for bitumen emulsifiers, with sustainability and speed of execution now central to road construction strategy. In June 2025, the Ministry of Road Transport and Highways formally positioned bitumen emulsion technologies as a cornerstone of “Vision 2047,” aligning road development with the country’s long-term net-zero construction ambition targeted for 2070. This policy signal has accelerated adoption of cold-applied emulsions across national highways, urban roads, and state corridors, particularly where energy-efficient construction methods are prioritized.

Demand dynamics reinforced this shift in 2025. Industry assessments from August recorded a 47% year-on-year rise in bitumen consumption, translating into sharply higher demand for specialized cationic emulsifier grades comparable to VG30 and VG40 for post-monsoon resurfacing. With road infrastructure projects generating an estimated 6.5 billion mandays of employment by mid-2025, contractors increasingly favor emulsifier-intensive “quick-fix” technologies that enable rapid reopening of urban roads without high-temperature mixing. Technical validation has further strengthened confidence. In June 2025, the CSIR-Central Road Research Institute, working with Nouryon, published a landmark laboratory study confirming the durability of bituminous emulsions in Cold Recycling Technology for high-traffic pavements. Import dependence remains a strategic consideration, with around 40% of bitumen still sourced from overseas markets in late 2025, opening a clear pathway for localized emulsifier manufacturing to stabilize supply chains. At the state level, Rajasthan’s infrastructure corridor has become a visible adoption hub, where contractors are switching to emulsions to avoid the energy intensity and emissions associated with hot-mix asphalt.

China Bitumen Emulsifiers Market: Environmental Governance and Digital Quality Control Reshape the Supply Base

China’s bitumen emulsifiers industry is undergoing a structural transformation anchored in environmental governance and industrial consolidation. In the second half of 2025, authorities introduced a stricter environmental approval regime for bitumen modification plants, mandating closed-system blending and advanced emissions controls for polymer additives and emulsifiers. This regulatory tightening has raised entry barriers and effectively eliminated smaller, non-compliant producers from the market.

As a result, supply is concentrating among large-scale manufacturers capable of meeting Domestic Environmental Governance certification standards. This consolidation has coincided with renewed investment in localized innovation. In November 2025, Nouryon opened a dedicated innovation center in Shanghai to tailor emulsifier chemistries for China’s high-speed highway specifications, where consistency and long-term performance are critical. Environmental compliance is also becoming a commercial differentiator abroad. Chinese suppliers that secured approvals in 2025 are leveraging this status to win infrastructure contracts in Southeast Asia and the Middle East, where sustainability criteria are increasingly embedded in tenders. In parallel, major provinces began mandating digital tracking of bitumen emulsion quality in 2025, linking chemical batch data directly to national infrastructure durability monitoring systems. This integration of smart infrastructure with chemical inputs is redefining quality assurance expectations for emulsifier suppliers.

United States Bitumen Emulsifiers Market: Cold Recycling Incentives and Portfolio Rationalization

In the United States, the bitumen emulsifiers market is shaped by federal recycling incentives, safety regulation, and strategic portfolio realignments among specialty chemical producers. In December 2025, Ingevity Corporation announced a strategic pivot following a comprehensive portfolio review, signaling a sharper focus on high-margin performance chemicals, including advanced bitumen additives, while exploring alternatives for lower-growth segments such as road markings.

Policy momentum is reinforcing emulsifier demand. Under the 2025–2026 infrastructure funding cycles, the U.S. Department of Transportation introduced enhanced incentives for Cold-In-Place Recycling. This method relies heavily on high-stability cationic emulsifiers to reuse 100% of existing pavement, reducing material transport and lifecycle emissions. Innovation is also advancing on the sustainability front. In 2025, Arkema and Dow launched bio-sourced bitumen additives and polymer-modified emulsions engineered to maintain adhesion under extreme weather conditions prevalent in the Midwest and Gulf Coast. Workforce safety is accelerating the transition as well. New 2025 OSHA guidelines aimed at reducing exposure to hot asphalt fumes have encouraged wider adoption of emulsion-based cold mixes, eliminating the burn risks associated with 150°C hot-mix applications.

Germany and the European Union Bitumen Emulsifiers Market: Decarbonization Accounting and Regulatory Streamlining

Across Germany and the wider European Union, the bitumen emulsifiers industry is increasingly defined by regulatory clarity and carbon accounting. The EU Omnibus VI package, enforced through 2025, streamlined classification and labeling requirements under REACH and CLP, directly affecting how isothiazolinone-based preservatives in bitumen emulsions are marketed and documented. This has reduced administrative friction while maintaining strict safety thresholds.

Decarbonization is emerging as a procurement lever. From July 2025, BASF began offering Product Carbon Footprint statements for its Butonal® dispersions, enabling road contractors to quantify CO2 savings per kilometer paved using emulsion-based systems. Manufacturing footprints are also evolving. In August 2025, Nouryon completed a renewable energy integration project at its Mons facility, using onsite wind and solar power to reduce Scope 2 emissions for surfactants and emulsifiers. Regulatory changes in waste handling are reinforcing local recycling. EU Regulation 2024/1157, enforced from January 2025, tightened cross-border hazardous waste shipment rules, incentivizing in-situ bitumen emulsion recycling of reclaimed asphalt rather than exporting waste for treatment.

Country-Level Strategic Snapshot: Bitumen Emulsifiers Industry

Bitumen Emulsifiers market County Level Snapshot

|

Country / Region

|

Strategic Orientation

|

Key 2025 Developments

|

|

India

|

Policy-led cold construction

|

Vision 2047 focus, 47% bitumen demand rise, CRRI validation, state-level adoption

|

|

China

|

Environmental compliance and digitization

|

Plant consolidation, Shanghai innovation center, digital quality tracking

|

|

United States

|

Recycling incentives and safety

|

CIR incentives, bio-based emulsions, OSHA-driven cold-mix shift

|

|

Germany / EU

|

Decarbonization and regulatory clarity

|

PCF disclosures, renewable manufacturing, tighter waste shipment rules

|

Bitumen Emulsifiers Market Report Scope

Bitumen Emulsifiers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$82.3 Million

|

|

Market Size (2034)

|

$155.2 Million

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Type (Cationic Emulsifiers, Anionic Emulsifiers, Non Ionic Emulsifiers), By Application Method (Surface Treatments, Paving Techniques, Recycling Applications, Cold Mix Asphalt), By Setting Rate (Rapid Setting, Medium Setting, Slow Setting, Quick Setting), By End Use Industry (Road Construction and Maintenance, Airport Infrastructure, Building and Construction, Industrial Flooring)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nouryon, Arkema, Ingevity Corporation, Evonik Industries, BASF, Kao Corporation, Croda International, Dow, Honeywell International, PetroChina, Sinopec Group, Shell, Chemoran, McAsphalt Industries, Industrial Quimica de Asfaltos

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bitumen Emulsifiers Market Segmentation

By Type

- Cationic Emulsifiers

- Anionic Emulsifiers

- Non Ionic Emulsifiers

By Application Method

- Surface Treatments

- Paving Techniques

- Recycling Applications

- Cold Mix Asphalt

By Setting Rate

- Rapid Setting

- Medium Setting

- Slow Setting

- Quick Setting

By End Use Industry

- Road Construction and Maintenance

- Airport Infrastructure

- Building and Construction

- Industrial Flooring

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bitumen Emulsifiers Industry

- Nouryon

- Arkema

- Ingevity Corporation

- Evonik Industries

- BASF

- Kao Corporation

- Croda International

- Dow

- Honeywell International

- PetroChina

- Sinopec Group

- Shell

- Chemoran

- McAsphalt Industries

- Industrial Quimica de Asfaltos

*- List not Exhaustive