Bituminous Paints Market Size and Growth Driven by Infrastructure Waterproofing and Corrosion Protection Demand

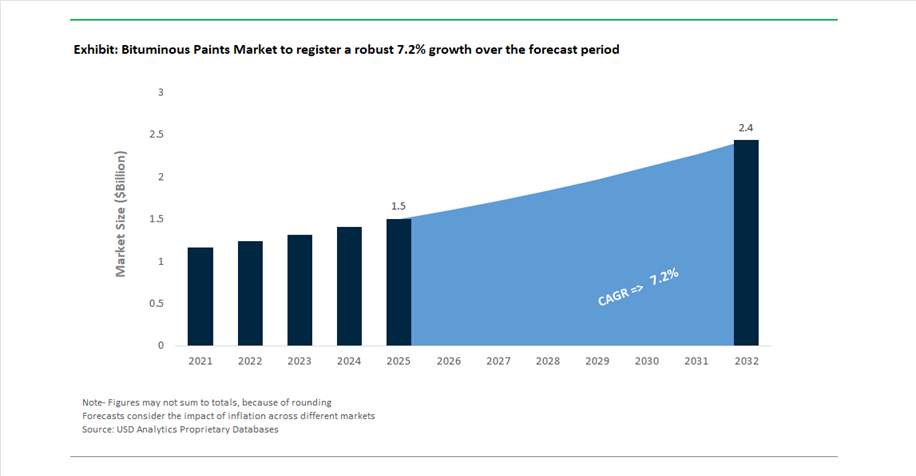

The Bituminous Paints Market is projected to grow from USD 1.5 billion in 2025 to USD 2.4 billion by 2032, registering a strong CAGR of 7.2%. This growth is primarily driven by the increasing need for durable waterproofing and corrosion protection solutions across large-scale infrastructure, marine, and underground construction projects.

Bituminous paints, derived from coal tar, asphalt, and pitch-based compounds, are widely recognized for their exceptional resistance to moisture, chemicals, and environmental degradation. These coatings are extensively used in roofing systems, foundation waterproofing, pipelines, storage tanks, bridges, and marine structures, where long-term protection against water ingress and corrosion is critical. Their ability to form thick, impermeable protective layers makes them particularly effective in harsh environments such as coastal regions, wastewater facilities, and buried infrastructure systems.

The market is benefiting from rising investments in transportation infrastructure, energy projects, and urban development, particularly in emerging economies where demand for cost-effective, high-performance protective coatings is increasing. Additionally, the growing focus on infrastructure longevity and lifecycle cost reduction is driving adoption of bituminous coatings in both new construction and maintenance applications.

Technological advancements are focused on improving flexibility, adhesion, and environmental compliance, with manufacturers developing low-VOC and modified bitumen formulations that maintain performance while reducing environmental impact. The integration of digital monitoring tools and predictive maintenance systems is also enhancing coating performance tracking in real-world conditions. Competitive dynamics are shaped by innovation in protective coating chemistry, strategic capacity expansion, and increasing alignment with sustainability standards, positioning bituminous paints as a key solution in global infrastructure protection strategies

Infrastructure Investments, Sustainable Formulation Innovation, and Strategic Consolidation Transforming Market Dynamics

The bituminous paints market is evolving through infrastructure-driven demand, sustainability-focused innovation, and strategic industry consolidation. Strategic investments in infrastructure are significantly boosting demand. Berger Paints India’s ₹2,500-crore expansion program (August 2024) highlights the growing requirement for bituminous coatings in rail, highway, and urban infrastructure projects, particularly in rapidly developing markets. Similarly, RPM International’s acquisition of Kalzip (January 2026) enables integration of bituminous moisture-barrier coatings into architectural metal systems, creating comprehensive solutions for roofing and structural protection.

Sustainability and regulatory compliance are increasingly influencing product development. Hempel prioritizes expansion in energy and infrastructure coatings, including bituminous solutions, while its 70% reduction in operational emissions (March 2026) reflects efforts to transition toward low-solvent, energy-efficient manufacturing processes. In parallel, RPM’s Innovation Center of Excellence is focusing on developing VOC-compliant bituminous coatings, addressing environmental concerns without compromising waterproofing performance.

Product innovation is also enhancing functional performance. Jotun’s industrial-grade bituminous coatings (October 2025) incorporate improved flexibility and thermal expansion resistance, ensuring durability in concrete structures exposed to temperature fluctuations. Additionally, PPG’s InsightsNav platform introduces digital monitoring capabilities, enabling real-time tracking of coating degradation and corrosion resistance in marine and infrastructure applications.

Corporate restructuring and strategic focus are shaping the competitive landscape. AkzoNobel’s divestment of its India business (December 2025) allows for increased focus on high-margin performance coatings, including bituminous anticorrosive solutions for water and wastewater infrastructure. Meanwhile, PPG’s $10 million investment in skilled trades training (March 2026) addresses the complexity of applying high-build bituminous coatings, ensuring proper installation and long-term performance.

EU REACH Restrictions on Coal Tar Pitch Driving Safer Bituminous Formulations

The bituminous paints industry is undergoing a decisive regulatory transition as the European Chemicals Agency enforces strict limitations on Coal Tar Pitch, High Temperature (CTPHT) under REACH. Classified as a Substance of Very High Concern due to its carcinogenic polycyclic aromatic hydrocarbon (PAH) content, CTPHT is being phased out across most consumer and professional coating applications, forcing a fundamental reformulation of traditional bituminous paints.

The regulatory thresholds are stringent. Coating formulations must now maintain PAH concentrations below 0.1% by weight, effectively eliminating coal tar-derived components from mainstream use. In parallel, new labeling requirements coming into force in October 2026 mandate clear hazard communication for coatings containing residual PFAS or PAHs above 1 mg/L, increasing compliance complexity for manufacturers.

This regulatory pressure has accelerated substitution strategies across the industry. More than 70% of legacy “black varnish” formulations have already been replaced with high-purity petroleum-derived bitumens and synthetic resin blends, which offer comparable adhesion and waterproofing performance while significantly reducing toxicological risks. At the production level, industrial operators have achieved measurable emission reductions, with German distillation facilities reporting a 40% decrease in Benzo(a)pyrene emissions compared to 2023 baselines.

This shift toward low-toxicity bituminous systems is redefining formulation strategies, positioning compliant, high-purity asphaltic coatings as the new industry standard while aligning with broader environmental and occupational safety regulations.

Waterborne Bituminous Emulsions Replacing Solvent-Based Systems in Waterproofing Applications

The transition toward waterborne bituminous emulsions represents one of the most significant technological shifts in the industry, driven by stringent VOC regulations such as SCAQMD Rule 1113 and the EU Industrial Emissions Directive. Traditional solvent-borne cutback bitumens are being rapidly replaced by cold-applied emulsion systems that offer improved safety, environmental compliance, and operational efficiency.

Performance parity has been achieved in modern formulations. Fast-set waterborne emulsions now allow for foundation backfilling within 24 to 48 hours, matching the application timelines of solvent-based systems while eliminating the need for heating or hazardous solvent evaporation. This has resulted in substantial energy savings, with contractors reporting a 15% reduction in on-site energy consumption due to the elimination of heating kettles.

Environmental benefits are even more pronounced. The adoption of water-based emulsions has enabled VOC emission reductions of approximately 85% to 90% at the project level, supporting compliance with green building standards and urban air quality regulations. Worker safety has also improved significantly. Industry data from 2025–2026 indicates a 60% reduction in respiratory incidents among applicators working in confined environments, such as basements and below-grade structures.

Low-PAH Bituminous Coatings Enabling Safe Drinking Water Infrastructure

The enforcement of the Revised Drinking Water Directive across the European Union is creating a high-value niche for low-PAH bituminous coatings designed for potable water infrastructure. These coatings must meet strict leaching standards to ensure that no harmful substances migrate into drinking water systems.

Advanced formulations are now engineered to pass EN 12873-1 leaching tests, maintaining total PAH migration levels below 0.10 μg/L. This ensures compliance with stringent water quality regulations while preserving the taste and odor neutrality of drinking water. These coatings are particularly relevant for protecting buried steel and ductile iron pipelines, where long-term corrosion resistance is critical.

From a lifecycle perspective, low-PAH bituminous coatings offer significant advantages. These systems can deliver service lives exceeding 50 years, reducing maintenance frequency and lowering total cost of ownership compared to some polymer-based alternatives. Additionally, the incorporation of inert mineral fillers enhances resistance to microbial growth, reducing the need for aggressive chemical disinfection within water distribution networks.

Regulatory harmonization under the Directive is also simplifying market access. Manufacturers offering certified low-PAH coatings are gaining streamlined entry into multiple European markets, creating a strong commercial incentive to develop compliant products.

Bituminous-Epoxy Hybrid Coatings Supporting Durability of Floating Solar Infrastructure

The rapid expansion of floating photovoltaic (FPV) systems is creating a new application frontier for bituminous coatings, particularly in marine and high-salinity environments. These installations require coatings that can withstand continuous exposure to water, UV radiation, and mechanical stress from wave action.

Bituminous-epoxy hybrid coatings are emerging as a high-performance solution in this segment. In accelerated testing conditions simulating marine environments, these coatings achieve corrosion resistance ratings equivalent to ASTM D1654 grade 9 after 4,000 hours of salt spray exposure, outperforming conventional epoxy systems by approximately 25%. This enhanced durability is critical for protecting metallic components such as pontoons and mooring structures.

Flexibility is another key advantage. The viscoelastic nature of bitumen allows these coatings to absorb mechanical stresses caused by wave-induced movement, preventing cracking and coating failure in dynamic environments. This makes them particularly suitable for floating infrastructure, where constant motion can degrade more rigid coating systems.

Recent formulation advancements have also improved UV resistance. The incorporation of micronized aluminum pigments enhances reflectivity, reducing surface degradation and preventing the chalking commonly associated with traditional bituminous coatings. These improvements translate into extended maintenance cycles, with FPV operators reporting up to a 20% increase in maintenance intervals.

Solvent-Borne Bituminous Paints Lead Market with 44% Share Driven by Cost Efficiency and Heavy-Duty Corrosion Protection

Form Analysis: Asphalt-Based Solvent-Borne Coatings Dominate Infrastructure and Industrial Applications

Solvent-borne bituminous paints account for a leading 44.0% share of the bituminous paints market in 2025, driven by their low cost, strong hydrophobic properties, and proven corrosion resistance in demanding environments. These coatings, formulated from asphalt, bitumen, or gilsonite dispersed in solvents like mineral spirits and xylene, cure through solvent evaporation to form a thick, flexible, water-resistant barrier. They are widely used in underground pipeline coatings, concrete foundation waterproofing, metal roofing, and automotive underbody protection, where durability outweighs aesthetic considerations. A key advantage is their 3x–5x lower cost compared to epoxy or acrylic coatings, making them the preferred choice in price-sensitive infrastructure markets across Asia, Africa, and Latin America. Additionally, bituminous aluminum coatings enhance UV resistance by reflecting solar radiation, extending service life in above-ground applications such as storage tanks and transmission structures, reinforcing their dominance in the industrial protective coatings market.

Infrastructure & Public Works Sector Leads Bituminous Paints Market with 36% Share Driven by Pipeline Protection and Waterproofing Demand

End-Use Industry Analysis: Buried Asset Protection and Trenchless Rehabilitation Fuel Market Growth

The infrastructure and public works segment holds a dominant 36.0% share of the bituminous paints market in 2025, driven by the need to protect extensive networks of buried and submerged assets, including water pipelines, sewer systems, culverts, and bridge decks. Bituminous coatings provide effective resistance against soil corrosion, moisture ingress, and chemical exposure, making them essential for long-term infrastructure durability. A major growth driver is the surge in global water infrastructure investments, supported by initiatives such as the U.S. Bipartisan Infrastructure Law and EU Green Deal. Additionally, the adoption of trenchless pipeline rehabilitation technologies, such as Cured-in-Place Pipe (CIPP) and spray-applied bituminous linings, is significantly boosting demand by enabling cost-effective pipeline restoration without excavation. These coatings extend asset life by 50+ years, reducing maintenance costs and downtime. Combined with their role in bridge waterproofing and foundation damp-proofing, infrastructure applications remain the primary growth engine in the global bituminous coatings market.

Bituminous Paints Market Competitive Landscape Driven by Infrastructure Protection, Waterproofing Technologies, and Polymer-Modified Coatings

The bituminous paints market is driven by rising demand for waterproof coatings, anti-corrosion coatings, and pipeline protection solutions. Key players are focusing on polymer-modified bituminous coatings, low-VOC formulations, and high-build protective systems to enhance durability, sustainability, and lifecycle performance across infrastructure and industrial applications.

RPM International leads bituminous coatings with fiber-reinforced waterproofing and MRO market dominance

RPM International is a major force in the bituminous paints market, supported by strong growth in its Performance Coatings segment contributing to 5% revenue growth in early 2026. Its Rust-Oleum 7300 range is widely used for waterproofing metal and concrete structures in the North American MRO market. The company introduced fiber-reinforced bituminous coatings that improve puncture resistance by 35%, enhancing below-grade protection. RPM’s diversified portfolio enables integration with Tremco roofing systems, offering full-envelope building protection solutions. Its Carboline brand strengthens its presence in heavy-duty industrial coatings. Product innovation focuses on durability, waterproofing efficiency, and infrastructure repair solutions.

AkzoNobel strengthens bituminous coatings leadership with maritime solutions and low-VOC innovations

AkzoNobel is a global leader in bituminous coatings, particularly in marine and industrial anti-corrosion applications. The company is progressing toward a major merger with Axalta, creating a $25 billion coatings entity with expanded R&D capabilities. Eco-friendly and low-VOC coatings now account for nearly 40% of its portfolio, including water-based bitumen systems. Its Interprime 160 series meets IMO standards for ballast tank protection, reinforcing its maritime leadership. Operating in over 150 countries, AkzoNobel improved supply chain efficiency by 10% through digital logistics. Product development focuses on sustainable coatings, corrosion protection, and global scalability.

Hempel advances bituminous coatings with high-solids formulations and energy-efficient production

Hempel is a key innovator in bituminous paints, achieving a record 18.2% EBITDA margin in 2026 through its strategic focus on infrastructure and energy sectors. The company launched Hempabit 313, a high-solids coating enabling single-coat applications up to 150 microns, reducing labor costs by 20%. Its modernization of production facilities has resulted in a 70% reduction in Scope 1 and 2 emissions. Growth in its Neogard division highlights rising demand for waterproofing and fire protection systems in urban infrastructure. Hempel’s strategy emphasizes efficiency, sustainability, and performance coatings. Product innovation focuses on cost-effective application and environmental compliance.

Jotun expands bituminous coatings footprint with tropicalized formulations and oil & gas infrastructure focus

Jotun is a leading player in bituminous paints across the Middle East and APAC regions, driven by strong infrastructure and energy sector demand. The company established a new production facility in Qatar to support pipeline and oil & gas projects. Its tropicalized bituminous coatings are engineered for extreme conditions, including high humidity and temperatures exceeding 50°C. The Jotabit range holds large market share in Southeast Asia for underground utility protection. Jotun integrates high-purity resins into both decorative and industrial coatings to ensure durability in harsh environments. Product development focuses on climate-resistant coatings and regional infrastructure growth.

BASF strengthens bituminous coatings value chain with polymer-modified binders and self-healing technologies

BASF plays a critical role in the bituminous paints market through its advanced polymer-modified binders and dispersion technologies. Expansion of its Mangalore facility supports production of Acronal resins used in flexible bituminous emulsions for construction applications. The company developed self-healing binders using micro-encapsulation technology, extending infrastructure coating lifespans by up to 15 years. BASF is targeting green infrastructure with bio-derived asphalt solutions that support net-zero construction goals. Its integrated value chain ensures consistent quality from raw materials to finished coatings. Product innovation focuses on durability, flexibility, and sustainable infrastructure solutions.

United States Bituminous Paints Market: Infrastructure Funding and PFAS-Free Transition Driving Growth

The United States bituminous paints market is experiencing strong growth, fueled by historic infrastructure investments and regulatory shifts. Under the $134 billion highway and bridge funding (2025–2026), the Federal Highway Administration is prioritizing high-build bituminous coatings for protecting bridge substructures, particularly in coastal regions exposed to corrosion. This is significantly increasing demand for durable, anti-corrosive coating systems.

Sustainability and innovation are also reshaping the market. The industry has transitioned over 90% of bituminous coatings to PFAS-free formulations, aligning with EPA directives. Urban initiatives such as cool pavement programs in Los Angeles are driving adoption of reflective bituminous coatings to reduce heat island effects. Additionally, advancements like nano-engineered primers with 30% higher adhesion are improving repair efficiency for aging infrastructure. Expansion of production capacity in Texas for modified membranes further supports demand in energy-efficient roofing applications.

China Bituminous Paints Market: Smart Infrastructure Integration and Waterborne Transition Driving Scale

China leads the global bituminous paints market in volume, driven by massive infrastructure development and smart city integration. The enforcement of GB 30981.1-2025 standards has triggered a 45% shift toward waterborne bituminous coatings, particularly for foundation waterproofing and underground structures.

Technological innovation is advancing rapidly. The integration of moisture-sensing layers in bituminous membranes for metro systems enables real-time leak detection, while titania-doped coatings are being deployed to neutralize NOx emissions in polluted regions. Infrastructure initiatives under the Belt and Road program are driving demand for anti-corrosive coatings in deep-foundation piles, and the adoption of high-dielectric bituminous layers is supporting smart highway electronics. Capacity expansions in cold-mix emulsions are further improving energy efficiency in application processes.

Germany Bituminous Paints Market: Bio-Based Surfactants and Circular Economy Driving Sustainability

Germany remains a global benchmark for sustainable bituminous coatings, driven by innovation in materials and strict environmental regulations. The introduction of bio-based cationic surfactants for bitumen emulsification is reducing environmental impact while maintaining high performance.

The market is also characterized by circular economy practices. The use of recycled asphalt pavement (RAP) in coatings (up to 15%) is reducing material waste, while investments in advanced production facilities are lowering carbon footprints. Innovations such as low-temperature cure (≈5°C) hybrid coatings are extending construction windows into colder seasons. Regulatory requirements, including VDI 6022 standards, are promoting biocide-free antimicrobial coatings in water infrastructure. Additionally, demand for UV-stable coatings in modular housing is expanding application scope, reinforcing Germany’s leadership in sustainable coatings.

India Bituminous Paints Market: Infrastructure Boom and Monsoon-Resistant Coatings Driving Rapid Growth

India is the fastest-growing market for bituminous paints, supported by large-scale infrastructure expansion and regulatory mandates. Projects under the National Infrastructure Pipeline and Bharatmala Pariyojana are driving demand for anti-carbonation bituminous coatings in thousands of culverts, underpasses, and transport systems.

Innovation is focused on climate resilience and cost efficiency. The introduction of water-based bituminous coatings is targeting residential construction in high-monsoon regions, while rubber-modified bituminous paints are improving crack resistance in airport and heavy-duty applications. Regulatory guidelines now mandate the use of high-performance coatings in underground water systems, further boosting demand. Additionally, the development of coal-tar-free alternatives is improving environmental compliance, positioning India as a high-growth market.

United Arab Emirates Bituminous Paints Market: Extreme Climate Solutions and Export Leadership Driving Expansion

The UAE is a global leader in extreme-temperature bituminous coatings, driven by large infrastructure projects and its role as a major bitumen exporter. Projects such as the Emirates Road expansion require high-temperature-resistant coatings compliant with AASHTO standards to withstand desert conditions exceeding 50°C.

The market is also advancing through innovation in cooling and durability. The adoption of light-reflective bituminous coatings is reducing surface temperatures by up to 10°C in urban environments, while high-solid epoxy-bitumen systems are extending service life for marine structures. Safety regulations are driving the use of intumescent additives for fire protection, and the transition to self-adhesive membranes is improving construction safety. These developments position the UAE as a leader in high-performance, climate-resilient bituminous coatings.

United Kingdom Bituminous Paints Market: Net-Zero Road Maintenance and Smart Coating Systems Driving Innovation

The United Kingdom is advancing toward net-zero infrastructure maintenance, supported by strong government investment and regulatory changes. Under the £27.4 billion Road Investment Strategy (RIS3), carbon-neutral bituminous emulsions have been standardized for road preservation projects.

Technological innovation is a key driver. The introduction of smart bituminous coatings with embedded moisture sensors is enabling predictive maintenance of aging infrastructure, reducing long-term costs. Regulatory updates under UK REACH have banned high-solvent coal tar coatings, accelerating the adoption of bio-solvent and low-VOC alternatives. Additionally, applications such as porous bituminous coatings for flood management (“Sponge Cities”) and polymer-modified bitumen for sewer refurbishment are expanding the market’s scope. These factors position the UK as a leader in sustainable and smart bituminous coating technologies.

Bituminous Paints Market Report Scope

Bituminous Paints Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2032)

|

$2.4 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Form (Solvent-Borne Bituminous Paints, Water-Borne, Bituminous Enamels, Polymer-Modified Bituminous Paints), By Substrate Compatibility (Concrete and Masonry, Metal and Steel, Wood and Timber, Existing Bituminous Surfaces), By End-Use Industry (Building and Construction, Infrastructure and Public Works, Oil, Gas and Mining, Marine and Shipbuilding, Transportation and Automotive), By Functional Specification (Thermal Resistant, Acid and Alkali Resistant Grade, UV-Stable, Rapid-Cure Systems)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Akzo Nobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Sika AG, BASF SE, RPM International Inc., Jotun A/S, Hempel A/S, TotalEnergies SE, Exxon Mobil Corporation, Nynas AB, Henkel Polybit Industries Ltd., Kansai Paint Co., Ltd., MC-Bauchemie Müller GmbH & Co. KG, Crown Paints

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bituminous Paints Market Segmentation

By Form

- Solvent-Borne Bituminous Paints

- Water-Borne

- Bituminous Enamels

- Polymer-Modified Bituminous Paints

By Substrate Compatibility

- Concrete and Masonry

- Metal and Steel

- Wood and Timber

- Existing Bituminous Surfaces

By End-Use Industry

- Building and Construction

- Infrastructure and Public Works

- Oil, Gas and Mining

- Marine and Shipbuilding

- Transportation and Automotive

By Functional Specification

- Thermal Resistant

- Acid and Alkali Resistant Grade

- UV-Stable

- Rapid-Cure Systems

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Bituminous Paints Market

- Akzo Nobel N.V.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Sika AG

- BASF SE

- RPM International Inc.

- Jotun A/S

- Hempel A/S

- TotalEnergies SE

- Exxon Mobil Corporation

- Nynas AB

- Henkel Polybit Industries Ltd.

- Kansai Paint Co., Ltd.

- MC-Bauchemie Müller GmbH & Co. KG

- Crown Paints

*- List not Exhaustive

Table of Contents: Bituminous Paints Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Bituminous Paints Market Landscape & Outlook (2025–2032)

2.1. Introduction to Bituminous Paints Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Market Drivers: Infrastructure Waterproofing, Corrosion Protection, and Urban Development

2.4. Regulatory Landscape: REACH Restrictions, VOC Compliance, and Environmental Standards

2.5. Technology Advancements: Modified Bitumen, Low-VOC Formulations, and Digital Monitoring

3. Innovations Reshaping the Bituminous Paints Market

3.1. Trend: Waterborne Bituminous Emulsions Replacing Solvent-Based Systems

3.2. Trend: Low-PAH and Coal Tar-Free Formulations for Safer Infrastructure Applications

3.3. Opportunity: Bituminous-Epoxy Hybrid Coatings for Floating Solar and Marine Infrastructure

3.4. Opportunity: Smart Coatings with Digital Monitoring and Predictive Maintenance Capabilities

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Bituminous Paints Market

5.1. By Form

5.1.1. Solvent-Borne Bituminous Paints

5.1.2. Water-Borne

5.1.3. Bituminous Enamels

5.1.4. Polymer-Modified Bituminous Paints

5.2. By Substrate Compatibility

5.2.1. Concrete and Masonry

5.2.2. Metal and Steel

5.2.3. Wood and Timber

5.2.4. Existing Bituminous Surfaces

5.3. By End-Use Industry

5.3.1. Building and Construction

5.3.2. Infrastructure and Public Works

5.3.3. Oil, Gas and Mining

5.3.4. Marine and Shipbuilding

5.3.5. Transportation and Automotive

5.4. By Functional Specification

5.4.1. Thermal Resistant

5.4.2. Acid and Alkali Resistant Grade

5.4.3. UV-Stable

5.4.4. Rapid-Cure Systems

6. Country Analysis and Outlook of Bituminous Paints Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Bituminous Paints Market Size Outlook by Region (2025–2032)

7.1. North America Bituminous Paints Market Size Outlook to 2032

7.1.1. By Form

7.1.2. By Substrate Compatibility

7.1.3. By End-Use Industry

7.1.4. By Functional Specification

7.2. Europe Bituminous Paints Market Size Outlook to 2032

7.2.1. By Form

7.2.2. By Substrate Compatibility

7.2.3. By End-Use Industry

7.2.4. By Functional Specification

7.3. Asia Pacific Bituminous Paints Market Size Outlook to 2032

7.3.1. By Form

7.3.2. By Substrate Compatibility

7.3.3. By End-Use Industry

7.3.4. By Functional Specification

7.4. South America Bituminous Paints Market Size Outlook to 2032

7.4.1. By Form

7.4.2. By Substrate Compatibility

7.4.3. By End-Use Industry

7.4.4. By Functional Specification

7.5. Middle East and Africa Bituminous Paints Market Size Outlook to 2032

7.5.1. By Form

7.5.2. By Substrate Compatibility

7.5.3. By End-Use Industry

7.5.4. By Functional Specification

8. Company Profiles: Leading Players in the Bituminous Paints Market

8.1. Akzo Nobel N.V.

8.2. PPG Industries, Inc.

8.3. The Sherwin-Williams Company

8.4. Sika AG

8.5. BASF SE

8.6. RPM International Inc.

8.7. Jotun A/S

8.8. Hempel A/S

8.9. TotalEnergies SE

8.10. Exxon Mobil Corporation

8.11. Nynas AB

8.12. Henkel Polybit Industries Ltd.

8.13. Kansai Paint Co., Ltd.

8.14. MC-Bauchemie Müller GmbH & Co. KG

8.15. Crown Paints

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures