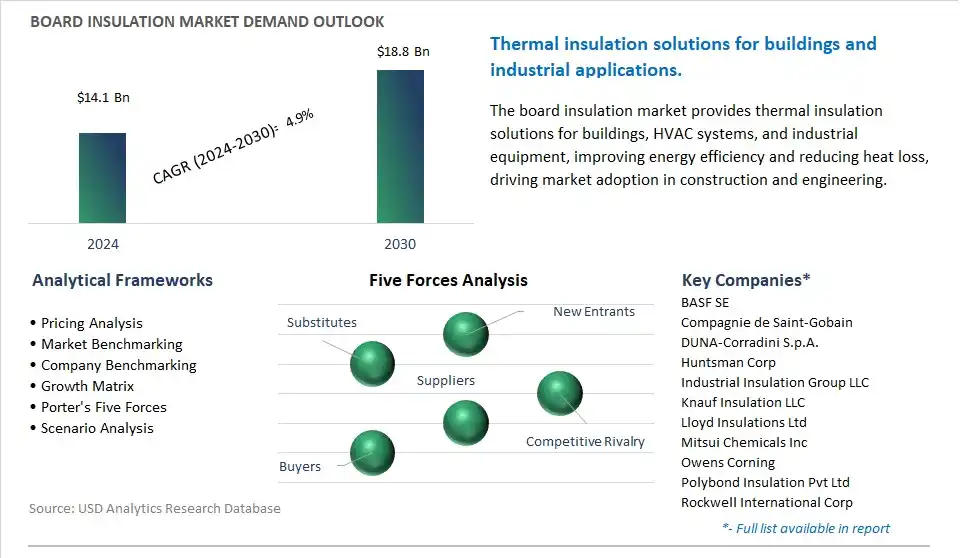

The global Board Insulation Market is poised to register a 4.9% CAGR from $14.1 Billion in 2024 to $18.8 Billion in 2030.

The global Board Insulation Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Application (Building & Construction, Transportation, Industrial, Others).

An Introduction to Global Board Insulation Market in 2024

The market for board insulation is improving energy efficiency and sustainability in buildings by offering effective thermal insulation solutions for walls, roofs, and floors. Key trends shaping the future of this industry include advancements in insulation materials, such as expanded polystyrene (EPS), extruded polystyrene (XPS), polyisocyanurate (PIR), and mineral wool, which provide superior thermal performance, moisture resistance, and fire protection properties. Additionally, developments in board insulation manufacturing processes, including continuous production methods and advanced bonding technologies, enhance product consistency, durability, and ease of installation. Moreover, the adoption of green building standards, energy codes, and sustainability certifications drives market demand for board insulation products that contribute to energy savings, indoor comfort, and environmental responsibility. As building owners, architects, and contractors prioritize energy-efficient building designs and compliance with environmental regulations, the demand for board insulation solutions is expected to grow, stimulating further innovation and market expansion in this vital sector of the construction industry.

Board Insulation Market Competitive Landscape

The market report analyses the leading companies in the industry including BASF SE, Compagnie de Saint-Gobain, DUNA-Corradini S.p.A., Huntsman Corp, Industrial Insulation Group LLC, Knauf Insulation LLC, Lloyd Insulations Ltd, Mitsui Chemicals Inc, Owens Corning, Polybond Insulation Pvt Ltd, Rockwell International Corp, Rogers Corp.

Board Insulation Market Dynamics

Board Insulation Market Trend: Increasing Emphasis on Energy Efficiency in Construction

A prominent trend in the market for board insulation is the increasing emphasis on energy efficiency in construction. With growing awareness of climate change and the need to reduce energy consumption, builders and homeowners are seeking ways to improve the thermal performance of buildings. Board insulation materials, such as rigid foam boards and fiberglass boards, offer effective thermal insulation, helping to reduce heat loss or gain through walls, roofs, and floors. As energy codes and regulations become more stringent and as consumers prioritize energy-efficient homes and buildings, the demand for board insulation is expected to rise, driving market growth and innovation in the construction industry.

Board Insulation Market Driver: Growth in Residential and Commercial Construction

A key driver behind the demand for board insulation is the growth in residential and commercial construction. Board insulation is widely used in both new construction and renovation projects for residential homes, commercial buildings, and industrial facilities. As populations grow, urbanization accelerates, and economies expand, there is an increasing need for housing, office space, retail centers, and industrial facilities. Board insulation materials play a critical role in meeting building code requirements, improving indoor comfort, and reducing energy costs for heating and cooling. As construction activity continues to increase globally, driven by factors such as population growth, urbanization, and infrastructure development, the demand for board insulation is expected to remain strong, driving market expansion and investment in building materials.

Board Insulation Market Opportunity: Development of High-Performance and Sustainable Insulation Solutions

An emerging opportunity in the market for board insulation lies in the development of high-performance and sustainable insulation solutions. Opportunities exist to innovate and optimize insulation materials and technologies to enhance thermal performance, durability, and environmental sustainability. Advanced insulation materials, such as aerogel-based boards, vacuum insulated panels (VIPs), and phase change materials (PCMs), offer superior insulation properties and thinner profiles compared to traditional insulation materials. Additionally, there is a growing demand for sustainable insulation solutions made from recycled content, renewable resources, or bio-based materials. By investing in research and development of advanced insulation technologies and collaborating with architects, builders, and energy consultants, manufacturers of board insulation can capitalize on new opportunities, differentiate their products in the market, and drive sustainable growth in the construction industry.

Board Insulation Market Ecosystem

The board insulation market involves diverse key stages, with raw material suppliers including Rockwool and Saint-Gobain, providing fibrous materials including mineral wool and natural fibers, along with chemical companies including BASF and Covestro supplying foam materials including Polyisocyanurate (PIR) or Polyurethane (PUR) foam. Additionally, metal manufacturers and plastics producers contribute facings including reflective foils or vapor barrier films.

Board insulation manufacturing is characterized by the presence of established insulation manufacturers including Knauf Insulation and Owens Corning, utilizing processes including felting, pouring, and lamination to create insulation boards with specific properties. Distribution and sales networks connect insulation manufacturers with building material distributors and contractors, facilitating the delivery of board insulation to construction projects. Installation, a crucial stage, involves trained professionals from insulation contractors or construction companies, ensuring proper installation to enhance thermal and acoustic performance in buildings.

Board Insulation Market Share Analysis: Building and Construction sector held the dominant revenue share in 2024

The largest segment in the Board Insulation Market is the Building and Construction sector, and diverse reasons contribute to its dominance. Firstly, building and construction projects are one of the primary consumers of board insulation due to the significant need for thermal and acoustic insulation in structures. Board insulation materials are widely used in residential, commercial, and industrial construction projects to improve energy efficiency, enhance occupant comfort, and meet regulatory requirements for insulation standards. Additionally, the growing trend toward sustainable construction practices has increased the demand for board insulation materials that offer high levels of thermal performance while minimizing environmental impact. Further, advancements in board insulation technology have led to the development of lightweight and easy-to-install products, making them preferred choices for builders and contractors. Overall, the building and construction sector holds the largest share in the Board Insulation Market due to its essential role in providing thermal comfort, energy efficiency, and sustainability in modern building projects.

Board Insulation Market Report Scope-

By Application

Building & Construction

Transportation

Industrial

Others

Board Insulation Market Companies Profiled

BASF SE

Compagnie de Saint-Gobain

DUNA-Corradini S.p.A.

Huntsman Corp

Industrial Insulation Group LLC

Knauf Insulation LLC

Lloyd Insulations Ltd

Mitsui Chemicals Inc

Owens Corning

Polybond Insulation Pvt Ltd

Rockwell International Corp

Rogers Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Board Insulation Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Board Insulation Market Size Outlook, $ Million, 2021 to 2030

3.2 Board Insulation Market Outlook by Type, $ Million, 2021 to 2030

3.3 Board Insulation Market Outlook by Product, $ Million, 2021 to 2030

3.4 Board Insulation Market Outlook by Application, $ Million, 2021 to 2030

3.5 Board Insulation Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Board Insulation Industry

4.2 Key Market Trends in Board Insulation Industry

4.3 Potential Opportunities in Board Insulation Industry

4.4 Key Challenges in Board Insulation Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Board Insulation Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Board Insulation Market Outlook by Segments

7.1 Board Insulation Market Outlook by Segments, $ Million, 2021- 2030

By Application

Building & Construction

Transportation

Industrial

Others

8 North America Board Insulation Market Analysis and Outlook To 2030

8.1 Introduction to North America Board Insulation Markets in 2024

8.2 North America Board Insulation Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Board Insulation Market size Outlook by Segments, 2021-2030

By Application

Building & Construction

Transportation

Industrial

Others

9 Europe Board Insulation Market Analysis and Outlook To 2030

9.1 Introduction to Europe Board Insulation Markets in 2024

9.2 Europe Board Insulation Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Board Insulation Market Size Outlook by Segments, 2021-2030

By Application

Building & Construction

Transportation

Industrial

Others

10 Asia Pacific Board Insulation Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Board Insulation Markets in 2024

10.2 Asia Pacific Board Insulation Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Board Insulation Market size Outlook by Segments, 2021-2030

By Application

Building & Construction

Transportation

Industrial

Others

11 South America Board Insulation Market Analysis and Outlook To 2030

11.1 Introduction to South America Board Insulation Markets in 2024

11.2 South America Board Insulation Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Board Insulation Market size Outlook by Segments, 2021-2030

By Application

Building & Construction

Transportation

Industrial

Others

12 Middle East and Africa Board Insulation Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Board Insulation Markets in 2024

12.2 Middle East and Africa Board Insulation Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Board Insulation Market size Outlook by Segments, 2021-2030

By Application

Building & Construction

Transportation

Industrial

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

BASF SE

Compagnie de Saint-Gobain

DUNA-Corradini S.p.A.

Huntsman Corp

Industrial Insulation Group LLC

Knauf Insulation LLC

Lloyd Insulations Ltd

Mitsui Chemicals Inc

Owens Corning

Polybond Insulation Pvt Ltd

Rockwell International Corp

Rogers Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Application

Building & Construction

Transportation

Industrial

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)