Market Analysis: Strategic Investments and Technological Advances Accelerate the EV Component Market

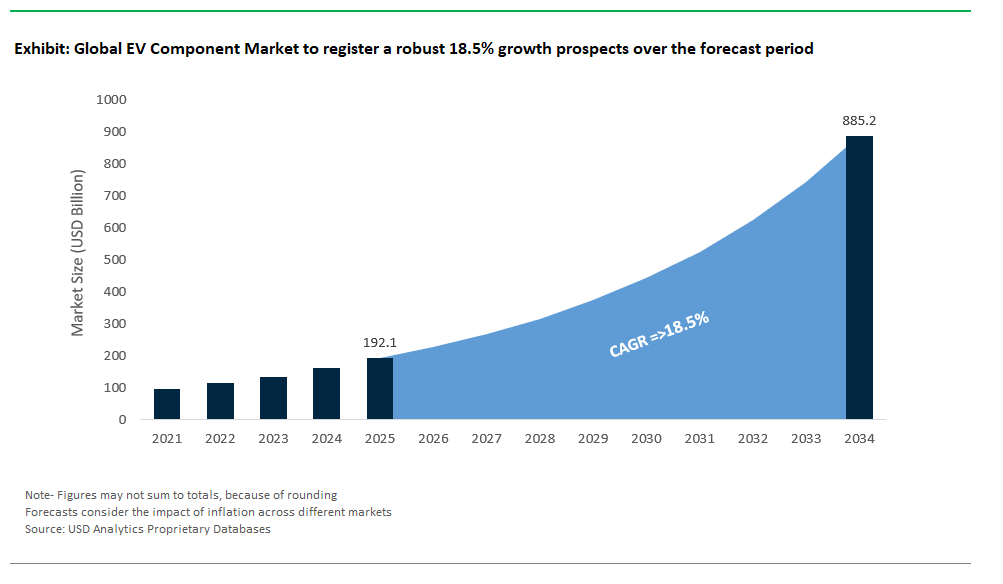

The Global EV Component Market Size is estimated at $192.1 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 18.5% to reach $885.1 Billion by 2034.

The global EV Component market is experiencing rapid expansion, fueled by large-scale investments, innovative joint ventures, and critical manufacturing milestones. In July 2025, Panasonic Energy commenced mass production of its 2170 cylindrical lithium-ion battery cells at its new De Soto, Kansas facility. This U.S. plant targets an impressive annual output of 32 gigawatt-hours (GWh), positioning Panasonic as a major force in North America’s EV battery supply chain. Meanwhile, Chinese electric vehicle leader BYD commissioned the world’s largest roll-on/roll-off (Ro-Ro) vessel, capable of transporting over 30,000 electric cars at once, significantly strengthening BYD’s global EV logistics and component distribution network.

Collaboration and joint ventures remain at the forefront of advancing EV technologies and securing critical raw materials. Volkswagen’s up-to-US$5.8 billion joint venture with Rivian Automotive will co-develop next-generation battery-electric vehicle platforms and software, giving Volkswagen direct access to Rivian’s innovative EV technology. In the resource domain, General Motors has committed US$625 million to a joint venture with Lithium Americas Corp for the Thacker Pass lithium mine, ensuring a reliable domestic supply of lithium a key component for EV batteries vital for scaling up North American EV production and supporting supply chain resilience.

Global expansion and technological innovation in charging and core EV systems are further propelling the market forward. Huawei is set to launch an ultra-fast EV charger in Singapore by late 2025, a move poised to enhance regional charging infrastructure with state-of-the-art high-power components. On the manufacturing side, the new ZF-Foxconn Chassis Modules joint venture will develop and produce advanced chassis systems for electric vehicles, simplifying the supply chain for automotive OEMs. Meanwhile, Magna International and LG Electronics are expanding their LG Magna e-Powertrain venture with new manufacturing and R&D facilities, focusing on electric motors, inverters, and onboard chargers key building blocks for the next wave of global EVs. Collectively, these strategic moves and innovations are reshaping the EV Component market, strengthening the global supply chain and accelerating the transition to electric mobility.

EV Component Market Advances with Structural Integration and Thermal Management Innovations

Cell-to-Chassis (CTC) Integration for Structural Efficiency

The EV Component Market is rapidly evolving with the widespread adoption of Cell-to-Chassis (CTC) integration, a breakthrough design approach that eliminates traditional module structures to enhance structural efficiency. By embedding battery cells directly into the vehicle chassis, manufacturers achieve significant weight reduction, improving energy density and extending overall vehicle range. This integration also optimizes space utilization within EV platforms, allowing for more compact designs without compromising safety or performance.

CTC adoption is gaining traction among leading automakers due to its scalability and manufacturing benefits. Incorporating structural battery trays into chassis design enables faster assembly times and streamlined production processes, resulting in substantial cost savings for high-volume manufacturing. This structural innovation is not only transforming EV architecture but also positioning CTC as a key enabler for next-generation electric mobility.

Hairpin Winding with Partial Discharge Monitoring

Another critical trend shaping the EV component market is the integration of hairpin winding technology in high-voltage 800V electric motors. This advanced winding method, often featuring asymmetric designs, offers significantly higher torque density compared to conventional round wire systems, directly contributing to improved power output and drivetrain efficiency. Automakers are adopting hairpin windings to meet the performance demands of premium EV models and fast-charging architectures.

Coupled with this advancement is the incorporation of AI-driven partial discharge monitoring systems, designed to predict potential motor failures hundreds of hours before they occur. These intelligent sensors provide real-time diagnostics, enabling proactive maintenance and ensuring optimal reliability for fleet operations. Validated in real-world scenarios, this predictive maintenance capability is revolutionizing EV motor performance management, minimizing downtime, and enhancing long-term vehicle durability.

Liquid Cooling Plate Optimization for Fast Charging

A major opportunity exists in the optimization of liquid cooling plates for EV battery packs, a critical requirement to support ultra-fast charging capabilities exceeding 350 kW. Innovative designs, such as 3D-printed cooling plates made from titanium and other advanced materials, are proving highly effective in mitigating thermal hotspots and maintaining uniform temperature distribution within battery cells. These enhancements ensure battery health and longevity even under extreme charging conditions, paving the way for the mass adoption of high-power charging infrastructure.

The demand for advanced cooling solutions is particularly strong in commercial EV segments, including electric buses and heavy-duty trucks, where extended operational cycles and fast-charging needs place heavy thermal loads on battery systems. This segment is projected to evolve into a multi-billion-dollar market by 2027, driven by the rapid electrification of freight and public transport fleets. Companies investing in cutting-edge thermal management systems will gain a strategic advantage in enabling high-performance, reliable electric mobility solutions globally.

Competitive Landscape: Electric Vehicle (EV) Component Market

Infineon Technologies: SiC and GaN Powerhouse Driving Electric Mobility Innovation

Infineon Technologies stands out as a global leader in the EV component market, renowned for its advanced power semiconductors and system solutions that underpin the modern electric vehicle revolution. The company’s automotive-grade Silicon Carbide (SiC) MOSFETs and diodes are widely recognized for their ability to maximize inverter efficiency and boost EV driving range, supporting everything from high-voltage traction inverters to onboard chargers and DC-DC converters. Infineon’s microcontroller (MCU) portfolio, including the AURIX™ and TRAVEO™ lines, offers robust, safety-compliant control for powertrains, battery management, and ADAS enabling intelligent, connected, and secure EV architectures. Strategic collaborations, such as the 2025 partnership with Tata Elxsi for India-focused scalable solutions, highlight Infineon’s commitment to market-specific innovation, covering electric two-wheelers to commercial vehicles with specialized SiC-based modules and thermal management technology. Infineon’s sustainability leadership is reinforced by ongoing R&D in GaN power devices, as well as a comprehensive suite of sensors, battery management ICs, and gate drivers all of which are integral for the safety, efficiency, and reliability of next-generation EVs. The company’s acquisition of Marvell’s Automotive Ethernet business and focus on light electric vehicles signal a broader ambition: to lead in every major EV segment as electrification and digitalization reshape the automotive landscape.

STMicroelectronics: Advanced SiC and Microcontroller Solutions for Future-Proof EVs

STMicroelectronics (ST) is firmly entrenched at the heart of the EV component supply chain, leveraging its global expertise in power semiconductors and intelligent control systems to serve both established automakers and emerging electric mobility innovators. ST’s fourth-generation STPOWER SiC MOSFETs set the benchmark for traction inverters, bringing high-voltage efficiency and fast-switching performance from luxury EVs to mass-market models. With investments accelerating toward the qualification of 1200V class SiC devices and the development of fifth-generation technologies, ST demonstrates relentless innovation in power density and robustness enabling both fast-charging infrastructure and longer EV range. The company’s STM32 Automotive-grade microcontrollers are renowned for their safety, flexibility, and reliability, handling everything from chassis and body control to battery management and e-motor drives. By integrating a broad suite of sensors, ESD protection, and battery cell balancing ICs, ST delivers holistic electromobility solutions that address the evolving needs of EV design. Notably, the company’s expansion into fast DC charging stations and modular EV platforms positions STMicroelectronics as a critical enabler for the electrification of transport, supporting both OEMs and charging ecosystem partners in building more efficient, connected, and safer electric vehicles worldwide.

onsemi: EliteSiC Technology and Sensor Leadership Powering the Next Generation of EVs

onsemi is a frontrunner in delivering intelligent power and sensing solutions that are redefining the standards of efficiency and integration in the electric vehicle component market. With its EliteSiC platform, onsemi is rapidly scaling up the adoption of high-voltage SiC MOSFETs and diodes, empowering automotive partners such as Schaeffler to design compact, thermally advanced traction inverters for global EV platforms. The company’s vertically integrated SiC supply chain spanning wafer growth to final packaging guarantees a reliable, high-quality source of critical power devices in an increasingly supply-constrained market. onsemi’s portfolio extends well beyond power semiconductors: integrated power modules, advanced gate drivers, robust battery management ICs, and high-performance sensors like Hyperlux™ for in-cabin and motor control applications. The company’s 2024 Sustainability Report underscores its commitment to ESG goals, while recent wins with automakers reflect the trust in onsemi’s ability to deliver superior efficiency, safety, and total cost-of-ownership benefits. As the demand for higher-performance EVs grows, onsemi remains at the leading edge, offering innovations that drive down system size, weight, and energy losses while supporting next-generation ADAS, connectivity, and vehicle autonomy.

Wolfspeed: Pure-Play SiC Leader Scaling Materials and Devices for Global Electrification

Wolfspeed is synonymous with Silicon Carbide (SiC) excellence, holding a unique position as a vertically integrated manufacturer of both SiC substrates and power devices. Wolfspeed’s automotive-grade SiC MOSFETs, Schottky diodes, and integrated modules are enabling a fundamental leap in electric vehicle performance, from main inverters and onboard chargers to high-efficiency DC-DC converters. The company’s Gen 4 MOSFET platform, launched in 2025, delivers breakthrough levels of durability and efficiency, providing OEMs with solutions that reduce power losses by up to 80% and extend EV range by as much as 10%. Wolfspeed’s capacity expansion anchored by its Mohawk Valley, New York fab and the John Palmour Manufacturing Center in North Carolina solidifies its status as the world’s largest SiC supplier, supporting both North American and global EV supply chains. Strategic partnerships with automotive giants like General Motors highlight Wolfspeed’s pivotal role in securing the future of EV production. By enabling smaller, lighter, and more efficient systems, Wolfspeed’s SiC technology accelerates the electrification of all vehicle classes, from passenger cars to heavy commercial vehicles, cementing its reputation as a foundational player in the shift to sustainable mobility.

Rohm Co., Ltd.: Japanese Innovation Driving SiC and Functional Safety in EV Platforms

Rohm Co., Ltd. is emerging as a major force in the EV component space, particularly in the development and mass production of advanced SiC power devices. The company’s fourth-generation SiC MOSFETs have been adopted by leading automakers like Toyota for flagship BEV models, setting new standards for efficiency and range in electric powertrains. Rohm’s approach to innovation is both deep and broad: it invests in the rapid evolution of SiC, with plans for fifth, sixth, and even seventh-generation device lines, while also providing a full suite of IGBTs, MOSFETs, sensors, and microcontrollers for automotive systems. The company’s joint venture in China and rollout of mass production for SiC modules underscore its commitment to global supply chain resilience. Rohm’s focus on functional safety, highlighted by its ISO 26262 development process and ComfySIL™ solutions, addresses the critical need for robust, reliable EV electronics in an era of software-defined vehicles. With advanced tools like the ROHM Solution Simulator for rapid circuit prototyping and an increasing presence in both powertrain and body electronics, Rohm is positioned to play a significant role in the ongoing evolution of electric vehicles across all segments.

Market Share and Segmentation Insights: EV Component Market

By Component: Power Modules Dominate, Traction Inverters and BMS Gain Pace

In the rapidly growing EV component market, power modules (IGBT/SiC) command the largest share at 35.3% in 2025. Their dominance stems from their pivotal role in high-efficiency energy conversion, with silicon carbide (SiC) technology accelerating adoption in next-generation electric vehicles. Traction inverters are expanding quickly, driven by a projected CAGR of 19.6%, as 800V EV architectures boost demand for SiC-based designs that enable higher power density and improved performance. Battery management systems (BMS) are also increasingly important, optimizing battery safety and longevity as battery pack complexity and energy density rise. On-board chargers and DC-DC converters are growing steadily, supporting evolving charging infrastructures and enabling efficient power distribution in modern electric drivetrains.

.png)

By Technology: Silicon IGBT Leads, Silicon Carbide Surges Ahead

Silicon IGBT technology holds the largest share at 60.7% in 2025, maintaining its dominance in cost-sensitive, entry-level electric vehicles due to its proven reliability and mature supply chain. However, Silicon Carbide (SiC) technology is the fastest-growing segment with an impressive CAGR of 20.1%, as leading manufacturers like Tesla and Lucid Motors leverage SiC’s superior efficiency, higher voltage tolerance, and lower switching losses to extend EV range and enable fast charging. Gallium Nitride (GaN), while representing a smaller share, is emerging as a key enabler in on-board chargers and DC-DC converters, supporting lightweight designs and ultra-fast charging capabilities for the next wave of electric mobility.

China: Global Battery Hub, Vertical Integration, and Infrastructure Supremacy

China is the undisputed epicenter of global EV component manufacturing, especially in batteries and key raw materials. In 2024, China produced 80% of the world’s battery cells and met 59% of global EV battery demand, with Chinese companies like CATL and BYD owning over three-quarters of this capacity. The country’s dominance extends up the supply chain, supplying 85% of cathode and 90% of anode materials globally. The rise of LFP (Lithium Iron Phosphate) batteries is a defining trend; LFP met nearly three-quarters of domestic demand and is projected to reach 80% by year-end, with global LFP share approaching 50%. This shift is led by safety, cost, and abundant local supply of necessary materials.

Chinese battery makers are at the cutting edge: CATL’s TECTRANS system, introduced in 2024, is optimized for commercial vehicles and hybrid EVs, promising smaller, lighter, and more powerful cells. The government-backed CASIP consortium signals a national push toward all-solid-state battery R&D, potentially leapfrogging the next era of EV batteries. On infrastructure, China added 4.22 million new charging points in 2024 (totaling 12.82 million), with major cities like Beijing and Chongqing accelerating deployment of ultra-fast chargers. The vertical integration of BYD from mining and cell production to launching the “Blade Battery” and the world’s largest EV Ro-Ro vessel underscores China’s cradle-to-grave EV dominance and expanding export ambitions.

United States: IRA-Fueled Localization, Tech Diversity, and Recycling Innovation

The Inflation Reduction Act (IRA) has supercharged U.S. EV component investment, triggering $112 billion in battery production projects and targeting 1,200 GWh/year domestic capacity by 2030. LG Energy Solution (LGES) leads the charge with new plants in Arizona and Michigan, now producing all major battery cell types (pouch, cylindrical, prismatic), while Ford and Tesla expand in-house cell production to tighten supply chain control and qualify for tax credits.

Public charging infrastructure in the U.S. grew by 20% in 2024, surpassing 200,000 public points and 50,000 fast chargers, supporting greater EV adoption. Recycling is becoming a strategic pillar: Ascend Elements and Koura have launched processes to reclaim 99.9% pure graphite, reducing reliance on virgin imports and positioning the U.S. as a sustainability leader. This ecosystem is further buttressed by battery supply chain security incentives and a growing emphasis on circular economy principles.

South Korea: Battery Cell Innovation, HBM Growth, and Fast-Charging Investment

South Korean giants SK On, Samsung SDI, and LGES are scaling up cell technology and expanding U.S. presence. SK On’s investment in High Bandwidth Memory (HBM) chips is notable for EVs requiring advanced computational power (especially for autonomous and connected vehicles). Samsung SDI’s focus on prismatic cells, energy efficiency, and safety has grown its U.S. market share to 35% in 2024.

On the supply chain side, Korean firms are securing lithium hydroxide deals (e.g., EcoPro to SK On) and investing heavily in next-generation cathode/anode materials. Government policies provide direct incentives for electric trucks and have boosted the 2025 charging infrastructure budget by 40%, with a majority going to fast-charging networks critical for nationwide EV adoption.

Japan: Solid-State Battery R&D and Leading Component Suppliers

Japan remains a pivotal EV component player through Panasonic’s ongoing U.S. battery dominance (still supplying half the U.S. EV battery market), as well as deep R&D in solid-state batteries via Toyota. Although commercialization of solid-state batteries is expected post-2025, Japan’s multi-billion-dollar investment signals the next phase of global battery innovation.

Japanese power electronics suppliers Denso and Hitachi are advancing inverter, e-motor, and power module technology, with a focus on miniaturization and efficiency. These components remain crucial to the next generation of BEVs and hybrid vehicles globally.

Germany: Localization of Cells, e-Drives, and Next-Gen Drivetrains

Germany is anchoring European efforts to localize battery cell manufacturing and advanced component production. Volkswagen’s PowerCo cell factory in Spain and BMW’s Dingolfing e-drive facility are flagships for in-house battery, motor, and electronics production. Bosch and ZF Friedrichshafen continue to lead in power electronics, inverters, and integrated e-drives, especially with SiC power semiconductor development.

Despite a short-term dip in domestic EV sales due to subsidy cuts, Germany’s long-term strategy remains centered on R&D, production scale-up, and supply chain resilience for Europe’s EV ecosystem. Investments in production will support renewed growth as subsidies return or as EU-wide mandates kick in.

India: Government-Driven Demand, Domestic Supply Chain, and Infrastructure Push

India is accelerating its EV component industry with FAME II and PLI incentives, new schemes for e-bus and e-drive, and significant investments in domestic battery cell and module manufacturing (Tata, Ola, Exide). Micron’s ATMP facility for semiconductors and Tata’s push into battery packs and power electronics are supporting the rapid growth in two-, three-, and four-wheeler EVs.

Charging infrastructure received a USD 240 million allocation in 2024, driving a fivefold increase in public chargers since FY22. BYD’s expansion and the localization of component production are positioning India to meet both domestic and export demand for EVs and parts.

United Kingdom: Gigafactory Grants, Specialized Cells, and Circular Economy Moves

The UK is cultivating battery cell manufacturing via gigafactory grants (e.g., Nissan’s EV36Zero with Envision AESC) targeting 100 GWh annual capacity by 2030. AMTE Power’s focus on high-power, specialty cells supports both automotive and niche applications. The UK is also a leader in smart charging technology and is building a recycling and recovery policy framework to ensure critical material security for the future.

France: European Battery Alliances and Component Specialization

France is at the heart of European battery production growth via the ACC (TotalEnergies, Stellantis, Mercedes-Benz) gigafactory in Douvrin, expanding capacity for high-performance Li-ion cells. The Stellantis-CATL joint venture further integrates LFP cell production into the EU supply chain, supporting the shift to affordable EVs.

French supplier Faurecia (Forvia) is driving innovation in thermal management, hydrogen storage for fuel cell EVs, and lightweight interiors key for improving EV range and safety. The French government’s support via the Chips Act and national incentives underscores France’s strategy of building a competitive, secure EV component sector within Europe.

EV Component Market Report Scope

EV Component Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$192.1 Billion

|

|

Market Size (2034)

|

$885.1 Billion

|

|

Market Growth Rate

|

18.5%

|

|

Segments

|

By Component (Power modules (IGBT/SiC), Traction inverters, On-board chargers, DC-DC converters, Battery management systems), By Technology (Silicon IGBT, Silicon carbide (SiC), Gallium nitride (GaN)), By Vehicle Type, BEVs, PHEVs, Commercial EVs), By Integration Level (Discrete components, Integrated power units)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Infineon, STMicroelectronics, onsemi, Wolfspeed, Rohm, BorgWarner, Valeo/Siemens, Texas Instruments, Mitsubishi Electric, Hyundai Mobis

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

EV Component Market Segmentation

By Component

- Power modules (IGBT/SiC)

- Traction inverters

- On-board chargers

- DC-DC converters

- Battery management systems

By Technology

- Silicon IGBT

- Silicon carbide (SiC)

- Gallium nitride (GaN)

By Vehicle Type

- BEVs

- PHEVs

- Commercial EVs

By Integration Level

- Discrete components

- Integrated power units

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in EV Component Market

- Infineon

- STMicroelectronics

- onsemi

- Wolfspeed

- Rohm

- BorgWarner

- Valeo/Siemens

- Texas Instruments

- Mitsubishi Electric

- Hyundai Mobis

* List Not Exhaustive

Research Coverage

The EV Component Market report from USDAnalytics provides in-depth market sizing, CAGR, and value projections, placing recent developments such as Panasonic’s U.S. battery plant launch, BYD’s global logistics expansion, and Volkswagen-Rivian’s $5.8 billion EV technology joint venture at the forefront of industry transformation. The study thoroughly examines dynamics, technology trends, and strategic investments driving rapid EV market growth, with special emphasis on CTC integration, SiC/GaN adoption, hairpin winding, and advanced cooling innovations.

Structured segmentation covers components (power modules, traction inverters, on-board chargers, DC-DC converters, BMS), technologies (Silicon IGBT, SiC, GaN), vehicle types (BEVs, PHEVs, commercial EVs), and integration levels (discrete, integrated units). Company coverage includes leaders such as Infineon, STMicroelectronics, onsemi, Wolfspeed, Rohm, BorgWarner, Valeo/Siemens, and others, profiling their product portfolios and global expansion strategies.

Geographic analysis encompasses North America, Europe, Asia Pacific, South America, and Middle East & Africa, with market data spanning historic (2021–2024) and forecast (2025–2034) periods. The report delivers actionable insights for industry professionals, OEMs, investors, and policymakers addressing supply chain resilience, battery innovation, manufacturing advances, regional developments, and regulatory impacts in the fast-evolving EV component sector.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.