Market Overview: Bonding Sheet Market Growth Driven by Semiconductor Packaging, EV Thermal Management, and Bio-Based Adhesive Transitions (2025–2034)

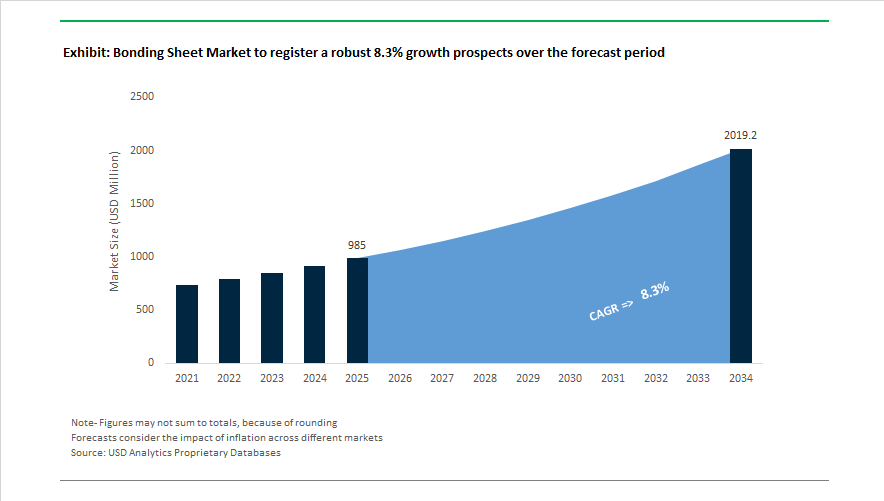

The bonding sheet market is projected to grow from USD 985 Million in 2025 to USD 2,018.8 Million by 2034, registering a CAGR of 8.3% supported by rapid expansion in semiconductor packaging, EV battery modules, flexible electronics, and sustainable industrial adhesives. Environmental compliance and advanced electronics manufacturing drove early developments in May 2024 when Toray Industries commercialized a PFAS-free mold release film designed for semiconductor package lamination processes. During late 2024, LG Chem strengthened its automotive adhesives presence through investments in thermally conductive bonding sheets used in EV electronic control units and battery cooling systems. Henkel also introduced phthalate-free Darex COV sealants across 2024 and 2025, aligning bonding and sealing solutions with safer packaging and sustainability requirements.

Manufacturing expansion and digitalization accelerated through 2025. In February 2025, 3M expanded adhesive production capacity in South Korea to supply structural and thermal bonding sheets for consumer electronics and EV battery assemblies. Semiconductor innovation intensified in November 2025 when Toray developed a temporary bonding material enabling the handling of wafers thinner than 30 micrometers for high-bandwidth memory chip production. In December 2025, Toray introduced a photo-definable polyimide sheet engineered for glass core substrates, with mass production targeted for April 2026. Digital product development tools emerged in December 2025 when 3M launched its Digital Materials Hub and AI assistant to simulate bonding sheet performance and reduce prototyping cycles.

Strategic realignments and material innovation are shaping 2026 outlooks. In August 2025, Tatsuta Electric Wire & Cable acquired UTM Corporation to expand EMI shielding and flexible circuit bonding capabilities. In November 2025, Sumitomo Chemical restructured its battery materials division, emphasizing separator bonding technologies to improve EV cell safety. January 2026 results from Resonac confirmed strong growth in bonding sheets for advanced packaging. In February 2026, Henkel partnered with Sekab to incorporate bio-based ethyl acetate into adhesive sheet production.

Supply Chain Control and Aerospace Qualification Requirements Driving Trends and Opportunities in the Bonding Sheet Market

Vertical Integration and Localization Secure Bonding Sheet Supply for EV and Semiconductor Programs

Automotive and electronics suppliers are reorganizing bonding sheet sourcing strategies to protect against chemical supply volatility, cost inflation, and geopolitical trade risk. Localization programs have accelerated, with tier-1 suppliers internalizing bonding sheet manufacturing to stabilize resin chemistries and ensure consistency in high-precision components. The Automotive Component Manufacturers Association confirmed in July 2025 that domestic OEM supply expansion is directly supported by in-house production of engineered bonding materials. Strategic agreements are reinforcing this shift. In October 2025, Ford and CATL finalized long-term partnerships centered on localized production of battery materials, including advanced bonding and insulation sheets, limiting exposure to cross-border tariffs and achieving just-in-time supply resiliency. This shift improves value retention, reduces lead-time uncertainty, and aligns with regional EV industrial policy frameworks.

Program-Specific Qualification and Traceability Become Mandatory for Aerospace Bonding Sheets

Aerospace primes are increasing approval stringency to ensure bonding sheet reliability in composite structural assemblies. Updated guidelines for MIL-STD-171 in February 2025 reinforced strict control of organic coatings and adhesive finishes to prevent long-term degradation in CFRP structures. Compliance with standards such as SAE AMS 3695 for adhesive films has become essential to maintain airworthiness certification. Airbus added “Material Part Manufacturing” under restricted Product Group AFM-002-2 in early 2025, requiring suppliers to provide resin-to-final-component traceability across all bonding sheet formats. These developments are shifting supplier evaluation criteria from price-per-part to certification credentials, aerospace pedigree, and digital transparency in quality control documentation.

Bonding Sheet Service Centers Enhance SME Access to Precision Die-Cutting and Assembly Efficiency

The rise of electronically functional bonding sheets with EMI shielding, thermal conduction, and multi-layer architecture is creating a strong growth opportunity for specialized conversion partners. Service centers such as Stockwell Elastomerics and CS Hyde are scaling precision die-cutting capabilities to tolerances of approximately ±0.015 inches, enabling small and medium manufacturers to deploy high-performance bonding materials without heavy investment in cleanroom fabrication tools. Just-in-time kitting models, increasingly adopted in 2025, bundle application-ready adhesive geometries onto a single release carrier. This configuration supports EV inverter production, medical wearables, and RF modules by reducing material waste by double-digit percentages and simplifying multi-step assembly into a standardized workflow.

Closed-Loop Recycling and Take-Back Schemes Reduce Polymer Waste and Material Cost Exposure

Bonding sheet production generates notable skeleton waste due to precision die-cutting, particularly with high-value polymers such as PEEK and polyimide. To safeguard supply economics and improve sustainability performance, manufacturers are developing closed-loop take-back programs that reprocess scrap into secondary industrial applications. Corporate commitments under Extended Producer Responsibility frameworks intensified in late 2025, enabling traceable material recovery. Avery Dennison’s AD Circular initiative provides a targeted model, allowing bonding sheet waste from converters to re-enter the supply chain as controlled recycling feedstock. Global institutions, including the World Bank and Citi, expanded financing programs between 2024 and 2025 that link recycled-content performance to capital access. These mechanisms incentivize bonding sheet producers to monetize waste reduction and reinforce ESG reporting credibility.

Bonding Sheet Market Share and Segmentation Insights

Market Share by Adhesive Material: Modified Epoxies Lead While Silicones Gain Momentum in Thermal Management

Modified epoxies command 41% of the Bonding Sheet Market in 2025, offering a balanced profile of adhesion strength, thermal stability up to 200°C, low moisture uptake, and chemical resistance, making them indispensable for semiconductor die attach, substrate lamination, and automotive power modules, with fast-curing, low-stress grades gaining traction. Polyimides rank second, dominating continuous-use temperatures of 250°C to 350°C for FPC reinforcement and aerospace electronics despite higher processing costs. Acrylic bonding sheets support optical applications in displays and interior automotive assemblies. Silicones are expanding rapidly in LED packaging and EV battery thermal interfaces, driven by wide-bandgap semiconductor adoption requiring stable dielectric properties at elevated temperatures. Polyesters remain a cost-focused option for non-critical lamination and packaging uses.

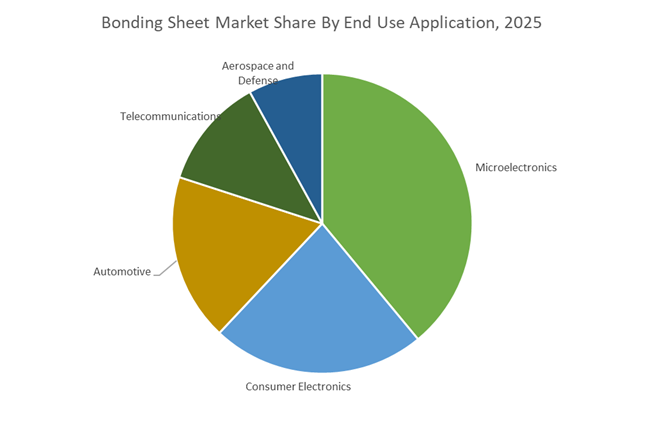

Market Share by End Use Application: Microelectronics Anchor Volume as Automotive and 5G Drive High-Performance Demand

Microelectronics represent 39% of bonding sheet consumption in 2025, encompassing die attach, wafer-level packaging, and substrate bonding as heterogeneous integration and chiplet architectures accelerate demand for ultra-thin, void-free materials with precise melt flow. Consumer electronics follow through camera modules and battery insulation, while automotive is the fastest-growing segment, driven by SiC-based power modules, ADAS sensors, and LED headlamps aligned with 800V EV platforms. Telecommunications is expanding rapidly as bonding sheets support 5G base stations, antenna arrays, and high-frequency PCB lamination, requiring low dielectric loss and stable Dk. Aerospace and defense remain niche but high-margin, with stringent outgassing and flame-retardant requirements sustaining demand in avionics and satellite systems.

Competitive Landscape Analysis of the Bonding Sheet Market

The global bonding sheet market in 2026 is being propelled by rapid growth in AI server infrastructure, EV power electronics, flexible printed circuits (FPC), aerospace composites, and advanced display modules. Competition is centered on low-dielectric bonding sheets, high-thermal-conductivity resin sheets, anisotropic conductive films (ACF), and thermoplastic composite bonding technologies. Market leaders are differentiating through micron-level thickness control, solvent-free manufacturing, and next-generation thermal management solutions. Strategic priorities now include 6G-ready multilayer PCBs, lightweight aircraft structures, circular-economy electronics, and high-voltage EV battery integration, positioning bonding sheets as critical enabling materials across electronics, mobility, and aerospace supply chains.

Low-dielectric bonding sheets for AI servers and EV electronics from Panasonic Industry Co., Ltd.

Panasonic Industry leads the electronic materials segment with high-performance prepreg and bonding sheets engineered for ultra-low dielectric loss, supporting 6G testing platforms and next-generation multilayer circuit boards. In early 2026, the company expanded production of low-transmission-loss bonding sheets to meet surging demand from AI data centers requiring PCBs exceeding 30 layers. Its core strength lies in proprietary resin chemistry that preserves electrical integrity under the extreme operating temperatures of EV power modules. Strategically aligned with “social problem solving,” Panasonic is advancing materials that enable miniaturization and energy efficiency, with a growing focus on thermal management solutions for high-voltage EV battery packs and automotive CASE applications.

Micron-precision bonding sheets for AR/VR and wearables by Dexerials Corporation

Dexerials sets the global benchmark for high-precision bonding sheets and anisotropic conductive films (ACF), where bond-line thickness is controlled at the micron scale. In 2026, its ACFs remain the industry standard for connecting micro-LED displays in premium AR/VR headsets. The January 2026 launch of the SFJ-21A Series, paired with complementary bonding interfaces, targets ultra-compact wearable medical devices. Using proprietary material compounding, Dexerials co-develops fast-curing sheets with OEMs, dramatically boosting smartphone camera module throughput. Backed by a CDP Leadership (A-) rating, the company is accelerating adoption of solvent-free bonding sheets and sustainable manufacturing.

High-thermal-conductivity resin bonding sheets from Sumitomo Bakelite Co., Ltd.

Sumitomo Bakelite dominates thermosetting resin bonding sheets for power electronics and high-temperature insulation. Its flagship heat dissipation sheets are engineered to transfer heat from power semiconductors while maintaining stability above 150°C. In January 2026, the company integrated these sheets into EV power modules, achieving industry-leading thermal conductivity of 18 W/(m·K). Strategically expanding into aerospace, Sumitomo Bakelite launched biomass-based PFA resin prepregs with superior flame retardancy for aircraft interiors. With deep phenolic resin expertise, its bonding sheets deliver triple the char yield of epoxy alternatives, making them preferred materials for fire-safe electronics and industrial-grade applications.

Flexible printed circuit bonding leadership from Nitto Denko Corporation

Nitto Denko leverages its Sanshin innovation framework to lead the flexible printed circuit and semiconductor encapsulation bonding sheet market. Its 2026 portfolio emphasizes high heat resistance and low moisture absorption, critical for automotive sensor reliability. Recognized as a Clarivate Top 100 Global Innovator 2026, Nitto deploys a powerful IP strategy to protect its high-frequency 5G/6G materials. Through its “0→1→10→100” commercialization flow, custom bonding sheets rapidly scale from lab concepts to mass production. The company’s PlanetFlags initiative further highlights solvent-free, eco-friendly bonding sheets aligned with global sustainability mandates.

CFRP thermal welding bonding sheets from Toray Industries, Inc.

Toray is redefining composite joining with breakthrough bonding sheet technology for carbon fiber reinforced plastics (CFRP). In January 2026, Toray introduced a proprietary thermal welding bonding sheet that bonds CFRP structures three times faster than conventional methods. Targeting next-generation single-aisle aircraft, Toray’s solutions eliminate heavy mechanical fasteners, enabling lighter thermoplastic composite airframes. Its strategic focus on aeronautical sustainability aligns with ICAO carbon reduction goals. Toray’s core strength lies in thermoset-to-thermoplastic hybridization, producing bonding sheets capable of welding dissimilar composites with higher strength than traditional liquid adhesives, accelerating aerospace and mobility lightweighting.

Intelligent acrylic bonding sheets for EV cockpits from Tesa SE

Tesa leads Europe in functional adhesive bonding sheets for electronics and automotive applications. The full operation of its Vietnam plant in 2025/2026 significantly expanded capacity for Asian EV and electronics hubs. Through Customer Solution Centers in Germany, China, and the USA, Tesa co-develops bonding sheets with OEMs to support ease-of-disassembly and circular economy goals. Its high-performance acrylic bonding sheets are now critical for joining glass and ceramics in premium EV digital cockpits. Marketed as “the joining technology of the 21st century,” Tesa’s solutions replace welding and riveting, delivering weight reduction, surface protection, and scalable automation.

Japan Bonding Sheet Market: Glass Core Substrates and Thermal Resilience Redefining Advanced Bonding Sheets

Japan continues to anchor the global bonding sheet industry through deep integration with next-generation semiconductor packaging, power electronics, and state-backed technology sovereignty initiatives. In December 2025, Toray Industries announced the development of a negative photo-definable polyimide bonding sheet tailored for glass core substrates. This material enables simultaneous redistribution layer formation and through-glass via resin filling, materially reducing process complexity and cost for AI-centric and high-bandwidth chips. The innovation directly addresses the shift toward glass substrates as silicon interposers reach physical and economic limits in advanced packaging.

Thermal management is another defining axis of Japan’s leadership. Showa Denko Materials (now Resonac) expanded capacity in late 2024 for high-thermal-conductivity bonding sheets engineered for silicon carbide power modules capable of continuous operation beyond 200°C. These materials are critical for EV inverters and fast-charging infrastructure. Policy alignment further reinforces scale-up. Subsidies under the Ministry of Economy, Trade and Industry’s Post-5G materials program are supporting pilot lines for ultra-flat bonding sheets that reduce glass cracking during lamination. In parallel, the 2025–2026 Sanaenomics framework is unlocking corporate capital via tax credits, accelerating investment in advanced bonding sheets with ultra-low melt viscosity required for sub-10-micron microvia processing in generative AI hardware.

United States Bonding Sheet Market: PFAS Elimination and CHIPS Act Funding Accelerating Bonding Sheet Innovation

The U.S. bonding sheet market is undergoing a structural reset driven by environmental compliance, aerospace lightweighting, and federally backed semiconductor infrastructure. As of early 2026, domestic manufacturers are rapidly phasing out fluorinated carriers, with 3M approaching its stated goal of eliminating PFAS from all products by late 2026. During 2025 alone, the company introduced more than 100 new bonding formulations, many designed for electronics and structural applications that meet tightening state and federal regulations.

Aerospace and automotive lightweighting remain high-value demand centers. In Q1 2025, 3M launched the Scotch-Weld™ DP8000 Series, a structural bonding sheet solution engineered to replace mechanical fasteners in EV frames and aerospace assemblies, enabling weight reduction without compromising crash or fatigue performance. At the ecosystem level, CHIPS Act funding in 2025 has been channeled into National Advanced Packaging Manufacturing Program centers, strengthening domestic R&D for thermocompression bonding sheets required for 2.5D and 3D stacked IC architectures. Beyond electronics, medical micro-fluidics is emerging as a niche but fast-growing segment. H.B. Fuller expanded its specialty bonding sheet line in late 2025, introducing biocompatible materials for lab-on-a-chip diagnostic sensors, reinforcing the role of bonding sheets in decentralized healthcare technologies.

India Bonding Sheet Market: Policy-Backed Localization and Semiconductor Ambitions Creating Structural Demand

India’s bonding sheet industry is transitioning from an import-dependent model toward localized manufacturing, supported by coordinated industrial policy and capital market depth. The 2025–2026 Union Budget expanded allocations under the Production Linked Incentive scheme for white goods and electronics, explicitly targeting localization of sub-assembly components such as PCB bonding sheets and prepregs. This policy thrust aligns with the rapid build-out of domestic electronics manufacturing capacity and rising quality requirements for multilayer boards and high-frequency applications.

Financial infrastructure is reinforcing this industrial momentum. A December 2025 NITI Aayog report highlighted the expansion of India’s corporate bond market to ₹53.6 trillion, improving access to long-term financing for chemical and adhesive manufacturing assets. Semiconductor ambitions further strengthen demand visibility. Following the extension of the IBM–TEL agreement in 2025, Gujarat-based semiconductor initiatives are prioritizing wafer-to-wafer bonding sheet integration for localized 3D chip production. Concurrently, the Bharat 6G Mission is stimulating demand for liquid crystal polymer-based bonding sheets optimized for high-frequency antenna arrays, positioning bonding sheets as enabling materials for India’s future telecom infrastructure.

Germany and the European Union Bonding Sheet Market: Regulation-Led Redesign and Circular Automotive Bonding

In Europe, bonding sheet innovation is being driven less by volume expansion and more by regulatory compliance, recyclability, and precision manufacturing. From January 2026, updated EU F-Gas regulations have effectively eliminated the use of high-GWP solvents in bonding sheet production, accelerating the shift toward water-borne and fully solid adhesive films across electronics and automotive applications. This regulatory pivot is reshaping process design and material selection for European producers.

Automotive circularity is a defining use case. In Q3 2024, Sika and H.B. Fuller entered a strategic collaboration to develop reversibly bonded sheets that allow EV battery modules to be disassembled at end-of-life without damaging cells, directly supporting EU recycling mandates. At the advanced packaging frontier, EV Group introduced the EVG 40 D2W platform in September 2025, the first dedicated die-to-wafer metrology system enabling full bonding precision control on 300 mm wafers. This capability underpins Europe’s competitiveness in hybrid bonding and advanced logic-memory integration.

Comparative Snapshot: Bonding Sheet Industry by Country

Bonding Sheet Market County Level Snapshot

|

Country / Region

|

Primary Demand Driver

|

Structural Industry Direction

|

|

Japan

|

Glass core substrates, power electronics

|

Ultra-flat, high-thermal, sub-10-micron bonding sheets

|

|

United States

|

PFAS phase-out, CHIPS Act, aerospace

|

PFAS-free, structural and thermocompression bonding

|

|

India

|

PLI schemes, semiconductor fabs, 6G

|

Localization of PCB and W2W bonding sheets

|

|

Germany / EU

|

F-Gas regulation, EV recycling

|

Solvent-free, reversible, hybrid bonding solutions

|

Bonding Sheet Market Report Scope

Bonding Sheet Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$985 Million

|

|

Market Size (2034)

|

$2018.8 Million

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Adhesive Material (Polyimides, Modified Epoxies, Acrylics, Polyesters, Silicones), By Substrate Compatibility (Glass Core Substrates, Flexible Printed Circuits, Rigid Flex PCBs, Metal and Ceramic Heat Sinks), By Functionality (Thermally Conductive Sheets, Electrically Conductive Sheets, EMI and RFI Shielding Sheets, Low Dk and Low Df Sheets), By Thickness (Ultra Thin, Standard, Thick), By End Use Application (Microelectronics, Automotive, Telecommunications, Consumer Electronics, Aerospace and Defense)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Toray Industries, 3M, Resonac Holdings, Henkel, Nitto Denko, DuPont, Arisawa Manufacturing, Dexerials, Shin Etsu Polymer, H B Fuller, Nikkan Industries, Namics, Sika, Arkema, Rogers Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bonding Sheet Market Segmentation

By Adhesive Material

- Polyimides

- Modified Epoxies

- Acrylics

- Polyesters

- Silicones

By Substrate Compatibility

- Glass Core Substrates

- Flexible Printed Circuits

- Rigid Flex PCBs

- Metal and Ceramic Heat Sinks

By Functionality

- Thermally Conductive Sheets

- Electrically Conductive Sheets

- EMI and RFI Shielding Sheets

- Low Dk and Low Df Sheets

By Thickness

- Ultra Thin

- Standard

- Thick

By End Use Application

- Microelectronics

- Automotive

- Telecommunications

- Consumer Electronics

- Aerospace and Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bonding Sheet Industry

- Toray Industries

- 3M

- Resonac Holdings

- Henkel

- Nitto Denko

- DuPont

- Arisawa Manufacturing

- Dexerials

- Shin Etsu Polymer

- H B Fuller

- Nikkan Industries

- Namics

- Sika

- Arkema

- Rogers Corporation

*- List not Exhaustive