Market Overview: Boron Trifluoride Market Expansion Backed by Semiconductor-Grade Purity, Fluorospecialty Capacity Additions, and Supply Chain Localization (2025–2034)

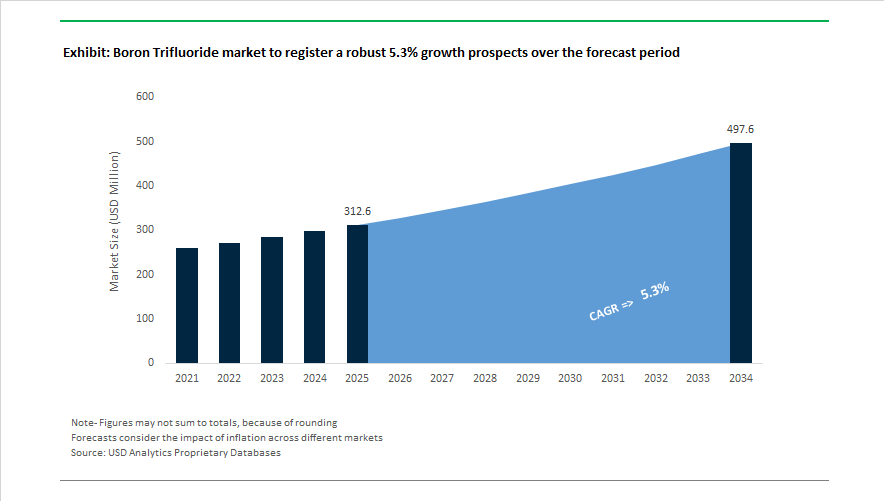

The boron trifluoride market is projected to grow from USD 312.6 Million in 2025 to USD 497.6 Million by 2034, registering a CAGR of 5.3% driven by rising demand for ultra-high-purity BF₃ in semiconductor fabrication, specialty polymerization catalysts, pharmaceutical intermediates, and advanced fluorochemical synthesis. Corporate restructuring began reshaping the competitive landscape in October 2024 when Honeywell announced plans to spin off its Advanced Materials business, which houses leading boron trifluoride and fluorine product lines. The separation timeline was clarified in October 2025 with confirmation that Solstice Advanced Materials would become an independent specialty chemicals entity. Concurrently, tariff measures implemented in January 2025 in the United States prompted BF₃ producers to prioritize domestic supply agreements and regionalized manufacturing.

Manufacturing and technology expansion accelerated through 2025. In August 2025, Arkema inaugurated a $60 million fluorospecialty production facility in Kentucky, reinforcing precursor availability for boron-based complexes used in insulation and polymer systems. October 2025 marked the revenue contribution of Navin Fluorine International Ltd’s new fluoro-specialty plant, strengthening supply of high-purity fluorinated intermediates used in catalyst and pharmaceutical synthesis. Navin Fluorine also advanced debottlenecking at its Dahej multi-purpose plant during 2025 to support new catalyst molecule production. Semiconductor-grade innovation gained momentum through Arkema’s partnership with Entegris during 2024 and 2025, focusing on clean-room-grade BF₃ complexes for microfabrication processes.

High-purity applications and digital manufacturing integration define 2026 outlooks. In January 2026, Stella Chemifa Corporation forecast strong earnings growth driven by ultra-high-purity BF₃ for ion implantation in 5 nm and 7 nm chip production. BASF strengthened its materials optimization strategy by opening a global digital hub in India in January 2026 to apply AI-driven process optimization across specialty chemical production. That same month, BASF realigned leadership within its Care Chemicals segment, a key user of BF₃ catalysts in fragrance and personal care intermediates. February 2026 collaboration between BASF and Xfloat extended BF₃ derivative use into light-stabilized polymers for floating solar platforms. Parallel fluorination technology progress through the Navin Fluorine and Chemours immersion cooling partnership underscores the expanding role of advanced fluorochemistries across semiconductor, renewable energy, and high-performance materials manufacturing.

Strategic Trends and High-Value Opportunities Shaping the Boron Trifluoride Market

Geopolitical Friction and China+1 Sourcing Shift Reshape BF3 Supply Models

Boron Trifluoride sourcing is undergoing structural change driven by geopolitical exposure and export policy uncertainty across East Asia. China currently dominates BF3 capacity, and export governance updates are influencing industry-level decisions for pharmaceutical and semiconductor buyers. In October 2025, MOFCOM issued Announcements No. 55–58 enforcing broader export controls and enhanced “end-use verification” for strategic chemicals. While primarily targeting rare earth elements and graphite, BF3 shipments have been indirectly affected due to licensing scrutiny, extending export clearance times to approximately 45 working days in some cases. This change has prompted U.S. and Indian distributors to initiate defensive stockpiling programs, following observable price volatility in May 2025. For India, where BF3 demand is strongly linked to pharmaceutical applications, stockpiling has supported pricing and allowed domestic intermediaries to capture value despite only moderate national production volumes. In parallel, multinational electronics and API manufacturers are formalizing China+1 strategies by contracting secondary sources in Southeast Asia to diversify exposure away from single-region supply risk.

UHP Boron-11 and Complexed BF3 Chemistries Gain Traction in Biopharma Synthesis

Sustained investment in advanced pharmaceutical manufacturing is reshaping BF3 consumption patterns. High-purity, application-specific complexes such as BF3•MeOH and BF3•THF are gaining adoption due to their role in improving regioselectivity and catalytic efficiency in API synthesis. This is supported by capacity investments such as BASF’s GMP Solution Center in Wyandotte, Michigan, launched in June 2025, designed to supply customized BF3 chemistries to bioprocessing and small-molecule drug makers. These specialized derivatives help ensure reaction control and batch-to-batch purity aligned to FDA and EMA quality systems. With the rise of oligonucleotide and anti-inflammatory drug development, pre-acidified BF3 complexes are now being evaluated as critical Lewis acid catalysts that enable higher yields and tighter impurity profiles.

Boron Trifluoride as a Critical P-Type Dopant in GAA Semiconductor Fabrication

BF3 is strategically positioned within advanced semiconductor materials due to its essential role in p-type doping of silicon-germanium layers. As fabrication transitions from 5 nm to 2 nm Gate-All-Around structures, the technical need for ultra-high purity BF3 (6N purity class) has intensified. With global wafer capacity set to expand significantly through the next decade, supply resilience has become a priority for chipmakers. Suppliers including Honeywell’s Advanced Materials spin-off (expected completion in late 2025) and Linde have begun scaling UHP BF3 output to avoid shortages similar to those observed during the chip supply crisis. BF3 utilization in ion implantation and epitaxial deposition is also increasing as AI chip architectures require higher transistor density and thermal reliability. Securing uninterrupted BF3 supply is therefore emerging as a procurement KPI for semiconductor fabs planning multi-year production cycles.

BF3 as a Catalyst for LiFSI, the Future Powertrain Electrolyte

EV battery manufacturers are moving toward lithium bis(fluorosulfonyl)imide electrolytes as part of the transition to higher energy density and faster charging. BF3 gas plays a catalytic role in industrial LiFSI synthesis and is increasingly evaluated within next-generation electrolyte design due to its effect on ionic conductivity and thermal performance. Chemical companies expanding LiFSI production, including Arkema through its Foranext portfolio, have indicated BF3 derivative stabilization via Dimethyl Carbonate complexes as a strategy to minimize electrolyte decomposition under high-voltage cycling. As regulatory frameworks push circularity mandates, producers are also exploring BF3 recycling and solvent recovery systems. Early adoption of closed-loop BF3 handling can create multi-year operating cost advantages and support compliance with EU Battery Regulation requirements on chemical footprint reduction.

Boron Trifluoride Market Share and Segmentation Insights

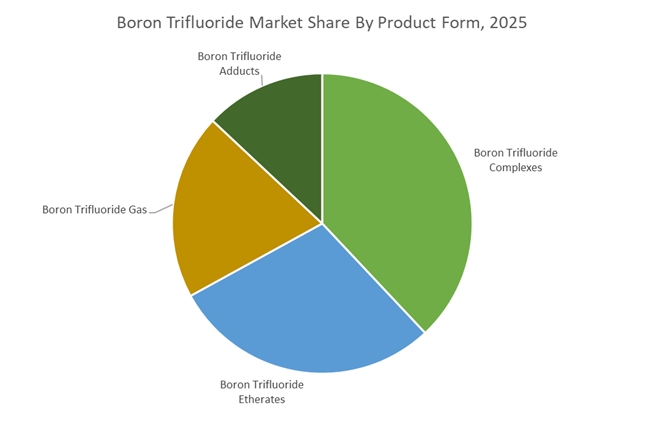

Market Share by Product Form: Complexes Lead Handling Efficiency While High-Purity Gas Serves Electronics

Boron trifluoride complexes account for 38% of the Boron Trifluoride Market in 2025, reflecting their enhanced stability, reduced vapor pressure, and improved handling versus gaseous BF₃. Complexes with amines, alcohols, and organic acids dominate epoxy curing, hydrocarbon resin synthesis, and polyol polymerization, particularly in elevated-temperature curing systems. Boron trifluoride etherates, especially BF₃·OEt₂, represent the second-largest segment, serving as a liquid Lewis acid catalyst in alkylation, esterification, and isomerization reactions closely linked to fine chemical and pharmaceutical intermediate production. High-purity boron trifluoride gas is critical for semiconductor ion implantation, where 99.99% + purity enables controlled p-type doping in silicon wafers, with isotopically enriched variants supporting neutron detection. Boron trifluoride adducts remain niche but are expanding in tailored electrochemical and polymer synthesis formulations, supporting advanced materials innovation.

Market Share by End Use Industry: Chemical Manufacturing Leads as Semiconductor Expansion Accelerates

Chemical manufacturing holds 41% of boron trifluoride demand in 2025, leveraging its strong Lewis acidity in Friedel-Crafts reactions, olefin polymerization, and specialty lubricant synthesis, with volumes tracking industrial production indices. Semiconductor and electronics is the fastest-growing and highest-value segment, driven by advanced node wafer fabrication, ion implantation processes, and 5G infrastructure scaling. Pharmaceuticals and agrochemicals utilize BF₃ etherates for regioselective and stereoselective API and crop protection synthesis, where high purity and catalytic consistency are critical. Petrochemical applications in alkylation and olefin oligomerization remain significant, though solid acid catalyst transitions are gradually reshaping demand. Energy storage is an emerging niche, with BF₃ complexes under evaluation as lithium-ion electrolyte additives to enhance SEI stability and high-voltage cycling performance.

Competitive Landscape of the Boron Trifluoride Market

The global boron trifluoride (BF₃) market in 2026 is being reshaped by accelerating demand from advanced semiconductor manufacturing, pharmaceutical synthesis, specialty polymers, and EV materials. Competition centers on electronic-grade BF₃ gas, high-purity BF₃ complexes, and safe delivery systems, with suppliers differentiating through vertically integrated fluorine chains, catalyst recycling, and fab-ready packaging technologies. Leading players are investing heavily in sub-5nm chip enablement, contract manufacturing for APIs, circular catalyst recovery, and next-generation dopant delivery, positioning BF₃ as a critical intermediate across electronics, agrochemicals, aerospace plastics, and high-performance resins.

Semiconductor-grade BF₃ and integrated fluorination leadership from Honeywell

Honeywell enters 2026 following the spin-off of its Solstice Advanced Materials business, creating a pure-play platform for specialty fluorochemicals, including boron trifluoride. Its flagship Solstice® Electronic Grade BF₃ is refined for sub-5nm semiconductor etching and doping, supporting next-generation AI and logic nodes. Backed by a vertically integrated fluorine supply chain and in-house hydrofluoric acid production, Honeywell ensures price stability amid geopolitical volatility. Strategically focused on “semiconductor enabling materials,” the company pairs BF₃ with proprietary gas-delivery systems to reduce waste and maximize fab uptime, addressing total cost of ownership for global chipmakers while accelerating adoption of advanced fluorination technologies.

High-purity BF₃ complexes and enriched isotopes from Stella Chemifa Corporation

Stella Chemifa remains the world’s leading specialist in high-purity inorganic fluorine compounds and is Japan’s only industrial BF₃ gas producer in 2026. Holding over 35% global share in BF₃ complexes, the company leverages decades of purification expertise. In early 2026, it scaled Enriched ¹¹BF₃ for advanced ion implantation in AI chips, reducing lattice damage versus conventional boron sources. Beyond electronics, Stella Chemifa dominates pharmaceutical and agrochemical catalysis, supplying BF₃ complexes for API synthesis and high-performance resins. Its launch of Steboronine® for BNCT therapy highlights a strategic move into life-saving boron-based pharmaceuticals.

Cost-efficient BF₃ complexes and circular catalyst systems by BASF SE

BASF leverages its Verbund integration to deliver logistically secure BF₃ complexes across Europe and Asia, supporting epoxy curing and polyisobutylene polymerization. Its 2026 portfolio spans phenol, ethylamine, and acetonitrile BF₃ complexes, produced under AI-driven real-time quality monitoring to consistently achieve 99.9% purity for electronics and personal care. Under its Green Verbund strategy, BASF has integrated waste-gas recovery into BF₃ production, cutting environmental impact by nearly 20% versus 2020. The company is also advancing circular catalyst solutions, collaborating with petrochemical majors to recover and recycle BF₃ from spent systems.

Rapidly scaling BF₃ capacity and CDMO integration from Navin Fluorine International Ltd

Navin Fluorine is the fastest-growing BF₃ supplier in 2026, powered by major capital investments and its expanding pharmaceutical CDMO platform. Record Q3 FY26 growth followed commissioning of its cGMP-4 Phase 1 facility, targeting BF₃-enabled specialty chemicals for global drug innovators. Navin is one of the few players offering BF₃ tube trailers and MEGC containers for high-tonnage international transport. A 2026 debottlenecking project at Dahej is boosting BF₃ and specialty fluoride capacity for Europe and North America. Combining Indian cost advantages with advanced R&D in Surat, Navin is emerging as a multi-product platform partner.

Fab-safe BF₃ delivery and dopant optimization by Entegris

Entegris focuses on advanced purity solutions, specializing in the storage, delivery, and performance optimization of BF₃ inside semiconductor fabs. In 2025/2026, it commercialized a precision ¹¹BF₃/H₂ mixture in a single cylinder, extending ion source life by up to 111% by minimizing halogen cycling. Its VAC® vacuum-actuated cylinders have become the 2026 safety standard, releasing BF₃ only under vacuum conditions. Integrated with Entegris’ filtration and purification platforms, BF₃ reaches wafers contaminant-free. Strategically centered on “content per wafer,” Entegris supports AI and 5G architectures through optimized dopant delivery.

Specialty BF₃ intermediates for sustainable polymers from Arkema

Arkema addresses the BF₃ market through high-performance intermediates under its Foranext® range, supplying aerospace and automotive customers with catalysts for advanced plastics and lubricants. In 2026, BF₃ is positioned as a pivotal intermediate for renewable energy and EV battery materials. Arkema has expanded Rilsan® and Luperox® integration, using BF₃ catalysis to produce bio-based high-performance polyamides that enable lightweight mobility. Known for stable BF₃ etherate and gas grades, Arkema specializes in extreme-environment chemistry, where catalyst consistency under variable pressure is essential for next-generation composites and sustainable polymer manufacturing.

China Boron Trifluoride Market: Semiconductor Self-Sufficiency and Cost-Leading BF₃ Ecosystems

China has consolidated its position as the structural anchor of the global boron trifluoride industry, driven overwhelmingly by semiconductor manufacturing and advanced materials synthesis. In November 2025, large-scale operations commenced at the Zhanjiang Verbund site, significantly strengthening localized availability of high-purity intermediates, including BF₃ derivatives critical for electronics-grade applications. This commissioning aligns with China’s dominance as the world’s largest consumer of ¹¹B-enriched boron trifluoride, where semiconductor doping alone accounted for an estimated 96% of domestic BF₃ utilization during the 2024–2025 cycle. The concentration of demand is closely tied to advanced logic and memory fabrication, where ultra-high purity and isotopic precision are mandatory for sub-5 nm process nodes.

Capacity expansion has also moved beyond gases into catalyst-driven specialty chemicals. In late 2025, a high-performance line was inaugurated at the Nanjing Jiangbei New Material Technology Park, leveraging Controlled Free Radical Polymerization pathways that rely on BF₃-based Lewis acid catalyst architectures. Parallel advances in boron isotope separation, announced by Chinese research institutes in mid-2025, have materially reduced the energy intensity required to reach purity thresholds above 99.9 percent, a decisive factor for 2 nm and 3 nm wafer fabrication. Despite new U.S. tariffs introduced in 2025, Chinese exporters have successfully redirected BF₃ volumes toward South Korea and Taiwan, supported by surplus domestic boric acid feedstocks that preserve cost leadership. Beyond electronics, new dispersant lines commissioned in Jiangsu Province have expanded BF₃ consumption in automotive coatings, reinforcing China’s role as both a technology and volume driver.

United States Boron Trifluoride Market: Supply Chain Reshoring and Battery-Oriented BF₃ Innovation

The U.S. boron trifluoride market in 2025–2026 is being reshaped by strategic supply chain fortification and downstream innovation in energy storage. Following tariff implementation in 2025, domestic producers accelerated reshoring initiatives to reduce reliance on Asian imports, prioritizing supply security over spot-price optimization. This structural shift contributed to a measurable rise in the domestic BF₃ price index, reflecting buyer willingness to pay a premium for reliability and regulatory transparency rather than volume-based sourcing.

A notable demand inflection point is emerging from lithium-ion battery manufacturing. Direct company disclosures in August 2025 confirmed expanded use of BF₃ derivatives as electrolyte additives to improve thermal stability and charge efficiency in EV battery cells produced at North American gigafactories. Safety and compliance have become equally critical. In July 2025, Honeywell expanded its automation and gas detection portfolio, integrating specialized BF₃ off-gas monitoring solutions designed for battery and specialty chemical plants. Regulatory oversight has tightened in parallel. Updated EPA Product Stewardship Summaries issued in 2025 now mandate real-time data management and enhanced handling protocols for boron trifluoride compressed gas, directly impacting pharmaceutical synthesis and fine chemical manufacturing across the U.S.

India Boron Trifluoride Market: Export Momentum and BF₃ Utilization in Pharmaceuticals and Agrochemicals

India’s boron trifluoride industry is characterized by export-led price momentum and diversified end-use adoption. In early 2025, the national BF₃ Price Index recorded a double-digit increase, driven by strong export demand from ASEAN semiconductor hubs combined with steady domestic chemical consumption. This pricing strength reflects India’s growing role as a competitive supplier rather than a purely import-dependent market.

Pharmaceutical synthesis remains the backbone of domestic BF₃ demand. As a global hub for generic drug manufacturing, Indian producers continue to rely on BF₃ etherate as a reagent in the synthesis of chronic therapy intermediates, sustaining consumption levels even amid global freight volatility. Beyond pharmaceuticals, agrochemical innovation is opening new demand pathways. Research published in May 2025 by Indian agricultural agencies highlighted the increasing use of BF₃ as a catalyst in bio-based pesticide synthesis, aligning closely with national sustainability and “Make in India” objectives. This dual exposure to export markets and value-added domestic applications positions India as a resilient mid-scale player in the global boron trifluoride value chain.

Japan Boron Trifluoride Market: High-Purity Fluorine Chemistry and Cost Pressure Management

Japan’s boron trifluoride market is tightly linked to semiconductor recovery and the strategic management of high-purity fluorine chemistry. Stella Chemifa reported a strong rebound in its semiconductor segment for the fiscal year ended March 2025, underpinned by renewed wafer demand and increased consumption of electronics-grade BF₃ gas. This recovery has reinforced Japan’s position as a supplier of ultra-high-purity fluorinated gases rather than a volume-driven producer.

Strategic direction is being formalized through Stella Chemifa’s Fourth Medium-Term Management Plan, launched in May 2025, which prioritizes sustainable process improvements and supply assurance for next-generation electronics through 2028. However, Japanese producers are simultaneously navigating feedstock volatility. Rising costs of anhydrous hydrofluoric acid, a critical BF₃ precursor, have triggered price renegotiations with downstream semiconductor manufacturers. This dynamic underscores Japan’s challenge of maintaining purity leadership while absorbing upstream cost inflation.

Germany and the European Union Boron Trifluoride Market: Verbund Optimization and Sustainability-Led Specialization

In Europe, the boron trifluoride industry is evolving through portfolio optimization rather than capacity expansion. In September 2025, major producers initiated strategic reviews at integrated Verbund sites such as Ludwigshafen, progressively phasing out lower-margin legacy chemistries in favor of high-value BF₃ catalysts aligned with the green energy transition. This shift reflects Europe’s broader emphasis on specialty performance chemicals over commodity intermediates.

Regulatory drivers are central to this transition. From mid-2025, enhanced handling and sustainability mandates introduced by the European Chemicals Agency have elevated compliance requirements for boron trifluoride, stimulating innovation in advanced gas containment, recycling, and recovery systems. As a result, European BF₃ production is increasingly differentiated by safety, traceability, and circularity credentials rather than scale, positioning the region as a premium supplier to energy, electronics, and sustainable synthesis markets.

Comparative Overview of Boron Trifluoride Industry Dynamics by Country

Boron Trifluoride market County Level Snapshot

|

Country / Region

|

Primary Demand Anchor

|

Strategic Industry Direction

|

|

China

|

Semiconductor doping, polymer catalysts

|

Isotope enrichment, cost-led export redirection

|

|

United States

|

EV batteries, reshored supply chains

|

Domestic security, safety-driven innovation

|

|

India

|

Pharma synthesis, agrochemicals

|

Export-led pricing with value-added diversification

|

|

Japan

|

High-purity semiconductor gases

|

Purity leadership with feedstock cost management

|

|

Germany / EU

|

Green energy catalysts, compliance

|

Specialty focus, sustainability and containment

|

Boron Trifluoride Market Report Scope

Boron Trifluoride Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$312.6 Million

|

|

Market Size (2034)

|

$497.6 Million

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Product Form (Boron Trifluoride Gas, Boron Trifluoride Etherates, Boron Trifluoride Complexes, Boron Trifluoride Adducts), By Purity Level (Purified Grade, High Purity Grade, Ultra High Purity Grade, Isotope Enriched Grade), By Technology (Complexation Reaction, Gas Phase Reaction, High Pressure Synthesis), By End Use Industry (Semiconductor and Electronics, Chemical Manufacturing, Pharmaceuticals and Agrochemicals, Energy Storage, Petrochemicals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Honeywell International, Arkema, Stella Chemifa, Navin Fluorine International, Linde, Air Liquide, Gulbrandsen, Entegris, Tanfac Industries, 3M, Stella Express, Qingzhou Chenkai Chemical, Wujiang Fugua Chemical, Heyi Gas Global

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Boron Trifluoride Market Segmentation

By Product Form

- Boron Trifluoride Gas

- Boron Trifluoride Etherates

- Boron Trifluoride Complexes

- Boron Trifluoride Adducts

By Purity Level

- Purified Grade

- High Purity Grade

- Ultra High Purity Grade

- Isotope Enriched Grade

By Technology

- Complexation Reaction

- Gas Phase Reaction

- High Pressure Synthesis

By End Use Industry

- Semiconductor and Electronics

- Chemical Manufacturing

- Pharmaceuticals and Agrochemicals

- Energy Storage

- Petrochemicals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Boron Trifluoride Industry

- BASF

- Honeywell International

- Arkema

- Stella Chemifa

- Navin Fluorine International

- Linde

- Air Liquide

- Gulbrandsen

- Entegris

- Tanfac Industries

- 3M

- Stella Express

- Qingzhou Chenkai Chemical

- Wujiang Fugua Chemical

- Heyi Gas Global

*- List not Exhaustive