Market Overview: Brominated Flame Retardants Market Reshaped by EU SVHC Actions, Polymeric BFR Innovation, and EV Electronics Safety Demand (2025–2034)

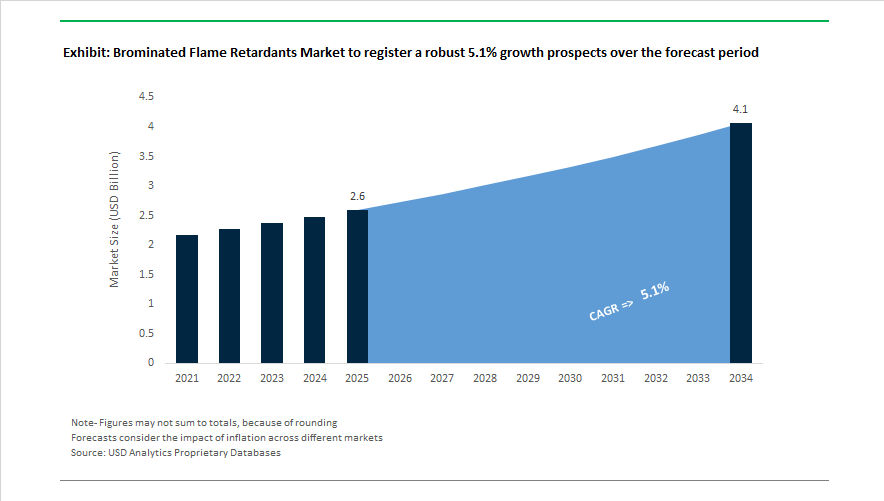

The brominated flame retardants market is projected to expand from USD 2.6 billion in 2025 to USD 4.1 billion by 2034, registering a CAGR of 5.1% supported by demand from electric vehicles, data centers, electronics, and high-performance polymers. Regulatory developments began influencing product strategies in 2024 when the U.S. Environmental Protection Agency advanced risk evaluation for TBBPA, encouraging the transition toward reactive grades chemically bound into epoxy systems for printed circuit boards. In September 2024, Asahi Kasei launched LASTAN flame-retardant nonwoven fabrics for EV battery safety applications, highlighting the expanding role of advanced brominated chemistries in thermal runaway prevention. October 2024 saw Albemarle Corporation introduce SAYTEX ALERO polymeric flame retardant, targeting electrification and data center growth with improved thermal stability and lower lifecycle carbon impact.

Regulatory pressure intensified in late 2025 and early 2026 across Europe. In November 2025, the European Chemicals Agency added DBDPE to the SVHC Candidate List, increasing documentation requirements and signaling potential restrictions. At K 2025 in October 2025, LANXESS introduced Emerald Innovation 5000, a polymeric brominated flame retardant designed to prevent migration and meet future compliance expectations. Supply-side strength was underscored in 2025 when ICL Group confirmed control of 33% of global bromine supply, supporting the shift toward new-generation reactive BFRs that chemically integrate into polymers to enhance recyclability. Albemarle also implemented a $450 million productivity program in November 2025 to sustain competitiveness amid pricing volatility.

Technology and market diversification define the 2026 outlook. In January 2026, ECHA launched a call for evidence toward a group restriction on aromatic brominated flame retardants, signaling broad regulatory harmonization. February 2026 financial updates from Tosoh Corporation showed resilience in advanced materials driven by semiconductor recovery and demand for brominated intermediates. AI-driven dosing systems adopted in Taiwan and South Korea during 2024 and 2025 improved additive dispersion accuracy and reduced polymer batch rejection rates. Meanwhile, ICL expanded R&D into bromine-based electrolytes for long-duration energy storage in 2025, illustrating diversification beyond fire safety applications.

Global Regulatory Acceleration and Aerospace Fire-Safety Standards Reshaping the Brominated Flame Retardants Market

SVHC Expansion and POPs Enforcement Intensify Compliance Pressure on Brominated Flame Retardants

Regulatory tightening is now a global rather than EU-only narrative, forcing manufacturers and downstream OEMs to re-evaluate BFR portfolios. In October 2025, the ECHA Member State Committee agreed to classify Decabromodiphenyl Ethane (DBDPE) as a Substance of Very High Concern, a ruling finalized in November 2025 that immediately triggered mandatory notification for any article containing more than 0.1% by weight. This change places pressure on BFR suppliers and electronics manufacturers, especially those using legacy formulations assumed to be safe post-Deca-BDE phaseout. An additional inflection point arrived on 17 November 2025, when the EU enacted POPs Regulation 2025/1482, reducing the allowable limit for five key PBDEs from 500 mg/kg to 10 mg/kg. The impact extends beyond Europe, as global recycling stakeholders are now confronted with stricter contaminant thresholds that hinder reuse of plastic housings and components in electronics, toys, and automotive applications.

Polymer-Bound BFRs and Reactive Formulations Dominate R&D Pipelines

Industry strategy has shifted toward polymer-integrated and reactive BFR solutions to mitigate leaching and end-of-life ecological concerns associated with additive systems. TBBPA reactive chemistries used in epoxy PCB laminates are already standard practice, but the next phase of innovation is led by polymeric BFRs engineered for full chemical immobilization. Leading suppliers, including ICL Group and LANXESS, emphasized in 2024–2025 technical publications that polymeric BFRs, such as the Emerald Innovation series, are engineered to maintain structural stability across a product’s entire use cycle. Complementing this, new phosphorus-bromine synergistic formulations introduced by LANXESS in late 2024 are specifically tailored for glass fiber-reinforced polyamide components in EV charging infrastructure. These blends support high thermal loads in ultra-fast chargers without the surface migration or discoloration commonly associated with older additive BFRs.

BFRs Remain Critical for Aerospace Composite Fire-Safety Where Alternatives Fail Performance Tests

Advanced aerospace platforms, including electric vertical takeoff and landing aircraft, require flame retardants that meet stringent Fire, Smoke, and Toxicity metrics. Non-halogenated alternatives struggle to deliver equivalent performance in Carbon Fiber Reinforced Polymer systems. Aerospace documentation released in February 2025 reconfirmed that brominated epoxy adhesive films are the only class capable of meeting combined MIL-STD fire resistance and structural adhesion benchmarks for critical-path components. These requirements also extend to military procurement applications, where rapid self-extinguish performance under 10 seconds is mandatory in communication shelters, naval interior systems, and high-voltage equipment cabins. BFR-qualified material lists remain restricted, meaning suppliers that retain aerospace certification can access long-term procurement cycles and customer lock-in.

Bromine Recovery Infrastructure Emerges as the Circular Growth Engine of the Decade

Growing regulatory scrutiny on hazardous waste and pressure to decarbonize chemical feedstocks is increasing demand for closed-loop bromine recapture. Technology developments in membrane separation and ion-exchange processing documented in August 2025 reveal that bromine recovery from WEEE waste is transitioning from pilot testing to industrial deployment. Recovered bromine is already being reintroduced into new flame retardant formulations, reducing dependency on virgin brine extraction and supporting ESG reporting. Strategic financing is also accelerating this shift. The 2025 World Circular Economy Forum identified bromine recovery as a priority segment eligible for EU-backed Global Gateway financing, especially in Latin America and Southeast Asia. Companies committing to take-back programs and closed-loop BFR production are gaining preferential access to sustainability-linked capital and are positioned to benefit from growing circular procurement requirements in electronics and construction sectors.

Brominated Flame Retardants Market Share and Segmentation Insights

Market Share by Product Type: TBBPA Dominates While DBDPE Gains as Replacement Chemistry

Tetrabromobisphenol A commands 42% of the Brominated Flame Retardants Market in 2025, primarily used as a reactive flame retardant in epoxy resins for printed circuit boards and as an additive in ABS and HIPS. Its regulatory acceptance and cost efficiency sustain leadership, with demand closely tied to consumer electronics and automotive PCB output. Decabromodiphenyl ethane represents the second-largest and fastest-growing segment, replacing legacy decaBDE in engineering plastics such as PC/ABS, PBT, and nylon used in connectors and electrical housings. Brominated polymeric flame retardants are expanding under regulatory pressure to reduce bioaccumulation risk, offering non-migrating performance in high-temperature polymers. Brominated carbonates and epoxies serve specialized transparent or high-gloss applications, while hexabromocyclododecane continues structural decline following global phase-out commitments. Brominated phthalates and synergists maintain stable use in PVC and textiles but face substitution by non-halogen alternatives.

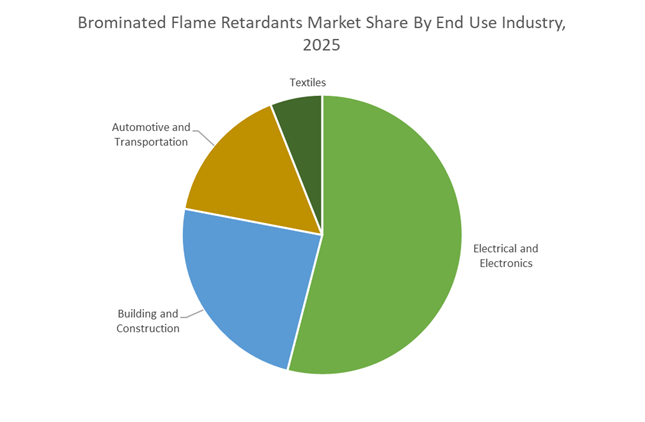

Market Share by End Use Industry: Electronics Anchor Demand as EV Growth Reinforces Automotive Adoption

Electrical and electronics account for 54% of brominated flame retardant consumption in 2025, encompassing PCBs, connectors, enclosures, and wire and cable insulation. Miniaturization, higher power densities, and 5G deployment are intensifying demand for thermally stable, high-performance FR systems, with TBBPA exemptions in PCBs supporting continued usage. Building and construction remains the second-largest segment, transitioning from HBCDD toward polymeric brominated and phosphorus-based systems in insulation and structural panels under evolving fire safety codes. Automotive and transportation is the fastest-growing sector, driven by EV battery enclosures, charging systems, and under-hood electronics requiring thin-wall, high-temperature flame retardancy. Textiles form a declining niche as sustainability commitments and regional regulations encourage phosphorus and mineral-based substitutions.

Competitive Landscape of the Brominated Flame Retardants Market

The global brominated flame retardants (BFR) market in 2026 is being driven by accelerating demand from EV battery systems, electronics housings, 6G infrastructure, construction insulation, and energy storage applications. Competition centers on polymeric and reactive BFRs, low-smoke formulations, and recycling-compatible additives, as manufacturers respond to tightening EU REACH, RoHS, and circular-economy mandates. Market leaders are differentiating through vertical bromine integration, advanced polymer-bound technologies, forensic tracers for recycling, and low-carbon product footprints, positioning BFRs as essential materials for fire-safe, lightweight, and electrically dense systems across automotive, consumer electronics, and grid-scale storage.

Vertical bromine integration and low-carbon SAYTEX® solutions from Albemarle Corporation

Albemarle enters 2026 having repositioned its bromine Specialties segment as a high-margin growth engine supporting its broader energy storage ambitions. Its SAYTEX® portfolio, led by SAYTEX® 8010, is marketed as a low-carbon DBDPE alternative with up to 70% lower footprint versus certain phosphorus competitors. The launch of SAYTEX ALERO™ addresses the highly electrified 2026 landscape, delivering polymeric flame retardancy for automotive and electronics applications requiring durability and environmental safety. Albemarle’s core strength lies in full vertical integration, controlling bromine brine assets in Arkansas and Jordan, while prioritizing recycling-compatible BFRs for smartphones, laptops, and next-generation plastic components.

Lifecycle-driven polymeric BFR platforms from ICL Group

ICL leads the market with its data-driven SAFR® methodology, enabling OEMs to select optimal BFRs using full life-cycle assessment tailored to application risk. In 2026, the company expanded its PolyQuel® polymeric and reactive flame retardants, which chemically bond to PCB and engineering plastic matrices to prevent leaching and enhance long-term performance. ICL dominates EV battery casings and stationary energy storage, delivering thermal stability for high-capacity lithium-ion systems. Its scaled SMX tracer technology allows automated identification of additive concentrations during recycling, reinforcing circular plastics strategies while leveraging Dead Sea bromine resources for consistent global supply.

Reactive and oligomeric BFR leadership from LANXESS AG

LANXESS has built one of the industry’s most comprehensive organic flame retardant portfolios, anchored by the Emerald Innovation® series. Emerald Innovation® 3000 remains the 2026 benchmark polymeric replacement for restricted HBCD in EPS/XPS insulation, while Emerald Innovation® 5000 expands processing flexibility as a next-generation alternative to DBDPE in electronics-grade plastics. Strengthened US distribution through Azelis supports Firemaster® and PHT4 Diol® growth in construction and automotive markets. LANXESS is strategically focused on low-exposure, reactive BFRs with minimal volatility, aligning its portfolio with EU REACH compliance and sustainable building material requirements.

Asian electronic-grade bromine expansion led by Tosoh Corporation

Tosoh anchors Asia’s bromine supply through its Nanyo Complex, which became fully operational in 2026 following a ¥10 billion capacity expansion. As Japan’s largest bromine producer, Tosoh provides just-in-time electronic-grade BFRs for semiconductor housings and emerging 6G infrastructure across Japan, South Korea, and Southeast Asia. Its Flame-Link derivatives meet ultra-low impurity standards for high-frequency applications, while automated bromine recovery upgrades improve margins and environmental performance. Tosoh’s regional dominance and supply reliability position it as a preferred partner for electronics OEMs navigating tight Asian bromine balances.

High-polymerization BFR growth from Shandong Weitai Fine Chemical

Shandong Weitai exemplifies China’s transition from commodity bromine to regulated, export-ready BFRs. Specializing in DBDPE and brominated polystyrene (BPS), the company supplies glass-fiber reinforced polyamides for automotive connectors and premium white goods. Its 2025 R&D center in Binhai Economic Development Zone accelerates development of high-polymerization grades with improved color stability and thermal resistance. Backed by proximity to coastal salt fields, Weitai benefits from a cost-efficient raw material base while targeting UL, RoHS, and SGS compliance to expand penetration in European and North American electronics supply chains.

Low-smoke hybrid systems and additive blending from ADEKA Corporation

ADEKA differentiates through synergistic bromine-based systems that combine chemical suppression with physical heat barriers. In 2026, its intumescent brominated hybrids create expanding char layers for enhanced fire protection, while the ADK STAB range introduces antimony-free packages delivering high CTI for EV charging and electrical components. ADEKA’s additive-blending model provides pre-formulated “one-pack” systems integrating BFRs with UV stabilizers and antioxidants, simplifying customer processing. Targeting high-frequency PCBs and automotive interiors, ADEKA focuses on maintaining mechanical integrity and color stability under intense UV and thermal exposure.

China Brominated Flame Retardants Market: Consolidation-Driven Compliance and Electronics-Centric Demand

China remains the structural backbone of the global brominated flame retardants industry, with its 2025–2026 trajectory defined by environmental consolidation, electronics vertical integration, and regulatory-driven product evolution. As part of intensified “Blue Sky” audits, authorities have centralized bromine extraction and downstream BFR synthesis into three state-sanctioned chemical parks in Shandong Province. This consolidation is not merely administrative. It enables centralized effluent treatment, real-time emissions tracking, and tighter control over bromine handling, effectively phasing out small-scale and non-compliant producers. The deployment of AI-powered isotope monitoring systems by the Shandong Environmental Protection Bureau in mid-2025 further reinforces enforcement, sharply reducing the prevalence of informal backyard BFR synthesis.

Demand fundamentals are anchored in electronics and electric mobility. With China now producing more than 97% of its domestic mobile phone requirements, the supply chain for TBBPA-grade epoxy resins used in printed circuit boards has become highly localized. Simultaneously, the 2025 NEV safety standards have mandated UL94 V-0 performance in EV battery casings without the use of restricted PBDEs. This has accelerated the shift toward polymeric and reactive brominated flame retardants that are chemically bound into polymer matrices. In December 2025, a Jinan University-led consortium commercialized a reactive-type brominated monomer designed to eliminate the leaching risks associated with DBDPE. These compliance and R&D costs have translated directly into export pricing. By January 2026, traders reported a 15% premium on electronic-grade brominated compounds shipped overseas, reflecting higher energy prices and stricter domestic compliance thresholds.

United States Brominated Flame Retardants Market: State-Level Bans and Infrastructure-Led Reformulation

The U.S. brominated flame retardants market is undergoing a rapid structural pivot driven by state prohibitions, federal infrastructure spending, and chemistry reformulation requirements. Effective January 1, 2026, Massachusetts and Rhode Island enacted bans on covered products containing certain flame retardants, including many legacy BFRs used in bedding, carpeting, and children’s products. These state-level actions are forcing manufacturers to transition toward polymeric brominated systems that exhibit lower migration potential and improved toxicological profiles.

At the same time, federal policy is creating selective demand tailwinds. Under the Bipartisan Infrastructure Law, more than $200 million was allocated in 2025 to advanced materials for grid security, incentivizing the use of high-durability brominated insulation in next-generation power transformers and electrical infrastructure. Product innovation is increasingly aligned with broader chemical policy. In April 2025, Albemarle Corporation announced the integration of its SAYTEX® brominated portfolio with PFAS-free formulations, directly addressing the convergence of flame retardant regulation and “forever chemical” bans. Regulatory spillovers are also evident from the EPA SNAP Rule 25, which mandates low-GWP blowing agents in foams. This has indirectly reshaped BFR demand by requiring compatibility with HFO-based systems, pushing suppliers toward reformulated, thermally stable brominated solutions.

Israel Brominated Flame Retardants Market: Resource-Led Leadership and EV Thermal Management

Israel continues to play a disproportionate role in the brominated flame retardants value chain due to its unique access to Dead Sea bromine resources. In February 2025, ICL Group disclosed a $1.3 billion investment across its bromine value chain, aimed at improving extraction efficiency and securing long-term supply leadership. These investments are increasingly paired with sustainability outcomes. ICL’s 2025 ESG disclosures confirmed a 25% reduction in the carbon footprint of bromine production following the conversion of its Sdom facility to hybrid solar-gas power.

Product strategy is closely aligned with electric mobility. In mid-2025, ICL launched the VeriQuel™ series, a reactive brominated solution engineered for the extreme thermal and electrical stresses of EV fast-charging connectors and relays. This positioning reflects a broader shift from commodity flame retardants toward application-specific, high-value systems that combine flame resistance with electrical reliability and long service life.

European Union (Germany / Belgium) Brominated Flame Retardants Market: POP Compliance and Circular Substitution

The European brominated flame retardants market is being reshaped by some of the world’s most stringent chemical regulations, accelerating substitution and circular design. The adoption of Regulation (EU) 2025/1482 in October 2025 drastically reduced the allowable unintentional trace contaminant limit for PBDEs from 500 mg/kg to just 10 mg/kg in new products, with immediate effect. This change has materially altered compliance economics for both domestic producers and importers. The regulatory pressure intensified further in November 2025, when the European Chemicals Agency added DBDPE to the Candidate List of Substances of Very High Concern, triggering mandatory notification and communication obligations across the supply chain.

In response, European producers are accelerating polymeric and recyclable alternatives. At the K 2025 trade fair, Lanxess AG showcased its Emerald Innovation® 5000, a polymeric substitute for deca-BDE designed to withstand multiple mechanical recycling cycles without degrading fire performance. This aligns closely with EU circular economy objectives and positions polymeric BFRs as transitional solutions in high-risk applications where non-halogenated systems are not yet technically viable. Regulatory coordination is also expanding beyond flame retardancy. In December 2025, the EU Biocidal Products Committee initiated reviews of brominated complexes for industrial preservation uses, signaling deeper cross-regulatory scrutiny of bromine chemistry heading into 2026.

Summary of Country-Level Dynamics in the Brominated Flame Retardants Industry

Brominated Flame Retardants Market County Level Snapshot

|

Country / Region

|

Primary Demand Driver

|

Strategic Market Direction

|

|

China

|

Electronics manufacturing, EV safety standards

|

Consolidation, reactive polymeric BFRs, export price premiums

|

|

United States

|

State bans, grid infrastructure investment

|

PFAS-free reformulation, polymeric alternatives

|

|

Israel

|

Dead Sea bromine resources, EV components

|

Resource efficiency, high-value reactive BFRs

|

|

European Union

|

POP and SVHC regulation

|

Circular polymeric substitutes, compliance-led innovation

|

Brominated Flame Retardants Market Report Scope

Brominated Flame Retardants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$4.1 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Product Type (Tetrabromobisphenol A, Decabromodiphenyl Ethane, Brominated Polymeric Flame Retardants, Brominated Carbonates and Epoxies, Hexabromocyclododecane, Brominated Phthalates and Synergists), By Application Method (Reactive Brominated Flame Retardants, Additive Brominated Flame Retardants), By End Use Industry (Electrical and Electronics, Building and Construction, Automotive and Transportation, Textiles), By Polymer Matrix (Epoxy Resins, Polyurethane and Polyisocyanurate, Polystyrene and ABS, Polyolefins, Engineering Plastics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Albemarle Corporation, ICL Group, LANXESS, Shandong Ocean Chemical, Tosoh Corporation, Italmatch Chemicals, ADEKA Corporation, Jiangsu Yoke Technology, Shandong Weifang Longwei Industrial, Kingboard Holdings, Suez, Tata Chemicals, Chemtura, Broseley Chemicals, Perstorp

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Brominated Flame Retardants Market Segmentation

By Product Type

- Tetrabromobisphenol A

- Decabromodiphenyl Ethane

- Brominated Polymeric Flame Retardants

- Brominated Carbonates and Epoxies

- Hexabromocyclododecane

- Brominated Phthalates and Synergists

By Application Method

- Reactive Brominated Flame Retardants

- Additive Brominated Flame Retardants

By End Use Industry

- Electrical and Electronics

- Building and Construction

- Automotive and Transportation

- Textiles

By Polymer Matrix

- Epoxy Resins

- Polyurethane and Polyisocyanurate

- Polystyrene and ABS

- Polyolefins

- Engineering Plastics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Brominated Flame Retardants Industry

- Albemarle Corporation

- ICL Group

- LANXESS

- Shandong Ocean Chemical

- Tosoh Corporation

- Italmatch Chemicals

- ADEKA Corporation

- Jiangsu Yoke Technology

- Shandong Weifang Longwei Industrial

- Kingboard Holdings

- Suez

- Tata Chemicals

- Chemtura

- Broseley Chemicals

- Perstorp

*- List not Exhaustive