Building Asphalt Market Size and Growth Driven by Roofing Demand and Infrastructure Revitalization

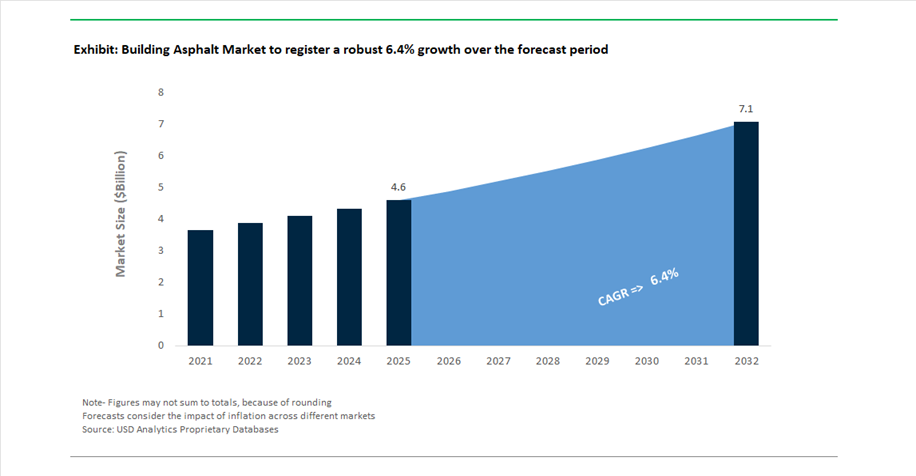

The Building Asphalt Market is projected to grow from USD 4.6 billion in 2025 to USD 7.1 billion by 2032, registering a CAGR of 6.4%. This growth is primarily driven by increasing demand for durable, weather-resistant construction materials, particularly in roofing, waterproofing, and flooring applications across residential and commercial infrastructure.

Building-grade asphalt plays a critical role in roofing shingles, bituminous membranes, and floor tiling systems, offering high durability, water resistance, and cost efficiency. Its ability to withstand extreme weather conditions, UV exposure, and mechanical stress makes it a preferred material in both new construction and renovation projects. The market is benefiting significantly from the revitalization of aging infrastructure and rapid urbanization in emerging economies, where demand for affordable and long-lasting building materials continues to rise.

Technological advancements are enhancing asphalt performance through polymer modification, impact-resistant formulations, and reflective coatings, enabling improved thermal efficiency and structural resilience. The increasing adoption of cool roof technologies and energy-efficient building materials is also driving innovation, with manufacturers developing asphalt products that reduce heat absorption and improve indoor energy performance.

Additionally, regulatory focus on building safety, climate resilience, and sustainability is influencing product development, pushing the industry toward low-emission manufacturing processes and recyclable material systems. Competitive dynamics are shaped by product innovation, capacity expansion, and strong distribution networks, positioning building asphalt as a foundational material in modern construction ecosystems.

Impact-Resistant Shingles, Cool Roof Innovation, and Manufacturing Expansion Transforming Market Dynamics

The building asphalt market is evolving rapidly through product innovation, sustainability initiatives, and strategic capacity expansion. A key development occurred in February 2026, when TAMKO launched the HailGuard™ shingle system, introducing impact-resistant asphalt technology with a dedicated hail warranty. This innovation addresses growing demand in storm-prone regions, where durability and insurance-backed performance are critical purchasing factors.

Product innovation is increasingly focused on aesthetic differentiation and performance enhancement. In January 2026, Owens Corning introduced “Evergreen Mist”, its 2026 Shingle Color of the Year, targeting the premium residential segment with a blend of visual appeal and high-performance asphalt technology. Similarly, GAF’s Bold Definition shingle collection (January 2026) incorporates algae-resistant properties and enhanced wind warranties, reflecting the industry’s focus on long-term durability and reduced maintenance.

Advanced roofing systems are also integrating multi-layer protection technologies. CertainTeed’s FORTIFIED™ Roof certification system (May 2025) combines asphalt shingles with waterproofing underlayments and sealing solutions, creating a comprehensive defense against extreme weather events. This approach highlights the shift toward system-level performance rather than standalone products.

Sustainability and energy efficiency are becoming key differentiators. IKO’s Dynasty® Cool Colors Plus shingles (October 2024) feature solar-reflective granules, reducing roof temperatures and supporting energy-efficient building design. Additionally, Soprema’s award-winning sustainable manufacturing processes (November 2025) demonstrate how asphalt production is evolving to meet environmental and green building standards.

Capacity expansion and operational scaling are reinforcing market growth. IKO’s new manufacturing facility in Texas (July 2025) significantly enhances production capabilities for high-performance asphalt shingles, improving supply responsiveness in high-demand regions. Meanwhile, IKO’s introduction of universal impact resistance ratings (February 2025) establishes a new industry benchmark for durability and product standardization.

Consumer-driven innovation is also shaping the market. TAMKO’s StormFighter FLEX® shingles (June 2025), recognized as Product of the Year, incorporate polymer-modified asphalt for superior impact resistance and installation efficiency, aligning with contractor and homeowner preferences for performance and ease of use.

EU REACH Annex XVII Enforcement Eliminating Coal Tar and Driving High-Purity Asphalt Adoption

The building asphalt industry is undergoing a structural transformation in Europe as regulatory enforcement under REACH Annex XVII accelerates the phase-out of Coal Tar Pitch, High Temperature (CTPHT). Classified as a Substance of Very High Concern due to its carcinogenic polycyclic aromatic hydrocarbon content, coal tar-based roofing systems have effectively been eliminated from new construction projects across the region as of 2026.

The regulatory thresholds are highly restrictive. Asphalt formulations must now maintain PAH concentrations below 0.1% by weight, forcing a full transition toward high-purity petroleum-derived bitumen systems. This shift is not only improving compliance but also enhancing material recyclability. Petroleum-based asphalt membranes can be more safely reprocessed into road construction materials or reused in roofing applications, contributing to a 30% increase in recycling efficiency compared to legacy coal tar systems.

Worker safety improvements are also notable. Construction environments transitioning to coal-tar-free asphalt systems have reported a 50% reduction in VOC exposure during heating and application processes, significantly improving occupational health conditions. At the same time, digital compliance requirements are becoming more stringent. Under 2026 regulations, manufacturers must register asphaltic products containing substances of concern within the SCIP database, introducing a new level of traceability and transparency across the supply chain.

This convergence of chemical safety, recyclability, and digital compliance is redefining material selection in the European asphalt market, positioning high-purity asphalt systems as the standard for modern roofing applications.

U.S. EPA NESHAP Reconsideration Balancing Compliance Costs and Emission Reduction Targets

In contrast to Europe’s strict regulatory tightening, the United States asphalt sector is experiencing a more dynamic policy environment as the Environmental Protection Agency reconsiders the 2024 NESHAP standards for asphalt processing and roofing manufacturing. The regulatory trajectory in 2025–2026 reflects a balance between maintaining emission reduction goals and alleviating capital expenditure burdens on industry operators.

A key development is the potential introduction of a two-year compliance exemption for certain facilities under the Clean Air Act, which could delay the implementation of Maximum Achievable Control Technology requirements. This reconsideration is expected to generate substantial cost savings, with projections indicating a reduction of approximately $1.8 billion in compliance costs over a 15-year period for the U.S. asphalt industry.

Despite this regulatory flexibility, emission control requirements remain in place for new facilities. Updated New Source Performance Standards mandate a 10% to 15% reduction in hazardous air pollutant emissions compared to historical baselines, ensuring continued progress toward environmental targets. Additionally, state-level regulations are maintaining stricter controls in key regions. For example, California’s SCAQMD Rule 1108 enforces VOC limits below 250 g/L for asphaltic primers and underlayments, creating a fragmented regulatory landscape across the country.

Polymer-Modified Bitumen Membranes Enabling High-Performance Green Roof Systems

The rapid expansion of green roofing systems, driven by LEED v5 and urban heat island mitigation policies, is creating strong demand for Polymer-Modified Bitumen membranes. These advanced materials are engineered to provide the durability and flexibility required for vegetated roof applications, where waterproofing systems must withstand mechanical stress from root penetration and environmental exposure.

Modern PMB membranes incorporate Styrene-Butadiene-Styrene modifiers, enabling elongation capacities exceeding 300%, which allows them to accommodate structural movement in large urban buildings. In terms of mechanical performance, these membranes are designed with thicknesses greater than 1.5 millimeters and can withstand puncture forces exceeding 250 Newtons, ensuring long-term integrity in root-intensive environments.

Longevity is a key advantage. PMB-based roofing systems are achieving service lives of 40 to 50 years, outperforming alternative materials such as single-ply TPO membranes by approximately 20% in high-moisture conditions. This extended lifespan reduces lifecycle costs and enhances the economic viability of green roof installations.

From a sustainability perspective, PMB membranes contribute directly to building certification outcomes. Projects utilizing these systems can earn multiple LEED v5 credits under categories such as rainwater management and heat island reduction, reinforcing their value in sustainable construction.

Low-Temperature Self-Adhering Underlayments Expanding Roofing Capabilities in Cold Climates

Cold climate construction presents unique challenges for asphalt roofing systems, particularly in terms of adhesion and installation efficiency. The development of low-temperature self-adhering underlayments is addressing these challenges, creating a new growth opportunity in northern markets.

These advanced underlayments utilize rubberized asphalt formulations that maintain adhesion performance at temperatures as low as -7°C, significantly extending the viable roofing season. This capability allows contractors to continue installations during colder months, increasing productivity and reducing project delays. Industry estimates suggest that this innovation can extend the roofing season by 30 to 45 days annually in colder regions.

Adhesion reliability is a critical performance parameter. Modern self-adhering underlayments achieve peel adhesion values exceeding 2.0 lb/in on plywood substrates, eliminating the need for additional primers or mechanical fastening. This simplifies installation processes and reduces labor requirements, particularly in retrofit applications.

Performance benefits extend to long-term durability. These underlayments provide enhanced protection against ice dam formation, reducing leakage incidents by approximately 40% compared to traditional felt-based systems. Additionally, improved UV resistance—rated for up to 120 to 180 days of exposure—allows projects to remain weather-protected for extended periods before final roofing materials are installed.

Asphalt Paving Mixtures Lead Building Asphalt Market with 51% Share Driven by Global Infrastructure Expansion

Product Category Analysis: Hot Mix Asphalt and RAP Technologies Dominate High-Volume Demand

Asphalt paving mixtures and blocks account for a dominant 51.0% share of the building asphalt market in 2025, driven by their critical role in road construction, airport runways, industrial flooring, and large-scale paving projects. Composed of approximately 95% aggregates and 5% bitumen binder, these materials provide flexibility, load-bearing strength, and waterproofing, making them essential for modern infrastructure. Key growth drivers include massive investments such as the U.S. Infrastructure Investment and Jobs Act (IIJA) and rapid urbanization across Asia and Africa, fueling demand for highways, logistics hubs, and warehouse developments. A major innovation trend is the adoption of Reclaimed Asphalt Pavement (RAP), with 20–50% recycled content, reducing environmental impact and material costs. Additionally, Warm Mix Asphalt (WMA) technologies—now representing over 40% of production in developed markets—lower energy consumption by 30–40%, reinforcing sustainability leadership in the global asphalt construction market.

Roofing & Siding Segment Leads Building Asphalt Market with 42% Share Driven by Durable Weatherproofing Solutions

Application Area Analysis: Asphalt Shingles and Bituminous Membranes Drive Building Envelope Protection

The roofing and siding segment holds a leading 42.0% share of the building asphalt market in 2025, driven by the need for cost-effective, durable, and weather-resistant building envelope solutions. Asphalt-based materials, particularly fiberglass asphalt shingles, dominate residential roofing, covering nearly 80% of homes in North America, with premium architectural shingles offering enhanced durability and 30–50 year warranties. In commercial construction, polymer-modified bituminous membranes (SBS and APP) are widely used for flat and low-slope roofing systems, providing superior flexibility, UV resistance, and thermal stability. The growing adoption of self-adhered membranes is improving installation safety and efficiency by eliminating the need for open flames. Additionally, asphalt-based water-resistive barriers (WRBs) and siding underlays play a critical role in preventing moisture ingress while maintaining breathability. These factors position roofing and siding as the primary growth drivers in the global building asphalt and waterproofing market.

Building Asphalt Market Competitive Landscape Driven by Roofing Innovation, Solar Integration, and High-Performance Shingles

The building asphalt market is highly competitive, driven by laminated asphalt shingles, cool roof technology, and integrated roofing systems. Key players are focusing on fiberglass-reinforced shingles, solar roofing solutions, and digital roofing platforms to enhance durability, sustainability, and contractor efficiency across residential and commercial construction segments.

Owens Corning leads asphalt roofing innovation with fiberglass-reinforced shingles and cool roof technology

Owens Corning dominates the building asphalt industry through its advanced fiberglass-reinforced asphalt shingles and roofing systems. Its TruDefinition Duration shingles set industry benchmarks for geometric complexity and high-performance roofing applications, including complex architectural designs. The company’s fiberglass technology delivers a 15% superior weight-to-durability ratio compared to traditional organic shingles. Strong focus on cool roof shingles enables up to 10% reduction in attic temperatures, supporting energy-efficient building standards. Circular economy integration has reduced production waste by recycling asphalt materials into underlayment systems. Product innovation focuses on durability, thermal efficiency, and sustainable roofing solutions.

GAF drives market leadership with solar shingles and AI-enabled roofing systems

GAF maintains a dominant position in the building asphalt market, particularly in high-performance laminated shingles and smart roofing technologies. Its Timberline Solar shingles integrate solar energy generation directly into roofing systems, positioning the company at the intersection of roofing and renewable energy. The laminated shingle segment is supported by rising demand for climate-resilient roofing. GAF’s AI-driven digital roofing tools deliver 99% accurate material estimation, improving contractor productivity and cost efficiency. The company has incorporated recycled asphalt shingles into 25% of its product volume, strengthening sustainability credentials. Product development focuses on solar integration, digital roofing, and recycled materials.

CertainTeed strengthens premium roofing systems with climate-specific underlayments and algae-resistant technology

CertainTeed leverages Saint-Gobain’s global expertise to lead in premium laminated asphalt shingles and integrated building envelope systems. Its Landmark series captures significant market share within the high-value roofing segment. The launch of climate-specific underlayments addresses extreme temperature fluctuations, enhancing performance in heat-intensive environments. Advanced copper-ion granule technology ensures 25-year algae resistance, maintaining long-term aesthetic performance. Expansion of solar-reflective roofing aligns with California Title 24 green building regulations. Product development focuses on climate resilience, moisture control, and sustainable roofing materials.

IKO Industries expands global footprint with vertically integrated asphalt production and high-wind resistant shingles

IKO Industries is a vertically integrated leader in building asphalt, controlling the full value chain from raw asphalt processing to finished roofing products. Its Cambridge and Dynasty shingles are engineered for high-wind resistance up to 130 mph, addressing demand in storm-prone regions. The company benefits from strong renovation-driven demand, with 65% of market consumption linked to aging housing stock. Vertical integration ensures supply chain resilience and cost control amid raw material volatility. Expansion through a $100 million UK manufacturing facility strengthens its European presence. Product development focuses on durability, wind resistance, and supply chain efficiency.

Beacon Building Products enables market growth through distribution scale and digital procurement platforms

Beacon Building Products plays a critical role in the building asphalt ecosystem as a leading distributor of roofing and construction materials. The company holds significant share in the roofing and insulation distribution market, supported by aggressive acquisitions and regional expansion. Strategic purchases of Passaic Metal and Chicago Metal Supply have strengthened its non-residential roofing footprint. Its Beacon PRO+ digital platform enables real-time tracking of asphalt pricing and project logistics, improving procurement efficiency for contractors. Backed by a $2.25 billion financing structure, Beacon is expanding its distribution network across North America. Business strategy focuses on digital integration, supply chain optimization, and market expansion.

United States Building Asphalt Market: Warm Mix Adoption and Mega Infrastructure Projects Driving Demand

The United States building asphalt market is undergoing a structural shift toward sustainable paving technologies, particularly Warm Mix Asphalt (WMA) and Reclaimed Asphalt Pavement (RAP). Regulatory mandates across more than 15 state DOTs now favor WMA for urban projects, delivering ~20% lower greenhouse gas emissions during production. This shift aligns with federal “Buy America” policies and decarbonization goals.

Large-scale infrastructure projects are key demand drivers. The $30 billion LAX modernization program is utilizing high-performance asphalt capable of handling extreme aircraft loads, while expansions at Portland and Pittsburgh airports are boosting demand for fuel-resistant specialty binders. Technological advancements such as polymer-modified rejuvenators are enabling RAP content above 40% without compromising durability. Additionally, market consolidation—highlighted by Quikrete’s acquisition of Summit Materials—is strengthening vertically integrated supply chains, with public sector projects accounting for over 55% of demand.

China Building Asphalt Market: Belt & Road Expansion and Refinery Transformation Reshaping Supply Dynamics

China leads the global building asphalt market through its Belt and Road Initiative (BRI), which reached $128.4 billion in construction contracts in 2025, driving export demand for asphalt materials and machinery. However, the domestic market is undergoing a structural shift as refineries transition toward oil-to-chemicals production, reducing asphalt output to prioritize higher-margin products.

This supply-side adjustment is balancing demand fluctuations caused by the real estate slowdown, which has led to a 16% decline in waterproofing asphalt consumption. Despite this, innovation remains strong, with national R&D programs focused on carbon-capturing asphalt binders derived from industrial emissions. Strategic inventory drawdowns and the commissioning of the Yulongdao Petrochemical facility in 2026 are expected to stabilize the supply-demand balance, reinforcing China’s global influence.

Saudi Arabia Building Asphalt Market: Smart City Integration and Desert-Grade Paving Driving Growth

Saudi Arabia is emerging as a global hub for desert-terrain asphalt technologies, driven by Vision 2030 and large-scale smart city projects. The Riyadh Ring Road Phase II (SAR 8 billion) is a major driver, requiring specialized asphalt mixes with anti-rutting additives to withstand extreme heat and unstable terrain.

Innovation is centered on smart infrastructure. Asphalt embedded with IoT sensors is being deployed in projects worth over $13 billion, enabling real-time monitoring of traffic and pavement conditions. The adoption of GPS-integrated paving systems is improving efficiency and reducing material waste by 12%. Additionally, stricter VOC regulations are encouraging the use of cold-mix asphalt near residential zones, positioning Saudi Arabia as a leader in high-performance, climate-resilient paving solutions.

Germany Building Asphalt Market: Self-Healing Surfaces and Circular Economy Leadership

Germany remains the European benchmark for sustainable asphalt technologies, particularly in recycling and energy-efficient production. The country has mandated Warm Mix Asphalt (WMA) for federal urban projects, significantly reducing energy consumption across the construction sector.

Technological advancements are redefining durability. The development of induction-based self-healing asphalt, incorporating steel fibers and bitumen capsules, allows micro-cracks to be repaired using mobile induction heating systems. Germany is also leading in bio-asphalt commercialization, utilizing lignin-based binders to reduce dependence on fossil fuels. Investments in IoT-enabled smart roads are further enhancing predictive maintenance capabilities, reinforcing Germany’s leadership in next-generation asphalt technologies.

India Building Asphalt Market: Green Leapfrog and Plastic-Asphalt Integration Driving Rapid Expansion

India is experiencing a “green leapfrog” in the building asphalt market, rapidly adopting high-performance and sustainable paving solutions. Under NHAI programs, national highway development has reached ~70% completion (2024–2026 cycle), driving massive demand for durable asphalt materials.

Innovation is strongly focused on sustainability and longevity. India leads globally in plastic-asphalt integration, with mandates requiring waste plastic in urban road resurfacing to reduce environmental impact. Additionally, new guidelines from MoRTH promote Warm Mix Asphalt for high-altitude regions, improving workability in challenging climates. Investments in port connectivity under the Sagarmala program are also increasing demand for high-stiffness asphalt mixes for heavy freight traffic. These developments position India as one of the fastest-growing markets globally.

Ireland Building Asphalt Market: Ultra-High RAP Innovation and Zero-Waste Paving Leadership

Although smaller in scale, Ireland is a global innovation leader in next-generation asphalt technologies. A major breakthrough was achieved in 2025 with the successful deployment of asphalt containing 70% reclaimed asphalt pavement (RAP), enabled by advanced rejuvenators.

The country is also pioneering sustainability. The use of lignin-based bio-binders is reducing carbon intensity, while asphalt plants powered by renewable energy and hydrotreated vegetable oil (HVO) have achieved up to 94% CO₂ reduction. Innovations such as intelligent compaction systems are optimizing pavement density and durability in real time. Ireland’s zero-waste approach—achieving 100% recycling of reclaimed materials—is setting new global benchmarks and influencing larger markets like the U.S. and UK.

Building Asphalt Market Report Scope

Building Asphalt Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.6 Billion

|

|

Market Size (2032)

|

$7.1 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Product Category (Asphalt Paving Mixtures and Blocks, Prepared Asphalt and Tar Roofing, Asphalt Shingles, Roofing Asphalts, Pitches and Coatings, Bituminous Membranes), By Material (Traditional Bitumen, Polymer-Modified Bitumen, Oxidized Asphalt, Bio-based Asphalt Binders, Emulsified Asphalt), By Technology (Hot Mix Asphalt, Warm Mix Asphalt, Cold Mix Asphalt), By Application Area (Roofing and Siding, Waterproofing and Damp-proofing, Flooring and Sound Insulation, Non-Building Paving, Pipe Coatings and Specialized Linings), By End-Use Sector (Residential Construction, Commercial and Institutional, Industrial)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shell plc, Exxon Mobil Corporation, Owens Corning, GAF, CertainTeed, TotalEnergies SE, Sika AG, Marathon Petroleum Corporation, BP p.l.c., Nynas AB, Sinopec, Indian Oil Corporation Limited, IKO Industries Ltd., Tamko Building Products, LLC, Valero Energy Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Building Asphalt Market Segmentation

By Product Category

- Asphalt Paving Mixtures and Blocks

- Prepared Asphalt and Tar Roofing

- Asphalt Shingles

- Roofing Asphalts, Pitches and Coatings

- Bituminous Membranes

By Material

- Traditional Bitumen

- Polymer-Modified Bitumen

- Oxidized Asphalt

- Bio-based Asphalt Binders

- Emulsified Asphalt

By Technology

- Hot Mix Asphalt

- Warm Mix Asphalt

- Cold Mix Asphalt

By Application Area

- Roofing and Siding

- Waterproofing and Damp-proofing

- Flooring and Sound Insulation

- Non-Building Paving

- Pipe Coatings and Specialized Linings

By End-Use Sector

- Residential Construction

- Commercial and Institutional

- Industrial

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Building Asphalt Market

- Shell plc

- Exxon Mobil Corporation

- Owens Corning

- GAF

- CertainTeed

- TotalEnergies SE

- Sika AG

- Marathon Petroleum Corporation

- BP p.l.c.

- Nynas AB

- Sinopec

- Indian Oil Corporation Limited

- IKO Industries Ltd.

- Tamko Building Products, LLC

- Valero Energy Corporation

*- List not Exhaustive

Table of Contents: Building Asphalt Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Building Asphalt Market Landscape & Outlook (2025–2032)

2.1. Introduction to Building Asphalt Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Market Drivers: Roofing Demand, Infrastructure Revitalization, and Urbanization

2.4. Regulatory Landscape: REACH Compliance, NESHAP Policies, and Sustainability Mandates

2.5. Technology Advancements: Polymer-Modified Asphalt, Cool Roof Systems, and Reflective Coatings

3. Innovations Reshaping the Building Asphalt Market

3.1. Trend: Impact-Resistant Shingles and High-Durability Roofing Systems

3.2. Trend: Cool Roof Technologies and Energy-Efficient Asphalt Solutions

3.3. Opportunity: Green Roofing Systems with Polymer-Modified Bitumen Membranes

3.4. Opportunity: Low-Temperature Self-Adhering Roofing Underlayments for Cold Climates

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Building Asphalt Market

5.1. By Product Category

5.1.1. Asphalt Paving Mixtures and Blocks

5.1.2. Prepared Asphalt and Tar Roofing

5.1.3. Asphalt Shingles

5.1.4. Roofing Asphalts, Pitches and Coatings

5.1.5. Bituminous Membranes

5.2. By Material

5.2.1. Traditional Bitumen

5.2.2. Polymer-Modified Bitumen

5.2.3. Oxidized Asphalt

5.2.4. Bio-based Asphalt Binders

5.2.5. Emulsified Asphalt

5.3. By Technology

5.3.1. Hot Mix Asphalt

5.3.2. Warm Mix Asphalt

5.3.3. Cold Mix Asphalt

5.4. By Application Area

5.4.1. Roofing and Siding

5.4.2. Waterproofing and Damp-proofing

5.4.3. Flooring and Sound Insulation

5.4.4. Non-Building Paving

5.4.5. Pipe Coatings and Specialized Linings

5.5. By End-Use Sector

5.5.1. Residential Construction

5.5.2. Commercial and Institutional

5.5.3. Industrial

6. Country Analysis and Outlook of Building Asphalt Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Building Asphalt Market Size Outlook by Region (2025–2032)

7.1. North America Building Asphalt Market Size Outlook to 2032

7.1.1. By Product Category

7.1.2. By Material

7.1.3. By Technology

7.1.4. By Application Area

7.1.5. By End-Use Sector

7.2. Europe Building Asphalt Market Size Outlook to 2032

7.2.1. By Product Category

7.2.2. By Material

7.2.3. By Technology

7.2.4. By Application Area

7.2.5. By End-Use Sector

7.3. Asia Pacific Building Asphalt Market Size Outlook to 2032

7.3.1. By Product Category

7.3.2. By Material

7.3.3. By Technology

7.3.4. By Application Area

7.3.5. By End-Use Sector

7.4. South America Building Asphalt Market Size Outlook to 2032

7.4.1. By Product Category

7.4.2. By Material

7.4.3. By Technology

7.4.4. By Application Area

7.4.5. By End-Use Sector

7.5. Middle East and Africa Building Asphalt Market Size Outlook to 2032

7.5.1. By Product Category

7.5.2. By Material

7.5.3. By Technology

7.5.4. By Application Area

7.5.5. By End-Use Sector

8. Company Profiles: Leading Players in the Building Asphalt Market

8.1. Shell plc

8.2. Exxon Mobil Corporation

8.3. Owens Corning

8.4. GAF

8.5. CertainTeed

8.6. TotalEnergies SE

8.7. Sika AG

8.8. Marathon Petroleum Corporation

8.9. BP p.l.c.

8.10. Nynas AB

8.11. Sinopec

8.12. Indian Oil Corporation Limited

8.13. IKO Industries Ltd.

8.14. Tamko Building Products, LLC

8.15. Valero Energy Corporation

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures