Cat Food Market Analysis: Premiumization, Functional Nutrition, and Sustainable Proteins

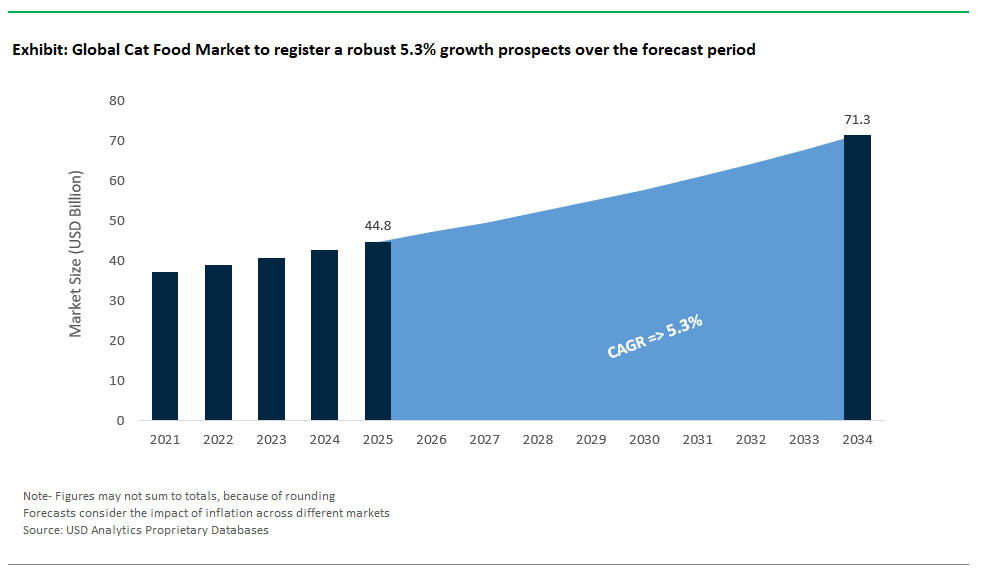

The Global Cat Food Market Size is estimated at $44.8 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 5.3% to reach $71.3 Billion by 2034.

The cat food market is seeing remarkable momentum as global companies expand, innovate, and respond to evolving pet owner demands. In July 2025, WH Group, a major international food company, made a significant move by acquiring Pupil Foods, a leading Polish manufacturer of wet and dry cat and dog foods. This acquisition marks WH Group’s direct entry into the European cat food sector, with Pupil Foods already serving prominent markets such as the UK, Germany, Hungary, and Serbia. Meanwhile, General Mills is set to launch the premium European brand Edgard & Cooper in the U.S. market, offering American cat owners fresh, real-ingredient recipes through an exclusive partnership with PetSmart a testament to the global expansion of high-quality, transparent pet nutrition.

Innovation in cat food is accelerating, with brands introducing science-driven and sustainable solutions. In April 2024, Go! Solutions unveiled its "Hairball Control + Urinary Care" cat food, developed alongside Board-Certified Veterinary Nutritionists to specifically address common feline health challenges. A major leap forward in sustainable proteins came from the UK, where Meatly created the world’s first cat food cans using cultivated chicken meat, and Omni introduced a nutritionally complete cat food with cultivated chicken, supporting environmentally conscious and ethical choices for cat owners. At the same time, Turkish company Tropikal Pet (with brands Goody and Champion) secured $9 million in investment to double export sales, ramp up production, and launch new products including a targeted U.S. entry highlighting global investor confidence in the sector’s growth.

Premiumization and functional nutrition are key drivers shaping the modern cat food market. Vafo’s Brit brand launched "Brit Care Cat RAW Treats," emphasizing super-premium quality and tailored nutrition for feline well-being. Pet Honesty expanded its functional treat portfolio with new dental chews designed to support feline oral health, while Tiki Cat introduced a product range for kittens, ensuring optimal nutrition for cats at every life stage. Collectively, these developments reveal a vibrant and innovative market, where brands are competing to deliver specialized, science-backed, and sustainable solutions that cater to the unique needs of cats worldwide.

Innovations Reshaping the Cat Food Market

Trend: Packaging Material Innovation to Reduce Feline Hyperthyroidism Risk

The cat food market is experiencing a notable shift toward safer packaging innovations aimed at reducing the risk of feline hyperthyroidism, a growing concern among pet owners and veterinarians. Research has shown that cats fed from BPA-lined cans exhibit higher thyroid hormone levels compared to those eating from glass or ceramic containers, highlighting the link between packaging materials and endocrine health. This insight is driving a major reformulation trend across the wet cat food industry, where leading brands are moving away from traditional bisphenol-containing linings to safer alternatives, such as BPA-free, recyclable, and bio-based materials.

Regulatory pressure is amplifying this trend. The European Union’s upcoming 2025 ban on bisphenols in food packaging is accelerating innovation, compelling manufacturers to adopt safer packaging that complies with strict health and sustainability standards. This transition not only addresses consumer demand for transparency and safety but also aligns with a larger industry movement toward environmentally responsible solutions. As more pet owners prioritize both pet health and eco-friendly choices, packaging innovation is emerging as a critical differentiator in the competitive cat food landscape, creating opportunities for brands that lead in compliance and innovation.

Opportunity: High-Moisture Diets for Senior Cats with Chronic Dehydration

High-moisture diets represent a significant untapped opportunity in the cat food market, especially for aging cats vulnerable to chronic dehydration a condition commonly associated with chronic kidney disease (CKD) and other age-related health issues. Cats over the age of 12 are particularly prone to subclinical dehydration, which can exacerbate existing medical conditions and compromise overall health. Veterinary studies confirm that incorporating hydrating solutions such as nutrient-rich broths, gels, and wet food formats significantly improves water intake, supporting better kidney function and overall wellness in senior felines.

Despite the clear health benefits and rising awareness of hydration-focused nutrition, this segment remains underpenetrated, signaling a large gap between consumer need and market availability. Brands that develop palatable, nutritionally balanced high-moisture diets stand to gain a strong foothold in this underserved niche. Educational campaigns highlighting the role of hydration in feline health, paired with innovative product formats, can drive consumer adoption and unlock considerable revenue potential. As pet owners increasingly seek targeted nutritional solutions for aging cats, high-moisture diets are positioned to become a key growth driver in the premium and veterinary-recommended cat food category.

Competitive Landscape: Cat Food Market

The global cat food market is highly competitive and innovation-driven, with leading brands investing in premiumization, functional health benefits, and sustainability. The growing trend of pet humanization, coupled with rising demand for tailored nutrition and gourmet experiences, is reshaping the product landscape. Key players are differentiating through science-backed formulations, breed-specific diets, natural ingredient transparency, and eco-friendly packaging, while also leveraging e-commerce and omni-channel distribution to reach pet parents globally.

Mars Petcare – Diverse Portfolio Driving Premium and Everyday Nutrition

Mars Petcare dominates the cat food market with powerhouse brands like Whiskas, Royal Canin, and Sheba, covering every segment from value to premium. Whiskas offers complete and balanced everyday nutrition through dry kibble, wet food pouches, and treats, appealing to affordability-conscious consumers. Royal Canin leads the science-based premium category, delivering breed-specific, life-stage, and veterinary therapeutic diets tailored to unique feline needs such as urinary health, digestive support, and weight control. Sheba, positioned as a luxury wet cat food brand, focuses on indulgent textures and high-quality ingredients for discerning cat owners seeking a gourmet experience. Mars is aggressively pursuing sustainability initiatives, aiming for 100% recyclable packaging and reduced virgin plastic by 2025, and spearheading innovation programs to develop future-ready, sustainable nutrition solutions. Strategic campaigns like "Feed Them Like Cats and Dogs" reinforce their leadership in pet education, while AI-driven health research and collaborations position Mars as an innovation leader in the feline nutrition space.

Nestlé Purina – Premium Innovation and Ingredient Transparency

Nestlé Purina remains a global powerhouse with flagship brands like Fancy Feast, Purina ONE, and Felix, catering to premium, health-conscious, and mass-market consumers. Fancy Feast dominates the gourmet wet cat food segment with varied textures and flavors, while Purina ONE emphasizes real meat-first formulas with probiotics, addressing digestive health, indoor cat needs, and sensitive systems. Felix, popular in Europe, offers a playful, flavor-rich wet food portfolio appealing to variety-seeking owners. Purina is driving premiumization through innovative product formats, including pyramid-shaped wet food under Fancy Feast Gems and Gourmet Revelations, designed for portion control and feline feeding behavior. Sustainability remains a core priority, with 100% recyclable packaging by 2025 and alternative protein exploration. Purina’s R&D strength, coupled with breakthroughs in functional nutrition (allergen reduction, mental acuity), keeps the brand ahead in meeting health-conscious and eco-aware consumer demands.

Hill’s Pet Nutrition – Veterinary-Recommended Precision Diets

Hill’s Pet Nutrition, under Colgate-Palmolive, commands strong credibility with its vet-recommended, science-driven cat food lines, Science Diet and Prescription Diet. Science Diet offers advanced everyday nutrition targeting specific needs like hairball control, sensitive digestion, and oral health, while Prescription Diet provides therapeutic solutions for conditions such as kidney disease, urinary health, obesity, and hyperthyroidism. Hill’s innovation pipeline includes ActivBiome+ Multi-Benefit technology, developed from a decade of microbiome research to support digestive and immune health. Strategic initiatives like the "World of the Cat Report" and partnerships with rescue organizations underscore Hill’s commitment to feline welfare and education. With significant investments in R&D and manufacturing facilities, coupled with a strong veterinary network, Hill’s continues to dominate the clinical nutrition segment, addressing the rising demand for personalized, health-oriented diets.

Blue Buffalo (General Mills) – Natural, Holistic, and Fresh Nutrition Leader

Blue Buffalo has carved a niche as a natural, clean-label brand, focusing on high-quality proteins, grain-free options, and limited-ingredient diets free from corn, wheat, and artificial additives. Core lines like BLUE Tastefuls, BLUE Wilderness, and BLUE Basics cater to different nutritional needs, from picky eaters to cats with food sensitivities. With growing consumer interest in minimally processed and fresh pet food, Blue Buffalo launched Love Made Fresh in 2025, entering the fresh segment to complement its dry and wet offerings. The acquisition of Edgard & Cooper, a European premium pet food brand, further strengthens its position in the premium and sustainable nutrition space, with expansion plans into the U.S. Through integrated marketing campaigns like "One Taste is All It Takes", Blue Buffalo leverages its natural positioning and flavor variety to capture health-conscious pet parents, aligning with the trend of pet food humanization.

J.M. Smucker – Value Leadership with Meow Mix

Post-divestiture of brands like 9Lives and Rachael Ray Nutrish, J.M. Smucker’s cat food strategy centers on Meow Mix, a trusted name in the value segment. Known for its catchy branding and wide flavor assortment, Meow Mix offers dry and wet food formulations that balance affordability with essential nutrition, making it a staple for cost-conscious households. The brand’s emphasis on flavor variety and convenience packaging keeps it relevant in the competitive economy-tier segment. With demand for Meow Mix outpacing production in recent quarters, J.M. Smucker is investing in capacity expansion and innovation within its core product line, aiming to maintain dominance in the mainstream category while optimizing portfolio performance.

Market Share and Segmentation Insights: Cat Food Market

By Product: Wet Cat Food Leads, Raw Diets Show Fastest Growth

Wet Cat Food holds the largest share at 44.6% in 2025, driven by premiumization trends and its alignment with feline hydration needs, as cats naturally consume low amounts of water. Dry Cat Food (Kibble) remains a strong alternative for convenience and affordability but grows slower due to rising obesity concerns. Cat Treats & Snacks are gaining traction as pet parents seek functional and indulgent options such as dental care treats. Among emerging formats, Raw Food is the fastest-growing segment with a CAGR of 6.1%, reflecting growing interest in biologically appropriate diets for better feline health. Veterinary and therapeutic diets are also gaining popularity for managing specific conditions, while niche products like freeze-dried, frozen, and semi-moist foods cater to specialized feeding preferences.

By Source: Animal-Derived Dominates, Insect Protein Accelerates Rapidly

Animal-Derived ingredients dominate with the largest share of 80.2% in 2025, supported by the high-protein requirements of obligate carnivores. This segment remains the foundation of premium and mainstream formulations with poultry, fish, and meat-based ingredients. Plant-Derived options are expanding moderately as part of grain-free and limited-ingredient diets, attracting eco-conscious and allergy-sensitive consumers. The most dynamic growth comes from Insect-Derived protein, the fastest-growing source at a CAGR of 6.9%, fueled by sustainability goals and regulatory approvals for innovative proteins like crickets and black soldier fly larvae.

United States: Wet Cat Food Dominance and Functional Innovation Propel Market Growth

The United States cat food market is characterized by the clear dominance of wet food, which accounts for a significant share of overall sales. This trend is driven by a growing understanding among cat owners of the importance of moisture-rich diets that support feline hydration, especially for cats prone to urinary and kidney issues. Major manufacturers, such as Mars Petcare’s TEMPTATIONS Brand, have responded with continual product innovation introducing premium wet recipes designed to promote muscle strength and overall feline health. The market is also witnessing the emergence of plant-based and alternative protein cat foods, with companies like Wild Earth launching nutritionally complete vegan options to meet the needs of sustainability-focused consumers.

Humanization and premiumization are stronger than ever, as 70% of U.S. households now own pets, fueling increased spending on high-quality and specialized nutrition. E-commerce is accelerating market expansion, with platforms like Amazon and Walmart making a wide selection of specialty cat foods more accessible to consumers across the country. The convergence of convenience, functional formulation, and a focus on pet wellness ensures that the U.S. cat food market continues to innovate and grow, catering to the evolving preferences of modern pet owners.

China: Urbanization, Premium Imports, and E-Commerce Drive Cat Food Market Expansion

China’s cat food market is rapidly expanding, underpinned by the nation’s growing pet economy, which reached $41.9 billion in 2024. Cat ownership is rising swiftly, particularly in urban environments where cats are viewed as more convenient pets for small apartments. This demographic shift fuels demand for easy-to-serve, nutritionally balanced, and hygienic cat food options. Chinese consumers increasingly favor premium and imported cat food, especially from countries with reputations for quality and safety. In 2024, U.S. pet food exports to China soared to $296.6 million, underscoring the sustained appetite for high-end nutrition.

E-commerce is the primary sales channel, with Tmall, Taobao, JD.com, and TikTok dominating the market by providing authenticity, variety, and convenience. As domestic brands gain ground, they are focusing on clean labels, grain-free options, and functional formulations tailored to local preferences. The result is a competitive, digitally driven cat food sector marked by continuous innovation, rapid growth, and rising standards for quality and safety.

Germany: Premium, Sustainable, and Functional Cat Food Leads Market Preferences

Germany’s cat food market is defined by a strong preference for superior, premium-quality products that emphasize sustainability and health. German consumers are particularly focused on natural ingredients and transparent formulations, driving demand for products with “no additives or preservatives” claims. Wet cat food remains especially popular, favored for its moisture content and palatability, aligning with the dietary instincts and preferences of cats.

There is also increasing demand for tailored nutrition addressing specific needs, such as sensitive stomachs, hairball control, and different life stages. The trend towards clean-label and eco-friendly packaging further cements Germany’s reputation for environmentally conscious consumption. With high veterinary involvement in purchase decisions and a culture that values animal welfare, Germany remains at the forefront of innovation and quality in the European cat food market.

United Kingdom: Cultivated Protein and Vegan Innovation Highlight UK Cat Food Market

The United Kingdom is at the cutting edge of cat food innovation, with companies like Meatly unveiling the world’s first cultivated chicken cat food in March 2024. This step toward sustainable, novel protein sources reflects the UK’s progressive stance on animal welfare and environmental responsibility. Alongside this, vegan cat food launches such as those from Omni demonstrate a growing niche for plant-based and alternative diets, appealing to eco-conscious consumers.

UK pet owners are also demanding products with proven health benefits, such as hydration support and dental care, with manufacturers responding through functional formulations. The rapid growth of e-commerce, projected at an annual rate of 12.6% by 2025, is making specialized and premium products widely available. This dynamic mix of scientific innovation, ethical consumption, and convenience ensures that the UK cat food market remains a leader in both growth and responsible product development.

Japan: Specialized Senior Diets, Flavor Innovation, and Nutritional Focus Shape Cat Food Market

Japan’s cat food market stands out for its focus on specialized diets, particularly for an aging cat population that requires targeted support for kidney health, joint function, and cognitive wellness. Japanese consumers show a marked preference for wet cat foods including canned and pouch varieties due to their palatability and ability to promote hydration.

Regional flavor innovation is another defining feature, with an emphasis on unique tastes such as scallop, cod, and bonito, driving new product launches. Japanese pet owners place a premium on complete and balanced nutrition, fueling robust growth in products emphasizing holistic health claims. With a meticulous approach to dietary needs and a strong emphasis on product quality, Japan’s cat food market remains highly differentiated and resilient.

Canada: Natural Formulations, Health-Driven Innovation, and Sustainability Shape Cat Food Trends

Canada’s cat food market reflects a rising demand for natural and limited ingredient diets, as cat owners seek to address sensitivities and provide clear, transparent nutrition. Brands like ORIJEN have responded with specialized formulas targeting multiple health benefits, such as immune and digestive support, indicating a trend toward holistic well-being. Sustainability is also becoming central, with Canadian manufacturers investing in recyclable and compostable packaging solutions to meet growing environmental expectations.

Raw and freeze-dried cat foods are increasing in popularity, offering perceived nutritional advantages and appealing to consumers seeking less processed options. The Canadian market, with its strong focus on health, wellness, and responsible sourcing, is well positioned for ongoing innovation and growth.

Australia: High Cat Ownership and Fresh, Functional Diets Drive Market Momentum

Australia’s robust pet ownership rates are fueling substantial growth in the cat food segment. Demand is rising for raw, biologically appropriate diets, as illustrated by launches from local companies like Tuckers Natural. Australian consumers are particularly focused on digestive and allergy support, seeking formulations that address common health concerns while delivering high-quality, locally sourced ingredients.

The trend towards “Buy Australian” is gaining momentum, with consumers valuing freshness and quality assurance alongside support for domestic producers. These factors, combined with a growing interest in raw and fresh diets, are shaping a vibrant and forward-thinking Australian cat food market.

France: Premium Wet Food, Natural Ingredients, and Veterinary Guidance Drive Cat Food Market

French cat owners are embracing premium wet food products that align with the trend of pet humanization and a desire to provide gourmet, high-quality meals. The market is seeing strong growth in natural and hypoallergenic formulations, catering to cats with sensitivities and reflecting a broader demand for clean-label products. Veterinary guidance plays a pivotal role in product selection, with many French consumers relying on professional recommendations for therapeutic and specialty diets.

Sustainability is increasingly important, with brands adopting responsible sourcing and eco-friendly packaging initiatives to align with consumer expectations. France’s cat food market, shaped by premiumization, wellness, and environmental responsibility, continues to advance rapidly in both quality and innovation.

Cat Food Market Report Scope

Cat Food Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$44.8 Billion

|

|

Market Size (2034)

|

$71.3 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Product (Wet Cat Food, Dry Cat Food (Kibble), Cat Treats & Snacks, Dehydrated Food, Freeze-Dried Food, Frozen Food, Raw Food, Semi-Moist Food, Powder, Veterinary Diets/Therapeutic Diets), By Nature (Organic, Natural, Conventional, Monoprotein, Limited Ingredient Diets (LID), Hypoallergenic, Human-Grade), By Source (Animal-Derived, Plant-Derived, Insect-Derived), By Application (Kitten, Adult, Senior, All Lifestages), By Pricing (Mass Market/Economy, Premium, Super Premium/Ultra-Premium, Therapeutic/Veterinary), By Distribution Channel (Specialty Pet Stores, Supermarkets & Hypermarkets, Veterinary Clinics & Pharmacies, E-commerce Platforms)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mars Petcare Inc., Nestlé Purina PetCare, Hill's Pet Nutrition, Blue Buffalo Company, Ltd., The J.M. Smucker Company, Diamond Pet Foods, WellPet LLC, Farmina Pet Foods, Arden Grange, Orijen / Acana (Champion Petfoods - owned By Mars), Affinity Petcare S.A., Heristo AG, Unicharm Corporation, Petcurean Pet Nutrition, Instinct Pet Food (formerly Nature's Variety), FreshPet, Stella & Chewy's, Fussie Cat (Pets Global), Open Farm, Caru Pet Food, Tiki Pets, Nutramax Laboratories, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cat Food Market Segmentation

By Product

- Wet Cat Food

- Dry Cat Food (Kibble)

- Grain-Free Kibble

- Traditional Kibble (with grains)

- Cat Treats & Snacks

- Training Treats

- Dental Chews

- Freeze-Dried Treats

- Soft Chews/Purees

- Dehydrated Food

- Freeze-Dried Food

- Frozen Food

- Raw Food

- Semi-Moist Food

- Powder

- Veterinary Diets/Therapeutic Diets

By Nature

- Organic

- Natural

- Conventional

- Monoprotein

- Limited Ingredient Diets (LID)

- Hypoallergenic

- Human-Grade

By Source

- Animal-Derived

- Plant-Derived

- Insect-Derived

By Application

- Kitten

- Adult

- Senior

- All Lifestages

By Pricing

- Mass Market/Economy

- Premium

- Super Premium/Ultra-Premium

- Therapeutic/Veterinary

By Distribution Channel

- Specialty Pet Stores

- Supermarkets & Hypermarkets

- Veterinary Clinics & Pharmacies

- E-commerce Platforms

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Cat Food Market

- Mars Petcare Inc.

- Nestlé Purina PetCare

- Hill's Pet Nutrition

- Blue Buffalo Company, Ltd.

- The J.M. Smucker Company

- Diamond Pet Foods

- WellPet LLC

- Farmina Pet Foods

- Arden Grange

- Orijen / Acana (Champion Petfoods - owned By Mars)

- Affinity Petcare S.A.

- Heristo AG

- Unicharm Corporation

- Petcurean Pet Nutrition

- Instinct Pet Food (formerly Nature's Variety)

- FreshPet

- Stella & Chewy's

- Fussie Cat (Pets Global)

- Open Farm

- Caru Pet Food

- Tiki Pets

- Nutramax Laboratories, Inc.

* List not Exhaustive

Research Coverage

The Cat Food Market report by USDAnalytics offers an in-depth assessment of global market sizing, CAGR, and value projections, with a sharp focus on key drivers, restraints, opportunities, and recent developments. The study captures critical industry dynamics such as WH Group’s acquisition of Pupil Foods in July 2025, General Mills’ U.S. launch of Edgard & Cooper, the introduction of the world’s first cultivated chicken cat food by Meatly, and a wave of innovative product launches from major brands like Go! Solutions and Tiki Cat. Regulatory shifts such as the EU’s 2025 ban on bisphenols are also explored as they impact packaging and product development.

Segment coverage includes product types (wet cat food, dry cat food/kibble, treats and snacks, raw, dehydrated, freeze-dried, frozen, semi-moist, veterinary/therapeutic diets), nature (organic, natural, conventional, monoprotein, limited ingredient, hypoallergenic, human-grade), source (animal, plant, insect-derived), application (kitten, adult, senior, all lifestages), and pricing tiers (economy, premium, super premium, therapeutic). Distribution analysis encompasses specialty pet stores, supermarkets, veterinary clinics, and e-commerce platforms.

The report profiles leading companies such as Mars Petcare, Nestlé Purina, Hill’s Pet Nutrition, Blue Buffalo, The J.M. Smucker Company, Diamond Pet Foods, WellPet LLC, and numerous innovative brands, highlighting strategies and product innovation. It covers historic data from 2021–2024 and delivers forecasts for 2025–2034, supporting strategic planning and decision-making.

Geographic coverage spans North America (US, Canada, Mexico), Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia), South America (Brazil, Argentina), and Middle East & Africa (Saudi Arabia, UAE, South Africa, Egypt, Rest of Africa). Designed for industry professionals, the report offers comprehensive insights into competitive landscape, product trends, growth opportunities, and future outlook within the global cat food industry.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.