Market Overview: Smart PPE, CBRN Innovation, and Major M&A Activity Redefine Chemical Protective Clothing Market

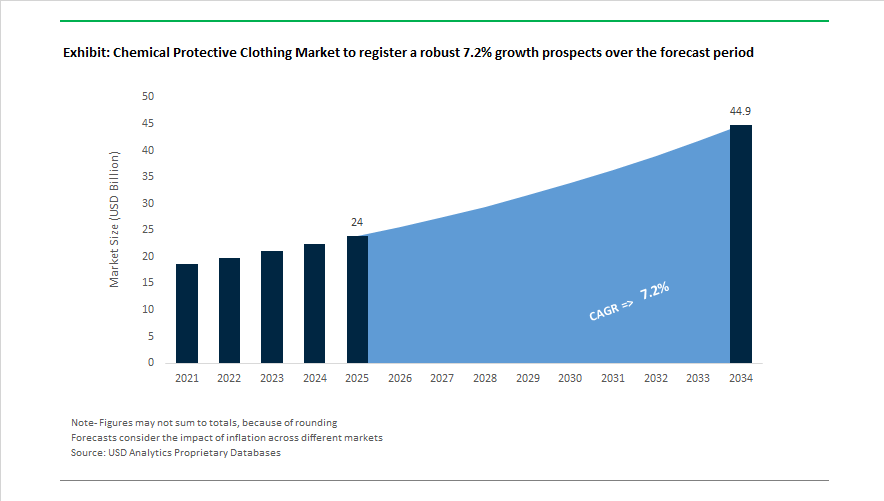

The Chemical Protective Clothing Market is projected to expand from USD 24 billion in 2025 to USD 44.9 billion by 2034, registering a CAGR of 7.2% as regulatory tightening, industrial safety mandates, and material innovation elevate demand for high-performance chemical resistant garments, disposable coveralls, and multi-hazard protective suits. Regulatory momentum strengthened in April 2024 when Japan revised its Industrial Safety and Health Act, tightening chemical exposure standards and prompting manufacturers such as Ansell to deploy Guardian Chemical assessment services for compliant protective clothing selection. Innovation accelerated in February 2024 when Avon Protection launched the EXOSKIN-S1 CBRN protective suit, engineered for up to 24 hours of defense against chemical, biological, radiological, and nuclear threats under NATO AEP-38 parameters. The competitive landscape shifted in July 2024 as Ansell acquired Kimberly-Clark’s PPE division, integrating Kimtech and KleenGuard cleanroom chemical protective apparel into its global portfolio.

Market consolidation intensified in May 2025 when Protective Industrial Products finalized the $1.325 billion acquisition of Honeywell’s PPE business, uniting North, Salisbury, and Fibre-Metal chemical protection brands under a single industrial safety platform. In the same month, DuPont partnered with Epicore Biosystems to embed biometric sensing technology into smart protective clothing, targeting real-time hydration and heat stress monitoring. Technology integration became more prominent in October 2025 when 3M introduced its Integrated Protection Program to ensure compatibility among respirators, helmets, and chemical protective suits, improving worker ergonomics. Ansell strengthened customer collaboration by opening its AXIS innovation studio in Georgia during October 2025, while supply chain ethics gained visibility in November 2025 as Ansell suspended ties with Mediceram to uphold ESG compliance.

Product breakthroughs accelerated into late 2025 and early 2026. At A+A 2025 in November 2025, DuPont unveiled Tyvek APX breathable fabric, delivering advanced chemical barrier performance with enhanced vapor permeability to reduce heat stress in pharmaceutical and utility environments. January 2026 saw Ansell launch the TouchNTuff 93-800 acetone-resistant disposable glove for semiconductor processing, addressing solvent exposure gaps in clean manufacturing. Lakeland Industries expanded internationally through major emergency service contracts across Europe and Asia in 2025 and achieved NFPA 1970 certification for its Ultimate Glow+ firefighting gloves in January 2026, reinforcing cross-sector adoption of chemical and thermal protection technologies.

Trends and Opportunities Reshaping the Competitive Direction of the Chemical Protective Clothing Market

IIoT-Enabled Smart Sensor Integration for Real-Time Worker Protection

The industry is moving from periodic fit-testing and manual monitoring toward continuous, real-time exposure intelligence. Facilities that implemented smart PPE systems recorded injury reductions of 30% to 70% (industrial hygiene reports, September 2025).

Smart protective suits now incorporate:

- Embedded IoT sensors that track gas exposure, suit permeation, and worker heat stress

- Wireless alerts that integrate with enterprise safety management dashboards

- Predictive failure analytics to schedule garment replacement before integrity loss occurs

Smart gloves, showcased at the E-Textiles 2025 Conference (Lille), demonstrated nanosensor-based PAH detection using microfluidic pathways. This expands the definition of chemical protection from “blocking permeation” to actively detecting and responding to exposure, a paradigm shift that aligns with insurers’ adoption of digitally-tracked safety compliance scoring.

Breakthroughs in Breathable, Multi-Hazard Materials to Bridge Compliance and Comfort

Compliance is directly tied to comfort. Workers abandon or misuse chemical suits when heat load is excessive or mobility is restricted. Manufacturers are now prioritizing ergonomic design paired with Type 3/4/5 chemical protection, creating breathable CPC that maintains impermeability under pressure conditions.

A pivotal launch occurred in November 2025 with DuPont Tyvek® APX, validated by Empa for:

- Increased heat dissipation under continuous shift conditions

- Lower thermal stress in chemical processing lines

- Retention of barrier integrity during stretch-based movements

Regulation is amplifying this trend. OSHA’s January 13, 2025 rule mandates that PPE must properly fit to be compliant. This forces employers to scale beyond “one-size-fits-most” inventories and expands demand for gender-specific and physique-specific CPC lines.

Opportunity to Supply CPC Tailored to Gigafactory and Battery Material Processing

Global battery-grade chemical production introduces unique risks: organolithium reactivity, dimethyl carbonate vapors, nickel/cobalt particulates, and thermal-runaway flames. This has opened a new industrial PPE niche.

Global safety regulators, including Health Canada (December 2025), are proposing enforceable standards for lithium-ion manufacturing zones. Gigafactories increasingly require suits that combine:

- Electrolyte-resistant chemical barrier fabrics

- Arc-flash and flame-resistance

- Cleanroom particulate control for ISO-grade battery chambers

Manufacturers who provide bundled hazard-class protection (FR + chemical + particulate) are positioned to become strategic suppliers to OEMs such as Tesla, CATL, Panasonic and to Tier-2 cell manufacturers in India and Southeast Asia.

Opportunity for Circular, Low-Carbon Chemical Protective Clothing in Regulated Sectors

Sustainability has shifted from a differentiator to a procurement prerequisite in the EU and healthcare-linked industries. Under the EU Waste Framework Directive (2025), PPE providers are increasingly obligated to ensure closed-loop waste recovery.

Key industrial shifts:

- First-ever recycled aramid IFR garment debuted in September 2025, addressing a segment where <1% of materials were previously recyclable

- Ansell’s Sustainability Management Report (2025) confirmed validated SBTi Scope-3 targets and 90% Scope-1/2 emissions reductions, alongside a pledge for 100% recyclable/compostable packaging by 2026

Hospitals, pharmaceutical labs, semiconductor cleanrooms, and biomanufacturing sites are now adding carbon footprint scoring to RFP documents. “Circular CPC” with verified recycled content and end-of-life take-back programs will attract contract awards under ESG-linked procurement evaluation.

Chemical Protective Clothing Market Share and Segmentation Insights

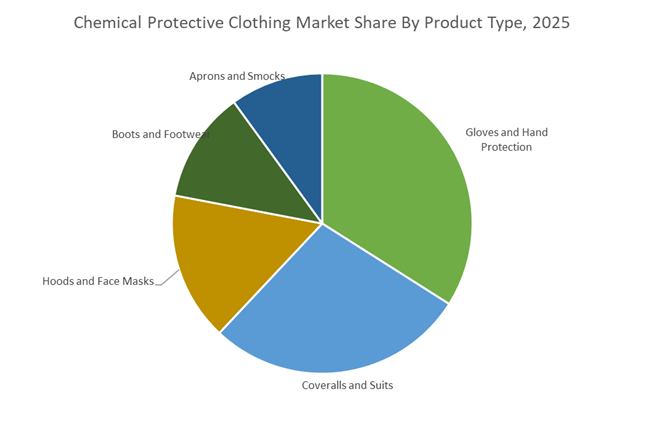

Product Type Market Share: Coveralls and Suits Lead at 38% as Breathable Barrier Materials Gain Traction

In 2025, coveralls and protective suits account for 38% of the chemical protective clothing market, driven by widespread use of Level A, B, and C garments across chemical plants, pharmaceutical manufacturing, hazardous waste remediation, and emergency response. These full-body solutions, commonly produced using flash-spun HDPE, laminated barrier films, and breathable membrane composites, protect against chemical splashes, vapors, and particulates while increasingly emphasizing heat-stress reduction. Gloves and hand protection form the second-largest segment, reflecting the high exposure risk of hands during chemical handling, with layered systems combining nitrile or neoprene inner gloves and butyl or Viton outer gloves tailored to specific chemistries. Boots and footwear remain essential in processing plants and refineries, with lightweight injection-molded designs replacing legacy PVC. Aprons, smocks, hoods, and face masks support task-specific protection in labs and cleanrooms, with rising demand for high-efficiency particulate filtration in biotech environments.

End-Use Industry Market Share: Chemical Processing Anchors Demand as Pharma and Healthcare Accelerate Growth

By end use, chemical processing represents 32% of global chemical protective clothing demand in 2025, encompassing petrochemicals, specialty chemicals, fertilizers, and industrial gases, where daily exposure to acids, solvents, and monomers necessitates robust PPE adoption. Aging plant infrastructure in developed regions and capacity expansion across Asia and the Middle East continue to support baseline volume. Oil and gas ranks second, requiring flame-resistant, arc-flash-compatible chemical apparel for upstream through downstream operations. Healthcare and medical applications are among the fastest-growing, fueled by infection control protocols and hazardous drug handling, while pharmaceuticals and biotechnology command premium pricing for sterile, cleanroom-compatible garments used in HPAPI and biologics manufacturing. Firefighting and emergency response remains specialized, supported by hazmat preparedness budgets. Mining, agriculture, and defense contribute niche demand, with Asia-Pacific emerging as the fastest-growing region amid tightening worker safety regulations.

Competitive Landscape of the Chemical Protective Clothing Market

The global Chemical Protective Clothing Market in 2026 is defined by rising regulatory pressure, expanding biopharma and hazardous materials handling, and growing demand for breathable, gas-tight, and liquid-tight PPE across chemical manufacturing, oil & gas, emergency response, and defense. Market leaders are differentiating through advanced barrier fabrics, heat-stress reduction, circularity programs, digital PPE assessment tools, and integrated protection ecosystems. Innovation is centered on Type 1 gas-tight suits, Type 3/4 liquid splash protection, recyclable materials, and IoT-enabled worker monitoring, while supply-chain agility and rapid-response manufacturing are becoming critical purchasing criteria for industrial buyers and government agencies.

DuPont sets the global benchmark for breathable, science-backed chemical protection

DuPont Personal Protection leads the 2026 market with Tyvek® and Tychem® platforms that combine high chemical resistance with proven wearer comfort. Its Tyvek® APX™ material, launched in late 2025/early 2026, is the first independently validated fabric to significantly reduce heat buildup while maintaining strong chemical barriers, directly addressing heat-stress risk in hazardous environments. DuPont’s Tychem® 6000 SFR and Tychem® 10000 series deliver Type 1 gas-tight and Type 3 liquid-tight protection for CBRN defense and spill response. Backed by physiological trials showing 20% longer worker endurance, DuPont is also scaling its #TyvekTogether recycling program, embedding sustainability and circular PPE design into its 2026 product roadmap.

Ansell integrates digital risk assessment with AlphaTec® chemical body protection

Ansell positions itself in 2026 as an end-to-end chemical PPE specialist, extending its glove leadership into full-body protection under the AlphaTec® brand. Its AnsellGuardian® Chemical digital platform allows safety managers to assess over 20,000 chemicals and receive customized PPE recommendations, simplifying compliance across complex sites. The AlphaTec® 6500 series delivers limited-use Level A gas-tight performance with ultrasonically welded seams, while the AlphaTec® Glove Connector ensures liquid-tight suit-to-glove integration. Ansell is also expanding aggressively into life sciences and cleanroom PPE, targeting sterile chemical handling in biopharmaceutical manufacturing, reinforcing its role as a systems-level partner rather than a single-product supplier.

Lakeland accelerates agile manufacturing for oil & gas and HazMat applications

Lakeland Industries is the 2026 agility leader, scaling capacity by 20% annually through new Southeast Asian facilities designed to bypass global trade bottlenecks. Its ChemMax® line is widely adopted by oil & gas operators, fire services, and HazMat teams, while the MicroMax® NS cool suit introduces zoned breathability for improved thermal comfort without compromising chemical splash resistance. Lakeland’s proprietary material blends deliver up to 35% longer service life than traditional PVC garments, reducing total ownership costs for industrial buyers. With rapid-response manufacturing and lightweight durability as core differentiators, Lakeland continues to gain share in high-intensity emergency and industrial environments.

3M advances integrated PPE ecosystems with smart compliance technologies

3M’s 2026 strategy centers on “Integrated Protection,” aligning chemical clothing with respiratory, hearing, and digital health systems to eliminate PPE interference. Its 3M™ Protective Coveralls (4500–4570 series) span particulate to Type 3/4 liquid chemical splash protection, while the Integrated Protection Program ensures ergonomic compatibility across PPE categories. In 2026, 3M is piloting IoT-enabled suits that monitor heart rate and core temperature in high-heat chemical zones, addressing compliance and worker safety simultaneously. Sustainability also features prominently, with upgraded packaging using recycled materials. 3M’s focus on comfort-driven compliance positions it strongly with large industrial operators seeking standardized global PPE platforms.

PIP emerges as a mega-aggregator following Honeywell PPE integration

Protective Industrial Products (PIP) enters 2026 as a newly consolidated powerhouse after completing the integration of Honeywell’s PPE business. This acquisition enables PIP to offer a massive combined portfolio of chemical-resistant apparel, including the North® and legacy Honeywell suit lines, covering ventilated, reusable, and long-shift chemical protection. PIP is rapidly expanding its global distribution network to support 24-hour fulfillment for emergency response teams across the US and Europe. By combining head-to-toe protection with automated supply logistics, PIP positions itself as a high-volume, rapid-deployment partner for chemical manufacturing, utilities, and disaster preparedness agencies.

United States: OSHA Penalty Escalation, PFAS Exit, and Smart Hazmat PPE Innovation

The U.S. chemical protective clothing market is undergoing structural transformation driven by regulatory enforcement, PFAS elimination, and smart PPE integration. Effective January 15, 2025, the Occupational Safety and Health Administration (OSHA) increased the maximum penalty for “Serious” violations to $16,550 per instance, triggering a capital reallocation across chemical manufacturing, oil & gas, and industrial processing sectors toward high-compliance chemical protective suits, flame-resistant apparel, and NFPA-certified gear. Simultaneously, 3M is finalizing its complete exit from PFAS manufacturing by December 31, 2025, accelerating the shift from fluoropolymer-based waterproof membranes toward silicone-coated fabrics and paraffin-treated chemical-resistant textiles. The transition is reshaping procurement standards for splash suits, Hazmat coveralls, and industrial rainwear.

OSHA’s updated construction PPE standards (effective January 13, 2025) now mandate individualized fit-testing, replacing universal sizing with body-specific protective garments to enhance barrier integrity and dexterity. In October 2025, Ansell launched the Ansell Xperience & Innovation Studio (AXIS) in Georgia to integrate immersive testing and digital prototyping into chemical-resistant garment design. Domestic resiliency strategies are also visible: Lakeland Industries increased inventories by over $3 million in early 2025 to mitigate tariff volatility. Concurrently, U.S. manufacturers are embedding AI-enabled biometric sensors into Kevlar-based industrial suits, delivering real-time toxin exposure alerts and heart-rate monitoring for high-risk Hazmat and confined-space operations.

Germany: Tyvek APX Launch, REACH-Driven PFAS Restrictions, and Circular PPE Standards

Germany remains a European innovation hub for breathable, multi-hazard chemical protective clothing. At A+A 2025 in Düsseldorf, DuPont unveiled Tyvek APX, a next-generation breathable barrier fabric validated by Empa physiological testing to significantly reduce heat stress while maintaining Type 5/6 particulate and splash protection. This addresses a critical demand in pharmaceutical manufacturing, automotive refinishing, and industrial coating applications where wearer comfort directly impacts compliance.

Germany is also at the forefront of the Universal PFAS Restriction proposal under REACH. In early 2026, the Federal Ministry for the Environment (BMUV) aligned national legislation with the EU Packaging and Packaging Waste Regulation (PPWR), affecting chemical-resistant garment coatings and repellent treatments. At A+A 2025, 3M showcased circular respirators and protective apparel incorporating recycled materials, reinforcing the EU’s 2026 sustainability objectives. German manufacturers are simultaneously investing in multi-hazard garments integrating chemical resistance, anti-static properties, and high-visibility features to serve advanced manufacturing and life sciences clusters.

China: Hazardous Chemicals Safety Law 2026 and Smart Factory PPE Expansion

China’s chemical protective clothing market is expanding under sweeping regulatory reform and industrial modernization. On December 27, 2025, the government promulgated the Hazardous Chemicals Safety Law (effective May 1, 2026), mandating certified protective gear and formal safety assessments for personnel entering high-risk chemical zones. The new law also standardizes Chinese-language Safety Data Sheets (SDS) and labeling requirements, increasing demand for hazard-profile-specific chemical protective suits aligned with national classification updates.

With urbanization projected to reach 65% by late 2025, infrastructure and pharmaceutical manufacturing growth is fueling an 8–10% annual increase in PPE consumption. China’s Smart Factory initiative is accelerating adoption of wearable monitoring in industrial helmets and suits, targeting 7% growth in high-tech protective equipment by early 2026. While China maintains dominance in non-woven polypropylene production for disposable coveralls and cleanroom garments, 2025 export audits have tightened quality controls for healthcare and electronic-grade protective textiles.

India: Technical Textile Incentives, POPs Compliance, and Pharmaceutical PPE Scaling

India’s chemical protective clothing industry is benefiting from aggressive technical textile incentives under the Textile Policy 2024–2025, which offers 10–35% capital subsidies for new manufacturing facilities producing chemical-resistant fabrics and industrial protective apparel. This policy aims to position India as a global hub for sustainable technical textiles, particularly as global buyers diversify away from single-country sourcing.

In alignment with the Stockholm Convention on Persistent Organic Pollutants (POPs), India initiated the phase-out of toxic chemical coatings in early 2025, encouraging bio-plastic and plant-oil-based protective finishes. The Ministry of Chemicals and Fertilizers has mandated certified PPE usage across pharmaceutical manufacturing facilities, which are expanding rapidly under the PLI 2.0 scheme. The combined impact of regulatory compliance, sustainability alignment, and infrastructure expansion is strengthening India’s domestic chemical protective clothing manufacturing ecosystem.

Japan: Acetone-Resistant Disposable Gloves and VOC Permeation Transparency

Japan’s chemical protective clothing market is advancing through precision engineering and regulatory transparency. In January 2026, Ansell Japan introduced the TouchNTuff™ 93-800, the first disposable glove delivering at least 15 minutes of acetone resistance—targeting semiconductor fabrication, chemical plant maintenance, and electronics assembly. This innovation responds to Japan’s advanced manufacturing sectors where solvent resistance and tactile precision are critical.

Between 2025 and 2026, Japan revised its Industrial Safety and Health Act, requiring manufacturers to disclose granular permeation rate data for protective garments exposed to volatile organic compounds (VOCs). This regulatory tightening enhances traceability and performance validation in high-risk environments. Ansell’s Japanese operations are currently outpacing global growth rates, reflecting sustained demand from life sciences and an aging workforce requiring higher compliance and ergonomic standards.

Denmark: National PFAS Ban with Transitional PPE Exemptions and Closed-Loop Recycling

Denmark has implemented one of the world’s most stringent PFAS policies affecting chemical protective clothing. Effective July 1, 2025, the Danish Environment Ministry introduced a national PFAS ban in clothing and footwear, with full sales restrictions commencing July 1, 2026. Importantly, the regulation includes temporary exemptions for Category III chemical PPE, recognizing that high-performance PFAS-free alternatives remain under validation.

Danish manufacturers are leading closed-loop recycling initiatives for mineral-fiber-based protective materials, aiming to establish a carbon-neutral PPE supply chain by 2030. The structured glide path for PFAS elimination provides industrial operators with transition time while accelerating R&D into fluorine-free barrier technologies, positioning Denmark as a global sustainability benchmark in the chemical protective clothing industry.

Chemical Protective Clothing Market Report Scope

Chemical Protective Clothing Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24 Billion

|

|

Market Size (2034)

|

$44.9 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Product Type (Coveralls and Suits, Aprons and Smocks, Gloves and Hand Protection, Boots and Footwear, Hoods and Face Masks), By Protection Level (Level A, Level B, Level C, Level D), By Material Type (Polyethylene and Polypropylene, Aramid and Blends, Polyamide, Laminated Fabrics, Rubber-based Materials, Multilayer Barrier Fabrics), By End-Use Industry (Chemical Processing, Oil and Gas, Pharmaceuticals and Biotechnology, Healthcare and Medical, Firefighting and Emergency Response, Mining and Agriculture, Law Enforcement and Military)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont, Ansell, 3M, Protective Industrial Products, Lakeland Industries, Drägerwerk, Kimberly-Clark Professional, Delta Plus Group, MSA Safety, Uvex Arbeitsschutz, Alpha Pro Tech, Sioen Industries, International Enviroguard, Unitika, Hultafors Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Chemical Protective Clothing Market Segmentation

By Product Type

- Coveralls and Suits

- Aprons and Smocks

- Gloves and Hand Protection

- Boots and Footwear

- Hoods and Face Masks

By Protection Level

- Level A

- Level B

- Level C

- Level D

By Material Type

- Polyethylene and Polypropylene

- Aramid and Blends

- Polyamide

- Laminated Fabrics

- Rubber-based Materials

- Multilayer Barrier Fabrics

By End-Use Industry

- Chemical Processing

- Oil and Gas

- Pharmaceuticals and Biotechnology

- Healthcare and Medical

- Firefighting and Emergency Response

- Mining and Agriculture

- Law Enforcement and Military

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Chemical Protective Clothing Industry

- DuPont

- Ansell

- 3M

- Protective Industrial Products

- Lakeland Industries

- Drägerwerk

- Kimberly-Clark Professional

- Delta Plus Group

- MSA Safety

- Uvex Arbeitsschutz

- Alpha Pro Tech

- Sioen Industries

- International Enviroguard

- Unitika

- Hultafors Group

*- List not Exhaustive