Chemical Resistant Coatings Market Size and Growth Driven by Industrial Protection and Harsh Environment Applications

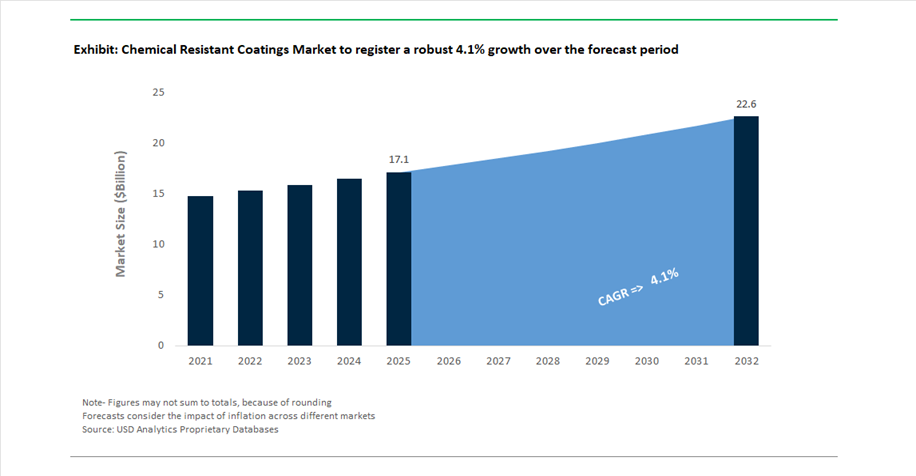

The Global Chemical Resistant Coatings Market Size is estimated at $17.1 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 4.1% to reach $22.7 Billion by 2032, driven by increasing demand for high-performance protective solutions in aggressive industrial environments such as oil & gas, petrochemicals, power generation, marine, and wastewater infrastructure. These coatings are engineered to provide exceptional resistance to acids, alkalis, solvents, and corrosive gases, ensuring the long-term integrity of critical assets exposed to extreme operating conditions.

Chemical resistant coatings typically include epoxy, polyurethane, novolac, and fluoropolymer-based systems, which offer barrier protection, adhesion strength, and durability under immersion and high-temperature environments. Their application is essential in storage tanks, pipelines, containment systems, and processing equipment, where failure due to chemical degradation can result in significant operational and safety risks. The increasing focus on asset lifecycle extension and maintenance cost reduction is a key factor driving adoption across industries.

The market is also benefiting from stricter environmental and safety regulations, particularly in developed regions, where industries are required to adopt coatings that prevent leakage, contamination, and structural degradation. Additionally, advancements in high-solids, solvent-free, and waterborne formulations are enabling manufacturers to deliver coatings that meet both performance and environmental compliance standards. The rise of energy transition projects, including offshore wind and hydrogen infrastructure, is further creating demand for coatings that can withstand chemically aggressive and marine environments.

Competitive dynamics are shaped by continuous innovation in resin chemistry, strategic investments in industrial coatings, and expansion into emerging markets, positioning chemical resistant coatings as a critical component of modern industrial protection systems.

Epoxy Innovation, Strategic M&A, and Infrastructure Demand Transforming Market Dynamics

The chemical resistant coatings market is undergoing transformation driven by material innovation, strategic consolidation, and increasing demand from infrastructure and energy sectors. A major development occurred in November 2025, when AkzoNobel and Axalta announced a merger of equals, creating a global coatings leader with a combined valuation of $17 billion. This consolidation integrates AkzoNobel’s industrial protective coatings portfolio with Axalta’s high-performance specialty finishes, accelerating development of advanced chemical-resistant systems.

Strategic portfolio realignment is also influencing market direction. AkzoNobel’s €922 million divestment of its India business (December 2025) enables the company to reinvest in R&D for next-generation coatings, particularly targeting chemical resistance in energy and infrastructure applications. This reflects a broader industry trend toward high-margin, performance-driven segments.

Product innovation remains a key growth driver. In January 2026, Jotun introduced next-generation zinc-rich and hybrid epoxy barrier coatings, designed for extreme industrial environments such as offshore platforms and petrochemical plants, offering enhanced resistance to both corrosion and chemical exposure. Similarly, Induron’s Nova-Safe coating, a ceramic-filled novolac epoxy, delivers high resistance to concentrated chemicals and wastewater, improving durability in treatment facilities.

Sustainability and operational efficiency are also shaping innovation strategies. Hempel’s Hempaguard Ultima system (January 2026) incorporates a biocide-free silicone topcoat, providing both chemical resistance and fouling protection for marine vessels while reducing fuel consumption and emissions. Meanwhile, Sherwin-Williams’ award-winning wastewater infrastructure project (September 2025) highlights the use of multi-layer epoxy and polyurethane systems to replace traditional coatings, offering superior resistance to corrosive gases and immersion conditions.

Specialized applications are expanding the scope of chemical-resistant coatings. Sihl’s ZM1 matte finish (April 2024) is engineered for chemical-resistant labeling, ensuring durability in laboratory and industrial identification systems. In parallel, PPG’s MASTER'S MARK™ innovations (January 2026) emphasize coatings that withstand frequent chemical cleaning, targeting hygiene-critical environments such as healthcare and food processing.

Financial performance and growth strategies further underscore market momentum. Axalta’s record EBITDA of $1.1 billion (February 2026) reflects strong demand for high-performance coatings across mobility and industrial sectors, particularly in applications requiring chemical durability.

EPA SCCAP Rule Driving High-Integrity Secondary Containment Coating Specifications

The chemical resistant coatings industry is transitioning into a compliance-driven “zero-failure” environment as the U.S. Environmental Protection Agency enforces the Safer Communities by Chemical Accident Prevention (SCCAP) rule, with critical deadlines set for May 10, 2027. This regulation impacts more than 12,000 Risk Management Plan facilities, fundamentally redefining coating performance requirements for secondary containment systems such as bund walls, dikes, and storage basins.

A key regulatory requirement is the ability of coatings to provide a verified impermeability barrier for a minimum of 72 hours against stored hazardous substances. This has rendered conventional epoxy systems insufficient in many high-risk applications, accelerating the transition toward advanced chemistries such as polyurea and vinyl ester coatings that offer superior chemical resistance and rapid cure profiles. In addition, the rule mandates expanded hazard reviews that include natural risks such as flooding and extreme temperature fluctuations. This has led to a 25% increase in demand for coatings with enhanced UV stability and thermal shock resistance.

Operational compliance is also becoming more rigorous. Facilities with prior incident histories are now subject to mandatory third-party audits, prompting proactive upgrades to containment coatings to avoid non-compliance penalties. Furthermore, new requirements related to facility siting—specifically the proximity of infrastructure to hazardous storage areas—are driving retrofitting activities, expanding the application scope of chemical resistant coatings across existing industrial assets.

This regulatory tightening is elevating coatings from a maintenance consideration to a critical safety system, making high-performance containment coatings a non-negotiable requirement in industrial risk management.

EU SEVESO III Enforcement Elevating Bund Wall Coating Standards and Environmental Protection

In Europe, the enforcement of the SEVESO III Directive is intensifying focus on containment integrity across more than 11,000 industrial installations. The 2025 implementation review identified leak containment as a persistent risk area, prompting stricter inspection regimes and higher performance expectations for bund wall coatings.

Regulatory updates in 2026 now require integrity testing of containment systems every three to five years, with coatings expected to demonstrate crack-bridging capabilities of up to 2 millimeters. This requirement ensures that coatings maintain a continuous barrier even as concrete substrates experience structural movement or thermal expansion. As a result, high-performance epoxy-novolac and elastomeric coating systems are becoming the default specification for bund wall applications.

Environmental protection is a central driver of these changes. The directive mandates the prevention of chemical leaching into groundwater, pushing facilities to adopt non-porous coating systems with superior impermeability. This shift has already contributed to a 15% reduction in soil contamination incidents year-over-year, highlighting the effectiveness of advanced coating technologies in mitigating environmental risks.

In major petrochemical hubs such as Rotterdam and Antwerp, compliance with SEVESO III standards is increasingly viewed as a “license to operate.” Facilities are prioritizing coatings that meet EN 1504-2 benchmarks for concrete protection, integrating coating performance into broader safety and sustainability strategies.

Fluoropolymer Coatings Enabling Ultra-Pure Semiconductor Processing Environments

The rapid advancement of semiconductor manufacturing, particularly at sub-5nm process nodes, is creating a specialized demand for fluoropolymer-based chemical resistant coatings. Materials such as ECTFE and PVDF are becoming essential in wet processing tools where ultra-high purity and resistance to aggressive chemicals are critical.

These coatings deliver exceptional chemical inertness, maintaining structural integrity when exposed to highly corrosive substances such as hydrofluoric acid and ozone. In modern fabrication environments, fluoropolymer coatings achieve sub-part-per-billion extractable metal levels, preventing contamination that could compromise wafer quality. This level of purity is essential for maintaining yield rates in advanced semiconductor production.

Thermal performance further enhances their value. PVDF coatings are widely used in wastewater treatment systems within semiconductor facilities, where they can withstand continuous exposure to aggressive chemical effluents at temperatures exceeding 100°C without degradation. Additionally, ECTFE coatings provide long service lifespans of five to eight years in highly corrosive environments, significantly reducing maintenance frequency and operational downtime.

Epoxy-Novolac Flooring Systems Supporting Safety and Durability in Lithium-Ion Battery Production

The global expansion of lithium-ion battery manufacturing is creating a high-growth application segment for chemical resistant coatings, particularly in electrolyte handling and filling areas. These environments expose surfaces to aggressive chemical mixtures, including lithium hexafluorophosphate and organic solvents, requiring coatings with exceptional chemical resistance and mechanical durability.

Epoxy-novolac systems are becoming the preferred solution due to their tightly cross-linked molecular structure, which prevents solvent penetration and swelling. Applied at thicknesses ranging from 60 to 125 mils, these coatings provide robust protection against chemical exposure while maintaining structural integrity under heavy operational conditions.

Safety considerations are also driving adoption. Battery manufacturing facilities are increasingly specifying conductive epoxy-novolac coatings to mitigate electrostatic discharge risks in environments where flammable solvents are present. This dual functionality—combining chemical resistance with electrostatic control—enhances both operational safety and process reliability.

Durability is another key advantage. In newly commissioned gigafactories, epoxy-novolac flooring systems are demonstrating a 40% improvement in abrasion resistance compared to standard industrial coatings, enabling them to withstand continuous traffic from automated guided vehicles and heavy equipment.

Solvent-Borne Chemical Resistant Coatings Lead with 38.5% Share Driven by High Cross-Link Density and Extreme Environment Performance

Technology Analysis: High-Solids Solvent-Borne Epoxy and Vinyl Ester Systems Dominate Industrial Applications

Solvent-borne coatings hold a leading 38.5% share of the chemical resistant coatings market in 2025, driven by their superior film integrity, low moisture vapor transmission rate (MVTR), and unmatched adhesion performance in aggressive environments. These coatings—primarily epoxies, polyurethanes, and vinyl esters—deliver high cross-link density, making them ideal for chemical storage tanks, secondary containment systems, pipeline coatings, and industrial flooring. Their ability to penetrate մակroporosity and cure at low temperatures (as low as 2°C) ensures reliable application in challenging field conditions, particularly in cold climates and outdoor maintenance projects. Additionally, high-solids solvent-borne formulations (60–80% solids) are increasingly adopted to meet VOC regulations (EPA AIM, EU IED) while retaining performance benefits. Their exceptional resistance to strong acids, solvents, and oxidizing chemicals positions them as the preferred solution in the global industrial protective coatings market.

Anti-Corrosive Coatings Dominate with 44% Share Driven by Infrastructure Protection and Asset Integrity Needs

Performance Specification Analysis: Epoxy and Zinc-Rich Systems Lead Corrosion Prevention Across Industries

Anti-corrosive coatings account for a dominant 44.0% share of the chemical resistant coatings market in 2025, as corrosion remains the most pervasive and costly degradation mechanism across industrial assets. These coatings, including epoxy systems, polyurethane topcoats, and zinc-rich primers, provide multi-layer protection through barrier resistance, cathodic protection, and chemical passivation. They are extensively used in oil & gas facilities, marine vessels, bridges, water treatment plants, and power infrastructure, where exposure to moisture, chlorides, and industrial pollutants accelerates material degradation. A key growth driver is the increasing focus on corrosion under insulation (CUI) prevention, particularly for pipelines operating between 0°C and 175°C, where trapped moisture can cause severe hidden damage. Additionally, regulatory frameworks such as the EPA SPCC rule are driving demand for chemical-resistant containment coatings, ensuring environmental compliance. These factors solidify anti-corrosive coatings as the backbone of the global chemical resistant coatings market.

Chemical Resistant Coatings Market Competitive Landscape Driven by High-Performance Epoxy Systems and Sustainable Formulations

The chemical resistant coatings market is moderately consolidated, with leading players advancing high-solids epoxy coatings, polyurethane coatings, and bio-based resin systems. Industry leaders are focusing on VOC-compliant coatings, corrosion protection, and long-life asset protection solutions to meet stringent environmental regulations across industrial, marine, and chemical processing sectors.

Sherwin-Williams dominates chemical-resistant coatings with epoxy systems and antimicrobial flooring solutions

The Sherwin-Williams Company leads the chemical resistant coatings market with a 12% global share, driven by high-performance epoxy and polyurethane coatings. Its solutions are widely used in pharmaceutical manufacturing, food processing plants, and secondary containment systems requiring chemical durability. The company is expanding antimicrobial chemical-resistant flooring to address rising demand in biotech manufacturing facilities. Strong focus on corrosion-under-insulation (CUI) protection enhances operational reliability and reduces downtime. Its spec-driven sales model embeds products in large-scale infrastructure projects globally. Product development focuses on industrial coatings, chemical durability, and regulatory compliance.

AkzoNobel advances sustainable powder coatings with laser curing and EV-focused chemical protection

AkzoNobel is a pioneer in sustainable chemical resistant coatings through its Interpon and Resicoat powder coating technologies. Its solvent-free coatings deliver high chemical resistance while meeting strict VOC regulations. The introduction of laser-based curing technology reduces energy consumption by up to 30% while maintaining coating performance. The Resicoat portfolio is optimized for EV battery insulation and chemical exposure resistance. Digital asset monitoring tools enhance predictive maintenance for chemical storage infrastructure. Expansion in Asia-Pacific supports industrial and offshore project demand. Product innovation focuses on sustainability, energy efficiency, and advanced powder coatings.

PPG strengthens chemical-resistant portfolio with advanced powder coatings and packaging solutions

PPG Industries continues to expand its presence in chemical resistant coatings through innovation in powder coatings and industrial applications. The ENVIROCRON Extreme Protection Edge Plus coating provides superior corrosion and chemical resistance for harsh environments. Its ENVIROLUXE Plus line incorporates recycled materials, targeting sustainable construction markets. PPG dominates the packaging coatings segment with non-BPA internal coatings for chemically aggressive storage applications. Investment in advanced manufacturing facilities supports high-performance coatings development. Automation through MOONWALK systems enhances formulation precision and reduces material waste. Product development focuses on sustainability, industrial coatings, and packaging protection.

Jotun expands chemical-resistant coatings through marine integration and emerging market growth

Jotun is a key player in chemical resistant coatings, driven by strong performance in marine and protective coatings segments. The company achieved record sales in 2025, supported by expansion into Africa and emerging industrial markets. Its Hardtop XPII coating provides advanced protection against chemical exposure and extreme weather conditions. Integration of marine and protective coatings divisions enhances R&D efficiency and product standardization. Regional R&D hubs enable rapid customization for local chemical environments. Strategic focus includes corrosion protection, marine coatings, and industrial durability solutions.

Hempel drives long-life chemical-resistant coatings with lifecycle cost optimization and CUI expertise

Hempel focuses on extending asset life through high-performance chemical resistant coatings designed for over 25 years of service. Its solutions are widely used in tank linings, hydrocarbon passive fire protection, and chemical processing facilities. Strong expertise in corrosion-under-insulation (CUI) ensures operational safety in high-temperature environments. The company emphasizes real-world performance validation over laboratory testing. Its foundation-owned structure supports long-term R&D investment and applicator training. Product strategy focuses on lifecycle cost reduction, industrial safety, and high-durability coatings.

BASF enables chemical-resistant coatings ecosystem with advanced resins and integrated system solutions

BASF plays a critical role in the chemical resistant coatings market through its Surface Technologies division and raw material supply leadership. The company provides high-performance resins, additives, and cross-linkers essential for coating formulations. Expansion of the Zhanjiang Verbund site strengthens its position in the Asia-Pacific chemical production market. BASF is shifting toward high-margin specialty resins to support advanced coating applications. Sustainability initiatives target significant CO2 emission reductions through renewable energy integration. Its vertically integrated model delivers system solutions combining chemical resistance, durability, and surface performance.

China Chemical Resistant Coatings Market: Industrial Expansion and Energy Investments Driving Dominance

China remains the largest and most influential market for chemical resistant coatings, fueled by massive industrial expansion and infrastructure development. National Oil Companies are projected to invest over $120 billion in drilling and well services, creating strong demand for novolac epoxy and fluoropolymer coatings capable of withstanding high-temperature, high-pressure (HTHP) environments.

Infrastructure and energy sectors are key drivers. Renovation of 53,700 residential communities and record natural gas production of 230 bcm are accelerating demand for coatings resistant to H₂S and CO₂ corrosion in pipelines and containment systems. Additionally, expansion of chemical industrial zones and offshore energy projects is boosting adoption of vinyl ester glass flake coatings and heavy-duty UV-resistant systems. China’s long-term outlook is reinforced by projected $13 trillion construction spending by 2030, cementing its leadership in high-volume chemical resistant coatings.

United States Chemical Resistant Coatings Market: Semiconductor Boom and High-Tech Infrastructure Driving Growth

The United States market is evolving toward high-performance, specialized applications, supported by strong federal funding and reshoring initiatives. Under the Infrastructure Investment and Jobs Act (IIJA), $40 billion is allocated for bridge rehabilitation, driving demand for ASTM-compliant chemical resistant coatings.

A major growth driver is the semiconductor fabrication boom, fueled by the CHIPS Act, which is increasing demand for ultra-high-purity coatings in cleanrooms and chemical storage facilities. Data center expansion is also accelerating adoption of epoxy floor coatings resistant to thermal loads and dielectric fluids. Regulatory pressures, such as carbon pricing under Washington State’s HB 1103, are pushing manufacturers toward bio-based resin systems, while supply chain disruptions are encouraging the use of thin-film coating technologies to optimize material efficiency.

Germany Chemical Resistant Coatings Market: Hydrogen Infrastructure and Bio-Based Innovation Driving Leadership

Germany continues to lead Europe in advanced chemical resistant coatings, particularly in pharmaceutical and green energy sectors. Growth in the pharmaceutical industry (+5.5%) is sustaining demand for non-leaching coatings in sterile environments, while the country’s push toward a national hydrogen grid is driving innovation in permeation-resistant coatings to prevent hydrogen embrittlement.

Regulatory frameworks under REACH and the EU Green Deal are accelerating the transition toward waterborne polyurethanes and PFAS-free systems. Germany is also pioneering bio-based resin technologies, including lignin-derived polyurethanes, and integrating smart coatings with self-healing or leak-indicating properties into automated industrial systems. These advancements position Germany as a leader in sustainable, high-performance coatings.

India Chemical Resistant Coatings Market: Urbanization and Industrial Expansion Driving High Growth

India is one of the fastest-growing markets for chemical resistant coatings, supported by rapid urbanization and industrial expansion. Government initiatives under the National Infrastructure Pipeline and smart city programs are significantly increasing demand for protective coatings in construction and infrastructure.

The market is also benefiting from industrial consolidation, highlighted by JSW Paints’ $1.07 billion acquisition of Akzo Nobel India, aimed at scaling industrial coating production. Growth in automotive manufacturing hubs such as Chennai and Pune is driving demand for OEM and refinish coatings, while increasing environmental awareness is accelerating the shift toward waterborne and powder coatings. Financial support programs for SMEs are further encouraging innovation in eco-friendly coating solutions, positioning India as a key growth hub.

South Korea Chemical Resistant Coatings Market: Semiconductor and EV Battery Demand Driving High-Purity Coatings

South Korea is a critical market for high-purity chemical resistant coatings, driven by its leadership in semiconductors and EV batteries. The expansion of photoresist plants and semiconductor facilities is increasing demand for coatings resistant to aggressive etching acids in cleanroom environments.

Technological innovation is focused on advanced electronics and packaging. The rise of chiplet and advanced packaging technologies is driving demand for thick-film insulating coatings that provide both chemical and mechanical protection. Additionally, the growth of EV battery manufacturing is fueling demand for electrolyte-resistant coatings in assembly lines and storage facilities. Investments in dual-site supply chains and smart mobility infrastructure further reinforce South Korea’s position as a leader in high-performance chemical resistant coatings.

Brazil Chemical Resistant Coatings Market: Energy Transition and Agribusiness Driving Demand

Brazil’s chemical resistant coatings market is expanding rapidly, supported by both traditional energy sectors and emerging green initiatives. Offshore oil exploration continues to drive demand for seawater- and chemical-resistant coatings for subsea infrastructure.

The country’s National Hydrogen Policy and “Fuel of the Future” law are creating new opportunities for coatings in biofuel storage and hydrogen infrastructure. Additionally, record agricultural output is increasing demand for coatings in fertilizer plants and logistics systems. Investments in sustainable aviation fuel (SAF) production are also boosting demand for corrosion-resistant coatings in biorefineries. Automation in coating production facilities is further improving quality and consistency, positioning Brazil as a key market in Latin America.

Japan Chemical Resistant Coatings Market: Lifecycle Durability and Advanced Polymer Systems Driving Innovation

Japan’s market is defined by its focus on long-term durability and advanced material science. Aging infrastructure is a major driver, with demand for heavy-duty coatings designed for 30+ year lifecycles in bridges and tunnels.

Innovation is centered on sustainability and performance. Japanese manufacturers are advancing solvent-free polymer systems and waterborne epoxy coatings that match the performance of traditional solvent-based systems. The transition to EVs is also driving demand for flame-retardant and chemical-resistant coatings for battery enclosures. Strict environmental regulations are encouraging the adoption of bio-based resins and low-emission curing technologies, reinforcing Japan’s leadership in high-performance and sustainable coatings.

Chemical Resistant Coatings Market Report Scope

Chemical Resistant Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17.1 Billion

|

|

Market Size (2032)

|

$22.7 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Resin Chemistry (Epoxy, Fluoropolymers, Polyurethane (PU), Polyester and Vinyl Ester, Specialty Hybrids), By Technology (Solvent-Borne, Water-Borne, 100% Solids, Powder Coatings, Radiation Curable), By Film Type (Thin Film Coatings (<15 mils), Medium Build Coatings (15–40 mils), Heavy-Duty Linings (>40 mils), Ultra-Heavy Duty Systems), By End-Use Industry (Chemical Processing, Oil and Gas, Water and Wastewater Treatment, Pharmaceutical and Food Processing, Marine and Offshore, Mining and Metallurgy), By Performance Specification (Alkali Resistant Grade, Solvent and Hydrocarbon Resistant Grade, High-Temperature Chemical Resistance, Anti-Corrosive, Smart Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., RPM International Inc., BASF SE, Axalta Coating Systems Ltd., Jotun A/S, Nippon Paint Holdings Co., Ltd., Hempel A/S, Kansai Paint Co., Ltd., Sika AG, The Dow Chemical Company, Henkel AG & Co. KGaA, Arkema S.A., Asian Paints Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Chemical Resistant Coatings Market Segmentation

By Resin Chemistry

- Epoxy

- Fluoropolymers

- Polyurethane (PU)

- Polyester and Vinyl Ester

- Specialty Hybrids

By Technology

- Solvent-Borne

- Water-Borne

- 100% Solids

- Powder Coatings

- Radiation Curable

By Film Type

- Thin Film Coatings (<15 mils)

- Medium Build Coatings (15–40 mils)

- Heavy-Duty Linings (>40 mils)

- Ultra-Heavy Duty Systems

By End-Use Industry

- Chemical Processing

- Oil and Gas

- Water and Wastewater Treatment

- Pharmaceutical and Food Processing

- Marine and Offshore

- Mining and Metallurgy

By Performance Specification

- Alkali Resistant Grade

- Solvent and Hydrocarbon Resistant Grade

- High-Temperature Chemical Resistance

- Anti-Corrosive

- Smart Coatings

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Chemical Resistant Coatings Market

- Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- RPM International Inc.

- BASF SE

- Axalta Coating Systems Ltd.

- Jotun A/S

- Nippon Paint Holdings Co., Ltd.

- Hempel A/S

- Kansai Paint Co., Ltd.

- Sika AG

- The Dow Chemical Company

- Henkel AG & Co. KGaA

- Arkema S.A.

- Asian Paints Limited

*- List not Exhaustive