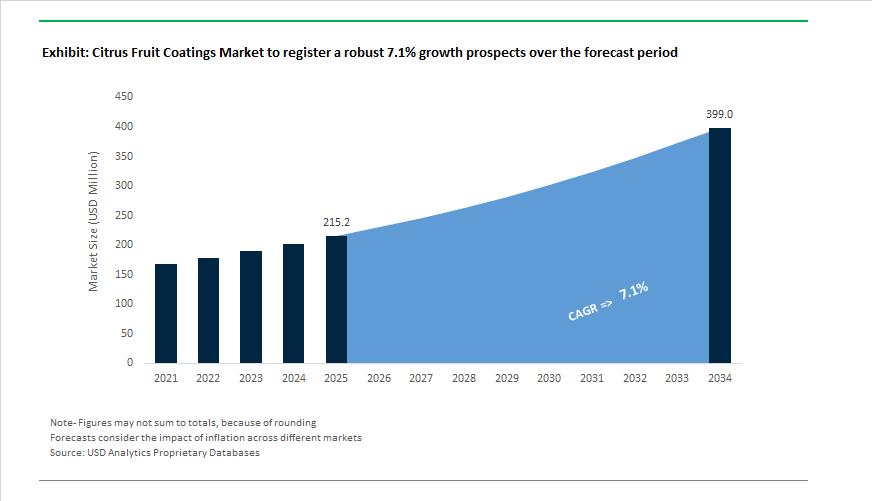

Citrus Fruit Coatings Market Outlook 2025–2034: $215.2 Million to $399 Million at 7.1% CAGR Driven by Post-Harvest Loss Reduction and Export Optimization

The global Citrus Fruit Coatings Market is projected to expand from $215.2 Million in 2025 to $399 Million by 2034, registering a CAGR of 7.1%. Growth is underpinned by rising global citrus exports, increasing demand for shelf-life extension technologies, and tightening retail quality standards. Post-harvest losses remain a structural challenge, with approximately 14% of fresh produce lost between harvest and retail. This loss rate has accelerated investment in edible coatings, wax emulsions, fungicidal treatments, and digital monitoring systems that reduce moisture loss, delay senescence, mitigate chilling injury, and maintain visual appeal during long-distance shipment.

Product innovation and digital integration accelerated across 2024–2026. In February 2024, Citrosol introduced the CitroFy real-time monitoring platform, enabling packing houses to precisely control wax and fungicide dosing for export-grade citrus. In February 2024, Decco launched DECCO Sol Max, a pre-coating detergent designed to remove sooty mold and improve coating adhesion, directly enhancing wax uniformity and post-harvest performance. In September 2024, AgroFresh expanded its U.S. pre-harvest portfolio with Harvista™ Mix, reinforcing fruit firmness before entry into coating lines. By November 2024, AgroFresh integrated spectral sensing and transit monitoring technologies into its FreshCloud™ platform, allowing growers to track coating effectiveness throughout shipment. These advancements reflect the industry’s pivot toward data-driven coating performance verification rather than standalone chemical application.

Strategic partnerships and sustainability positioning strengthened market competitiveness in 2025. In April 2025, AgroFresh introduced Proteku® at Macfrut, enabling tighter quality control integration alongside protective coatings. In May 2025, AgroFresh partnered with Biotalys to develop biological post-harvest coatings and fungicides targeting mold reduction in citrus supply chains. In June 2025, Apeel Sciences was recognized for its plant-based edible coatings composed of mono- and diglycerides, reinforcing retailer adoption of plant-derived barrier technologies aimed at lowering greenhouse gas emissions and reducing food waste. In September 2025, JBT Marel sponsored the International Citrus & Beverage Conference, highlighting automated coating application systems that optimize detergent and wax usage. During late 2024–2025, Decco completed the acquisition of Citrashine South Africa, securing strategic access to one of the world’s largest citrus export regions and integrating localized coating formulations into its global network.

Regulatory transparency and product diversification intensified in 2026. In late 2025, the introduction of the Apeel Reveal Act in the U.S. House of Representatives and parallel discussions in Florida prompted clearer labeling requirements for produce treated with mono- and diglyceride-based coatings. This regulatory shift is increasing traceability and formulation disclosure across the citrus coatings value chain. At Fruit Logistica in February 2026, Citrosol reinforced its leadership in vegan PlantSeal® and SunSeal® coatings capable of reducing weight loss by nearly 50% and mitigating chilling injury during extended transport. Sufresca expanded adoption of edible coatings as direct plastic replacement solutions in 2024, enabling breathable barriers for naked produce retail. These combined developments indicate sustained mid-to-high single-digit growth through 2034, supported by export expansion, digital monitoring integration, biological innovation, and sustainability-driven retail mandates in the citrus fruit coatings market.

Citrus Fruit Coatings Market Trends and Drivers

Marketwide Pivot Toward Bio-Based, Plant-Derived Waxes and Lipid Systems to Align with Regulatory and Sustainability Mandates

The citrus fruit coatings industry is undergoing a strategic transformation driven by global regulatory harmonization and premium-grade export requirements. Petroleum-based polyethylene waxes are steadily being replaced by carnauba, candelilla, beeswax, and lecithin-based formulations, as global fruit exporters seek renewable, organic-compliant, and higher-gloss alternatives.

This shift is being accelerated by the European Commission Regulation (EU) 2025/651, which formally broadened the authorization of carnauba wax (E 903) and lecithins (E 322) as glazing agents. These bio-based coatings provide moisture-barrier protection, oxidation resistance, and extended shelf-life performance, supporting year-round supply without compromising natural sensory attributes. A defining metric in this shift is the rise of T1 refined carnauba wax, which in 2025 registered a 62% adoption share among premium citrus exporters—primarily due to its superior surface gloss, compatibility with organic standards (EU 2025/973), and ability to enhance visual merchandising in high-value retail formats. Strategically, this trend represents a dual value proposition: regulatory compliance plus brand-differentiating consumer appeal, positioning bio-based coatings as premium-margin product categories in future contract awards.

Growing Adoption of Active Antimicrobial and Gas-Barrier Coatings to Reduce Post-Harvest Losses

The industry is shifting from passive coatings aimed solely at moisture retention to functional, active coating systems designed to inhibit fungal development, reduce respiration rates, and delay senescence.

A landmark March 2025 study published in Pesticide Biochemistry and Physiology demonstrated that potassium sorbate and sodium benzoate embedded in edible coatings suppressed citrus mold growth by up to 100%, offering a GRAS-approved, eco-friendly alternative to banned or restricted fungicides such as imazalil. Simultaneously, polysaccharide-based coatings incorporating xanthan gum and plant-derived extracts now create controlled internal CO₂/O₂ exchange, enabling optimal modified-atmosphere storage. Research in 2025 confirmed these systems significantly slow respiration in thin-skinned varieties—meaning fewer losses during transcontinental cold-chain logistics and stronger performance for citrus shipped from North Africa and LATAM to EU-27 and East Asia markets.

Strategically, active coatings allow exporters to reduce chemical fungicide dependency, comply with rising residue-limit regulations, and compete in the growing premium clean-label fresh fruit segment.

Tailored Citrus Coatings for Controlled Environment Agriculture (CEA) and Specialty Indoor-Grown Citrus

Controlled Environment Agriculture (CEA) and vertical citrus farming are emerging high-margin demand pockets. Indoor-grown citrus (e.g., Meyer lemons, finger limes) lack the natural thick cuticle found in field-grown varieties, making them more vulnerable to dehydration and storage-related deterioration.

Suppliers such as JBT Corporation and AgroFresh are developing gentle, low-heat, spray-on coatings optimized for CEA citrus supply chains that move from greenhouse to shelf within 48 hours. These lipid-emulsion coatings prevent rapid water loss while delivering desirable surface gloss without requiring traditional heat-drying tunnels—critical in indoor farming environments where energy consumption and post-harvest damage tolerance are tightly managed.

As high-tech citrus hubs scale across the Middle East, North America, and APAC megacities, the demand for specialty CEA-tailored coatings represents a high-margin, low-competition segment likely to capture procurement budgets from retailers focused on premium SKU differentiation.

Edible, Transparent Coatings Enabling Plastic-Free Retail and Naked Fruit Merchandising

Retailers are under pressure to comply with EU Green Deal policies and 2025 plastic-waste directives, accelerating a transition toward edible, ultra-thin biodegradable coatings that eliminate secondary packaging for citrus.

In November 2025, the Virginia Tech food materials research team announced a breakthrough in spray-coated bioplastic coatings composed of PLA and PHA blends, which can be applied either directly onto fruit or on recyclable paper. Laboratory testing showed 50% improvement in oxygen barrier performance, enabling retailers to sell naked citrus without plastic mesh bags or clamshells. Commercial viability is further strengthened by waste-to-value formulations that utilize pectin, alginate, and natural food-processing byproducts, aligning with the clean-label movement and lowering lifecycle emissions across citrus packaging.

Citrus Fruit Coatings Market Share and Segmentation Insights

Coating Type Distribution: Wax-Based Coatings Maintain Dominance as Edible Alternatives Gain Momentum

Wax-based citrus fruit coatings account for 58% of market share in 2025, reinforcing their dominance in post-harvest treatment solutions. Carnauba wax, polyethylene wax, and shellac formulations are widely adopted due to their superior ability to minimize moisture loss, reduce shriveling, and enhance the glossy surface appearance that significantly influences retail purchase decisions. Fungicide-incorporated coatings represent a substantial share, reflecting the industry's continuous effort to combat post-harvest diseases such as green mold and blue mold during long-haul export. These coatings combine a physical moisture barrier with targeted antifungal agents, extending shelf life and preserving fruit integrity during 2 to 6 weeks of shipping. Plant-derived and edible coatings, formulated from chitosan, cellulose derivatives, and essential oils, currently hold the smallest share but represent the fastest-growing segment, driven by clean label produce trends and regulatory pressure to reduce synthetic chemical residues on fresh citrus fruits.

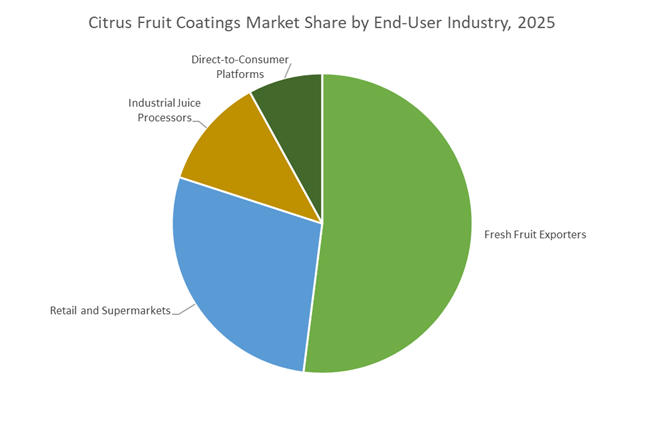

End-User Industry Breakdown: Exporters Lead Consumption as Direct-to-Consumer Channels Reshape Demand Patterns

Fresh fruit exporters dominate the citrus fruit coatings market with 52% share, as international shipments require robust post-harvest protection to prevent dehydration, maintain firmness, and preserve visual quality during extended transit. Coatings are critical in sustaining export-grade citrus across diverse climatic conditions and logistics chains. Retailers and supermarkets form the second-largest segment, where aesthetic appeal under high-intensity store lighting directly influences consumer purchasing behavior, making high-gloss wax coatings commercially valuable. Industrial juice processors represent a relatively small share since cosmetically imperfect fruits, often lightly coated or untreated, are diverted for processing where peel removal eliminates coating relevance. The emerging direct-to-consumer segment, including farm-to-table subscription boxes and online grocery platforms, is accelerating adoption of plant-based and edible coatings, as these channels prioritize traceability, freshness, and minimal chemical treatment to appeal to health-conscious consumers.

Competitive Landscape of the Citrus Fruit Coatings Market

The Citrus Fruit Coatings Market is shaped by post-harvest technology leaders integrating edible coatings, digital quality monitoring, and automated packing infrastructure to reduce shrinkage and extend shelf life. Competitive differentiation centers on plant-based wax alternatives, zero-residue formulations, electrostatic application systems, and data-driven packhouse optimization. Market leaders are prioritizing near-zero waste logistics, regulatory compliance for global exports, and breathable coating chemistries to preserve mandarins, limes, and premium citrus varieties. Strategic expansion across Latin America, Europe, Asia, and the Southern Hemisphere continues to accelerate adoption of sustainable, performance-driven citrus coating solutions.

AgroFresh drives data-enabled, plant-based citrus coatings with FreshCloud integration

AgroFresh Solutions is a global leader in citrus post-harvest technology, holding approximately 27.5% market share through its data-driven service model and sustainable coating portfolio. Its VitaFresh™ Botanicals line delivers plant-based edible coatings that reduce weight loss and preserve freshness without synthetic waxes. During 2025 to 2026, AgroFresh expanded its FreshCloud™ digital platform, integrating real-time coating thickness and fruit quality metrics directly with applicators. The company’s core strength lies in global regulatory expertise, enabling exporters to meet complex food safety standards. Strategically, AgroFresh targets near-zero waste logistics, extending shelf life of highly perishable citrus like mandarins and limes by up to 30%.

JBT combines automation and Sta-Fresh coatings for high-throughput citrus packhouses

JBT Corporation delivers a fully integrated citrus processing ecosystem, supplying both coating chemistry and high-speed mechanical infrastructure. In 2025, JBT completed its landmark merger with Marel, forming JBT Marel and unifying automation, digitalization, and coating technology. Its Sta-Fresh® portfolio, including Sta-Fresh 2850 formulated for organic citrus, provides superior moisture control and high-shine finishes. JBT showcased its Automation plus Coating platforms at Mercoagro 2026, targeting fast-growing South American and Asian export hubs. The company dominates large commercial packing houses, where automated spray systems process thousands of fruits per hour with consistent coating performance.

Citrosol advances zero-residue Mediterranean citrus protection with PlantSeal technology

Spain-based Citrosol is recognized for residue-free citrus solutions and leadership across Mediterranean markets. Its PlantSeal® vegan-certified, plant-based coating reduces internal browning and chilling injury by up to 84% during cold storage. At Fruit Logistica 2026, Citrosol introduced GREENFOG-AS fumigation to complement coatings and prevent fungal decay in cold rooms and export containers. The company is expanding into fresh-cut fruit through Citrocide® Fresh-Cut, combining washing and coating for minimally processed citrus segments. Citrosol’s strategic focus on zero-residue post-harvest management aligns with European retailer demand for fruit free from conventional fungicide traces.

Decco leverages localized R&D and electrostatic Fullcover systems for climate-specific coatings

Decco Post-Harvest, part of UPL, supplies climate-adapted citrus coatings across the US, South Africa, and emerging export regions. The company holds up to 90% market share in select areas like Baja California due to localized R&D tailored to extreme humidity and temperature conditions. Growth accelerated following Decco’s acquisition of CITRASHINE in South Africa, strengthening its dosing equipment and wax capabilities. Its Fullcover system uses electrostatic charges to achieve 100% homogeneous coating with minimal water and chemical usage. Decco integrates deeply with UPL’s OpenAg network, offering a comprehensive Grove-to-Grocery platform spanning pre-harvest protection and post-harvest coatings.

Pace International optimizes breathable coatings to maximize premium citrus pack-out yields

Pace International specializes in high-performance citrus coatings and sanitizers, with strong penetration across North American export markets. Its PrimaFresh® portfolio, including the 606 GL high-shine edible coating, delivers the wet-look finish favored by premium retailers. In late 2025, Pace launched a Sustainable Pack-out Program incorporating biodegradable surfactants to reduce packing house wastewater impact. Guided by its “Science of Freshness” strategy, Pace engineers breathable coatings that regulate citrus respiration and prevent anaerobic fermentation and off-flavors. Through the Pace Postharvest Academy, the company provides technical training to help packers optimize coating dosage and maximize pack-out yield.

United States: Commercial Scale-Up of Edible Coatings and Automation-Driven Efficiency

The United States citrus fruit coatings industry is undergoing a decisive shift from conventional petroleum-based waxes toward plant-derived, edible coating technologies that directly address food waste, plastic reduction, and regulatory alignment. A defining milestone was achieved in June 2025 when Apeel Sciences was recognized by Food & Wine as a 2025 Game Changer for its plant-based edible coating platform. By late 2025, Apeel reported that its coatings had prevented more than 166 million pieces of fruit from being wasted globally, a metric that has become increasingly influential for U.S. growers and retailers responding to sustainability-linked procurement policies. Corporate disclosures in September 2025 further demonstrated the material impact of these technologies, with science-based coatings replacing plastic wrap on individual citrus units and eliminating plastic equivalents associated with millions of straws and bottles during a single pilot cycle.

Regulatory alignment has accelerated adoption across major producing states such as Florida and California. The convergence of Consumer Product Safety Commission expectations with U.S. Food and Drug Administration GRAS approvals has strengthened confidence in plant-derived coatings as compliant post-harvest treatments. This trend has been reinforced by the 2025 National Strategy to Reduce Food Loss and Waste, which explicitly prioritizes non-synthetic interventions. In parallel, operational modernization is reshaping packhouse economics. JBT Corporation, operating through JBT Marel, showcased automated dosing and precision wax application systems at IFFA 2025, enabling citrus processors to optimize layer thickness while minimizing chemical runoff. Between 2024 and 2025, major Central Valley packing houses invested heavily in upgraded coating application lines, including secondary infrared drying systems designed to improve adhesion consistency and throughput reliability.

Spain: Yield Compression Driving High-Performance, Residue-Free Coatings

Spain’s citrus fruit coatings market is being reshaped by structural supply constraints and increasingly strict sustainability requirements from export destinations. Facing its lowest citrus harvest in 16 years, with the 2025–26 crop forecast at 5.44 million tonnes, Spanish packers have shifted strategic focus from volume expansion to value retention and shelf-life optimization. This has accelerated the transition toward biocontrol waxes and mild antifungal dips such as chitosan, which align with European Union sustainability frameworks and reduce reliance on synthetic fungicides. The emphasis on performance under extended cold storage conditions has elevated the role of advanced post-harvest coatings as a critical quality lever.

Scientific validation has reinforced this transition. In June 2024, the Valencian Institute of Agricultural Research published findings confirming that advanced coatings applied to Lanelate oranges significantly reduced weight loss and physiological disorders during prolonged storage. This evidence has supported rapid adoption among export-oriented packhouses. Technological infrastructure is also advancing, with Citrosol introducing the CATsystem® in late 2024, the first automatic in-line control system capable of real-time monitoring of coating concentration and fungicide efficacy. Regulatory pressures are intensifying in parallel. Spanish exporters are increasingly relying on ISO 14001 certified coatings to secure access to premium Northern European retail channels, many of which have announced residue-free fruit finish requirements effective from 2026. As a result, Spain’s citrus coatings landscape is evolving toward data-validated, compliance-first solutions that support export resilience despite declining production volumes.

Brazil: Export-Led Demand and Bio-Based Wax Sourcing

Brazil’s citrus fruit coatings industry is being propelled by expanding export access, rising domestic citrus valuations, and a strategic shift toward bio-based inputs. In April 2025, a landmark bilateral agreement between Brazil and India granted market access for five Brazilian citrus varieties, triggering immediate investment in export-grade wax treatments capable of preserving fruit integrity during long-haul maritime transport to Asia. These coatings are increasingly specified for durability, gloss retention, and resistance to dehydration under extended transit conditions, making them central to Brazil’s export competitiveness.

At the regional level, São Paulo has emerged as a focal point for quality-driven coating adoption. With record lime yields reaching 40 tons per hectare in 2025, state authorities mandated enhanced traceability and the use of bio-inputs in surface coatings to meet the expectations of high-value European food service buyers. Economic signals have further reinforced investment. Citrus prices paid by the Brazilian industry reached record levels in early 2025, encouraging juice processors to deploy peel-integrity coatings that protect essential oil content during extraction. On the supply side, Brazilian coating manufacturers have completed a strategic transition to 100% domestically sourced carnauba wax, replacing imported petroleum-based paraffins. This shift aligns with national Green Export initiatives and strengthens Brazil’s positioning as a supplier of sustainably coated citrus to environmentally sensitive markets.

India: Infrastructure-Led Adoption and Crop-Specific Coating Protocols

India’s citrus fruit coatings market is transitioning from limited adoption to structured deployment, driven by government-backed infrastructure programs and crop-specific post-harvest guidelines. In July 2025, the Ministry of Food Processing Industries reported that the Pradhan Mantri Kisan Sampada Yojana had funded upgrades across more than 290 districts, with waxing and grading lines integrated into primary processing units. These investments directly target post-harvest loss reduction, a persistent challenge in India’s citrus supply chain, and have created new demand for standardized wax formulations compatible with semi-automated systems.

Policy guidance has also become more technically prescriptive. Government recommendations issued in 2025 endorsed Bavistin-enriched wax at defined concentrations to extend the shelf life of Nagpur mandarins to nearly four weeks under ambient conditions. This development has enabled reliable long-distance rail transport within India, improving market access for growers in central regions. Complementing these measures, the Agriculture Infrastructure Fund provided debt financing in 2025 for 150 new citrus packhouses, each equipped with modern spray-coating systems designed to ensure uniform application and reduced wastage. From an industry capability standpoint, JBT Marel strengthened its regional footprint by inaugurating a Global Production Center in India in September 2025, localizing the manufacture of food processing and coating equipment for South Asia. Collectively, these developments indicate a shift toward institutionalized, scalable citrus coating practices across India’s production hubs.

Comparative Summary: Country-Level Evolution in Citrus Fruit Coatings

Citrus Fruit Coatings Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Dominant Industry Response

|

Direction of Coating Innovation

|

|

United States

|

Food waste reduction and plastic replacement

|

Rapid adoption of plant-based edible coatings

|

Automation, infrared drying, and precision dosing

|

|

Spain

|

Yield pressure and export compliance

|

Shift to biocontrol and residue-free waxes

|

Real-time monitoring and certified formulations

|

|

Brazil

|

Export expansion and price incentives

|

Investment in peel-integrity and bio-waxes

|

Carnauba-based, long-haul performance coatings

|

|

India

|

Infrastructure funding and loss reduction

|

Scaling of waxing and grading lines

|

Crop-specific protocols and localized equipment

|

Citrus Fruit Coatings Market Report Scope

Citrus Fruit Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$215.2 Million

|

|

Market Size (2034)

|

$399 Million

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Coating Type (Wax-Based Coatings, Plant-Derived and Edible Coatings, Fungicide-Incorporated Coatings), By Citrus Variety (Oranges, Lemons and Limes, Mandarins and Tangerines, Grapefruits), By Application Method (Spray Coating, Dipping and Immersion, Brush and Roller Coating, Fogging and Cold Misting), By End-User Industry (Fresh Fruit Exporters, Retail and Supermarkets, Industrial Juice Processors, Direct-to-Consumer Platforms)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AgroFresh Solutions, Inc., JBT Corporation, Apeel Sciences, Inc., Productos Citrosol, S.A., Pace International, LLC, Fomesa Fruitech, UPL Limited, Citrosuco S.A., BASF SE, Akzo Nobel N.V., SUEZ S.A., CHRYSO Group, Xeda International, Infraca S.L., River-Cide Services, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Citrus Fruit Coatings Market Segmentation

By Coating Type

- Wax-Based Coatings

- Carnauba Wax

- Shellac

- Beeswax

- Paraffin Wax

- Plant-Derived and Edible Coatings

- Cellulose-Based

- Chitosan-Based

- Protein-Based

- Fungicide-Incorporated Coatings

- Imazalil

- Thiabendazole

- Fludioxonil

By Citrus Variety

- Oranges

- Lemons and Limes

- Mandarins and Tangerines

- Grapefruits

By Application Method

- Spray Coating

- Dipping and Immersion

- Brush and Roller Coating

- Fogging and Cold Misting

By End-User Industry

- Fresh Fruit Exporters

- Retail and Supermarkets

- Industrial Juice Processors

- Direct-to-Consumer Platforms

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Citrus Fruit Coatings Industry

- AgroFresh Solutions, Inc.

- JBT Corporation

- Apeel Sciences, Inc.

- Productos Citrosol, S.A.

- Pace International, LLC

- Fomesa Fruitech

- UPL Limited

- Citrosuco S.A.

- BASF SE

- Akzo Nobel N.V.

- SUEZ S.A.

- CHRYSO Group

- Xeda International

- Infraca S.L.

- River-Cide Services, Inc.

*- List not Exhaustive