Clear Coatings Market Size, Growth Trajectory, and High-Performance Application Insights

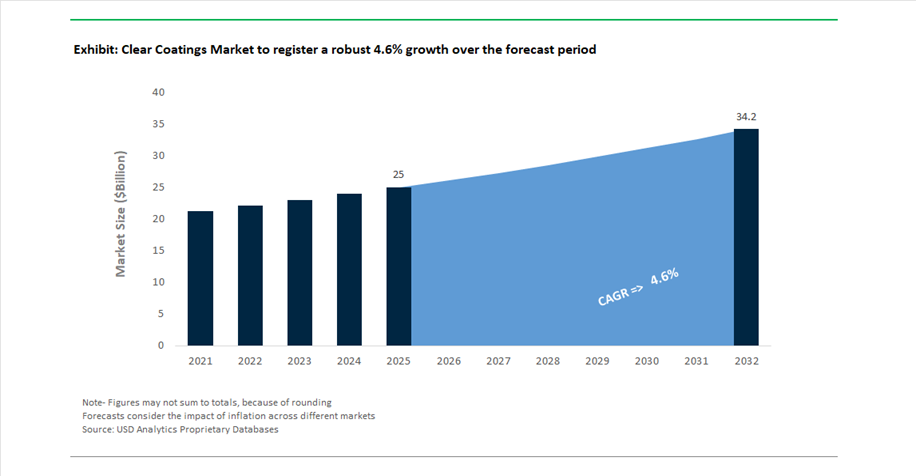

The global clear coatings market reached a valuation of $25 billion in 2025 and is projected to grow at a CAGR of 4.6% between 2025 and 2032, ultimately attaining $34.3 billion by 2032. This steady expansion reflects sustained demand across automotive OEM, refinish, industrial equipment, wood finishes, and consumer appliances, where clear coatings play a critical role in enhancing durability, corrosion resistance, UV stability, and aesthetic appeal.

Clear coatings, often referred to as transparent protective layers, are increasingly being engineered with advanced resin chemistries, low-VOC formulations, and high-performance curing technologies. The market is undergoing a structural shift toward energy-efficient curing systems, lightweight coating solutions, and multi-layer optical enhancement technologies, particularly in automotive and electronics applications. The increasing penetration of electric vehicles (EVs) and premium mobility solutions is accelerating demand for high-gloss, scratch-resistant, and chemically stable clearcoat systems capable of maintaining visual integrity under harsh environmental conditions.

In addition, regulatory pressures targeting volatile organic compound (VOC) emissions and industrial carbon footprints are reshaping product innovation strategies. Manufacturers are prioritizing waterborne, powder-based, and low-temperature curing clear coatings, aligning with global sustainability mandates while improving operational efficiency for end users such as automotive body shops and appliance manufacturers.

The market is also benefiting from infrastructure development and rising construction activity, particularly in emerging economies, where clear coatings are widely used in wood finishes, architectural varnishes, and protective sealants. Simultaneously, innovation in nano-coatings and hybrid polymer systems is enabling improved performance characteristics such as self-healing, anti-fingerprint, and anti-microbial properties, further expanding application scope.

Strategic M&A, Product Innovation, and Energy-Efficient Technologies Reshaping the Clear Coatings Market

Recent developments in the clear coatings market highlight a strong emphasis on portfolio optimization, performance differentiation, and sustainability-driven innovation. A significant structural shift is underway with BASF’s agreement to divest its Automotive OEM and Refinish coatings business, including its clearcoat portfolio, to Carlyle and the Qatar Investment Authority for €4.5 billion. The transaction, expected to close in mid-2026, will establish a standalone coatings entity under new leadership, with Jens Luehring announced as CEO in March 2026. This move reflects increasing investor interest in specialized coatings platforms and signals further consolidation in the global coatings ecosystem.

Product innovation remains a primary competitive lever. In March 2026, PPG Industries introduced an ultra-fast-drying clearcoat under its DELTRON® automotive refinish line, significantly reducing bake times in collision repair operations. This advancement directly addresses industry demand for higher throughput and reduced energy consumption, without compromising gloss and durability. Building on this, PPG launched a dual-tier clearcoat portfolio in April 2026, targeting both cost-sensitive and premium repair segments, enabling body shops to optimize performance-to-cost ratios across diverse repair requirements.

Technological innovation is also evident in curing processes. In March 2026, PPG partnered with IPG Photonics and Whirlpool to commercialize laser-based powder curing technology, representing a breakthrough for clear powder coatings. This method offers precise energy delivery, reduced cycle times, and superior finish clarity, outperforming conventional thermal curing systems. Similarly, Axalta’s R&D 100 Award-winning low-energy curing system (November 2025) demonstrates industry-wide momentum toward low-temperature curing solutions, enabling reduced carbon emissions and operational costs for automotive refinishing applications.

Strategic expansion initiatives are further shaping regional dynamics. The Sherwin-Williams acquisition of BASF’s Brazilian architectural coatings business (July 2025, ongoing into 2026) strengthens its footprint in South America, particularly in wood coatings and clear protective finishes, enhancing supply chain control and market penetration. Meanwhile, Axalta’s 2026 Color of the Year launch (“Solar Boost”) underscores the increasing role of advanced clearcoat layering technologies in achieving complex visual effects, especially in EV and luxury vehicle segments.

Finally, high-performance applications continue to drive innovation at the extreme end of the spectrum. The extended partnership between AkzoNobel and McLaren Racing (January 2026) focuses on developing ultra-lightweight, aerodynamically optimized clear coatings, with direct technology transfer into commercial product lines. This reinforces a broader industry trend toward performance-driven material science, where coatings are engineered not just for protection but also for weight reduction, efficiency gains, and functional enhancement.

EU BPA Ban Reshaping Clear Coatings for Metal Packaging Applications

The clear coatings industry is undergoing a fundamental reformulation cycle following the enforcement of Commission Regulation (EU) 2024/3190, which mandates the elimination of Bisphenol A (BPA) from food-contact materials. This regulation directly impacts epoxy-based clear coatings used in metal packaging, forcing a rapid transition toward alternative chemistries.

The compliance timeline is aggressive. While the regulation entered into force in January 2025, full industry compliance is required by July 20, 2026, with limited exemptions extending to 2028 for specific applications such as processed fish and certain vegetables. The regulatory framework imposes extremely low migration limits, capping free BPA at ≤ 1 μg/kg, effectively requiring non-detectable levels in compliant formulations.

This has triggered a large-scale material shift. As of 2026, more than 75% of European metal packaging lines have transitioned away from epoxy systems toward polyester and polyacrylate-based clear coatings. These alternatives offer comparable barrier performance while eliminating regulatory risks associated with bisphenol compounds.

The implications extend beyond compliance into supply chain restructuring. Coating manufacturers are redesigning formulations to maintain adhesion, corrosion resistance, and food safety performance without relying on traditional epoxy resins. This transition is also influencing global markets, as multinational packaging companies standardize BPA-free coatings across regions to ensure regulatory alignment and simplify procurement.

This regulatory-driven transformation is redefining material selection in the clear coatings industry, positioning BPA-free systems as the new baseline for food-contact applications.

California VOC and MIR Limits Accelerating High-Solids Clear Coat Adoption

The automotive refinish segment is experiencing parallel regulatory pressure in the United States, particularly under California’s SCAQMD Rule 1151 and CARB emission standards. These regulations are tightening VOC limits and introducing Maximum Incremental Reactivity constraints, fundamentally altering formulation strategies for clear coatings.

A key development is the differentiation between gloss and matte clear coatings, each subject to distinct VOC-per-liter thresholds. At the same time, manufacturers must meet stringent reactivity limits, targeting approximately 0.38 g O₃ per gram of VOC to ensure compliance with ozone formation standards. This dual constraint—limiting both VOC content and reactivity—has increased formulation complexity, requiring the use of advanced solvent systems and reactive diluents.

Application efficiency is also under regulatory scrutiny. Professional refinish operations must now utilize equipment capable of achieving a minimum transfer efficiency of 65%, reducing overspray and associated emissions. This requirement is driving changes in both coating chemistry and application technology.

The net effect is a strong shift toward high-solids clear coatings, which offer lower VOC emissions while maintaining performance. Adoption of these systems has increased by approximately 15% year-over-year, supported by their ability to deliver high gloss, durability, and compliance with hazardous air pollutant restrictions.

Anti-Fingerprint Clear Coatings Enhancing Durability and Hygiene in Stainless Steel Applications

The growing demand for low-maintenance, aesthetically durable surfaces in appliances and commercial equipment is driving the adoption of anti-fingerprint clear coatings. These advanced coatings utilize oleophobic and hydrophobic surface treatments to reduce surface energy, preventing the adhesion of oils and contaminants.

Performance characteristics are highly optimized. Modern anti-fingerprint coatings achieve water contact angles exceeding 100 degrees and oil contact angles above 65 degrees, enabling surfaces to resist smudging and facilitating easier cleaning. In practical terms, this translates into up to 90% reduction in cleaning effort compared to untreated stainless steel surfaces.

Durability is a critical differentiator. Industrial-grade coatings are engineered to withstand more than 20,000 abrasion cycles under standardized testing conditions without losing functionality, ensuring long-term performance in high-use environments. Additionally, these coatings are applied at ultra-thin thicknesses below 5 micrometers, preserving the natural appearance of brushed stainless steel while preventing discoloration or yellowing over extended periods.

Self-Healing Clear Coatings Driving Premium Surface Protection in Automotive and Marine Sectors

The advancement of smart polymer technologies is creating a high-growth opportunity for self-healing clear coatings, particularly in luxury automotive and marine applications. These coatings incorporate microcapsule-based systems or dynamic covalent bonding mechanisms that enable autonomous repair of surface damage.

Performance capabilities are significant. Next-generation self-healing coatings can repair up to 80% of micro-scratches within 15 minutes when exposed to sunlight or moderate heat, maintaining surface integrity without the need for mechanical intervention. This functionality is particularly valuable in high-end applications where surface aesthetics are critical to product value.

Durability improvements further enhance their appeal. In accelerated weathering tests, these coatings retain more than 90% of their original gloss after 2,000 hours of UV exposure, significantly outperforming conventional high-solids clear coats. Additionally, they offer a 30% improvement in resistance to UV-induced degradation, preventing common issues such as chalking and oxidation.

Economic benefits are also evident. In the marine sector, vessels coated with self-healing systems maintain approximately 15% higher resale value over five years, reflecting reduced maintenance requirements and sustained visual quality.

Polyurethane Clear Coatings Lead Market with 34% Share Driven by Superior Durability and Automotive-Grade Performance

Resin Type Analysis: 2K Polyurethane Systems Dominate with UV Resistance and High Gloss Retention

Polyurethane (PU) clear coatings hold a leading 34.0% share of the global clear coatings market in 2025, driven by their unmatched combination of UV resistance, chemical durability, abrasion resistance, and flexibility. Widely used in automotive OEM clearcoats, industrial wood coatings, and high-performance finishes, PU systems—particularly 2K aliphatic polyurethane coatings—deliver long-term gloss retention and distinctness of image (DOI) for over a decade under harsh environmental exposure. These coatings exhibit superior resistance to acid rain, bird droppings, car wash abrasion, and mechanical wear, making them the industry standard for automotive topcoats and premium furniture finishes. A major trend in 2025 is the rapid adoption of waterborne 2K polyurethane clear coatings, which reduce VOC emissions by 80–90% while maintaining performance parity with solvent-based systems. This shift is accelerating growth in eco-friendly clear coatings and high-performance industrial coatings markets.

Automotive Sector Dominates Clear Coatings Market with 38% Share Driven by Premium Finishes and Performance Requirements

Application Area Analysis: OEM and Refinish Clearcoats Drive High-Value Demand

The automotive segment accounts for a dominant 38.0% share of the clear coatings market in 2025, reflecting its role as the most technologically advanced and performance-driven application area. Automotive clearcoats—primarily high-solids 2K polyurethane systems—are applied over basecoats to provide scratch resistance, UV protection, chemical durability, and high-gloss finishes, with typical film thickness of 35–50 microns. These coatings must meet stringent performance standards, including acid etch resistance, gravel impact durability, and long-term weathering stability, ensuring vehicle longevity and aesthetic appeal. The automotive refinish market further drives demand with fast-curing clearcoats optimized for collision repair efficiency and showroom-quality finishes. Additionally, the rise of matte and satin clearcoats—now a mainstream premium feature—along with increasing use in electric vehicles and advanced display coatings, is boosting value growth. These factors firmly position automotive as the leading segment in the global clear coatings market.

Clear Coatings Market Competitive Landscape Driven by High-Gloss Finishes, UV-Resistant Technologies, and Sustainable Clearcoat Systems

The clear coatings market is highly competitive, driven by high-solids clearcoats, UV-resistant coatings, and non-yellowing finishes. Leading players are focusing on automotive clearcoats, industrial wood coatings, and sustainable waterborne technologies to enhance durability, optical clarity, and regulatory compliance across automotive, aerospace, and architectural applications.

Sherwin-Williams expands clear coatings leadership through self-healing automotive finishes and wood coating innovation

Sherwin-Williams strengthens its position in the clear coatings market through advanced industrial wood and automotive clearcoat technologies. The acquisition of BASF’s decorative paints business enhances its footprint in high-performance clear topcoats. Its Colormix Forecast collections utilize non-yellowing clear sealers that enhance natural wood aesthetics in architectural applications. The company is advancing self-healing clearcoats using thermal-reactive polymers to repair micro-scratches in automotive refinish markets. Its Aurora Color System integrates gloss control with basecoat chemistry for precise color matching. With over $23 billion in annual revenue, Sherwin-Williams focuses on high-clarity coatings, durability, and digital integration.

AkzoNobel drives sustainable clear coatings with superdurable finishes and bio-based innovation

AkzoNobel is a key innovator in clear coatings, combining sustainability with high-performance finishes across industrial and aerospace sectors. Its Aerodur basecoat-clearcoat system enhances fuel efficiency and weight reduction in aviation applications. The company expanded its Interpon D portfolio with superdurable clear finishes offering over 25 years of UV resistance. Strategic collaboration with BASF and Arkema supports the transition to bio-attributed raw materials. A 47% reduction in Scope 1 and 2 emissions highlights its sustainability leadership. The proposed Axalta merger is expected to strengthen global R&D capabilities. Product development focuses on durable coatings, sustainability, and advanced powder clearcoats.

PPG advances clearcoat technologies with automation, UV protection, and aerospace-grade innovation

PPG Industries leads in clear coatings innovation through advanced automation and high-performance formulations. Its MOONWALK and LINQ platforms optimize clearcoat mixing and reduce material waste by up to 15%. The SOLARON Blue Protection technology provides UV-blocking clearcoats with full optical clarity for aerospace applications. Significant investment in a North Carolina facility supports expansion in EV and aerospace clearcoat chemistries. PPG has also captured a strong share in packaging coatings through BPA-NI clear linings. With a strong patent portfolio, the company focuses on digital coating solutions, sustainability, and high-performance clear finishes.

Axalta accelerates clear coatings innovation with AI-driven application systems and EV safety coatings

Axalta Coating Systems is a leading innovator in clear coatings, driven by digitalization and high-performance mobility coatings. Its EcoNextJet system enables precision application of color and clearcoats at production scale. The company achieved a record 22% EBITDA margin in 2025, supporting continued R&D investment. Its Alesta e-PRO coatings provide fire-resistant protection for EV batteries at temperatures exceeding 1200°C. TintMaster AI enhances manufacturing efficiency by improving first-time accuracy by 29%. Strategic focus on mobility and refinish segments strengthens its premium coatings portfolio. Product innovation centers on AI integration, EV coatings, and high-durability finishes.

Nippon Paint strengthens clear coatings portfolio with high-solids automotive finishes and renovation-driven demand

Nippon Paint is a dominant force in clear coatings, particularly in automotive OEM and Asian renovation markets. The acquisition of AOC strengthens its position in specialty chemicals and high-margin coating segments. Its high-solids clearcoats deliver superior depth-of-image for automotive finishes, widely adopted by Japanese OEMs. The company has shifted focus toward renovation and maintenance, which now accounts for over 70% of decorative sales in Asia. Waterborne clearcoats aligned with VOC regulations support its sustainability goals. With strong revenue growth, Nippon Paint focuses on green coatings, automotive finishes, and regional market expansion.

China Clear Coatings Market: Intelligent Manufacturing and Waterborne Shift Driving Global Leadership

China dominates the global clear coatings market, transitioning rapidly toward high-tech, low-carbon solutions aligned with its “Dual Carbon” goals. The commissioning of advanced facilities such as Allnex’s Jiaxing site is accelerating production of UV-curable and waterborne resins, particularly for premium automotive clear coats.

The country’s massive automotive sector—projected to reach 35 million units by 2025—is a major demand driver for high-gloss, scratch-resistant clear finishes, especially in New Energy Vehicles (NEVs). Additionally, tightening air quality regulations have triggered a 40% shift from solvent-based to waterborne clear coatings in key industrial clusters. Growth in renewable energy and electronics is also expanding applications, with self-cleaning hydrophobic coatings for solar panels and ultra-thin protective coatings for consumer electronics. These developments reinforce China’s leadership in both scale and innovation.

United States Clear Coatings Market: Infrastructure Modernization and Semiconductor Expansion Driving Demand

The United States clear coatings market is benefiting from a manufacturing resurgence and strong federal investment. The CHIPS Act is driving demand for ultra-high-purity clear coatings in semiconductor fabrication facilities, while the Infrastructure Investment and Jobs Act (IIJA) is supporting adoption of epoxy and polyurethane clear sealants for bridge rehabilitation.

The automotive refinish segment remains a key growth engine due to an aging vehicle fleet and high repair standards. Sustainability trends are also shaping the market, with stricter VOC regulations pushing manufacturers toward bio-based and energy-curable clear coatings. Additional growth is coming from sustainable packaging, where clear coatings enhance barrier properties while maintaining recyclability, and from aerospace maintenance, which requires UV-resistant clear topcoats.

Germany Clear Coatings Market: Circular Economy and Self-Healing Coatings Leading Premium Innovation

Germany continues to lead in premium clear coating technologies, particularly through sustainability and circular economy initiatives. The commercialization of mass-balance bio-circular clear coats is reducing CO₂ emissions by up to 50%, aligning with EU environmental targets.

Innovation is particularly strong in the automotive sector, where partnerships with luxury OEMs are advancing self-healing clear coats capable of repairing micro-scratches through heat-induced reflow. Regulatory compliance under REACH is accelerating the transition toward PFAS-free and isocyanate-free systems, while pharmaceutical and food sectors are driving demand for antimicrobial clear coatings. Additionally, the furniture industry is rapidly adopting UV-LED curable clear finishes, enabling instant curing and zero VOC emissions.

India Clear Coatings Market: Urbanization and Automotive Investment Driving High Growth

India’s clear coatings market is evolving rapidly, supported by strong foreign investment and infrastructure expansion. With $25 billion in FDI in the automotive sector, demand for OEM clear coats is rising significantly alongside vehicle production.

Regulatory pressure is also accelerating change, with stricter VOC deadlines pushing the industry toward water-based clear coatings. Infrastructure projects under the National Infrastructure Pipeline are increasing demand for anti-carbonation clear coatings for bridges and transit systems. Growth in logistics and e-commerce is driving adoption of chemical-resistant epoxy clear coatings for industrial flooring, while urban design trends are boosting demand for decorative clear finishes on exposed concrete and brick.

Japan Clear Coatings Market: EV-Specific Coatings and Nanotechnology Driving Advanced Applications

Japan is a leader in advanced material science for clear coatings, particularly in EV and electronics applications. The development of in-mold coating (IMC) technology has significantly reduced VOC emissions (up to 99%) while improving manufacturing efficiency for thermoplastic components.

Innovation is focused on multifunctionality. Japan is advancing heat-reflective and insulating clear coatings to optimize EV battery performance, as well as nanocoatings with 9H+ hardness for superior durability. Additional applications include optical clear coatings for displays and non-toxic antifouling coatings for marine vessels. These developments position Japan at the forefront of high-performance, next-generation clear coatings.

South Korea Clear Coatings Market: Electronics Leadership and Smart Infrastructure Driving Innovation

South Korea’s clear coatings market is closely tied to its dominance in electronics and semiconductor industries. Innovations in ultra-flexible, high-transparency coatings are supporting foldable OLED displays capable of withstanding over 200,000 folds.

Smart city initiatives are also driving demand for anti-graffiti and photocatalytic clear coatings in public infrastructure. In shipbuilding, the adoption of high-build epoxy clear systems for LNG carriers is enhancing durability under cryogenic conditions. Additionally, stringent environmental regulations targeting fine dust pollution are accelerating the transition toward powder clear coatings, eliminating solvent emissions. These factors position South Korea as a leader in high-performance and multifunctional clear coating technologies.

Vietnam Clear Coatings Market: Manufacturing Shift and Furniture Export Boom Driving Demand

Vietnam is emerging as a key growth market for clear coatings, driven by manufacturing diversification and strong export demand. As a global furniture export hub, the country is seeing high adoption of UV-curable clear wood coatings for high-speed production lines.

The broader industrial sector is also expanding, with increased demand for coatings in electronics and appliance manufacturing. Rapid urbanization is boosting the use of protective clear coatings for architectural steel and facades, while investments in automation and digital quality control are improving production efficiency. These developments position Vietnam as a strategic secondary hub in the global coatings supply chain.

Brazil Clear Coatings Market: Automotive Refinish and Agribusiness Applications Driving Growth

Brazil’s clear coatings market is driven by strong demand in the automotive aftermarket and agricultural sectors. The automotive refinish segment is a major growth engine, with high demand for quick-dry polyurethane clear coats due to vehicle wear and road conditions.

Agribusiness is another key driver, requiring chemical-resistant clear coatings to protect machinery from fertilizers and harsh environments. Regulatory developments such as the “Fuel of the Future” law are increasing demand for ethanol-resistant coatings in fuel storage infrastructure. Additionally, the rise of premium automotive finishes and sustainable packaging is boosting demand for high-transparency, recyclable clear coatings, while local resin production is strengthening supply chains.

Clear Coatings Market Report Scope

Clear Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25 Billion

|

|

Market Size (2032)

|

$34.3 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Resin (Acrylic Clear Coatings, Polyurethane (PU), Epoxy Clear Coatings, Polyester, Specialty Resins, Fluoropolymers, Silicone and Silane-Modified, Bio-based Resins), By Technology (Water-borne, Solvent-borne, Powder Clear Coatings, UV-Cured and Radiation Curable), By Application Area (Automotive, Industrial Wood, General Industrial, Consumer Electronics, Packaging, Aerospace and Marine), By End-Use Sector (Residential and Commercial Construction, Automotive and Transportation, Consumer Goods and Electronics, Packaging and Industrial Goods)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Axalta Coating Systems Ltd., BASF SE, Nippon Paint Holdings Co., Ltd., RPM International Inc., Kansai Paint Co., Ltd., Jotun A/S, Hempel A/S, Asian Paints Limited, Berger Paints India Limited, Beckers Group, Sika AG, Benjamin Moore & Co.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Clear Coatings Market Segmentation

By Resin

- Acrylic Clear Coatings

- Polyurethane (PU)

- Epoxy Clear Coatings

- Polyester

- Specialty Resins

- Fluoropolymers

- Silicone and Silane-Modified

- Bio-based Resins

By Technology

- Water-borne

- Solvent-borne

- Powder Clear Coatings

- UV-Cured and Radiation Curable

By Application Area

- Automotive

- Industrial Wood

- General Industrial

- Consumer Electronics

- Packaging

- Aerospace and Marine

By End-Use Sector

- Residential and Commercial Construction

- Automotive and Transportation

- Consumer Goods and Electronics

- Packaging and Industrial Goods

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Clear Coatings Market

- Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Axalta Coating Systems Ltd.

- BASF SE

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Kansai Paint Co., Ltd.

- Jotun A/S

- Hempel A/S

- Asian Paints Limited

- Berger Paints India Limited

- Beckers Group

- Sika AG

- Benjamin Moore & Co.

*- List not Exhaustive