Coated Steel Market Size, Green Steel Transition, and High-Performance Coating Demand Dynamics

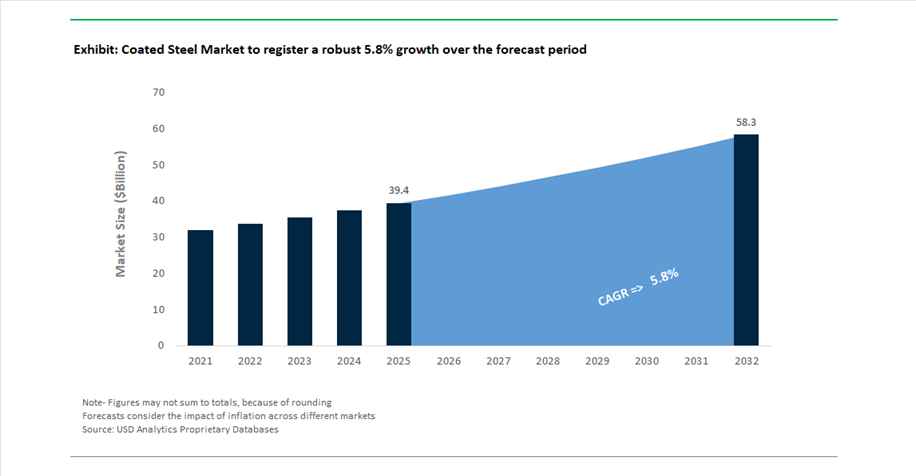

The global coated steel market was valued at $39.4 billion in 2025 and is projected to grow at a CAGR of 5.8% between 2025 and 2032, reaching $58.5 billion by 2032. This expansion is being driven by strong demand across construction, automotive manufacturing, appliances, renewable energy infrastructure, and industrial equipment, where coated steel provides essential benefits such as corrosion resistance, enhanced durability, aesthetic finish, and lifecycle cost efficiency.

A defining trend shaping the market is the rapid transition toward green steel and low-carbon coated steel solutions, as manufacturers respond to tightening environmental regulations and sustainability mandates. Leading producers are investing heavily in carbon-neutral production processes, recycled steel integration, and eco-friendly coating technologies, particularly for automotive and infrastructure applications. The rise of renewable energy projects, including solar and wind installations, is further accelerating demand for advanced metallic-coated steel products designed to withstand harsh environmental conditions over extended service lifespans.

Technological advancements in coating processes, including galvanization, galvannealing, pre-painted coatings, and alloy-based metallic coatings, are enhancing product performance across applications. The growing adoption of zinc-aluminum-magnesium (Zn-Al-Mg) coatings and high-performance organic coatings is enabling superior corrosion resistance and reduced maintenance requirements, making coated steel increasingly attractive for coastal infrastructure, industrial facilities, and high-humidity environments.

Additionally, rapid industrialization in Asia-Pacific, particularly India, is strengthening domestic production capabilities and reducing reliance on imports. Strategic investments in new coating lines, greenfield plants, and capacity expansions are positioning the region as a global hub for coated steel manufacturing. The integration of smart manufacturing technologies and automation is further improving production efficiency and quality consistency, reinforcing the long-term growth outlook for the market.

Mega Mergers, Green Steel Commercialization, and Capacity Expansion Reshaping the Coated Steel Ecosystem

The coated steel market is undergoing a transformative phase marked by large-scale mergers, sustainability-driven product innovation, and aggressive capacity expansion strategies. A landmark development occurred in March 2026, when Nippon Steel Corporation finalized its $14.9 billion acquisition of United States Steel Corporation, creating a combined entity with over 86 million tons of annual production capacity. This integration enables the deployment of advanced coating technologies, including high-grade automotive galvannealed and tin-free steel, directly within the North American market, reducing trade dependencies and strengthening regional supply chains.

Sustainability-led product innovation is gaining strong momentum. In February 2026, JSW Steel introduced its GreenEdge low-emission steel brand, incorporating coated steel products backed by verified carbon credits, with approximately 1 million tonnes of CO₂ credits secured for initial rollout. Similarly, SSAB’s commercialization of SSAB Zero™ in partnership with Volvo Cars (March 2026) marks a critical milestone in the adoption of fossil-free, recycled-based coated steel for automotive applications, enabling reduced carbon footprints without compromising performance standards.

India is emerging as a key growth engine through aggressive portfolio expansion and infrastructure investments. ArcelorMittal Nippon Steel India (AM/NS India) has been at the forefront, launching Magnelis® (September 2024) for solar applications and introducing Vibrance and Optima (February 2026) for appliance and industrial sectors. Additionally, the company laid the foundation for a greenfield steel plant in Andhra Pradesh in March 2026, which will include advanced coating lines for high-end galvanized and color-coated steel, aligning with import substitution and renewable energy demand.

Capacity expansion and consolidation strategies are also intensifying among domestic players. Jindal (India) Limited commissioned a new coating line in February 2026, increasing output capacity by 60% to nearly 300,000 tons annually, while Tata Steel’s acquisition of full control over Tata BlueScope Steel (December 2025) strengthens its position in premium color-coated steel for infrastructure and construction. Furthermore, Tata Steel’s $2 billion overseas investment and NINL merger approval (March 2026) is aimed at streamlining production and accelerating investments in high-value coated steel and green technologies.

At the same time, strategic challenges persist in global expansion initiatives. The delayed acquisition of Thyssenkrupp Steel Europe by Jindal Steel International (March 2026) highlights complexities associated with pension liabilities and regulatory approvals, impacting plans for green hydrogen-based coated steel production in Europe. Despite these hurdles, the broader industry trajectory remains firmly aligned with decarbonization, vertical integration, and advanced coating innovation, positioning coated steel as a critical material in next-generation industrial and infrastructure ecosystems.

Regulatory Push Toward Waterborne and High-Solids Coating Systems Reshaping Coated Steel Manufacturing

The coated steel market is undergoing a structural transformation as environmental regulations accelerate the phase-out of solvent-based coatings in favor of waterborne, high-solids, and UV-curable systems. The enforcement of the EU Industrial Emissions Directive (IED) Amending Directive (EU) 2024/1785 in August 2024 has created a compliance-driven shift across European steel coating operations. Under this directive, industrial installations are mandated to implement Environmental Management Systems (EMS) by July 2030, including detailed circular economy transition plans. This regulatory framework is directly increasing the adoption of low-VOC coating technologies across coil coating lines, galvanized steel processing, and pre-painted steel manufacturing.

The regulatory timeline is further compressing investment cycles, with EU Member States required to transpose these standards into national law by July 2026. Newly commissioned coating systems must demonstrate immediate compliance, prompting accelerated capital allocation toward waterborne polyurethane and advanced high-solids coatings. According to findings published in the Journal of Coatings Technology and Research (2025), next-generation waterborne polyurethane coatings deliver up to 44% reduction in lifecycle carbon emissions compared to solvent-based systems, while maintaining corrosion resistance standards required for C4 and C5 environments. This convergence of environmental compliance and performance parity is reinforcing waterborne coatings as the new baseline technology in the global coated steel industry.

Zinc-Aluminum-Magnesium Coated Steel Gains Momentum in India’s Pre-Engineered Building Sector

The rapid expansion of India’s infrastructure ecosystem is catalyzing the adoption of Zinc-Aluminum-Magnesium (ZAM) coated steel, particularly within the Pre-Engineered Building (PEB) segment. Driven by the scale of the National Infrastructure Pipeline and the need for high-durability materials in aggressive environments, ZAM coatings are emerging as a superior alternative to conventional galvanization. In September 2024, ArcelorMittal Nippon Steel India introduced Magnelis®, a locally produced ZAM-coated steel product designed to reduce reliance on imports while aligning with India’s ambition to achieve 300 million tonnes of crude steel capacity by 2030.

From a technical perspective, ZAM coatings provide up to three times higher corrosion resistance compared to standard galvanized steel, as highlighted by the Ministry of Steel (India). A key differentiator is the “self-healing” property at cut edges, which significantly enhances durability in coastal, industrial, and high-humidity environments. This capability is particularly critical for PEB structures, warehouses, and industrial sheds exposed to aggressive atmospheric conditions. Supporting this transition, AM/NS India commissioned a dedicated Continuous Galvanizing Line (CGL) in July 2025 to manufacture advanced coated steel grades for industrial and appliance applications, signaling a strategic industry shift toward value-added steel production.

Growing Demand for On-Site Repair Coating Systems in Utility-Scale Solar Steel Structures

The expansion of utility-scale solar infrastructure is unlocking a new service-oriented growth segment for coated steel manufacturers through on-site repair coating systems. Steel tracker mounts, which are critical structural components in solar farms, are prone to coating damage during installation and operation, especially in high-salinity and desert environments. Research from the National Renewable Energy Laboratory (NREL) indicates that solar infrastructure must achieve a 35-year operational lifespan to ensure optimal return on investment, making corrosion protection a critical performance parameter.

To address this need, manufacturers are developing field-applied cold-galvanizing compounds and epoxy-based repair kits designed for rapid deployment and long-term durability. Studies on solar mounting systems in 2025 confirm that the maintenance and retrofit segment is expanding as asset owners prioritize lifecycle extension of high-capital installations. This shift is also driving coated steel producers toward integrated service models, where they offer bundled solutions combining coated steel products with proprietary repair chemistries. Such models are increasingly aligned with renewable energy financing requirements, which now demand extended warranties of up to 25 years backed by robust corrosion protection strategies.

Polymer-Aluminum Composite Coatings Unlock New Pathways for Hydrogen Transport Infrastructure

The emergence of the green hydrogen economy is creating a high-value opportunity for advanced coated steel technologies, particularly in mitigating hydrogen embrittlement (HE) in pipelines and storage systems. Hydrogen transport poses significant material challenges, as atomic hydrogen can diffuse into steel, leading to structural degradation and cracking. Recent research published on ResearchGate demonstrates that internal polymeric coatings, such as 2 mm crosslinked poly(vinyl alcohol) (PVA), can reduce hydrogen concentration at the steel interface by 44% over extended operational periods, significantly enhancing material integrity.

Policy and investment momentum are further accelerating this segment, with India’s National Green Hydrogen Mission receiving ₹600 crore allocation in the 2025–26 Union Budget to support hydrogen infrastructure development. Pilot projects led by NTPC Ltd and GAIL (India) Ltd are actively testing hydrogen blending in existing gas pipelines. These initiatives are validating the effectiveness of advanced coatings such as polytetrafluoroethylene (PTFE) and polyurethane-based systems, which demonstrate up to 57% lower friction coefficients and superior hydrogen barrier performance under pressures reaching 94 bar. As hydrogen economies scale globally, polymer-aluminum composite coatings are expected to become a foundational technology for enabling safe, cost-efficient retrofitting of existing steel infrastructure.

Coated Steel Market Share and Segmentation Insights

Market Share by Coating Process: Hot-Dipped Galvanized (HDG) Leads with 42% Share Driven by Scalable Corrosion Protection

Hot-Dipped Galvanized (HDG) steel commands a leading 42% share of the global coated steel market in 2025, anchored by its cost-effective corrosion protection and deeply entrenched industrial ecosystem. HDG delivers sacrificial zinc protection, forming a metallurgically bonded coating that shields steel from moisture, oxidation, and aggressive environmental exposure, making it the default specification across construction, infrastructure, and general industrial applications. Its economic advantage over advanced alloy coatings and electro-galvanized alternatives, combined with long service life and minimal maintenance requirements, reinforces its widespread adoption. Additionally, HDG benefits from a highly established global supply chain, with continuous galvanizing lines integrated into major steel mills, ensuring consistent coating thickness, uniform quality, and high throughput production. The process also offers strong compatibility with downstream fabrication processes such as welding, forming, and painting, enhancing its versatility across end-use industries. While emerging technologies like zinc-aluminum-magnesium (Zn-Al-Mg) and Galvalume coatings are gaining traction in high-performance environments, HDG remains the backbone of the coated steel market due to its scalability, recyclability, and proven field performance.

Market Share by Application Area: Building and Construction Segment Dominates with 48% Share Fueled by Infrastructure Expansion

The building and construction sector leads the coated steel market with a substantial 48% share in 2025, reflecting its position as the largest global consumer of steel and steel-based products. Coated steel is integral to a wide range of construction applications, including roofing systems, wall cladding, structural framing, gutters, and load-bearing components in residential, commercial, and industrial buildings. The segment’s dominance is driven by the need for materials that combine structural strength with long-term corrosion resistance, particularly in outdoor and high-humidity environments. Coated steel variants such as HDG, Galvalume (aluminum-zinc), zinc-aluminum-magnesium alloys, and color-coated steel are widely specified to achieve extended service lifespans of 20 to 50 years with minimal maintenance, significantly reducing lifecycle costs for builders and asset owners. Rapid urbanization, large-scale infrastructure projects, and increasing demand for durable, low-maintenance building materials in emerging economies are further accelerating coated steel consumption in this segment. As sustainability and lifecycle performance become central procurement criteria, coated steel continues to solidify its role as a foundational material in modern construction ecosystems.

Coated Steel Market Competitive Landscape Driven by Advanced High-Strength Steel, Corrosion-Resistant Coatings, and Low-Carbon Production

The coated steel market is highly competitive, driven by advanced high-strength steel (AHSS), galvanized and pre-painted steel, and low-carbon steel technologies. Key players are focusing on corrosion-resistant coatings, EV-grade steel, and sustainable manufacturing to meet rising demand across automotive, construction, energy, and infrastructure sectors.

ArcelorMittal leads coated steel innovation with low-carbon XCarb and EV-grade AHSS solutions

ArcelorMittal dominates the coated steel market with strong global revenues of $61.35 billion and a strategic shift toward low-carbon steel production. Its XCarb platform integrates sustainable steelmaking with advanced coatings for automotive and infrastructure applications. The launch of Usibor 1500 XCarb steel for EV platforms delivers 10–15% weight reduction with enhanced corrosion resistance. Significant investments of $1.1 billion support renewable-powered coated steel expansion in Brazil and India. The company’s expertise in Galvaneal and Alusi coatings strengthens its leadership in EV and construction segments. Product innovation focuses on lightweight steel, corrosion resistance, and decarbonization.

China Baowu drives coated steel scale with ZAM coatings and AI-enabled smart manufacturing

China Baowu Steel Group leads in coated steel production scale, focusing on efficiency and high-value coated products. Its ZAM coating technology offers three times the corrosion resistance of traditional galvanization, supporting solar and infrastructure applications. The company recorded 6.5 million metric tons in exports, driven by strong demand for pre-painted steel in emerging markets. Implementation of AI-enabled "lights-out" manufacturing enhances coating precision and operational efficiency. Pricing adjustments in 2026 reflect rising alloy costs and value-added product positioning. Product development focuses on smart manufacturing, corrosion-resistant coatings, and export-driven growth.

Nippon Steel strengthens specialty coated steel with ZAM technologies and global expansion strategy

Nippon Steel is advancing its coated steel portfolio through high-performance products and global expansion initiatives. Its ZAM and SuperDyma coatings are optimized for data center infrastructure and coastal environments requiring long-term durability. The company is pursuing a major acquisition strategy in North America to expand its coated steel footprint. Investments of ¥6 trillion aim to transition toward hydrogen-based steelmaking and advanced electrical steel coatings. Focus on specialty applications such as clean energy and defense enhances margin stability. Product innovation centers on high-performance coatings, sustainability, and specialty steel segments.

POSCO advances coated steel with PosMAC innovation and integration into energy materials ecosystem

POSCO is a key innovator in coated steel, driven by its PosMAC magnesium-aluminum alloy coating technology. PosMAC delivers superior corrosion resistance for solar farms and agricultural applications in harsh environments. The company’s dual focus on steel and energy materials creates synergies in EV battery and structural applications. Localization strategies in Southeast Asia strengthen its competitive position amid global trade barriers. Automation initiatives enhance safety and efficiency in coating operations. Product development focuses on advanced coatings, renewable energy applications, and integrated material solutions.

JSW Steel expands coated steel capacity with value-added products and export-driven growth

JSW Steel is rapidly expanding its coated steel presence through capacity additions and strategic partnerships. The company recorded production growth of 6% and significant export expansion of 53% in 2025. Its joint venture with JFE Steel strengthens capabilities in high-end electrical steel and coated products. Investments in new production facilities support long-term growth in value-added coated steel. Its Colouron+ and Platina brands lead in roofing and appliance applications with eco-friendly coatings. Product strategy focuses on export markets, infrastructure demand, and sustainable coated steel solutions.

India Coated Steel Market: PLI-Led Expansion and Automotive Transformation Driving High Growth

India has emerged as the fastest-growing market for coated steel, fueled by aggressive policy support and rising demand from automotive and infrastructure sectors. The launch of PLI Scheme 1.2 (Feb 2026) has formalized investments of ₹11,887 crore ($1.43 billion) across 55 companies, specifically targeting specialty and coated steel production.

Capacity expansion is a key driver, with total commitments across PLI phases reaching ₹43,874 crore ($5.28 billion), aimed at adding 8.7 million tonnes of specialty steel capacity by FY2031. Strategic developments such as the JSW–POSCO joint venture (6 MTPA) are accelerating production of high-grade galvanized and cold-rolled coils for automotive applications. Demand is also surging under the Smart Cities Mission ($19.67 billion funding), boosting adoption of PPGI and PPGL for urban infrastructure. Additionally, India’s shift toward Advanced High-Strength Steel (AHSS) with anti-corrosive coatings is supporting EV lightweighting, while import substitution policies aim to reduce reliance on $8–10 billion worth of coated steel imports annually.

China Coated Steel Market: Green Mandates and Export Rebalancing Driving Strategic Shift

China’s coated steel market is transitioning from volume dominance to high-value, low-carbon production, supported by strong regulatory frameworks. The Steel Work Plan (2025–2026) mandates increasing Electric Arc Furnace (EAF) output to 15%, promoting cleaner substrates for advanced coated steel products.

The inclusion of the steel sector in China’s National Emissions Trading Scheme (ETS) is internalizing carbon costs for over 1,500 production sites, accelerating decarbonization. While domestic construction demand has softened, exports have surged, with total steel exports exceeding 110 million tonnes in 2024, particularly to Southeast Asia and the Middle East. Technological advancements such as AI-driven coating optimization are reducing zinc usage by up to 8%, improving efficiency. Additionally, strong demand for magnesium-aluminum-zinc (ZM) coated steel in solar infrastructure is reinforcing China’s leadership in high-performance coated steel solutions.

United States Coated Steel Market: Infrastructure Modernization and Green Reshoring Driving Demand

The United States coated steel market is being reshaped by federal investments and sustainability mandates. Under the Infrastructure Investment and Jobs Act (IIJA), bridge rehabilitation projects are prioritizing galvanized and duplex-coated steel systems to extend asset lifespans.

The ASCE 2025 Report Card highlights that nearly 49.1% of U.S. bridges remain in “fair” condition, driving sustained demand for high-performance coatings. Additionally, the CHIPS Act is boosting demand for chemical-resistant coated steel in semiconductor fabrication facilities. Regulatory requirements under “Build America, Buy America” (BABA) are encouraging domestic production using low-carbon EAF steel. The automotive sector is also contributing, with increased demand for electro-galvanized sheets in the refinish market due to an aging vehicle fleet. Supply chain volatility in coating resins is further pushing innovation toward bio-based and powder coatings, reinforcing long-term sustainability trends.

Germany Coated Steel Market: Hydrogen-Based Steel and Circular Economy Leadership Driving Innovation

Germany is at the forefront of green coated steel production, driven by ambitious decarbonization goals and advanced manufacturing technologies. The country’s green steel market reached $33 billion in 2024 and is expected to double by 2035, supported by hydrogen-based direct reduction (DR) technologies.

Innovation is centered on sustainability and traceability. Germany is pioneering Digital Product Passports (DPP), enabling full lifecycle transparency for coated steel products. The dominance of Electric Arc Furnace (EAF) production supports circular economy objectives by maximizing scrap recycling. Additionally, German manufacturers are leading the shift toward PFAS-free and isocyanate-free coatings, anticipating stricter REACH 2.0 regulations. Investments in electric IR-curing systems are reducing energy consumption in coating processes by up to 25%, reinforcing Germany’s leadership in sustainable coated steel technologies.

Brazil Coated Steel Market: Agribusiness Demand and Industrial Consolidation Driving Growth

Brazil’s coated steel market is expanding through strong demand from agribusiness and strategic industrial investments. The ArcelorMittal Vega expansion (640,000 tonnes) has strengthened capacity for galvanized steel production, particularly for automotive and appliance applications.

Agriculture is a major growth driver, with a 15% increase in demand for zinc-aluminum coated steel used in grain storage silos and logistics systems. M&A activity, including ArcelorMittal’s acquisition of Tuper, is consolidating market capacity and improving supply chain efficiency. Additionally, Brazil’s $19.5 billion decarbonization investment plan (2024–2029) is driving adoption of low-emission steel production technologies. Regulatory developments such as the “Fuel of the Future” law are also boosting demand for epoxy-coated steel in ethanol and biodiesel infrastructure, positioning Brazil as a key regional player.

Vietnam Coated Steel Market: Export Growth and “China Plus One” Strategy Driving Expansion

Vietnam is rapidly emerging as a global hub for coated steel production, driven by export growth and supply chain diversification. The country achieved 5.0 million tonnes of coated steel consumption and exports in 2024, marking a 31% year-on-year increase despite global market challenges.

Capacity expansion across Southeast Asia is projected to reach 90.8 million tonnes by 2026, supported by investments under the “China Plus One” strategy. Vietnam is also strengthening its domestic industry through anti-dumping measures on imported hot-rolled coil (HRC), ensuring supply chain stability. Growth in solar energy and infrastructure projects is increasing demand for aluminum-zinc coated steel, while upgrades to high-spec organic coatings are enabling access to premium U.S. and EU markets. Legal reforms in the real estate sector are expected to further boost demand for coated steel in residential construction.

Coated Steel Market Report Scope

Coated Steel Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$39.4 Billion

|

|

Market Size (2032)

|

$58.5 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Coating Process (Hot-Dipped Galvanized (HDG), Electro-Galvanized (EG), Galvannealed (GA), Aluminized Steel, Advanced Alloy Coatings, Galvalume, Zinc-Aluminum-Magnesium (Zn-Al-Mg), Color-Coated), By Resin (Polyester (PE), High-Durability Polyester (HDP), Siliconized Modified Polyester (SMP), Polyvinylidene Fluoride (PVDF), Plastisol (PVC)), By Application Area (Building and Construction, Automotive Components, Appliances and Consumer Electronics, Infrastructure and Energy, Pipe and Tubular), By Functional Performance (High-Reflectivity, Antimicrobial and Food-Grade, Anti-Fingerprint)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ArcelorMittal S.A., Nippon Steel Corporation, POSCO Holdings Inc., China Baowu Steel Group Corp., Ltd., Tata Steel Limited, JSW Steel Limited, BlueScope Steel Limited, Thyssenkrupp AG, United States Steel Corporation, Nucor Corporation, Ternium S.A., JFE Holdings, Inc., Voestalpine AG, SSAB AB, Hesteel Group Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coated Steel Market Segmentation

By Coating Process

- Hot-Dipped Galvanized (HDG)

- Electro-Galvanized (EG)

- Galvannealed (GA)

- Aluminized Steel

- Advanced Alloy Coatings

- Galvalume

- Zinc-Aluminum-Magnesium (Zn-Al-Mg)

- Color-Coated

By Resin

- Polyester (PE)

- High-Durability Polyester (HDP)

- Siliconized Modified Polyester (SMP)

- Polyvinylidene Fluoride (PVDF)

- Plastisol (PVC)

By Application Area

- Building and Construction

- Automotive Components

- Appliances and Consumer Electronics

- Infrastructure and Energy

- Pipe and Tubular

By Functional Performance

- High-Reflectivity

- Antimicrobial and Food-Grade

- Anti-Fingerprint

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Coated Steel Market

- ArcelorMittal S.A.

- Nippon Steel Corporation

- POSCO Holdings Inc.

- China Baowu Steel Group Corp., Ltd.

- Tata Steel Limited

- JSW Steel Limited

- BlueScope Steel Limited

- Thyssenkrupp AG

- United States Steel Corporation

- Nucor Corporation

- Ternium S.A.

- JFE Holdings, Inc.

- Voestalpine AG

- SSAB AB

- Hesteel Group Co., Ltd.

*- List not Exhaustive